Table of Contents

Contents are generated from article headings.

Budget categories are the organizational compartments within a financial plan that group related expenses into trackable, manageable units. Budget categories transform a single overwhelming number (“I spent $4,200 this month”) into actionable intelligence (“Housing consumed $1,400, food cost $520, transportation absorbed $380, and I cannot identify where $340 went”). Without categories, a budget is a total — not a plan.

The Bureau of Labor Statistics Consumer Expenditure Survey identifies the average American household spending breakdown: housing (33%), transportation (17%), food (13%), personal insurance/pensions (12%), healthcare (8%), entertainment (5%), with the remaining 12% distributed across remaining categories. Individual budgets should reflect actual patterns, not averages — but these benchmarks reveal whether any single category is significantly out of proportion.

This content discusses budget categorization using BLS consumer expenditure data and financial planning principles. Individual spending patterns vary by location, household size, and financial circumstances. FinQuarry provides informational content only — this does not constitute personalized financial advice.

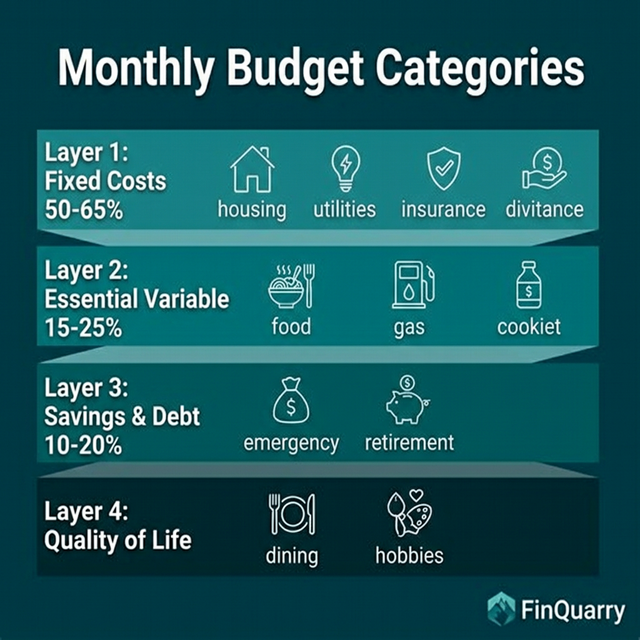

The Four-Layer Category System

Layer 1: Non-Negotiable Fixed Costs

Expenses that cannot be quickly reduced and carry severe consequences for non-payment:

- Housing: Rent/mortgage, property tax, renter’s/homeowner’s insurance ($1,000–2,200/month)

- Utilities: Electric, gas, water, internet ($150–350/month)

- Insurance: Health, auto, life ($200–600/month)

- Minimum debt payments: Student loans, credit cards, auto loan ($150–500/month)

- Transportation (essential): Car payment or transit pass ($100–450/month)

Layer 1 costs typically consume 50–65% of after-tax income. A person earning $4,200/month with $2,700 in Layer 1 costs has 64% committed before any discretionary decision.

Layer 2: Essential Variable Costs

Necessary expenses with variable monthly amounts:

- Groceries: ($300–600/month for a household of 2)

- Gas/transportation variable: ($100–250/month)

- Personal care/household supplies: ($40–100/month)

- Medical co-pays/prescriptions: ($20–150/month)

Layer 2 costs are essential but adjustable — the person eats more economically or drives less. Typical range: 15–25% of income.

Layer 3: Savings and Debt Acceleration

Financial progress categories:

- Emergency fund contributions: ($50–300/month)

- Retirement contributions beyond employer match: ($100–500/month)

- Debt payments above minimums: ($50–300/month)

- Sinking funds for irregular expenses: ($100–300/month)

Layer 3 should consume 10–20% of income. A person directing $0 to Layer 3 is maintaining the current financial position without improving it.

Layer 4: Quality of Life

Discretionary spending that sustains well-being:

- Dining and entertainment: ($100–350/month)

- Hobbies and recreation: ($30–150/month)

- Subscriptions and memberships: ($30–100/month)

- Personal spending money: ($50–200/month)

Layer 4 is not waste. It is the psychological sustainability mechanism that prevents budget burnout. Eliminating Layer 4 creates the deprivation-binge cycle that causes more spending than a funded discretionary allocation.

How Many Categories Should a Budget Have?

The 5–7 Category Sweet Spot

Fewer than 5 categories provides insufficient visibility (“I spent $1,800 on ‘everything else’” — not actionable). More than 12 categories creates tracking fatigue.

Recommended starter categories: Housing + Utilities, Food, Transportation, Debt Payments, Savings, Everything Else. This 6-category structure provides actionable visibility with minimal categorization overhead.

Common Categorization Mistakes

Mistake 1: Creating Too Many Sub-Categories

Separating “groceries” from “household supplies” from “personal care” creates categorization decisions at the store (“Does shampoo go in groceries or personal care?”). Merge into one “food and household” category.

Mistake 2: No “Buffer” Category

A budget without a miscellaneous/buffer category of $50–100/month forces every unexpected $15 charge into an existing category, creating chronic overages that make the budget feel broken when it is actually functioning normally within normal variance.

Mistake 3: Ignoring Annual Costs

Annual and quarterly expenses ($600 insurance, $200 car registration, $500 holiday gifts) must be divided by 12 and assigned to a monthly sinking fund category. Without this, these costs arrive as “surprises” that break the budget mid-month.

Should Budget Categories Change Over Time?

Categories should be reviewed quarterly. Life changes — a new debt payment, a child entering daycare, a paid-off car loan — alter the category structure. A category that was unnecessary (childcare) becomes essential. A category that was essential (car payment) disappears. The budget reflects current reality, not the reality from when it was created.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry