Table of Contents

Contents are generated from article headings.

A zero-based budget is an income-allocation method where every dollar of after-tax income is assigned to a specific category — expenses, savings, debt payments, or discretionary spending — until the remaining unallocated balance equals zero. Zero-based budgeting eliminates unassigned money, which is the primary cause of unconscious overspending in traditional budgets.

Zero-based budgeting differs from percentage-based methods like the 50/30/20 rule by requiring granular category-level assignment rather than broad allocation. This precision produces maximum visibility over where money goes but demands higher ongoing tracking effort — typically 20–30 minutes per week compared to 5 minutes for simpler methods.

This content discusses zero-based budgeting using financial planning principles and behavioral economics research. Income levels, costs, and financial products vary by jurisdiction. FinQuarry provides informational content only — this does not constitute personalized financial advice.

How a Zero-Based Budget Works

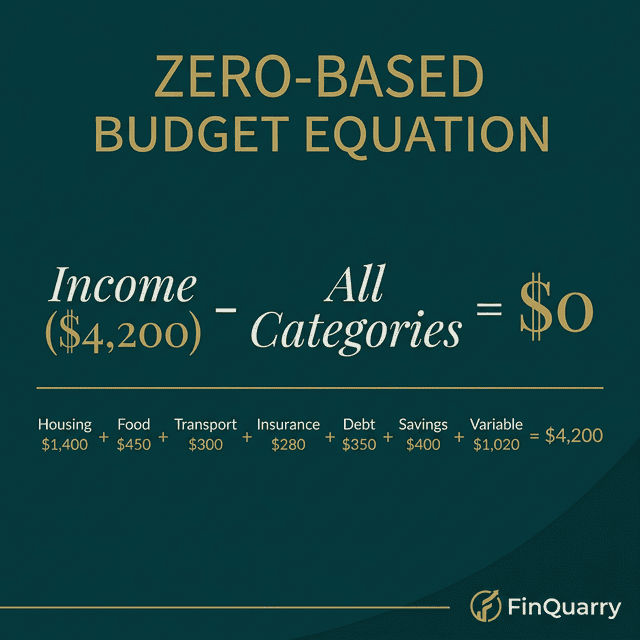

The zero-based budget equation is: Income − All Allocations = $0. Every dollar entering the household receives a destination before the month begins. No dollar remains unassigned.

The Assignment Process

Zero-based budgeting begins with total after-tax income at the top and subtracts each allocation sequentially: housing, utilities, insurance, groceries, transportation, debt minimums, savings, and discretionary categories. The final line reads $0.00.

A person earning $4,200/month after taxes might allocate: rent ($1,200), utilities ($180), car payment ($350), insurance ($120), groceries ($450), gas ($100), minimum debt payments ($250), savings transfer ($200), subscriptions ($45), dining out ($100), personal spending ($80), clothing ($50), household items ($40), and miscellaneous ($35). The total: $4,200 − $4,200 = $0.

What “Zero” Actually Means

Zero does not mean the bank account reaches zero. Zero means the budget has no unassigned dollars. The difference matters: unassigned money tends to be spent without awareness, producing the “where did my money go?” experience. Assigned money — even money assigned to “fun” or “dining out” — carries intentionality that prevents unconscious depletion.

Why Zero-Based Budgeting Works for Debt Elimination

Zero-based budgeting excels at debt reduction because it makes every dollar’s destination visible, which reveals discretionary spending that can be redirected to debt payments.

The Visibility Mechanism

A person carrying $8,000 in credit card debt at 22% APR who uses a zero-based budget can see that $145/month goes to dining out, $80 to subscriptions, and $55 to impulse purchases. That $280/month, redirected to debt, would eliminate the $8,000 balance in approximately 24 months (accounting for interest) instead of the 11+ years that minimum payments alone require.

This visibility is structurally impossible in budgets where spending categories are estimated rather than tracked. Envelope budgeting produces similar visibility through a physical mechanism.

The Debt Snowball in Zero-Based Format

The zero-based framework naturally supports the debt snowball method. As each small debt is eliminated, its monthly allocation is reassigned to the next debt rather than absorbed into general spending. Because zero-based budgets track every dollar, the freed allocation is always visible and always available for reassignment.

Where Zero-Based Budgeting Breaks Down

High Tracking Burden

Zero-based budgeting requires tracking every transaction against its assigned category. For a household averaging 120–150 transactions per month, this means daily or near-daily categorization. Research on financial behavior indicates that tracking fatigue — the gradually declining willingness to categorize — causes 40–60% of zero-based budgeters to abandon the method within 90 days.

The tracking burden is manageable for people who find categorization satisfying or use apps that automate it. For people who find tracking aversive, simpler methods produce better long-term outcomes through sustained use.

Irregular Income Incompatibility

Zero-based budgets require a known income number to build from. Freelancers, commission workers, and gig economy participants whose income varies monthly must either budget from their lowest month (leaving surplus income unplanned until it arrives) or rebuild the budget each month from scratch — adding complexity to an already high-effort system.

Perfectionism Trap

Some zero-based budgeters treat category overages as personal failures rather than data points. A $30 grocery overage in a $450 category (6.7% variance) is normal monthly fluctuation. Treating it as a crisis — or as evidence that the budget doesn’t work — produces psychological stress disproportionate to the financial impact.

How to Start a Zero-Based Budget

Step 1: Calculate Exact Take-Home Income

Use the after-tax, after-deduction number from the most recent pay stub. For variable income, use the lowest of the past six months.

Step 2: List Every Expense Category

Start with fixed obligations (housing, debt, insurance), then variable essentials (food, gas, medical), then discretionary (dining, entertainment, clothing, personal). Include savings and debt payments as categories — they are not leftovers.

Step 3: Assign Dollar Amounts Until Zero

Allocate known fixed amounts first. Then assign variable categories based on three-month spending averages. Adjust until income minus all allocations equals exactly zero.

Step 4: Track and Adjust Weekly

Check category balances weekly. When a category runs over, transfer from another category — do not add new money. This forced trade-off is the behavioral mechanism that makes zero-based budgeting produce spending awareness.

Can I Use a Zero-Based Budget With a Budgeting App?

Yes — several budgeting apps are specifically designed for zero-based methodology. YNAB (You Need A Budget) is the most prominent, requiring users to assign every dollar before spending. EveryDollar provides a guided zero-based template. Both automate the category tracking that makes manual zero-based budgeting time-intensive.

The app reduces the tracking burden from 20–30 minutes weekly to 5–10 minutes, which significantly improves the method’s sustainability for people whose primary barrier is effort, not philosophy.

Is Zero-Based Budgeting Worth the Effort?

For people in active debt repayment — particularly credit card debt above $3,000 — zero-based budgeting tends to produce faster debt elimination because it reveals redirectable spending that broader methods miss. For people whose finances are stable and whose primary goal is maintenance rather than change, the tracking effort often exceeds the marginal benefit over simpler approaches.

The right question is not whether zero-based budgeting is theoretically superior but whether the person will sustain the tracking effort long enough for the method to produce results. A budget calculator can help determine whether the complexity is justified given an individual’s financial situation.

Written by Marcus Tremblay, Senior Financial Analyst | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry