Table of Contents

Contents are generated from article headings.

A broken budget is any financial plan that consistently fails to match actual spending behavior — producing chronic category overages, missed savings targets, or complete abandonment within 60–90 days. A broken budget is diagnostic information, not evidence of personal failure. The budget broke because something in its design does not match the person’s actual financial reality or behavioral patterns.

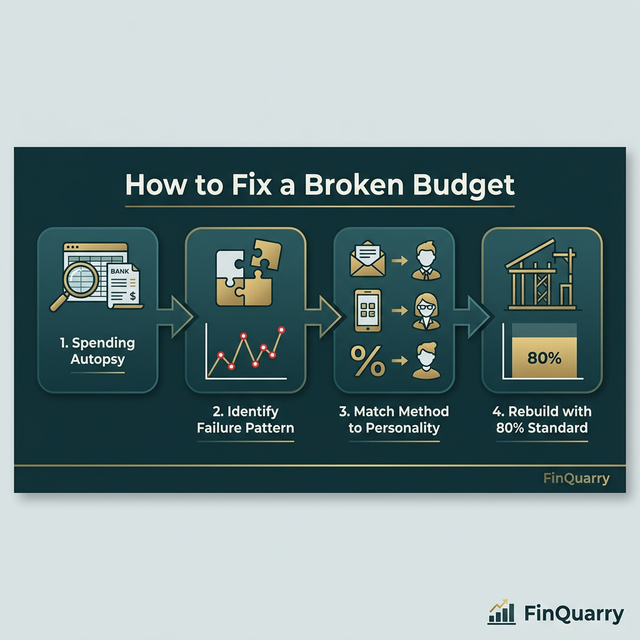

Budget repair follows a four-step process: diagnose the failure mode, establish the factual financial baseline, rebuild with an appropriate framework, and add structural failure prevention. Most broken budgets can be repaired without changing total income or expenses — the fix is typically architectural, not financial.

This content discusses budget repair using financial planning principles and behavioral economics. Financial circumstances and available solutions vary by jurisdiction. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Step 1: Diagnose the Failure Mode

The Categories That Break

Pull three months of actual spending data and compare to the budget’s allocations. The categories where actual spending consistently exceeded budget reveal the failure mode:

- Food/dining over by $150–300/month: The allocation was based on aspiration, not behavior. Recalibrate to 3-month average.

- “Miscellaneous” absorbing $200–400/month: The budget lacks sufficient categories — expenses without a home get dumped into catch-all categories that balloon.

- Savings target missed every month: The savings allocation was set first rather than calculated from the surplus remaining after actual obligations.

The Five Failure Patterns

Estimation failure: Budget built on estimated rather than actual spending data. Fix: rebuild from 3 months of actual bank/credit card statements.

Complexity failure: Too many categories (15+) creating tracking fatigue. Fix: consolidate to 5–7 categories.

Restriction failure: Discretionary spending eliminated, producing deprivation-driven budget abandonment. Fix: add funded guilt-free spending category.

Irregular expense failure: Annual and quarterly costs not pre-funded. Fix: add sinking funds.

Income-expense structural failure: Essential expenses exceed income — no budget design can fix a mathematical impossibility. Fix: address income or structural costs first.

Step 2: Establish the Factual Baseline

The Three-Statement Audit

Pull bank and credit card statements for the past 3 months. Categorize every transaction into 5–7 groups: housing, transportation, food, utilities/insurance, debt payments, discretionary, and savings. Calculate the actual monthly average for each category.

A person who thought they spent $250/month on food but discovers a $420 average across 3 months has found a $170/month budget design error. Multiplied across underestimated categories, the total gap often explains why the budget “never worked.”

The Real Surplus Calculation

Total after-tax income minus total actual spending (not budgeted spending) = real surplus. If the real surplus is $0 or negative, savings goals are structurally impossible until spending is reduced or income increases. If the real surplus is $200, that is the maximum achievable savings rate — not the $500 the original budget aspired to.

Step 3: Rebuild With the Right Framework

Match Framework to Personality

Not every budget method works for every person. The framework must match cognitive style:

- Detail-oriented planner: Zero-based budgeting assigns every dollar a job.

- Big-picture thinker: 50/30/20 rule manages three macro-categories.

- Tracking-averse person: Envelope system or loose budgeting with automated savings.

- Variable-income earner: Priority-based allocation that adjusts monthly.

A person who abandoned a zero-based budget due to tracking fatigue does not need more discipline — they need a different method.

Build From Actuals, Not Goals

The rebuilt budget uses actual 3-month averages as category starting points, then makes deliberate, specific adjustments. Not “spend less on dining” but “reduce dining from $420 to $350 by cooking two additional meals per week.” Specific, modest adjustments are sustainable. Vague, dramatic cuts are not.

Step 4: Add Structural Failure Prevention

Automate the Non-Negotiables

On payday: auto-transfer savings allocation, auto-pay all fixed bills, auto-transfer sinking fund amounts. After automation, the remaining balance is spending money. This structure means the budget functions correctly even during weeks when the person does not engage with it at all.

The Monthly 15-Minute Review

Replace daily tracking with one monthly review: compare actual category spending to plan, note 2–3 adjustments, and carry forward. The review should use data (bank statements), not memory, and focus on patterns rather than individual transactions.

The 80% Compliance Standard

A budget hitting 80% of its targets across 80% of months is performing well. Abandon the 100% standard — it produces guilt, shame, and abandonment. Treat deviations as calibration data.

How Long Does Budget Repair Take?

Months 1–2: data collection and baseline establishment. Month 3: rebuilt framework in operation. Months 4–6: calibration through actual performance. A repaired budget typically reaches stable operation by month 4 — producing consistent results without constant effort.

What If I Have Tried Multiple Budgets and None Work?

Repeated budget failure across multiple methods usually indicates one of two root causes: either the essential expenses genuinely exceed income (structural issue requiring income intervention), or the person has unaddressed financial anxiety that makes any financial engagement emotionally threatening. The first requires financial restructuring. The second may benefit from financial therapy.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry