Table of Contents

Contents are generated from article headings.

Budget failure is a predictable pattern caused by design flaws — not discipline failures. Research consistently shows that while approximately 85% of Americans maintain some form of budget, nearly 74% struggle to follow it consistently. This gap is not a willpower problem. It is a structural problem: most budgets are built on assumptions about human behavior that do not match how people actually make financial decisions.

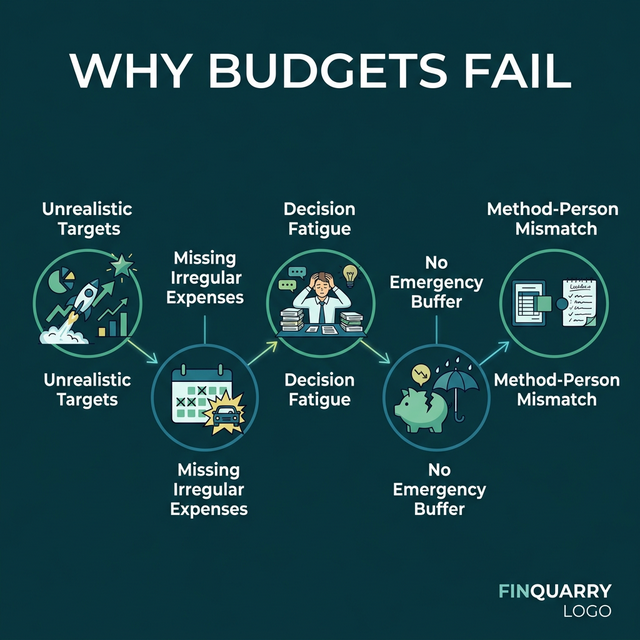

Budget failure follows a repeatable pattern across income levels, age groups, and circumstances: unrealistic spending targets, neglected irregular expenses, excessive restriction, decision fatigue from granular tracking, and treating budgeting as a one-time event rather than an adaptive system.

This content discusses why budgets fail using behavioral economics research, consumer survey data, and financial planning frameworks. Financial products and economic conditions vary by jurisdiction. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Unrealistic Expectations: The Most Common Cause

The Estimation Problem

Budget failure begins most often with estimated rather than measured spending data. People systematically underestimate spending in categories where purchases are small, frequent, and emotionally driven — coffee, delivery fees, subscriptions, convenience items — while overestimating their ability to reduce socially embedded spending like dining and entertainment.

A person estimating $200/month for dining who actually spends $340 has built a $140/month budget error before the first week ends. Across 5–6 underestimated categories, the accumulated gap can reach $300–500/month — accounting for the entire savings allocation the budget was designed to produce.

The fix is measurement, not better estimation. A budget built from three months of actual bank/credit card data starts from factual baseline rather than aspirational projection.

Unsustainable Savings Targets

A budget setting $600/month savings on $4,000 income when actual discretionary spending has historically been $800/month is engineering failure. The person must compress $800 of existing behavior into $200 — a 75% reduction that functions like a crash diet: short-term compliance followed by budget abandonment.

Sustainable approach: start at 5–10% savings ($200–400) and increase by $25–50/month as spending patterns adjust. The person who saves $250/month for 12 months ($3,000) outperforms the person who saves $600/month for 3 months ($1,800) and quits.

The Deprivation Trap

Overly restrictive budgets trigger the same psychological response as dietary restriction: deprivation produces compensatory excess. A person denying all discretionary spending for three weeks is psychologically primed for a spending binge — accumulated emotional pressure releases as exactly the unplanned spending the budget was designed to prevent.

How Restriction Creates Burnout

Financial restriction depletes self-control through a process behavioral economists call ego depletion. Every resisted spending impulse consumes finite cognitive control capacity. A budget requiring constant resistance — no coffee, no convenience meals, no small satisfactions — progressively exhausts this capacity until resistance fails.

The structural solution: a funded discretionary allocation. A budget including $100–150/month of planned “guilt-free spending” prevents the deprivation-binge cycle by providing regular satisfaction that makes the overall system sustainable.

Forgotten Irregular Expenses

Budgets built around monthly recurring expenses fail when non-monthly costs arrive: annual insurance premiums ($600–1,200), car maintenance ($200–800), holiday gifts ($500–1,500), medical co-pays ($50–250). These costs are predictable annually but invisible monthly.

The failure mechanism: irregular expenses consume funds allocated to other categories, creating cascading violations that feel like the budget “doesn’t work.” A comprehensive budget includes a monthly sinking fund calculated from last year’s actual non-monthly spending ÷ 12, converting unpredictable costs into a funded monthly line item.

Decision Fatigue and Tracking Overload

Budgets requiring granular tracking of every transaction impose unsustainable cognitive burden. Every tracked purchase demands a decision (which category?), an evaluation (over or under budget?), and an adjustment (cut elsewhere?). Across 15–30 daily transactions, this produces decision fatigue — progressive quality degradation that causes system abandonment.

Why Most Tracking Fails After Week Two

Expense tracking requires high effort (manual data entry, categorization) and delivers low immediate reward (no dopamine, no tangible benefit). This effort-reward mismatch makes tracking one of the most difficult financial behaviors to sustain — budgeting apps typically show engagement cliffs around day 14.

The fix: monitor 3–5 major categories rather than 20 sub-categories. Automate tracking where possible so the system requires observation rather than input. This preserves awareness without the cognitive load that causes tracking abandonment.

The All-or-Nothing Failure Mode

Many budgets fail because a single violation triggers total abandonment. One overspent category becomes “the budget doesn’t work” and the entire system is discarded.

Effective budgets accommodate deviation. A category overage in one area is offset by an underage in another, or by adjusting next month. The goal is directional consistency: a budget capturing 80% of intended allocation across 90% of months produces dramatically better outcomes than one demanding 100% compliance and abandoned after the first violation.

What Is the Simplest Budget That Works?

Three categories: fixed obligations (rent, utilities, insurance, minimum debt), savings/debt reduction (automated transfer on payday), and spending money (everything remaining). This structure eliminates granular tracking overhead while preserving the core function: savings happens before spending consumes available income.

How Do I Know If My Budget Is Too Restrictive?

A budget is too restrictive if: maintaining it requires constant willpower expenditure, violations produce guilt rather than useful data, or the person frequently “cheats” and hides spending from themselves. These symptoms indicate a design flaw. Adding genuine discretionary allocation typically improves overall compliance — because a sustainable budget that is followed outperforms an ideal budget that is abandoned.

Written by Marcus Tremblay, Senior Financial Analyst | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry