Table of Contents

Contents are generated from article headings.

Persistent budget failure — where a person has tried multiple budgets across months or years and none have worked — is a structural pattern indicating a mismatch between the budgeting method, the person’s cognitive style, their income-expense ratio, or unaddressed emotional barriers to financial engagement. Persistent budget failure is distinctly different from a single failed budget: one failed budget is a design problem. Budgets that never work signal a deeper incompatibility.

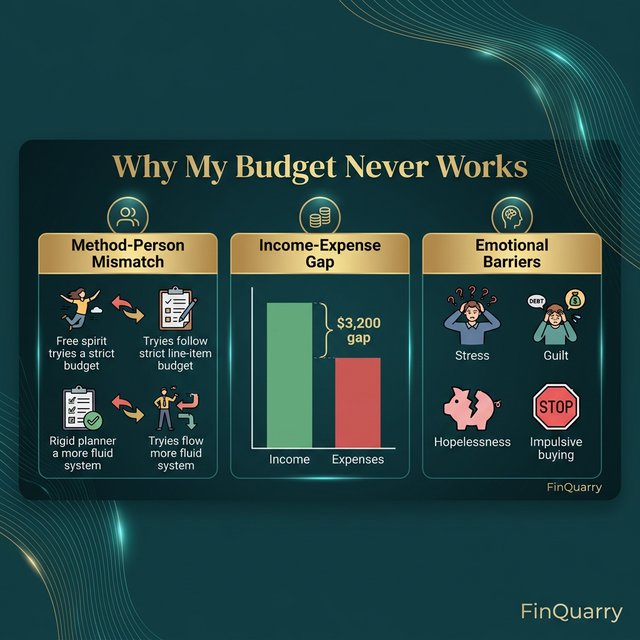

Three root causes explain nearly all persistent budget failure: the method-person mismatch (wrong tool for the person’s behavioral style), the income-expense gap (essential costs exceed or nearly equal income, leaving no margin for any budget to manage), and the emotional barrier (unresolved financial anxiety that prevents sustained engagement with money).

This content discusses persistent budget failure using behavioral economics, financial psychology, and financial planning principles. Individual financial situations, cognitive styles, and emotional relationships with money vary. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Root Cause 1: Method-Person Mismatch

The Wrong Tool Problem

A detail-averse person using a 20-category zero-based budget will fail — not from lack of discipline but from cognitive incompatibility. A person who thrives on structure will fail with a loose budgeting approach because insufficient structure produces anxiety.

The match:

- High-detail tolerance: Zero-based budget, envelope system

- Low-detail tolerance: 50/30/20 rule, anti-budget (automate savings, spend the rest)

- Variable income: Priority waterfall, baseline budgeting

- Shared finances: Contribution account method, household budgeting

A person who has “tried everything” has usually tried 2–3 methods from the same complexity level. Switching from a high-detail method to a fundamentally different approach often solves the persistence problem.

Root Cause 2: The Income-Expense Gap

When No Budget Can Work

If essential expenses (housing, food, utilities, insurance, minimum debt payments, transportation) consume 95–100% of after-tax income, no budgeting method can produce savings. The issue is not the budget — it is the mathematical relationship between income and obligations.

A person earning $3,200/month with $3,050 in essential costs has $150 of margin. This $150 must absorb all variable spending, savings, and irregular expenses — a mathematical impossibility that produces chronic budget failure regardless of method.

Diagnosis: calculate the survival floor (total of all non-negotiable monthly costs from actual data). If the survival floor leaves less than 10–15% of income as margin, the priority shifts from budgeting to structural financial intervention — income increase, cost reduction, or assistance programs.

Root Cause 3: Emotional Barriers

The Avoidance Pattern

Some people cannot sustain budgets because financial engagement triggers anxiety, shame, or avoidance. Opening the budget app produces dread. Checking balances triggers catastrophizing. The budget becomes a source of emotional distress rather than a planning tool.

This pattern is not a budgeting problem — it is a financial anxiety pattern that budgeting methods cannot solve alone. The intervention may involve anxiety-adapted budgeting (3-number budget, weekly 10-minute check-ins) or professional financial therapy.

The Budget Compatibility Test

Before starting another budget, answer three diagnostic questions:

1. “Does my income exceed my essential expenses by at least 10%?” If no, address the income-expense gap first. No budget works without margin.

2. “Does the budgeting method match how I naturally process information?” If the method requires daily tracking and daily tracking feels unbearable, the method is wrong.

3. “Can I check my bank balance without significant anxiety?” If checking balances triggers avoidance or panic, financial anxiety needs addressing before budgeting can succeed.

What If I Have a Budget That Works for 2–3 Months Then Fails?

A budget lasting 2–3 months typically has one of two issues: it relies on motivation (which fades) rather than automation (which persists), or it lacks irregular expense funding (working months are “normal” months; failure occurs when a quarterly or annual expense arrives).

The fix for motivation-dependent budgets: automate savings, auto-pay bills, reduce tracking to weekly. The fix for irregular expense failure: add sinking funds calculated from last year’s actual non-monthly spending.

Is It My Fault?

Budget failure is almost never a character flaw. It is an engineering problem — the wrong tool applied to a specific situation. The person who cannot follow a 20-category spreadsheet budget is not lazy. The person whose expenses exceed income is not irresponsible. The person who avoids financial engagement is not immature. Each needs a different solution, and the diagnosis determines the prescription.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry