Table of Contents

Contents are generated from article headings.

A zero-savings budget is a financial plan that prioritizes building the first emergency buffer while managing living expenses on a paycheck-to-paycheck basis — where no financial cushion exists to absorb unexpected costs. Having no savings changes the budget’s fundamental function from allocation optimization to financial vulnerability reduction.

The standard advice — “save 3–6 months of expenses” — describes the destination without acknowledging the starting point. A person with $0 in savings needs a different framework: one that builds the smallest viable buffer through micro-contributions and structural reallocation rather than aspirational targets that collapse under their own weight.

This content discusses budgeting strategies for individuals with no savings using financial planning principles and behavioral economics. Financial products, assistance programs, and economic conditions vary by jurisdiction. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Why Zero Savings Changes Everything

The Vulnerability Multiplier

A $400 car repair for a person with an emergency fund is an inconvenience — the fund absorbs the cost and the monthly budget continues. The same $400 repair for a person with no savings may require a credit card charge at 22% APR, creating a new $25/month minimum payment that permanently reduces budget capacity. The absence of savings does not just leave a gap — it creates a cycle where small problems generate ongoing costs.

According to Federal Reserve research, approximately 37% of U.S. adults report they would struggle to cover an unexpected $400 expense without borrowing or selling something. This is not a discipline problem — it is a structural vulnerability that budgeting must address architecturally.

The Psychological Weight

Living without savings produces chronic low-grade financial anxiety — a rational response to genuine vulnerability. This anxiety can become an obstacle to budgeting: engaging with the numbers means engaging with the vulnerability, and avoidance feels safer than awareness. But awareness is the only path to building safety.

The First $500: The Most Important Financial Target

Financial research identifies $500 as the threshold below which emergency savings provide minimal protection and above which the protective effect begins. A $500 buffer covers the most statistically common financial emergencies: minor car repairs ($200–400), medical co-pays ($50–250), essential appliance replacement ($150–400), or temporary income reduction.

Why $500 Before All Other Goals

The $500 buffer takes priority over debt acceleration, retirement saving, and every other financial goal — because without this buffer, every disruption produces new debt, which pushes all goals further away. The buffer breaks the cycle: unexpected expense → credit card → new minimum payment → less income → greater vulnerability → next expense.

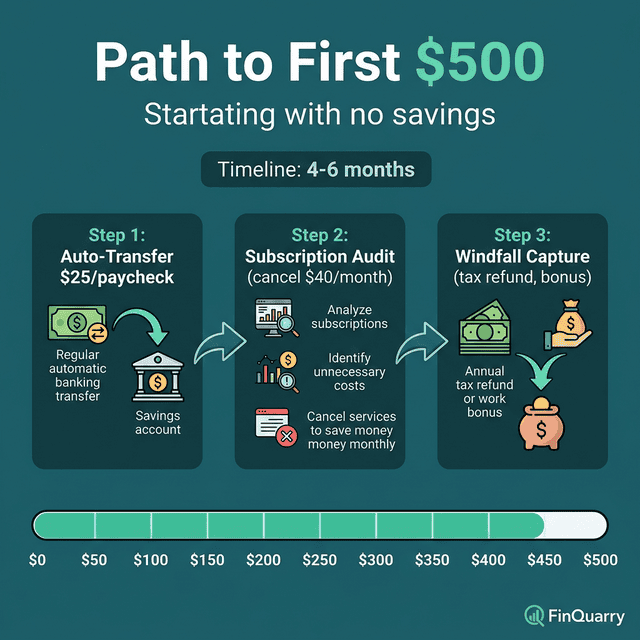

Three Paths From $0 to $500

The $25 automation: Auto-transfer $25 per paycheck to a separate savings account. At bi-weekly pay, this produces $650 in 12 months and reaches $500 in approximately 10 months. The amount is small enough to absorb. The automation removes the decision point that spending psychology will use to redirect the money.

The audit free-up: Conduct the subscription and recurring charge audit used for building a monthly budget. The average household discovers $40–80/month in forgotten or unused charges. Redirecting these produces $480–960/year with zero lifestyle change.

The windfall capture: Tax refunds, birthday money, rebates, work bonuses — all non-recurring income goes directly to savings until $500 is reached. This is strategic deployment of unexpected money toward the highest-return goal: protection from the next unexpected expense.

The Zero-Savings Budget Framework

Step 1: Stabilize the Month

Before savings can begin, the monthly budget must function without credit card reliance. If expenses exceed income, the first priority is closing the deficit. Attempting to save while in deficit creates progress illusion while debt accumulates.

Step 2: Add a Micro-Savings Line Item

Once the month stabilizes, add savings at the smallest viable amount — $10, $15, $25. This appears alongside rent and groceries as a non-negotiable allocation. Small, consistent contributions compound psychologically: each successful transfer builds the identity of “person who saves” — a behavioral change more powerful than financial advice.

Step 3: Protect the Buffer

When savings reach $500, define the boundary: the buffer covers only genuine emergencies (unforeseen, unavoidable, immediately necessary). A sale is not an emergency. A dining opportunity is not an emergency. A car repair preventing commute to work is an emergency.

Defining “Emergency” on Zero Savings

With no savings, the emergency definition must be strict: unforeseen, immediately necessary, and producing material consequences if ignored. Car repair for work transportation qualifies. Medical treatment for acute illness qualifies. Time-limited sales and social pressure purchases do not. Using the buffer for non-emergencies restarts the cycle from zero.

Paycheck-to-Paycheck Budgeting

The most demanding financial management scenario. Calculate the survival floor: minimum cost for housing, food, utilities, transportation, and minimum debt payments. Subtract from take-home. The remainder — even if $50 — divides between micro-savings and minimal discretionary spending.

A person earning $2,800/month with $2,680 in essential costs has $120 available. Directing $25 to savings, $50 to a small debt payment, and $45 to discretionary spending is not comfortable — but it builds $300/year in protection that did not exist before.

Debt vs. Savings: Which Comes First?

When savings are $0 and debt exists, the $500 buffer comes first — even while carrying debt. The mathematical reason: without a buffer, the next emergency creates new debt, which compounds and increases minimums. The buffer breaks this cycle. After $500 is established, surplus funds split between continued savings growth and debt acceleration.

Available Resources

The National Foundation for Credit Counseling provides free financial counseling. Local 211 hotlines connect to community assistance. Employer assistance programs may offer emergency funds. These resources are tools designed specifically for zero-savings situations — using them early produces better outcomes than waiting for crisis.

Written by Marcus Tremblay, Senior Financial Analyst | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry