How to Reset Your Budget After Overspending: A Step-by-Step Recovery Plan

Budget reset addresses overspending-caused financial disruption through systematic spending realignment with income. This process involves four core components:…

Expert insights, data-driven guides, and actionable advice.

Financial anxiety transforms budgeting from practical task to emotional threat. Learn anxiety-adapted budgeting: three numbers only, time-boxed engagement, and the exposure ladder.

Budget reset addresses overspending-caused financial disruption through systematic spending realignment with income. This process involves four core components: immediate spending freeze to prevent further damage, comprehensive assessment of overspending extent and triggers, strategic expense prioritization when resources fall short, and behavioral modification to prevent relapse into previous spending patterns. Unlike creating a new budget from…

Short-term goals have deadlines measured in weeks or months. Learn sinking funds, parallel vs sequential funding, and the priority stack that protects essential spending.

Starting a budget with no savings means starting honestly. Learn the vulnerability multiplier, the first $500 target, and how to build micro-savings from zero.

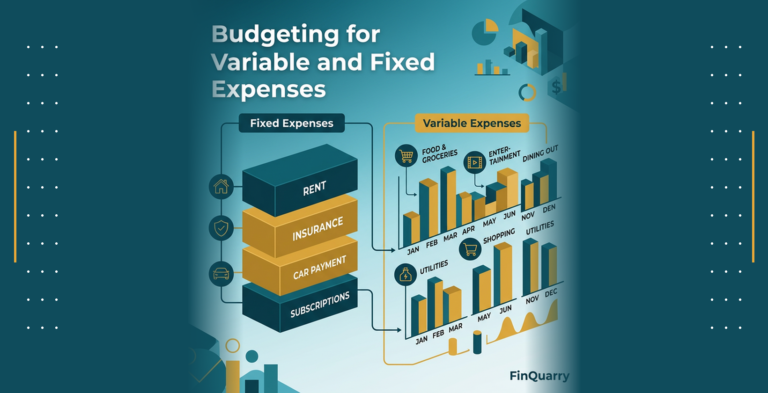

Managing money effectively requires understanding how different expense types behave. Some costs stay constant regardless of activity levels. Others fluctuate based on usage, sales volume, or personal choices. Variable expenses change month-to-month based on consumption, business activity, or lifestyle decisions. Fixed expenses remain relatively stable over specific time periods regardless of usage patterns. Budgeting for…

Fixed income means expenses can rise but income stays the same. Learn the three-layer architecture, program enrollment audits, and healthcare cost management strategies.

Living paycheck to paycheck means finishing each pay period with little or no money left over. This pattern affects many households regardless of income level. Traditional monthly budgeting often fails in this situation. Bills hit before money arrives. Expenses rarely split evenly across 30 days. Paycheck-based budgeting works differently. It organizes spending around actual pay…

Budgeting guilt punishes responsible budgeters for being responsible. Learn the three guilt mechanisms and structural interventions that make spending feel permitted.

Variable expenses are the default, not the exception. Learn rolling averages, category buffers, and the flex budget framework for financial stability on shifting ground.

A household budget manages shared resources across multiple people with competing priorities. Learn the three-layer architecture and why individual autonomy allocations matter.

Explore our most recent guides and insights on this topic.

Budget reset addresses overspending-caused financial disruption through systematic spending realignment with income. This process involves four core components:…

Managing money effectively requires understanding how different expense types behave. Some costs stay constant regardless of activity levels.…

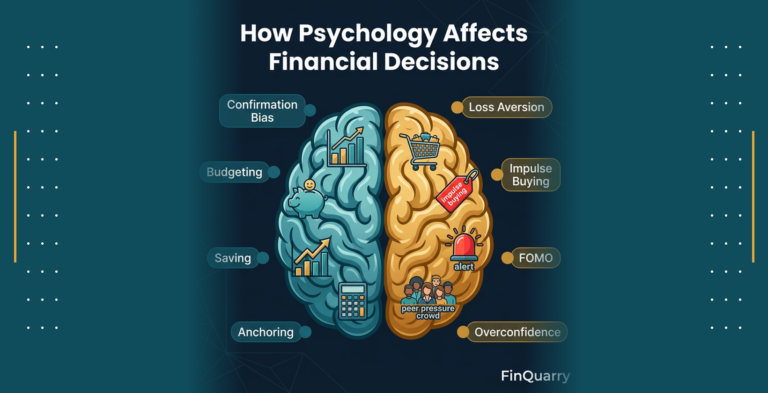

Psychology affects financial decisions by introducing cognitive biases, emotional responses, and mental shortcuts that systematically override rational analysis.…

Money psychology refers to the study of how psychological factors—including emotions, cognitive biases, personality traits, and mental models—influence…

Join 25,000+ readers for expert insights delivered weekly.