Table of Contents

Contents are generated from article headings.

A variable-expense budget is a financial plan designed to absorb monthly cost fluctuations — utility swings, seasonal price changes, irregular medical costs, and lifecycle events — without requiring a complete budget rebuild each month. Variable expenses represent 30–55% of most household budgets, making fluctuation the operational norm rather than a budgeting exception.

The feeling that “the budget is always wrong” typically indicates a structural design problem rather than spending failure. Budgets built on static monthly assumptions break when costs deviate by even 10–15%. Budgets designed for fluctuation absorb those deviations as expected operational variance.

This content discusses budgeting approaches for variable expenses using financial planning principles and behavioral economics. Expense variability is influenced by jurisdiction, season, household size, and individual circumstances. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Why Expenses Change More Than Expected

Seasonal Variation

Energy costs fluctuate with climate: a household paying $120/month for electricity in spring may see $220 in January (heating) or $195 in August (cooling). Food costs tend to increase 8–12% during November–December holiday periods. These variations are predictable annually but appear as disruptions monthly — which is why budgets without annual planning experience them as failures.

Price Drift

Grocery prices, insurance premiums, fuel, and subscription costs increase gradually — often without conscious registration. A grocery budget accurate two years ago may understate current costs by 15–20% due to accumulated price drift. The Bureau of Labor Statistics tracks these changes through the Consumer Price Index, but individual household inflation often differs from the national average based on spending composition.

Lifecycle Events

Moving, marriage, new child, job change, or becoming a caretaker reshapes the spending structure entirely. A new parent’s budget includes $500–1,200/month in childcare, diapers, and medical visits that did not exist six months earlier. These changes require a budget rebuild, not a category adjustment.

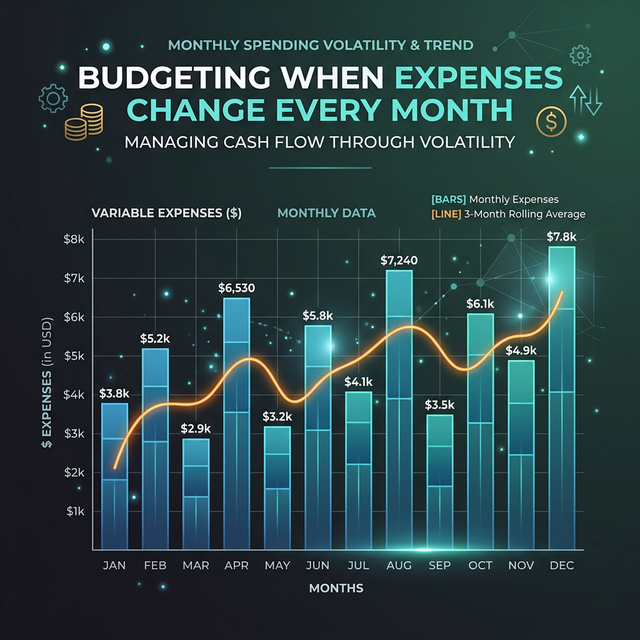

The Rolling Average Method

Instead of budgeting from a single month’s data, the rolling average uses the past 3–6 months as each category’s target. If electric bills over six months were $87, $95, $142, $210, $168, and $112, the rolling average is $136/month.

How Rolling Averages Absorb Spikes

When the bill arrives at $210 (above average by $74), the category exceeds its target. When it arrives at $87 (below average by $49), the category runs under. Over six months, overages and underages approximately cancel — distributing volatility across time rather than concentrating it in one month.

When to Recalculate

Recalculate rolling averages every three months. If actual spending exceeds the rolling average for three consecutive months, the average needs upward adjustment — the cost pattern has shifted permanently. Budget calibration is adjustment, not failure.

The Category Buffer Strategy

For high-volatility categories — medical expenses, car maintenance, home repairs — rolling averages alone are insufficient. These categories need dedicated buffers.

Sizing the Buffer

Review 12 months of spending in the volatile category. Identify the highest single month. The buffer target should cover that peak comfortably. For car maintenance: if the highest month was $800 (new tires), the buffer should accumulate toward $1,000, funded at $80–100/month.

This is functionally a sinking fund: a pool converting unpredictable costs into funded events. An $800 car repair from a funded buffer feels manageable. The same repair from the grocery allocation feels like a crisis — despite identical dollar amounts.

The Three-Zone Flex Budget

Fixed Zone

Rent, loan payments, insurance premiums, subscriptions — costs identical each month. Auto-pay these and remove from active management. This is the budget’s stable foundation.

Predictable Variable Zone

Groceries, utilities, fuel, personal care — costs changing within a known range. Budget these using rolling averages with a 10% buffer. A grocery average of $420 gets budgeted at $462. Treat monthly variation as normal rather than alarming.

Unpredictable Variable Zone

Medical expenses, car repairs, home maintenance, gifts — costs impossible to predict monthly. Fund through dedicated sinking funds. When expenses arrive, they draw from their designated fund rather than competing with the monthly operating budget.

How Do I Stop Feeling Like My Budget Is Always Wrong?

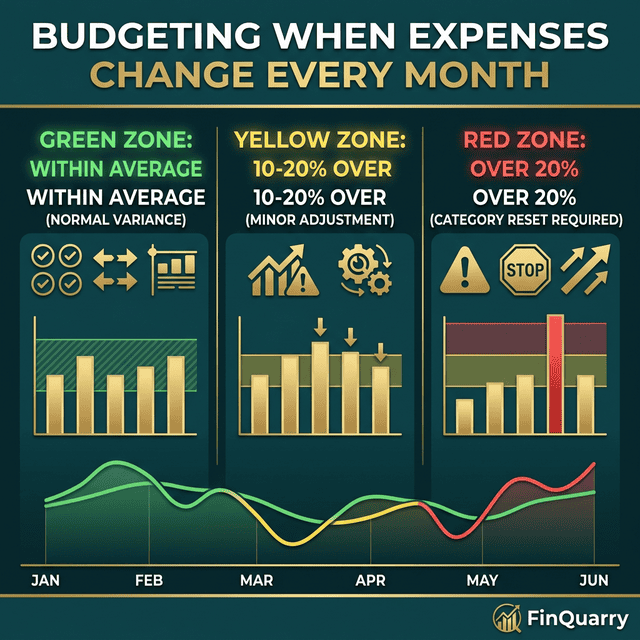

The feeling of constant budget failure is typically an expectations problem. A budget matching reality within 5–10% per category is performing well. Categories that diverge produce diagnostic information: either the allocation needs adjustment or the spending needs examination. The budget that tracks spending patterns over 3+ months becomes progressively more accurate through calibration.

Should I Rebuild Every Month?

Monthly rebuild is unnecessary and signals missing structural architecture. The monthly process should be adjustment: review actuals vs. planned, modify 2–3 categories by small amounts, note upcoming irregular expenses. The core structure (fixed obligations, savings, autonomy) stays constant. Only variable categories flex.

What If My Expenses Are Too Variable for Any Budget?

Extreme variability usually stems from one of two issues: too many granular categories (15 fluctuating categories create chaos — consolidating to 5–7 smooths variation) or income too close to expenses (zero margin means zero absorption capacity). In the first case, simplify. In the second, the structural income problem must be addressed before any budgeting method can function.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry