Table of Contents

Contents are generated from article headings.

A short-term financial goal is a specific savings target with a defined deadline of 1–12 months and a funded monthly contribution path. Short-term goals include emergency fund starts, purchase savings, experience funding, debt payoff milestones, and seasonal expense preparation. The critical distinction: a vague intention (“I want to save for a vacation”) is an aspiration. A funded allocation (“I need $1,200 by June — $300/month for four months”) is a goal that a budget can execute.

Short-term goals matter more to budget sustainability than most financial advice acknowledges. A person who successfully saves $800 for a vacation over four months has proven that their budget can produce tangible outcomes — evidence that transforms budgeting from abstract discipline into concrete capability.

This content discusses short-term financial goal budgeting using financial planning principles. Income levels, savings capacity, and financial product availability vary by jurisdiction. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Common Short-Term Goals

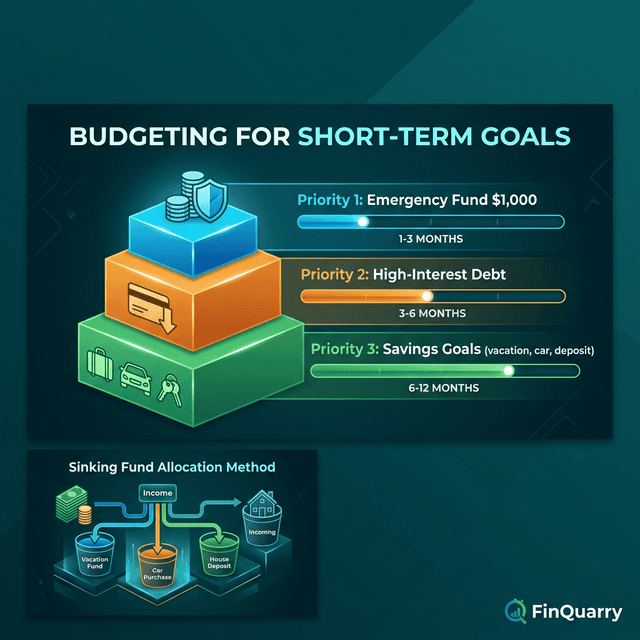

Emergency fund start: The first $500 buffer — the highest-priority short-term goal for anyone without savings.

Debt payoff milestone: Eliminating a specific credit card or reaching a target balance within 6–12 months. Paying off a $2,400 card at $400/month takes 6 months and saves up to $800 in interest compared to minimum payments.

Purchase savings: Security deposits ($1,500–3,000), car down payments ($2,000–5,000), appliance replacements ($400–1,200) — any planned purchase exceeding monthly discretionary capacity.

Experience savings: Vacations ($800–3,000), event tickets ($200–600), wedding attendance ($500–1,500) — time-bound costs requiring advance funding.

Seasonal preparation: Holiday gifts ($500–1,500), back-to-school ($300–800), annual insurance premiums ($600–2,400) — predictable costs requiring monthly pre-funding through annual budget planning.

The Sinking Fund Method

A sinking fund is a dedicated savings sub-account accumulating monthly contributions toward a specific future expense. The mechanism:

Calculate: Total amount needed.

Deadline: When the money is needed.

Divide: Target ÷ months remaining = monthly contribution.

Automate: Transfer on payday.

Protect: Withdraw only for designated purpose.

A $1,200 vacation in 6 months requires $200/month. A $3,600 annual insurance premium pre-funded over 12 months requires $300/month. When the expense arrives, the sinking fund covers it — converting a large disruptive bill into small manageable transfers already absorbed by the regular budget.

Balancing Goals With Budget Obligations

The Priority Stack

Short-term goals are not the budget’s top priority. The funding order: (1) survival needs (housing, food, utilities, minimum debt), (2) financial protection (emergency fund), (3) debt reduction, (4) short-term goals, (5) long-term goals.

A person skipping debt minimums to fund a vacation creates more financial damage than the vacation’s value. Goals occupy position four — after the infrastructure that keeps financial life stable.

The Surplus Allocation Method

Goal funding comes from the budget’s surplus — money remaining after obligations, savings transfers, and minimum discretionary spending. If monthly surplus is $350, goal funding draws from that pool, not from grocery or emergency fund allocations.

Temporary Category Reallocation

For time-sensitive goals, temporarily reduce a lower-priority category. Cutting entertainment from $150 to $75 and redirecting $75 for four months produces $300 of additional goal funding without touching essentials.

The keyword is temporary — the reallocation has a defined end date matching the goal’s completion, then the category reverts to normal allocation.

Managing Multiple Simultaneous Goals

Parallel vs. Sequential Funding

Parallel (splitting surplus across multiple goals): makes progress on everything, completes nothing quickly. Sequential (fully funding one goal before starting the next): reaches targets faster, delays later goals.

If all goals share a deadline, parallel funding is necessary. If deadlines are staggered, sequential funding — starting with the earliest deadline — produces faster psychological wins that build momentum.

The Three-Goal Maximum

Budgets with more than three active sinking funds tend to produce inadequate progress on all of them. Monthly contributions become too small for visible progress, which erodes motivation. Limiting active goals to 2–3 forces prioritization and creates observable progress.

Goal Funding on Tight Budgets

When the budget has minimal surplus, three options exist: extend the timeline (smaller contributions over more months), use micro-contributions ($15/month toward a $360 goal reaches target in 24 months), or allocate supplemental income exclusively to the goal fund.

A person selling unused items ($50–200), doing occasional freelance work ($100–300), or directing overtime pay entirely to the sinking fund accelerates progress without disrupting the monthly operating budget.

Savings vs. Credit for Short-Term Goals

Savings always costs less than credit. A $1,200 vacation funded by a 6-month sinking fund costs $1,200. The same vacation on a credit card at 22% APR with minimum payments costs $1,500–1,600 and takes 12+ months to repay.

The sinking fund approach costs less, creates no new debt, and builds the saving behavior that reduces credit dependency over time.

What If Zero Surplus Means Zero Goal Funding?

If the monthly budget leaves no surplus after essentials, goal funding is not currently possible. The honest response: increase income, reduce an expense category, or defer the goal. A goal that cannot be funded is a reality assessment, not a budget failure. Directing emotional energy toward stabilizing current finances — rather than guilt over unfunded aspirations — produces better long-term outcomes.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry