Table of Contents

Contents are generated from article headings.

A multiple-paycheck budget is a financial plan that allocates specific expenses to specific pay periods based on bill due dates and paycheck arrival timing — solving the cash flow mismatch that makes adequate income feel insufficient. Multiple-paycheck budgeting addresses a timing problem, not a spending problem: total monthly income covers total monthly expenses, but the sequence of when money arrives and when bills depart creates temporary shortfalls that produce overdraft risk and credit card reliance.

Bi-weekly workers receive 26 paychecks per year (two months include a third paycheck). Semi-monthly workers receive 24. Dual-income households where each earner follows a different pay schedule face coordination complexity that monthly budgets structurally cannot address without per-paycheck allocation.

This content discusses budgeting for multiple pay schedules using financial planning principles. Pay frequencies, bill due dates, and banking structures vary by employer, jurisdiction, and provider. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Why Multiple Paychecks Create Budget Chaos

The Cash Flow Mismatch

Household bills are monthly with fixed due dates that do not align with paycheck dates. Rent is due the 1st. Car insurance auto-pays on the 15th. Utilities bill on the 22nd. Paychecks arrive the 7th and 21st (bi-weekly) or 15th and 30th (semi-monthly).

A person earning $4,800/month via two $2,400 bi-weekly paychecks may have $2,100 in bills due between the 1st and 14th, but only $2,400 arriving on the 7th — leaving $300 for two weeks of variable spending. The second pay period has $900 in fixed bills and $2,400 arriving, leaving $1,500. Same monthly income. Dramatically different per-period availability.

The Mental Allocation Trap

Many people mentally assign bills to paychecks: “Paycheck 1 covers rent. Paycheck 2 covers the car.” This works until an irregular expense — medical co-pay, car repair, annual subscription — overloads one paycheck while the other has surplus. Without structural allocation, the overloaded paycheck produces overdraft or credit card usage for a timing problem.

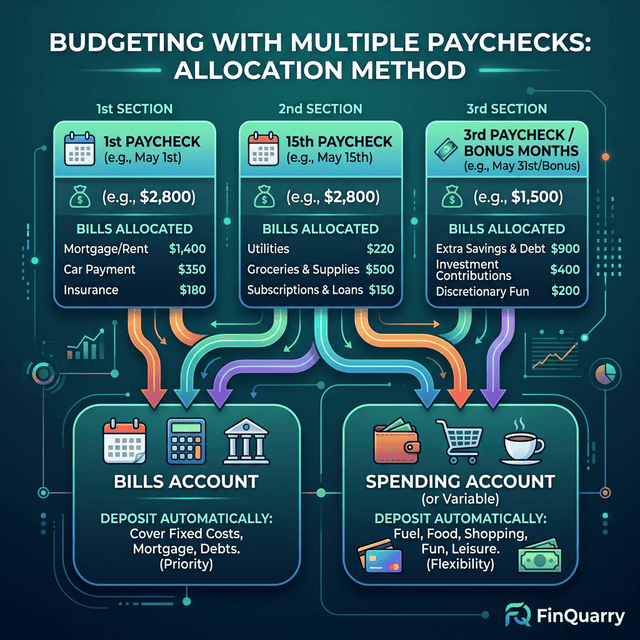

The Paycheck Allocation Method

Step 1: Map Every Bill to Its Due Date

Create a 30-day calendar with every recurring expense placed on its due date. Group expenses by pay period to reveal load distribution between paychecks.

Step 2: Rebalance Due Dates

If one pay period carries disproportionate obligations, contact providers to adjust due dates. Most utility companies, insurance providers, and subscription services accommodate date changes. Moving car insurance from the 5th (overloaded with rent on the 1st) to the 20th redistributes cash flow without changing total costs.

Step 3: Assign Variable Spending Per Period

After fixed obligations are mapped, divide remaining variable spending equally across pay periods. If Paycheck 1 ($2,400) has $1,800 in fixed costs and a $150 savings transfer, the variable allocation is $450 for that period. This prevents front-loading spending and running short late in the month.

The Three-Paycheck Month Strategy

Bi-weekly workers receive three paychecks in two months per year. These are strategic opportunities — the monthly budget is designed on two paychecks, making the third paycheck bonus capacity.

Identifying Three-Paycheck Months

Three-paycheck months occur when the first paycheck falls early enough for a third to fit before month-end. Identify them at the start of each year and mark them in the annual budget.

Strategic Third-Paycheck Allocation

The third paycheck — typically $1,500–2,500 — should be pre-committed to specific targets:

- Emergency fund acceleration

- Sinking fund for irregular expenses (holiday gifts, annual insurance)

- Debt payoff boost

- Short-term goal funding

The worst use: absorbing it into regular spending without deliberate allocation, which produces zero strategic benefit.

Dual-Income Paycheck Coordination

The Contribution Account Method

Both earners transfer their household contribution (proportional to income) to a shared account on each payday. The shared account funds all household obligations. Each earner retains the remainder as personal spending.

A couple earning $5,200 combined ($3,200 + $2,000) with $3,800 in household costs might contribute proportionally: Partner A contributes 61.5% ($2,340), Partner B contributes 38.5% ($1,460). Personal remainders: $860 and $540 respectively. This eliminates “your paycheck covers the mortgage” coordination problems.

Income Disparity Management

Proportional contribution (each contributing their income percentage rather than 50/50) prevents the lower earner from financial strain while maintaining fairness. The household budgeting approach makes the model explicit.

The Buffer Account Solution

For persistent timing issues, a buffer account holding one month’s essential expenses eliminates timing problems permanently. Bills pay from the buffer. Paychecks replenish the buffer. This decouples bill timing from paycheck timing.

Building the buffer takes 2–3 months of directing surplus into the account. Once established, it permanently eliminates paycheck-to-bill anxiety.

Monthly vs. Per-Paycheck Budgeting?

Both work — monthly budgeting provides overview while per-paycheck provides immediate paycheck-level clarity. A hybrid captures both: the monthly plan sets totals, per-paycheck allocation executes in real time.

What If Paycheck Amounts Vary?

For overtime, commission, or tip income: budget on the smallest recent paycheck. Treat variable surplus as uncommitted income — allocated after arrival, never before.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry