Table of Contents

Contents are generated from article headings.

An unpredictable-expense budget is a financial plan that treats unexpected costs as a structured category — funded through sinking funds, emergency reserves, and category buffers — rather than as exceptions that break the monthly plan. Unpredictable expenses are the single most common reason budgets feel impossible to sustain, not because the person overspent but because the budget was structurally unprepared for costs it should have anticipated as a category even if the specific timing was unknowable.

While individual unexpected expenses are unpredictable, the pattern is not. Something unexpected will happen in any 12-month period. The exact event is unknowable. The certainty that something will occur is virtually absolute. A budget designed for this reality treats “unexpected” as a funded line item.

This content discusses budgeting for unpredictable expenses using financial planning principles and consumer finance data. Emergency costs, insurance products, and assistance resources vary by jurisdiction. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Three Types of Unpredictable Expenses

Type 1: Foreseeable but Undated

Car maintenance will be needed — when is unknown. Medical co-pays will occur — for what is unknown. Home repairs will be required — which system fails first is unknown. These expenses are statistically certain within any 12-month period. Defense mechanism: sinking funds through annual budget planning.

Type 2: Genuinely Unforeseen

A tree falls on the car. A pipe bursts at 2 AM. A family medical emergency requires travel. These could not have been anticipated. Defense mechanism: the emergency fund.

Type 3: Price Unpredictability

The grocery bill was $380 last month and $440 this month. Utilities jumped $60. Insurance renewed higher. These are known categories with unpredictable amounts. Defense mechanism: rolling average budgeting with category buffers.

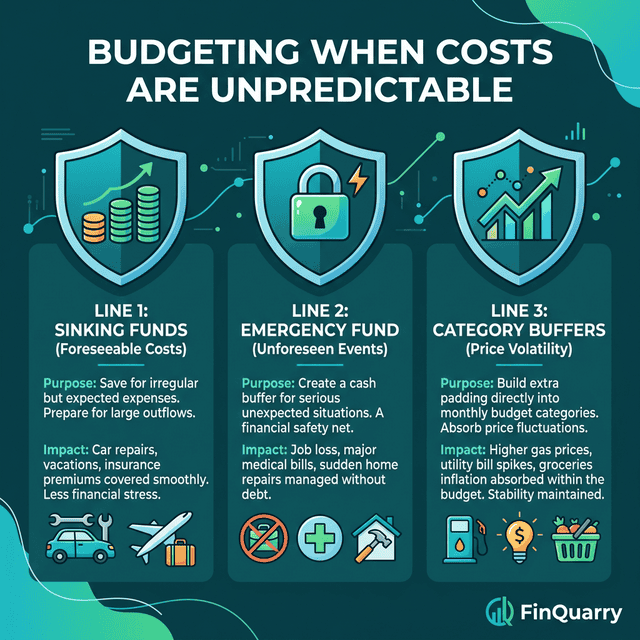

The Three-Line Defense System

Defense 1: Sinking Funds (Foreseeable Undated)

A sinking fund accumulates monthly contributions for a specific expense category with unknown timing.

Car maintenance: Average annual cost is $700–1,000 (under warranty) to $1,200–1,800 (older vehicles). Monthly set-aside: $60–150.

Home maintenance: General guideline is 1–3% of home value annually. A $300,000 home should budget $3,000–9,000/year ($250–750/month). Renters face smaller costs — $30–60/month for appliance, furniture, and household maintenance.

Medical expenses: Average out-of-pocket costs for a privately insured individual are $1,200–1,800/year. Monthly set-aside: $100–150.

Pet expenses: Emergency veterinary costs average $800–5,000 per incident. Monthly set-aside: $40–80 for basic emergency preparedness.

Defense 2: Emergency Fund (Genuine Emergencies)

The emergency fund is financial insurance — money sitting untouched until genuine unforeseen emergency requires it.

Target levels:

- Single-income households: 6–9 months essential expenses

- Dual-income households: 3–6 months

- Variable income: 6–12 months (higher target reflects greater income interruption risk)

The emergency fund must be liquid (accessible in 24–48 hours), safe (high-yield savings, not volatile investments), and protected (not used for non-emergencies regardless of temptation). The Consumer Financial Protection Bureau recommends starting with even a small buffer and building gradually.

Defense 3: Category Buffers (Price Volatility)

Each variable budget category carries a 10–15% buffer above its rolling average. If the grocery rolling average is $420, budget $460–480. This absorbs price fluctuations without triggering a category overage that disrupts the monthly plan.

The buffer is not extra spending capacity — it is volatility absorption that prevents the budget from feeling permanently wrong.

The Decision Framework

When an unpredictable expense arrives:

Step 1: Is this from a sinking fund category? → Fund from sinking fund. No other budget impact.

Step 2: Is this a genuine emergency (unforeseen, immediately necessary, material consequences)? → Fund from emergency fund. Begin replenishing next month.

Step 3: Can this be delayed or structured into payments? → Evaluate: a medical bill on a 0% payment plan disrupts finances less than depleting the emergency fund.

Step 4: Is insurance applicable? → File homeowner’s, renter’s, auto, health, or pet insurance claims before using savings.

How to Stop Feeling Financially Surprised Every Month

The feeling of constant surprise usually stems from three budget gaps: no sinking funds (foreseeable costs arrive unfunded), no category buffers (price changes break tight allocations), or no annual perspective (seasonal and annual costs invisible in monthly view).

Closing these three gaps does not prevent unexpected expenses. It changes most “surprises” from unfunded events to funded events the budget absorbs without disruption.

When the Emergency Fund Is Too Small

When an emergency exceeds the fund: use available savings first, negotiate payment plans (medical facilities and contractors often offer interest-free installments), access lowest-cost credit (0% intro APR card, personal line of credit), then consider hardship assistance programs.

A $3,000 car repair charged to a card at 22% APR costs $4,200 total and takes 5+ years on minimums. The same repair from a sinking fund costs $3,000 and takes zero months to repay. The cost of unfunded emergencies is not just the emergency — it is the debt service that follows.

Can I Stop Worrying About Unpredictable Expenses?

Eliminating concern entirely is unlikely. Substantially reducing financial impact is achievable through the three-line defense. A person with funded sinking funds, a 6-month emergency fund, and buffered categories does not prevent unpredictable costs — they prevent unpredictable costs from becoming financial crises.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry