Table of Contents

Contents are generated from article headings.

Living paycheck to paycheck means finishing each pay period with little or no money left over. This pattern affects many households regardless of income level. Traditional monthly budgeting often fails in this situation. Bills hit before money arrives. Expenses rarely split evenly across 30 days. Paycheck-based budgeting works differently. It organizes spending around actual pay dates instead of calendar months. This approach generally reduces overdrafts and late fees.

Quick Steps:

- Track all income sources and expenses first

- Allocate each paycheck to specific bills

- Build a small buffer between paychecks

- Automate payments right after payday

- Align bill due dates with pay cycles

- Review spending weekly, not monthly

These steps describe general methods people use when cash flow is tight. Results vary based on income stability, expenses, and personal circumstances.

This guide explains how paycheck-first budgeting works and what it tends to improve over time.

Understanding Paycheck-to-Paycheck Budgeting

Paycheck-to-paycheck budgeting assigns expenses to specific paychecks rather than monthly totals. This method matches spending plans to actual cash availability.

Monthly budgeting assumes steady cash throughout 30 days. Paycheck budgeting acknowledges that money arrives in chunks on specific dates.

The difference matters when bills are due between paychecks. Traditional budgets ignore timing gaps. Paycheck budgets solve timing problems directly.

Why timing matters: Rent might be due on the 1st, but payday might be the 15th. Monthly budgets don’t address this gap.

Paycheck-to-paycheck budgeting generally helps prevent overdrafts and late fees. It improves financial awareness by tracking actual cash flow patterns.

This approach does not eliminate financial constraints. It organizes spending within those constraints more effectively.

Primary benefit: Better alignment between when money arrives and when bills must be paid.

People living paycheck to paycheck often face stress from timing mismatches. Organizing by pay periods tends to reduce this specific stress.

What This Method Does Not Do

Paycheck budgeting does not increase total income or eliminate existing debt. It organizes current resources, not expands them.

This method will not guarantee savings or financial freedom. It may improve spending control when applied consistently over time.

Results depend heavily on expense levels relative to income. If expenses exceed income, budgeting alone cannot resolve insolvency.

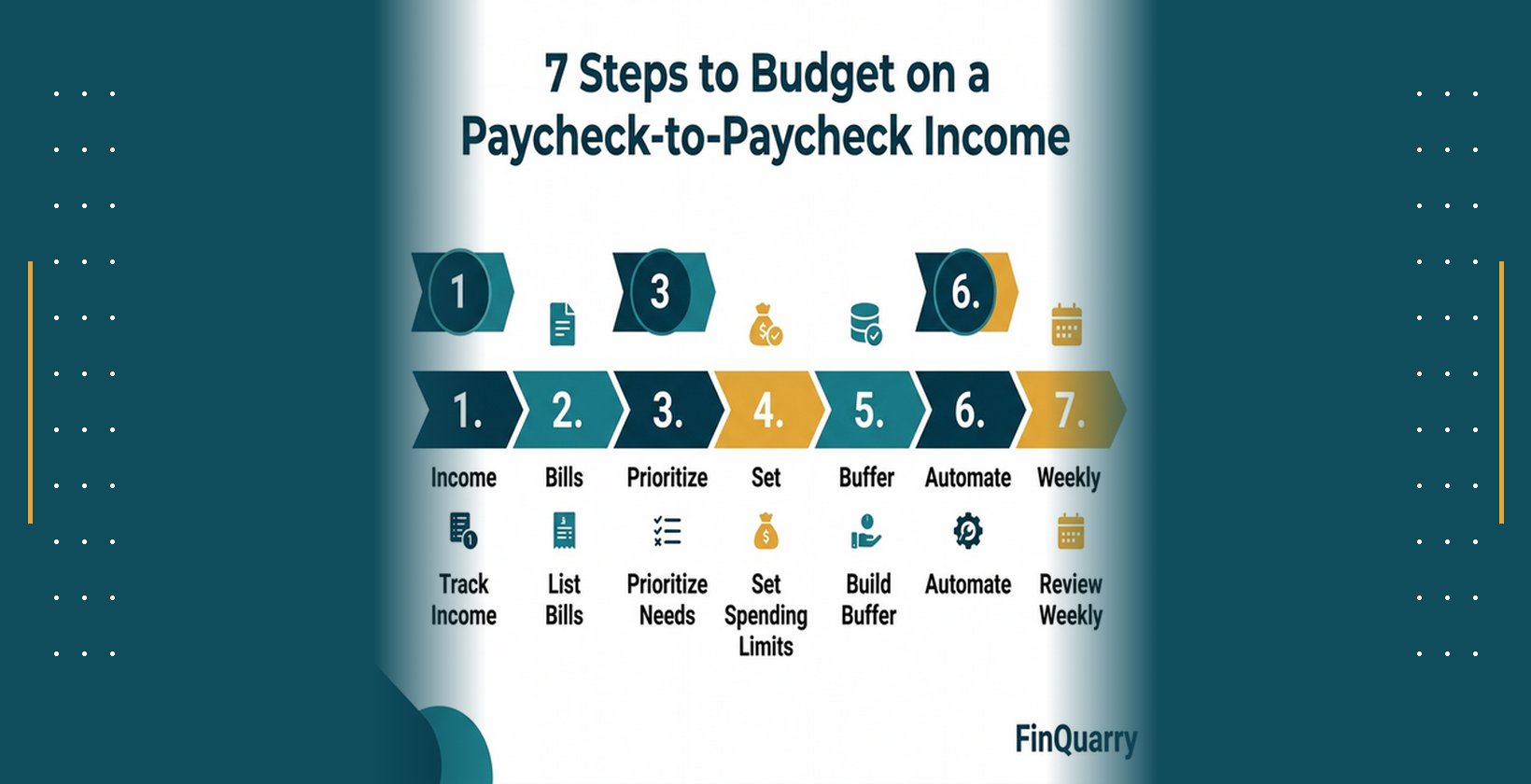

7 Practical, Step-by-Step Approach to Budgeting on a Paycheck-to-Paycheck Income

This step-by-step framework is designed for people whose income and expenses do not align neatly within a monthly budget cycle. Instead of planning around a calendar month, it focuses on managing money based on when paychecks actually arrive.

The steps below emphasize cash-flow visibility, bill timing, and small financial buffers rather than aggressive saving or long-term investing. In practice, many people adapt or reorder these steps depending on income stability, household size, and fixed expenses.

Because financial situations vary widely, these steps are best viewed as a practical reference model rather than a strict checklist. The goal is to reduce short-term financial stress while improving day-to-day money management.

Assess Your Income and Expenses First

Understanding current cash flow comes before any budgeting method works. Track where all money comes from and goes to first.

This assessment reveals actual spending patterns. Many people underestimate discretionary expenses by 20-30% without tracking.

List All Sources of Income

Regular paychecks form the foundation. Include the exact amount after taxes and deductions, not gross pay.

Side income from gigs or freelance work counts too. Track this separately since it often arrives irregularly.

Bonuses, tax refunds, or gift money should be noted. These windfalls require different planning than regular paychecks.

Child support, alimony, or government assistance are income sources. Include them if they arrive predictably each month.

Key point: Use take-home amounts only. Gross income creates unrealistic budgets since that money never reaches your account.

Track Fixed and Variable Expenses

Fixed expenses stay the same each month. Rent, car payments, insurance premiums, and loan minimums fall here.

Variable expenses change monthly. Groceries, gas, utilities, and discretionary spending fluctuate based on usage and choices.

Essential expenses support basic survival. Housing, food, utilities, transportation, and healthcare qualify as essentials under most circumstances.

Non-essential expenses include entertainment, dining out, subscriptions, and hobby costs. These become optional during tight financial periods.

Tracking method: Review 2-3 months of bank statements to establish baseline spending patterns across categories.

Categorize & Prioritize

Priority one covers housing, minimum utilities, basic food, and essential transportation. These prevent homelessness, hunger, or job loss.

Priority two includes full utility bills, insurance payments, and minimum debt payments. Missing these creates fees or coverage gaps.

Priority three covers quality-of-life items like phone plans, internet, and modest discretionary spending for mental health.

Everything else falls into priority four. This category gets funded only after priorities one through three are covered.

Critical rule: Never cut priority one expenses to fund priority three or four items.

Expense tracking improves financial awareness by showing actual spending versus perceived spending. This awareness enables better allocation decisions.

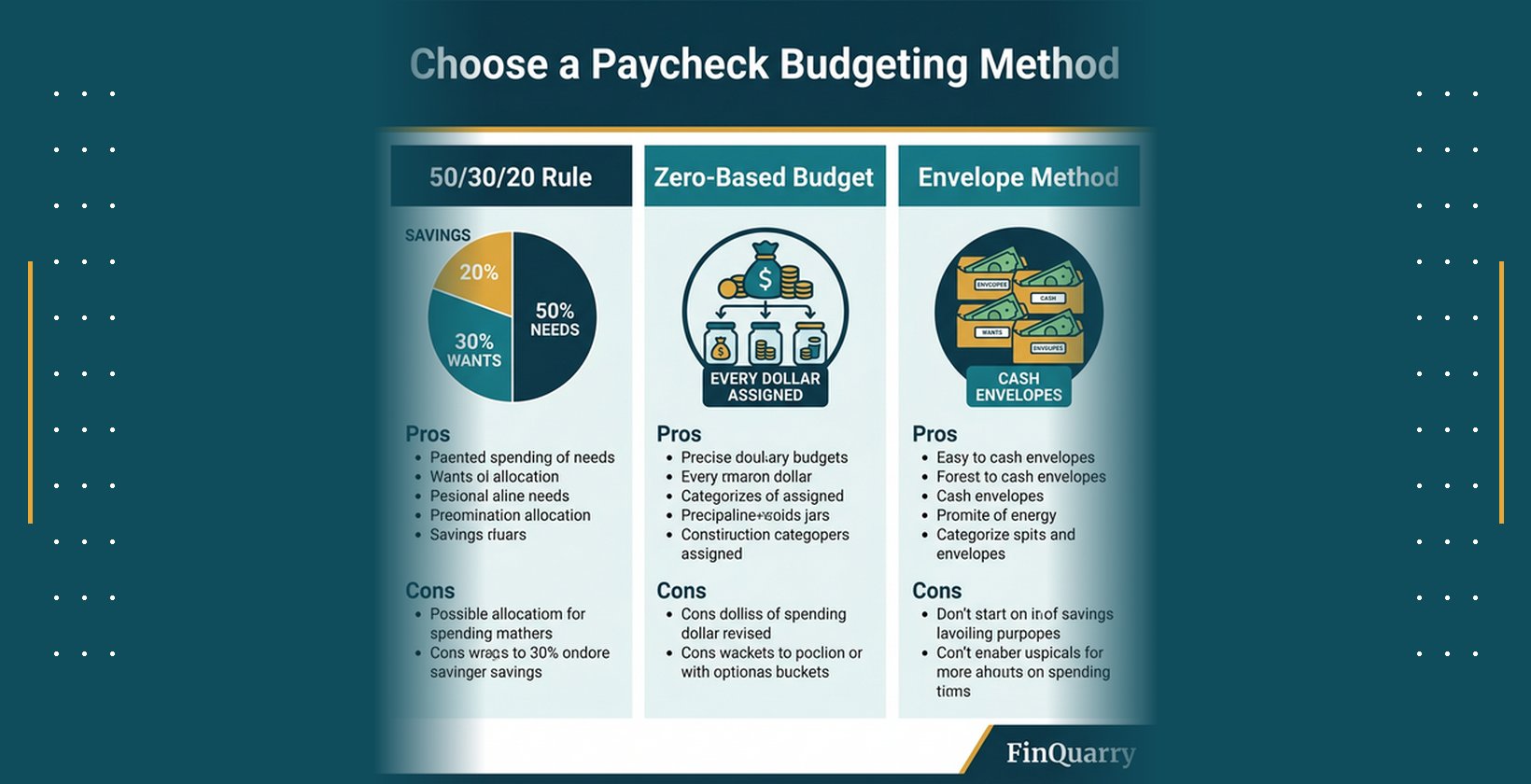

Choose a Paycheck Budgeting Method

Several frameworks help organize spending by paycheck. Each works differently based on pay frequency and personal preferences.

Paycheck-First Budgeting

This method assigns specific bills to specific paychecks. First paycheck covers rent and utilities. Second paycheck handles groceries and gas.

Match bill due dates to paychecks that arrive just before. This timing prevents overdrafts from bills hitting before money arrives.

Split bills evenly if possible. Two paychecks per month means each covers roughly half the monthly obligations.

Execution: Write down paycheck dates. List all bill due dates. Assign each bill to the nearest prior paycheck.

Leftover money after essentials goes toward buffer building first. After buffer exists, allocate to discretionary or debt reduction.

This framework tends to reduce late fees by ensuring money exists when bills are due.

Weekly, Biweekly, and Monthly Paycheck Variations

Weekly paychecks require splitting monthly bills into four segments. Rent becomes four payments mentally, even if paid once.

Biweekly pay creates two paychecks most months. Two months yearly have three paychecks. Those extra paychecks need separate plans.

Monthly paychecks require covering all bills from one deposit. This demands tighter discipline since mistakes last 30 days.

Biweekly advantage: Bills split more naturally into two chunks. Most people find this easiest to manage practically.

Irregular pay from freelancing or hourly work needs flexible allocation. Build buffer first, then cover essentials from any paycheck.

Envelope Method for Discipline

Physical envelopes hold cash for specific categories. Grocery envelope gets $200. Gas envelope gets $100. Spending stops when empty.

Digital versions use separate bank accounts or budgeting apps. Each category becomes a virtual envelope with assigned money.

This method prevents overspending by creating hard limits. When an envelope empties, that category is done until next paycheck.

Best use case: People who struggle with impulse spending or credit card overuse benefit most from envelope systems.

Zero-based budgeting assigns every dollar a job before spending begins. This combines well with envelope methods for maximum control.

Build a Small Emergency Buffer

A buffer creates space between paychecks. Even $100 reduces financial stress by covering small unexpected expenses.

Start with micro-savings targets. Saving $500 takes months. Saving $100 happens faster and provides immediate breathing room.

Micro-Savings per Paycheck

Set aside $10-$25 from each paycheck initially. This amount is small enough to manage while building savings habit.

Automate the transfer immediately after payday. Manual saving often fails because discretionary spending happens first.

Target: Reach $100-$250 within 2-3 months. This cushion covers minor car repairs or medical copays without credit cards.

Once first buffer exists, increase savings slightly. Add $5-$10 more per paycheck until buffer reaches $500.

Emergency buffers protect against unexpected expenses. They reduce reliance on high-cost borrowing when small financial shocks occur.

Prioritize Essentials First

Buffer building happens after essentials are covered. Never skip rent or utilities to save money faster.

Savings matter, but not at the expense of housing stability or utility shutoffs. Build buffers from leftover money only.

Sequencing rule: Essentials → Minimum debt payments → Buffer → Additional savings → Discretionary.

This order prevents creating new problems while solving old ones. Savings that cause late fees cost more than they help.

Small buffers tend to reduce overall financial stress more than larger savings that take years to build.

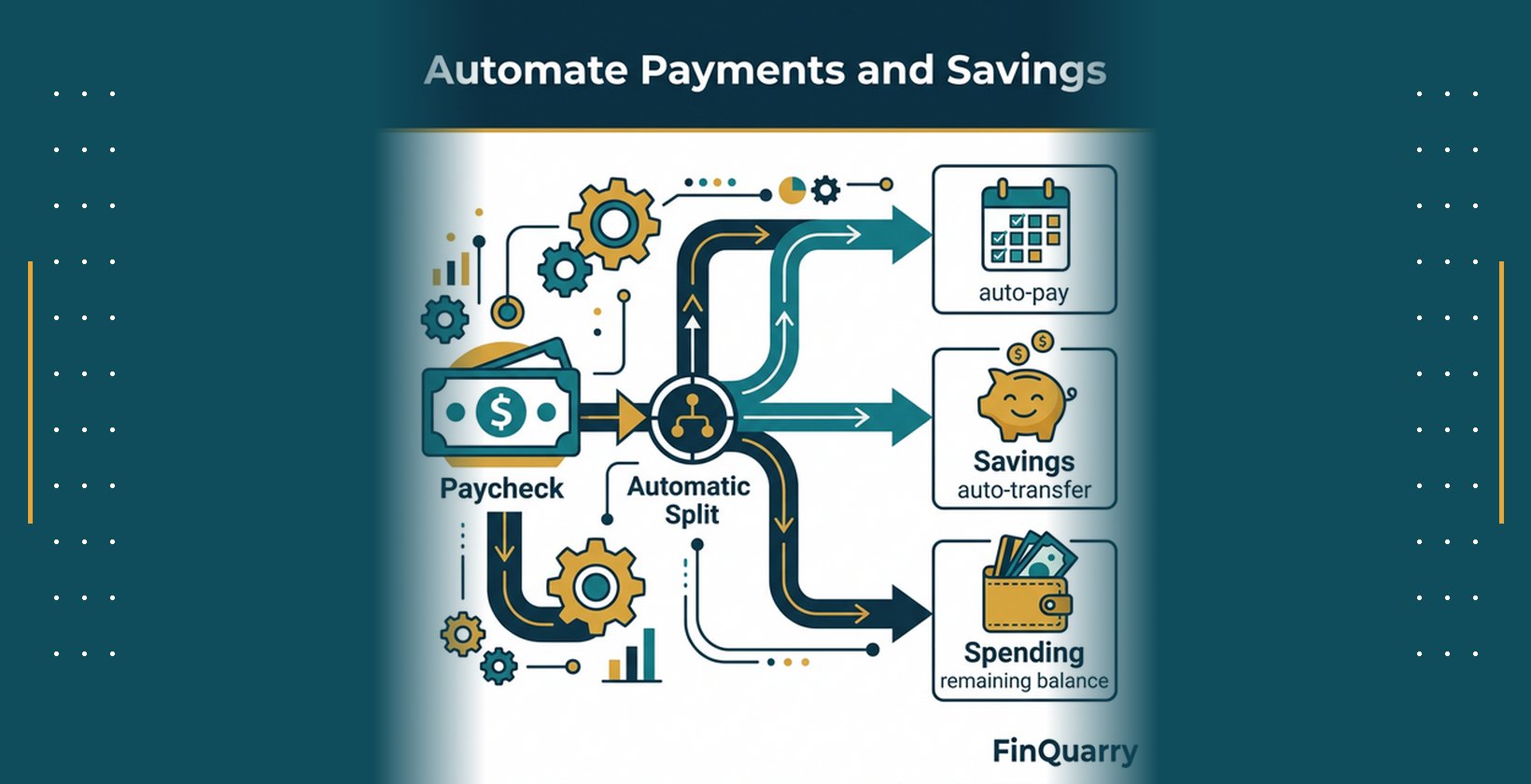

Automate Payments and Savings

Automation removes human error from bill paying. Late fees often result from forgetting, not from lacking money.

Automated Bill Payments

Set up automatic payments for rent, utilities, insurance, and loan minimums. Schedule them 1-2 days after payday.

This timing ensures money exists in the account when bills process. Early automation before payday causes overdrafts.

Safety rule: Never automate bills before confirming paycheck deposit dates. Check with employer for exact deposit timing.

Review automated payments quarterly. Catch billing errors, price increases, or unnecessary subscriptions before they drain accounts.

Automation reduces missed payments. This improves credit scores over time since payment history affects 35% of FICO scores.

Automated Savings Transfers

Schedule automatic transfers to savings immediately after payday. Treat savings like a bill that must be paid.

Start with $10-$20 per paycheck if that’s all budget allows. Consistency matters more than amount initially.

Transfer timing: Same day as paycheck deposit works best. Money moves before temptation to spend it arrives.

Automated transfers build buffers faster than manual saving. People tend to spend money they see sitting in checking accounts.

Apps & Tools

Budgeting apps like YNAB, Goodbudget, or EveryDollar offer paycheck-based planning features. Most include automation and tracking.

Free options include Mint or bank-provided budgeting tools. These track spending automatically by linking to accounts.

Selection criteria: Choose apps that support pay-period budgeting, not just monthly. Match tool features to pay frequency.

Spreadsheets work for people who prefer manual control. Many free paycheck budget templates exist online for download.

Apps generally improve expense tracking. They show spending patterns that are hard to see manually.

Align Bills and Due Dates With Paychecks

Bill due dates are negotiable. Most companies allow due date changes upon request.

Move Due Dates

Call utility companies, lenders, and service providers. Request due date changes to match paycheck schedules.

Most agree immediately. They prefer payments on specific dates over late or missed payments.

Optimal timing: Schedule bills 2-5 days after payday. This provides buffer for deposit timing variations.

Group similar bills together. Pay all utilities on the same date to simplify tracking and reduce mental load.

Due date alignment smooths cash flow by eliminating gaps between money arrival and bill obligations.

Split Large Payments

Some expenses allow splitting. Annual insurance might split into monthly or quarterly payments.

Ask about payment plans for large irregular expenses. Many providers offer installment options without interest.

Cost consideration: Splitting sometimes includes small fees. Calculate if convenience outweighs the extra cost.

Property taxes, HOA fees, or annual memberships often allow payment plans. Request these in advance, not when bills arrive.

Splitting large payments prevents cash flow shocks that derail monthly budgets.

Practical Budgeting Tools and Templates

Templates and calculators reduce setup time. Pre-built structures help start budgeting faster than creating systems from scratch.

Paycheck Budget Template

Excel templates divide income by paycheck and assign expenses accordingly. Most include category suggestions and formulas.

Printable PDF worksheets work without computers. Fill these out manually each pay period.

Template components: Income section by paycheck, fixed expenses list, variable expenses tracker, buffer progress chart.

Free templates exist on budgeting websites and financial education platforms. Download several and test which format feels intuitive.

Paycheck Calculator

Online calculators divide monthly expenses by pay frequency automatically. Input bills and paychecks, receive allocation suggestions.

These tools show dollar amounts per paycheck after essential expenses. Remaining money becomes visible for budgeting decisions.

Limitation: Calculators suggest starting points, not personalized financial advice. Adjust outputs based on actual spending patterns.

Recommended Apps

YNAB (You Need A Budget) supports paycheck-to-paycheck budgeting explicitly. It costs $14.99 monthly after free trial.

Goodbudget uses envelope method digitally. Free version allows 10 envelopes, which often suffices for basic budgeting.

EveryDollar offers free basic features. Premium version costs $79.99 yearly but adds bank linking and tracking automation.

App selection: Try free versions first. Upgrade only if features genuinely improve budgeting consistency.

Best app for paycheck-to-paycheck budgeting depends on pay frequency and preferred tracking method. No single tool fits everyone.

Adjusting Budget for Variable or Extra Paychecks

Pay schedules sometimes create irregular patterns. Two months yearly typically include three paychecks for biweekly earners.

Three-Paycheck Months

Extra paychecks aren’t truly extra money. They result from calendar math, not income increases.

Use third paychecks strategically. Options include buffer building, debt reduction, or modest quality-of-life improvements.

Common strategy: Split third paycheck three ways—one-third to buffer, one-third to debt, one-third to discretionary spending.

Avoid treating extra paychecks as windfalls. This money is part of annual income, just distributed unevenly.

Planning third-paycheck usage in advance prevents impulse spending that eliminates the opportunity.

Irregular Income Planning

Freelancers and hourly workers face unpredictable paychecks. Build larger buffers first to smooth income volatility.

Use lowest monthly income as baseline budget. Higher-earning months fund buffer and cover income gaps later.

Baseline method: Review 6-12 months of income. Budget using the lowest monthly amount earned during that period.

Irregular income requires larger emergency buffers. Target 1-2 months of expenses instead of $500 for predictable income.

Flexible allocation methods work better than rigid paycheck assignments. Prioritize essentials first, allocate rest based on income received.

Avoid Common Budgeting Mistakes

Budget failures follow predictable patterns. Recognizing these patterns prevents repeating them.

Not Tracking Expenses

Budgets fail when spending goes unmonitored. Small purchases add up invisibly without tracking systems.

Track everything for at least 30 days. This reveals actual spending versus estimated spending.

Common discovery: Most people underestimate discretionary spending by $200-$400 monthly when they finally track it.

Ignoring Small Discretionary Spending

Coffee runs, vending machines, and impulse buys seem insignificant. They accumulate to hundreds monthly without attention.

Small spending creates budget leaks. These leaks prevent buffer building and cause cash shortfalls before payday.

Fix: Track small spending specifically for one week. Total daily $5-$10 purchases to see weekly impact.

No Buffer

Operating without any buffer means every small surprise becomes a crisis. Car repairs require high-cost credit cards.

Lack of buffers increases financial stress significantly. Stress impairs decision-making, creating more financial problems.

Priority: Build even $100 buffer before other financial goals. This cushion protects against overdraft fees and payday loans.

Relying on High-Cost Credit

Payday loans, cash advances, and high-interest credit cards increase future expenses. This creates downward financial spirals.

Borrowing at 300-400% APR costs more than the original emergency. Future paychecks must cover both old and new expenses.

Alternative: Small buffers eliminate most need for emergency borrowing. Focus effort on buffer building before debt reduction.

High-cost borrowing increases expense burdens. This makes escaping paycheck-to-paycheck cycles significantly harder over time.

Review, Monitor, and Iterate

Budgets need regular adjustment. Life circumstances, prices, and income change frequently.

Weekly Check-Ins

Review spending midweek to catch problems early. Small overspending corrects more easily than end-of-month discoveries.

Check if current week’s spending matches budget allocation. Adjust remaining week if necessary.

Weekly habit: Spend 10-15 minutes reviewing transactions every Wednesday or Thursday.

Weekly reviews enhance budget discipline by maintaining constant awareness of spending patterns.

Monthly Reviews

Compare actual spending to planned budget monthly. Identify categories that consistently exceed allocations.

Look for patterns across 3-4 months. One-time spikes differ from ongoing overspending problems.

Monthly action: Adjust budget allocations for categories that regularly exceed limits. Make budgets realistic, not aspirational.

Monthly reviews tend to improve financial awareness. They reveal slow expense increases before they create major problems.

Adapt to Life Changes

Income changes, rent increases, new bills, or life events require budget updates. Outdated budgets fail quickly.

Recalculate entire budget when major expenses change. Don’t just adjust one category while ignoring ripple effects.

Change triggers: Job change, move, new debt, insurance changes, family size changes all require full budget reviews.

Flexible budgets that adapt to reality work better than rigid systems that ignore changing circumstances.

Summary & Next Steps

Paycheck-to-paycheck budgeting organizes spending by actual pay dates instead of monthly totals. This alignment generally reduces overdrafts and late fees.

Core steps include tracking income and expenses, allocating each paycheck to specific bills, building small buffers, automating payments, and aligning due dates with paychecks.

Starting point: Track spending for 30 days first. Understanding current patterns enables effective budget creation.

Begin with one or two changes. Add automation or move one due date. Build gradually rather than overhauling everything immediately.

Small consistent improvements tend to produce better results than dramatic changes that prove unsustainable.

Paycheck budgeting does not guarantee wealth or eliminate financial constraints. It improves spending control within existing limitations when applied consistently over time.

Results vary based on income stability, expense levels, and personal discipline. Some situations require income increases or expense reductions beyond budgeting alone.

Realistic expectation: Better cash flow management, reduced fees, and modest buffer building over 3-6 months.

Financial stability develops gradually through consistent application of budgeting principles. Quick fixes rarely produce lasting improvements.

Start simple. Track, allocate, automate, and review. Adjust based on what actually works for your specific situation and pay schedule.