Table of Contents

Contents are generated from article headings.

Loose budgeting is a reduced-tracking financial management approach that controls macro-level financial outcomes — income allocation, savings automation, and spending boundaries — while deliberately ignoring transaction-level detail. Loose budgeting trades precision for sustainability: a system capturing 85% of spending accuracy and lasting 12 months produces dramatically better outcomes than a system capturing 100% accuracy and lasting 3 weeks.

Detailed budgeting fails most people not because the method is flawed but because the effort required to maintain it exceeds the perceived benefit. Research on behavioral sustainability indicates that when ongoing effort outweighs perceived return, behavior abandonment follows — typically within 60–90 days. Loose budgeting designs around this constraint by reducing effort to sustainable levels.

This content discusses reduced-tracking budgeting approaches using behavioral economics, financial planning principles, and research on habit sustainability. Individual tracking tolerance and budgeting complexity vary by person. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Why Detailed Tracking Fails for Most People

The Effort-Reward Imbalance

Tracking every transaction requires daily effort: data entry, categorization, reconciliation. The reward — financial awareness — peaks during weeks 1–2 (when spending patterns are first discovered) and then plateaus. By week three, the same effort produces diminishing informational return because spending patterns are already known.

This is when tracking abandonment occurs — not from laziness but from rational cost-benefit calculation. The person is investing 20 minutes daily for information they already possess.

The Guilt Multiplier

Detailed tracking transforms every purchase into a judgment event. A $4 coffee is not just consumed — it is categorized as “dining – unnecessary” and displayed as a budget overage. Multiplied across 8–12 daily transactions, the cumulative micro-guilt load becomes a reason to abandon budgeting entirely.

The Loose Budgeting Framework

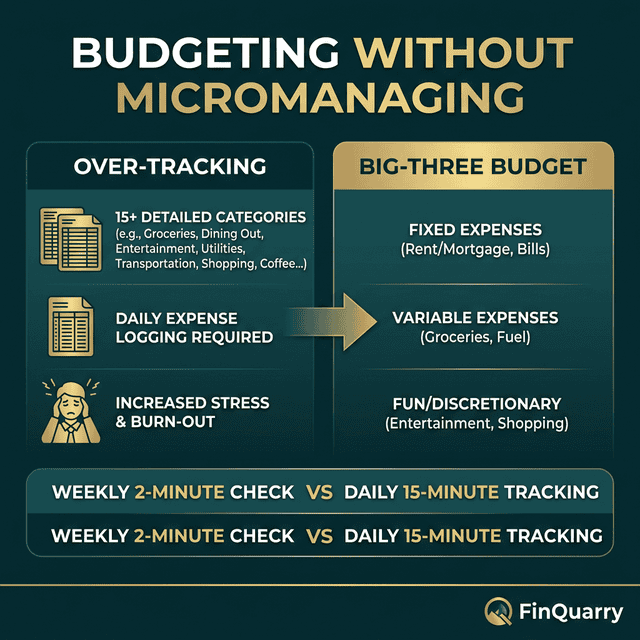

Principle 1: Control the Big Three Only

Loose budgeting manages three macro-categories:

Fixed obligations: Total of all recurring payments (housing, utilities, insurance, minimum debt, subscriptions). Calculated once, updated quarterly.

Savings and debt acceleration: A defined amount transferred automatically on payday. Even $50/month qualifies — the amount matters less than automation.

Spending money: Everything remaining after fixed obligations and savings. This is the total pool for all variable spending — groceries, gas, dining, entertainment — without sub-category tracking.

A person earning $4,200/month with $2,400 in fixed obligations and $300 in automated savings has $1,500 as their spending money pool. No sub-categories. No transaction logging. Just one number to monitor.

Principle 2: Automate Everything Possible

Auto-pay all fixed obligations. Auto-transfer savings. Auto-pay minimum debt payments. The fewer manual financial actions required, the higher the system’s sustainability. Loose budgeting aims for a system that operates correctly even during weeks when the person never opens a spreadsheet.

Principle 3: Weekly Balance Check, Not Daily Tracking

One weekly check replaces daily transaction monitoring: “Is the spending account balance consistent with where I should be at this point in the month?”

A person with $1,500 spending money on day 15 should see approximately $750 remaining. If the balance is roughly there — fine. If significantly lower — spend less this week. If higher — margin exists. This single weekly data point produces sufficient awareness without surveillance-level tracking.

The Spending Account Method

The most effective loose budgeting execution uses a dedicated spending account — a checking or debit account receiving only the monthly spending allocation. On payday, the spending allocation transfers in. All variable purchases come from this account.

Why the Balance Is Enough

When spending money lives in a dedicated account, the balance reflects remaining capacity without calculation. A person who starts with $1,500 and sees $400 remaining on day 22 knows — without any tracking — that $400 must stretch 8 days. That is $50/day. No categories. No app. Just a number that updates with every purchase.

Credit Card Adaptation

If using credit cards for variable spending (rewards, purchase protection), pay the credit card balance from the spending account weekly. This weekly payment keeps card spending visible in the spending account balance and prevents invisible debt accumulation.

When Loose Budgeting Is Not Enough

Loose budgeting requires margin between income and essential expenses to absorb tracking imprecision. It does not work for:

Zero-margin situations: When income barely covers essentials, every dollar must be tracked. No-savings budgeting requires detail that loose budgeting cannot provide.

Active debt elimination: Aggressive debt payoff requires identifying compressible categories — visibility that loose budgeting’s aggregation obscures. Zero-based budgeting is more effective for debt elimination.

Specific time-bound goals: Tight deadline goals benefit from targeted category tracking even if the rest of the budget is loosely managed. Short-term goal budgeting combines targeted precision with overall looseness.

Can Loose Budgeting Build Wealth?

If savings automation is functioning — money transfers automatically to savings and investment accounts on payday — loose budgeting builds wealth as effectively as detailed budgeting. Wealth building depends on savings rate, not on whether dining and grocery spending are tracked in separate categories.

A person automating 15% of income to savings/investing and spending the remainder without tracking accumulates the same assets as a person tracking every category and saving the same 15%.

What If Spending Money Runs Out Early?

Early depletion is the loose budget’s most valuable diagnostic output: the spending allocation is too small or the spending rate is too high. The data point “I run out around day 22” is often sufficient to identify the problem without reviewing individual transactions.

Is Loose Budgeting Lazy?

Loose budgeting is optimized, not lazy. It eliminates low-return tracking effort and preserves high-return behaviors (savings automation, obligation management, weekly awareness). The person practicing loose budgeting is directing finite attention toward the financial actions producing the most impact per unit of effort — which is strategy, not avoidance.

Written by Marcus Tremblay, Senior Financial Analyst | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry