Table of Contents

Contents are generated from article headings.

A single-income budget is a financial plan designed for households where all money flows through one paycheck — whether by choice (one-earner household), circumstance (single person), or transition (job loss, career change, parental leave). Single-income budgeting operates under the constraint that every financial obligation, savings goal, and discretionary purchase depends on one income stream — making income disruption a complete financial event rather than a partial one.

Single-income households face a unique vulnerability: no secondary income cushion. A dual-income household losing one income retains 40–60% of cash flow. A single-income household losing its income retains 0%. This asymmetry demands larger emergency reserves, tighter essential expense management, and more aggressive structural protection.

This content discusses single-income budgeting using financial planning principles and household finance data. Income levels, cost of living, and available assistance vary by jurisdiction. FinQuarry provides informational content only — this does not constitute personalized financial advice.

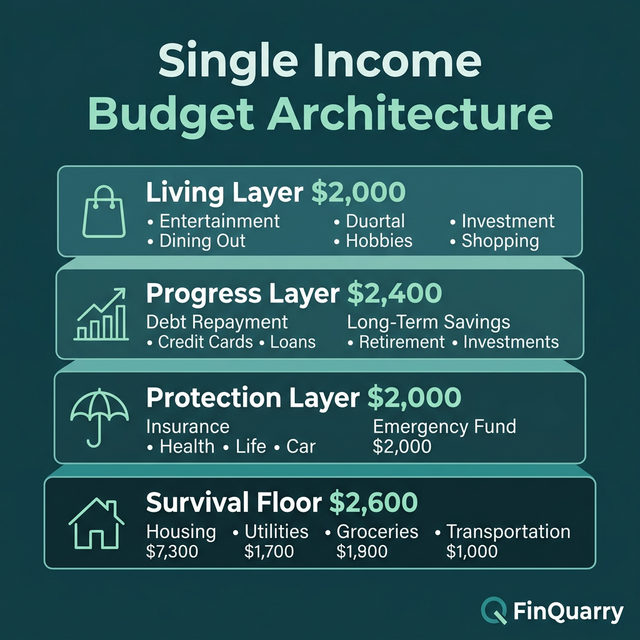

The Four-Layer Single-Income Structure

Layer 1: Survival Floor

The survival floor is the total of all non-negotiable monthly costs: housing, utilities, food (basic), transportation (essential), insurance premiums, and minimum debt payments. For a single-income household earning $3,800/month, a typical survival floor ranges from $2,400–2,900.

Knowing the survival floor precisely — not approximately — is the foundation. This number determines everything: how much margin exists, how large the emergency fund must be, and whether the current income can sustain the household without structural changes.

Layer 2: Financial Protection Buffer

Single-income households need a larger emergency fund than dual-income households. Target: 6–9 months of survival floor expenses. On a $2,600 survival floor, that is $15,600–23,400.

Building this buffer at $200/month takes 6.5–9.75 years at the full target — which is why starting with a $500 initial buffer and then a $2,500 intermediate target provides meaningful protection while the full fund builds over time.

Layer 3: Debt Compression

After survival floor and buffer contributions, direct surplus to debt acceleration. The single-income constraint makes debt particularly dangerous: debt payments reduce already-limited margin, and income disruption makes debt obligations unserviceable.

A person paying $350/month in minimums on $8,000 debt can direct an additional $100/month to the highest-interest balance. At 22% APR, this accelerated payment eliminates the debt 14 months sooner and saves approximately $1,200 in interest.

Layer 4: Living Money

Everything remaining after layers 1–3 is living money — discretionary spending that the person uses without guilt or tracking. On $3,800 income with a $2,600 survival floor, $200 buffer contribution, and $100 debt acceleration, living money is $900/month.

The Single-Income Emergency Protocol

When a single-income household faces income reduction or loss:

Week 1: Reduce to survival floor only. Suspend all non-essential spending, sinking fund contributions, and debt acceleration beyond minimums.

Week 2: Contact creditors and request hardship accommodation. Most offer payment deferrals or reduced minimums during documented income loss.

Week 3: Assess available resources — unemployment benefits, assistance programs, emergency fund, family support.

Ongoing: The emergency fund buys time measured in months. A 6-month buffer on a $2,600 survival floor provides $15,600 of runway — time to find new employment without the crisis decisions that produce long-term financial damage.

How to Increase Single-Income Margin

The Expenses Audit

Review 3 months of actual spending and identify costs that provide low satisfaction relative to their price. Common findings: subscriptions used less than twice monthly ($30–80/month), insurance policies not comparison-shopped in 2+ years (potential $50–150/month savings), and service bundles containing unused components.

The Income Supplement

Irregular supplemental income (freelance work, part-time work, selling unused items) should not be budgeted for regular expenses. Treat supplemental income as acceleration money — directed entirely to emergency buffer, debt payoff, or short-term goals. This prevents the household from becoming dependent on income that may not recur.

Is Single-Income Budgeting Harder?

Single-income budgeting is more constrained — fewer dollars require more deliberate allocation. The reduced margin demands precision that dual-income budgets can absorb through volume. However, single-income budgets are also simpler: one income source, one cash flow timeline, no coordination complexity.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry