Table of Contents

Contents are generated from article headings.

An annual budget is a 12-month financial plan that maps all income, expenses, savings targets, and debt obligations across the full calendar year — capturing seasonal spending patterns, irregular costs, and financial goals that monthly budgets structurally cannot see. Annual budgeting shifts financial management from reactive (responding to each month independently) to proactive (preparing for known costs months before they arrive).

Monthly budgets capture approximately 65–70% of actual annual spending — the recurring costs that repeat predictably. The remaining 30–35% consists of irregular, seasonal, and annual expenses that arrive unpredictably within any given month but are entirely predictable when viewed across 12 months.

This content discusses annual budget planning using financial planning frameworks. Tax schedules, seasonal cost patterns, and insurance timelines vary by jurisdiction. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Why Monthly Budgets Alone Are Not Enough

The Irregular Expense Pattern

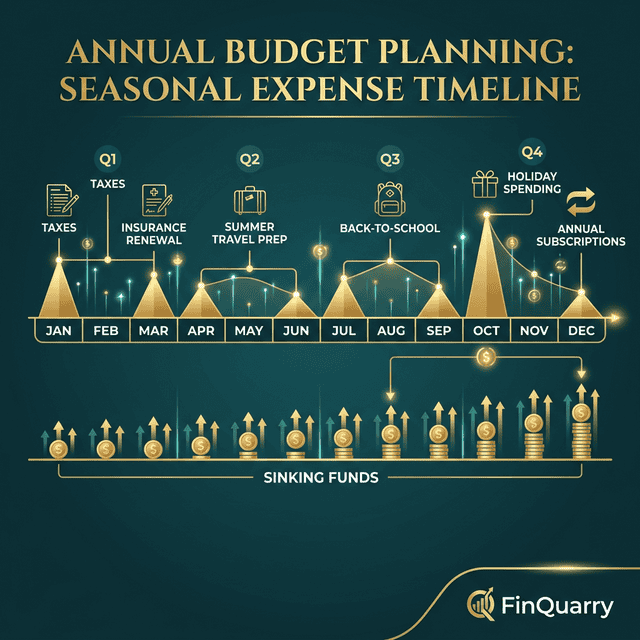

Car registration, veterinary visits, back-to-school costs, holiday gifts, annual subscriptions, tax preparation fees, home maintenance, and medical co-pays are not surprises — they occurred last year and will occur this year. Without annual planning, each arrives as a mid-month disruption that consumes savings, generates debt, or breaks the budget.

A household that spent $4,200 on irregular annual expenses last year — car maintenance ($1,200), holiday gifts ($1,100), medical co-pays ($800), annual subscriptions ($500), home repairs ($600) — will likely spend a similar amount this year. Without annual planning, these costs arrive as 8–12 separate “emergencies.” With annual planning, they are a $350/month sinking fund set-aside that pre-funds every one.

Seasonal Spending Patterns

Energy costs peak in summer (cooling) and winter (heating) — a household paying $120/month in spring may see $220/month in January. Food costs increase during holidays. Clothing purchases spike during back-to-school. These patterns are visible in an annual view but invisible monthly, and invisible patterns are the ones that consistently cause budget failure.

How to Build an Annual Budget

Step 1: Pull 12 Months of Actual Spending Data

Review bank and credit card statements for the past 12 months. Categorize every expense into recurring monthly costs, irregular predictable costs (annual/quarterly), and truly unexpected costs. This data reveals the complete spending landscape.

Step 2: Create the Month-by-Month Expense Calendar

Build a 12-month grid placing every known expense in its expected month: January (annual memberships, gym renewal), March (car registration, insurance), April (tax preparation), August (back-to-school), November–December (holiday spending). This calendar transforms future expenses from abstract anxiety into a specific, funded plan.

Step 3: Calculate Monthly Set-Asides

Total all irregular annual expenses from the 12-month data. Divide by 12. This produces the monthly sinking fund transfer.

If total annual irregular expenses are $3,600, the monthly set-aside is $300. When the $900 car insurance bill arrives in March, the sinking fund holds $900 (three months of $300 contributions). The “surprise” bill is pre-funded and the monthly budget continues undisrupted.

Step 4: Layer in Financial Goals

Annual budgeting integrates multi-month goals: emergency fund targets, debt payoff timelines, vacation savings, major purchase savings, retirement contribution increases. Each goal receives a monthly allocation and target date.

At $200/month, a $2,400 emergency fund target is reached in 12 months. At $400/month toward a $12,000 debt balance, payoff occurs in approximately 30 months. The annual perspective makes goal timelines visible and achievable rather than abstract.

Step 5: Forecast Revenue Across 12 Months

Project income noting anticipated changes: annual raises (typically January or July), bonus months, seasonal income variation. For bi-weekly workers, two months per year have three paychecks — these “bonus” paychecks represent $1,500–2,500 in extra income that monthly budgets miss but annual budgets can strategically allocate to sinking funds, debt acceleration, or savings.

Annual Budget Review Checkpoints

Quarterly Review

Every three months, compare actual spending to plan. Identify categories tracking over budget (adjust or investigate) and categories under budget (reallocate surplus). Quarterly reviews catch small monthly overages before they compound into annual shortfalls.

Mid-Year Reset

At six months, recalibrate the second half based on actual first-half performance. Income may have changed. Expenses may have shifted. Goals may have been revised. A mid-year reset produces a more accurate plan than the original January projection.

Common Annual Budgeting Mistakes

Planning on Unconfirmed Income

An annual budget that includes a projected raise or expected bonus treats future money as present money. Until income materializes, only confirmed income should fund committed allocations. Mark projected income as “tentative” — do not fund essential goals with it.

Setting Aggressive January Targets

January budgets with aggressive savings targets and spending cuts rarely survive Q1 without adjustment. A person who sets a $400/month savings target and achieves it for two months before reverting to $0 saves $800. A person who sets $150/month and sustains it saves $1,800 across the year. Conservative targets that build confidence produce higher annual totals than ambitious targets that collapse.

How Does an Annual Budget Connect to Monthly?

An annual budget creates the master plan. A monthly budget executes one month of that plan. The annual budget determines total allocations for savings, debt, sinking funds, and goals. The monthly budget divides those into operational amounts. Neither works optimally alone.

Is Annual Budgeting Worth It for Simple Finances?

Even simple financial situations — steady income, renter, no debt — contain irregular expenses that monthly budgets miss. Annual insurance, holiday spending, medical costs, car maintenance, and subscription renewals exist in every financial life. The annual view identifies these costs and distributes them across 12 months, preventing the cycle that makes people feel their budget never works.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry