Table of Contents

Contents are generated from article headings.

Yes, you can file bankruptcy on tax debt, but bankruptcy only eliminates certain income tax debts, and only if strict legal conditions are met. Most tax debts are not automatically erased, and many survive bankruptcy entirely. Whether tax debt can be discharged depends on the type of tax, age of the debt, timing of tax filings, IRS assessment dates, and whether fraud or tax evasion occurred.

As of 2026, bankruptcy may fully discharge qualifying federal or state income tax debt under Chapter 7 or partially resolve tax debt under Chapter 13. However, payroll taxes, trust fund taxes, recent tax debts, penalties related to fraud, and tax liens are generally not eliminated. This guide explains exactly when bankruptcy clears tax debt, when it does not, and how to decide which bankruptcy chapter—if any—makes sense.

Jurisdiction Scope Note: This article explains general bankruptcy and tax principles under U.S. federal law. Specific rules vary by state, court interpretation, and IRS policies.

Temporal Validity: Information reflects U.S. bankruptcy law as of 2026, unless laws or regulations change.

What Does It Mean to Discharge Tax Debt in Bankruptcy?

Discharging tax debt through bankruptcy means the legal obligation to repay that specific tax debt is permanently eliminated. When tax debt qualifies for discharge, the IRS or state tax authority can no longer collect the debt through wage garnishment, bank levies, or other enforcement actions.

What “Discharge” Legally Means

Bankruptcy discharge is a court order that releases the debtor from personal liability for specific debts and prohibits creditors from attempting collection on discharged obligations. For tax debt, discharge means the IRS loses the legal right to pursue payment of the discharged amount, and the taxpayer owes nothing further on that particular tax liability. Discharge differs fundamentally from a payment plan or settlement, where the debt remains legally valid but is paid over time or reduced through negotiation.

Why Most Tax Debt Is Not Automatically Discharged

Most tax debt is classified as priority debt under bankruptcy law, which receives special treatment and typically cannot be discharged. The federal government designates certain debts as priority claims to protect public revenue collection and ensure essential government functions continue. Tax debts that fail to meet specific age, filing, and assessment requirements remain nondischargeable priority obligations that survive bankruptcy, meaning debtors remain personally liable after bankruptcy concludes.

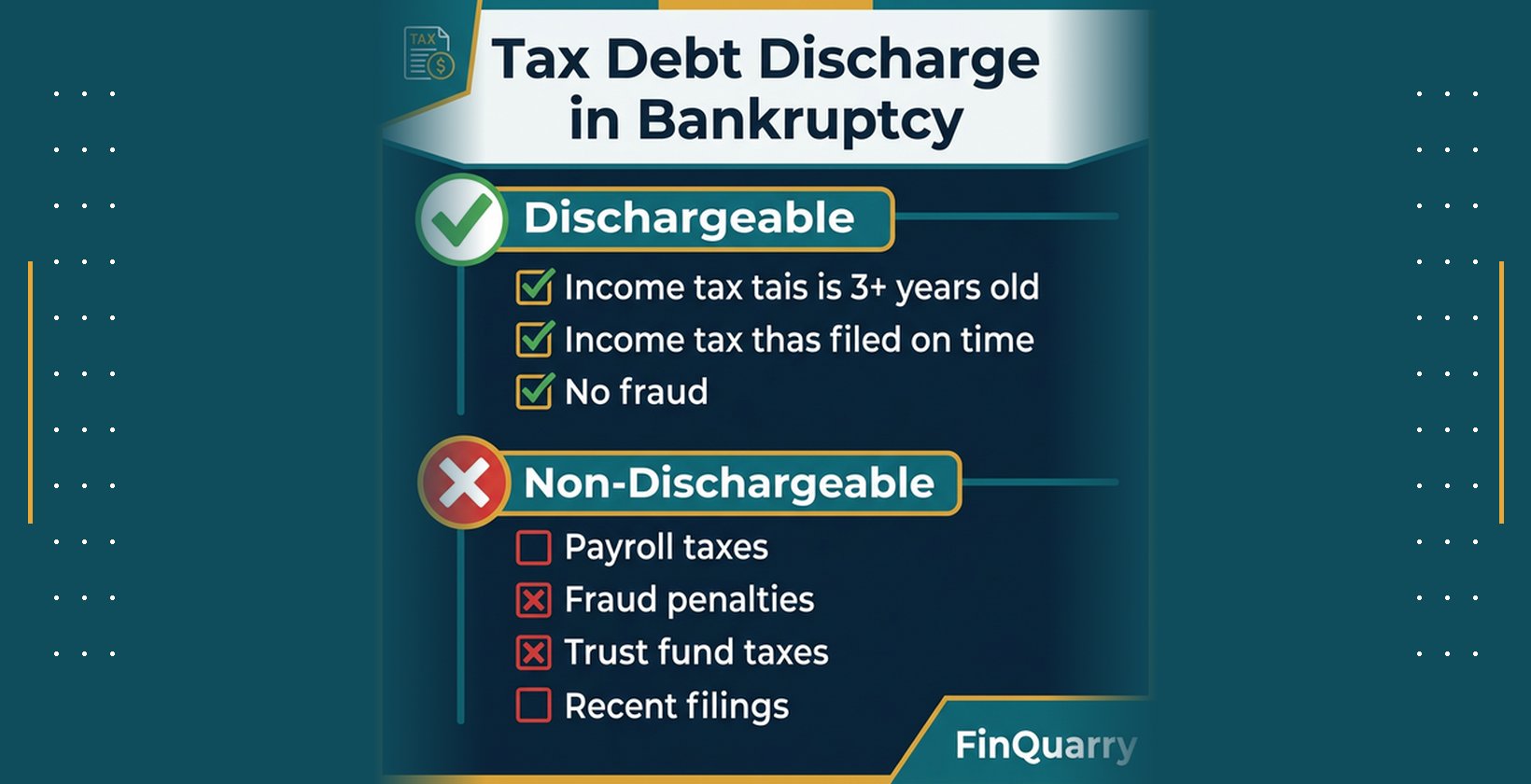

What Types of Tax Debt Can Be Discharged in Bankruptcy?

Only specific categories of tax debt qualify for potential discharge in bankruptcy. The tax type, rather than the amount owed, determines whether bankruptcy can eliminate the obligation.

Federal and State Income Taxes

Federal income taxes reported on Form 1040 and state income taxes may be discharged in bankruptcy if they meet all timing and filing requirements. Income tax debt refers specifically to taxes on wages, investment income, business income, and other personal earnings reported annually to federal and state tax authorities. Both federal income taxes owed to the IRS and state income taxes owed to state revenue departments follow similar discharge rules, though state-specific variations exist in some jurisdictions.

Taxes That Cannot Be Discharged

Certain tax categories are permanently nondischargeable regardless of age or other factors. Payroll taxes, which consist of Social Security and Medicare taxes withheld from employee wages, cannot be discharged because employers hold these funds in trust for the government rather than incurring personal tax liability. Trust fund recovery penalties, assessed when businesses fail to remit withheld payroll taxes, represent personal liability for unpaid trust obligations and remain nondischargeable. Sales taxes collected from customers but not remitted to tax authorities are similarly nondischargeable because the business acted as a collection agent rather than the actual taxpayer. Tax penalties resulting from fraud or willful tax evasion are permanently nondischargeable as a matter of public policy.

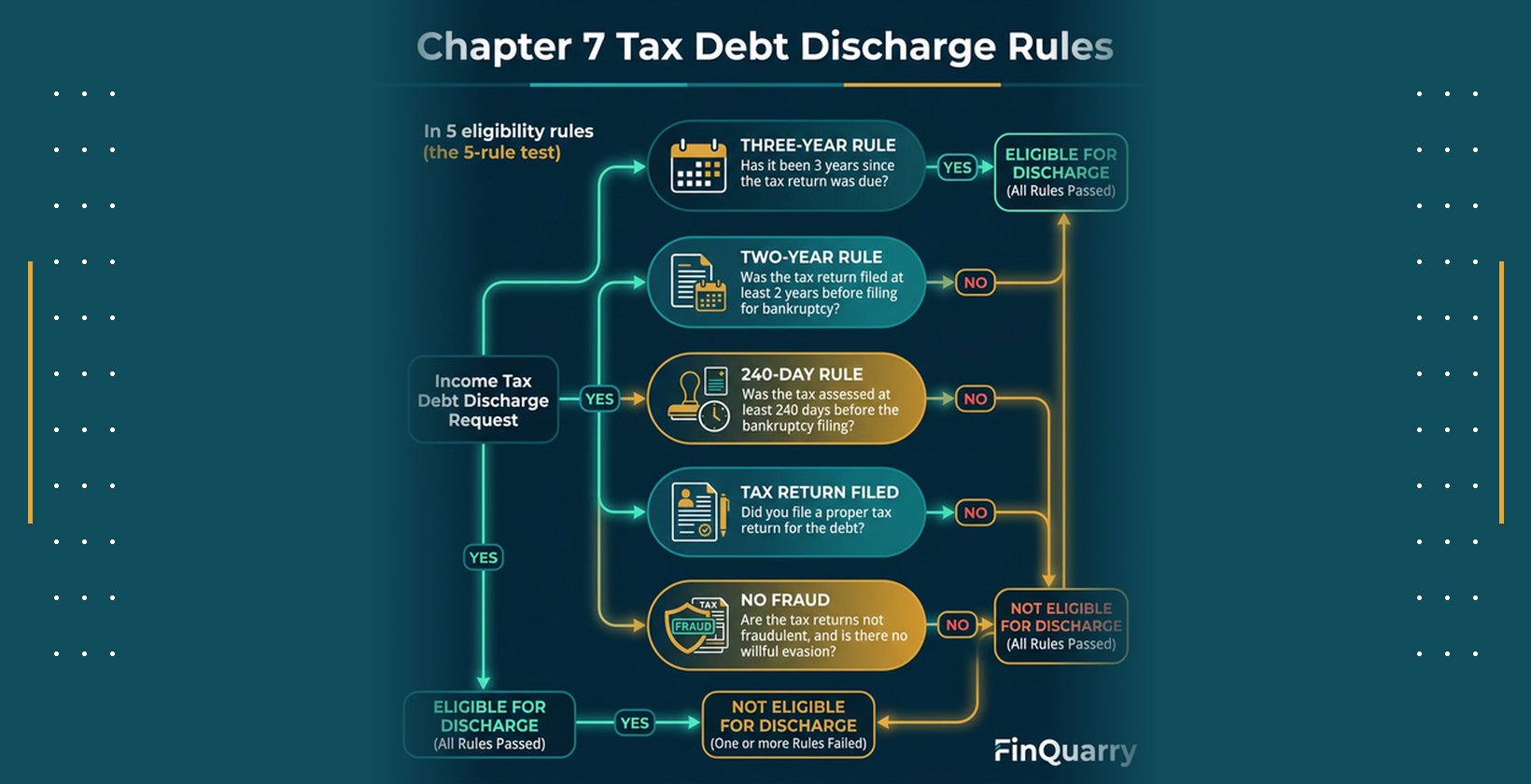

The Bankruptcy Rules That Determine Whether Tax Debt Is Dischargeable

Four separate legal requirements must all be satisfied for income tax debt to qualify for discharge in bankruptcy. These rules establish minimum timeframes and compliance standards that protect government revenue while allowing discharge of sufficiently old, properly filed tax obligations.

The Three-Year Rule

The three-year rule requires that the tax debt relate to a tax return with a due date at least three years before the bankruptcy filing date, including any extensions granted. For most individual income tax returns, the due date is April 15 of the year following the tax year, meaning a 2021 tax return due April 15, 2022 would satisfy the three-year rule if bankruptcy is filed on or after April 16, 2025. Extensions to file push the due date forward, extending the three-year waiting period accordingly. Recent tax debts that do not meet the three-year threshold remain priority debts that survive bankruptcy regardless of other circumstances.

The Two-Year Filing Rule

The two-year rule requires that the taxpayer actually filed the tax return at least two years before filing bankruptcy. This rule prevents taxpayers who file late or fail to file from immediately discharging tax debt through bankruptcy. If the IRS filed a substitute return on behalf of a taxpayer who never filed, that substitute return does not satisfy the two-year rule—only returns voluntarily filed by the taxpayer count toward the two-year requirement. Late-filed returns start the two-year clock from their actual filing date rather than the original due date, which can significantly delay discharge eligibility.

The 240-Day Assessment Rule

The 240-day rule requires that the IRS assessed the tax debt at least 240 days before the bankruptcy filing date. Assessment occurs when the IRS formally records the tax liability in its system, which typically happens shortly after a return is filed or when the IRS completes an audit and determines additional taxes are owed. Certain events toll or pause the 240-day period, including previous offers in compromise, collection due process hearings, and prior bankruptcy filings. Taxpayers who recently completed IRS negotiations or filed earlier bankruptcies may face extended waiting periods before the 240-day requirement is satisfied.

Fraud or Willful Evasion Rule

Tax debts arising from fraudulent tax returns or willful attempts to evade tax obligations are permanently nondischargeable under any circumstances. Fraud includes intentionally filing false information to reduce tax liability, claiming nonexistent deductions, hiding income sources, or using false identities. Willful evasion involves deliberate actions to avoid paying known tax obligations, such as hiding assets, using nominee accounts, or conducting business in cash to conceal income. The IRS must prove fraud or evasion, but once established, the associated tax debt and penalties cannot be discharged in any bankruptcy chapter.

Can Chapter 7 Bankruptcy Eliminate Tax Debt?

Chapter 7 bankruptcy liquidates non-exempt assets to pay creditors and discharges remaining qualifying debts, including eligible income tax debts. Chapter 7 provides the fastest and most complete debt relief when tax debt meets all discharge requirements.

When Chapter 7 Works for Tax Debt

Chapter 7 bankruptcy works for tax debt when the taxpayer has qualifying income tax debt that meets the 3-year, 2-year, and 240-day rules, has no fraud or evasion issues, and either has few assets or can protect existing assets through bankruptcy exemptions. Discharged tax debt in Chapter 7 requires no repayment, and the case typically concludes within four to six months. Taxpayers who qualify for Chapter 7 and have dischargeable tax debt receive full elimination of personal liability without ongoing payment obligations or trustee oversight beyond the case closure.

When Chapter 7 Fails

Chapter 7 bankruptcy fails to help with tax debt when the tax obligations are too recent to meet discharge requirements, involve nondischargeable tax types like payroll taxes, or when the taxpayer has significant non-exempt assets that the bankruptcy trustee will liquidate to pay creditors. Priority tax debts that do not qualify for discharge must be paid in full through asset liquidation or remain as personal obligations after bankruptcy closes. Additionally, taxpayers who fail the means test due to higher income may be ineligible for Chapter 7 and must consider Chapter 13 instead.

What Happens to Tax Liens in Chapter 7

Tax liens filed by the IRS before bankruptcy remain attached to property even when the underlying tax debt is discharged. Discharge eliminates personal liability for the tax debt, meaning the IRS cannot pursue wage garnishment or bank levies for discharged amounts. However, the lien survives as a secured claim against property titled in the debtor’s name at the time of filing. Property with IRS liens cannot be sold or refinanced without satisfying the lien amount, effectively requiring payment of the lien to clear title even though personal liability no longer exists.

Can Chapter 13 Bankruptcy Help With Tax Debt?

Chapter 13 bankruptcy establishes a court-approved repayment plan lasting three to five years that allows debtors to catch up on nondischargeable debts while protecting assets from liquidation. Chapter 13 provides options for managing tax debt that does not qualify for Chapter 7 discharge.

How Chapter 13 Treats Tax Debt

Chapter 13 treats tax debt according to its priority status and discharge eligibility. Priority tax debts that do not meet discharge requirements must be paid in full through the repayment plan, though the debtor receives the full plan term to complete payment. Non-priority tax debts that would qualify for discharge in Chapter 7 may receive reduced payment or no payment if other priority and secured claims consume available plan funds. Nondischargeable tax debt not paid through the plan remains as personal liability after Chapter 13 concludes, though successful plan completion discharges other qualifying unsecured debts.

Why Some People Choose Chapter 13 Anyway

Some taxpayers choose Chapter 13 over Chapter 7 when they have valuable assets they want to protect from liquidation, such as home equity, vehicles, or business equipment. Chapter 13 allows debtors to keep assets while repaying priority tax debts over time under court protection. Additionally, Chapter 13 stops IRS collection actions through the automatic stay and prevents new liens or levies during the plan period. Taxpayers with recent tax debt who cannot wait for discharge eligibility may use Chapter 13 to manage payment obligations while avoiding aggressive IRS enforcement.

Interest, Penalties, and Trustee Fees

Interest on tax debt generally stops accruing during Chapter 13 for priority tax claims, reducing the total amount owed compared to payment plans outside bankruptcy. However, non-priority tax debts continue accruing interest unless specifically addressed in the plan. Penalties on nondischargeable tax debt typically continue, and the bankruptcy trustee charges fees of approximately 3-10% of all payments distributed through the plan. These costs mean Chapter 13 often requires paying more total dollars than the original tax debt, though the structured payment timeline and collection protection may provide value despite higher costs.

What Happens If Your Tax Debt Does Not Qualify for Discharge?

When tax debt cannot be discharged, bankruptcy still offers temporary relief through the automatic stay and may provide strategic advantages for managing nondischargeable obligations.

Automatic Stay Protection

Filing bankruptcy triggers an automatic stay that immediately halts most IRS collection activities, including wage garnishments, bank levies, and asset seizures. The automatic stay remains in effect throughout the bankruptcy case for Chapter 7, typically four to six months, and throughout the repayment plan period for Chapter 13, generally three to five years. However, the automatic stay does not prevent the IRS from conducting audits, issuing tax assessments, demanding tax return filings, or pursuing criminal tax investigations. Once the bankruptcy case concludes, the automatic stay expires and the IRS can resume collection on nondischargeable tax debts.

Post-Bankruptcy Tax Obligations

Tax debts that survive bankruptcy remain legally enforceable after the case closes. The IRS can resume collection efforts immediately upon case closure for Chapter 7 or after completion or dismissal of Chapter 13. However, the collection statute expiration date continues to run during bankruptcy for most purposes, meaning old tax debts may expire under the ten-year collection statute even if they were not discharged. Taxpayers with remaining tax obligations after bankruptcy can pursue IRS payment plans, offers in compromise, or currently not collectible status for debts that survived bankruptcy.

How IRS Tax Liens Affect Bankruptcy Outcomes

Tax liens represent secured claims against property that receive different treatment than unsecured tax debt in bankruptcy. Understanding lien mechanics is critical for evaluating whether bankruptcy provides meaningful relief.

Difference Between Tax Debt and Tax Lien

Tax debt is an unsecured personal obligation to pay taxes owed, while a tax lien is a legal claim against specific property securing payment of tax debt. The IRS files a Notice of Federal Tax Lien in public records after assessing tax debt and demanding payment, which creates a secured interest in all property owned by the taxpayer. The lien attaches to real estate, vehicles, bank accounts, and future acquired property until the tax debt is paid or the lien is released. Tax debt can be discharged in bankruptcy if it meets requirements, but the lien survives as a secured claim against property.

Can Bankruptcy Remove a Tax Lien?

Bankruptcy generally cannot remove an IRS tax lien, even when the underlying tax debt qualifies for discharge. The lien remains attached to property titled in the debtor’s name at bankruptcy filing, meaning the IRS retains the right to collect from that property despite personal liability being discharged. Property subject to tax liens cannot be sold or refinanced without paying the lien amount to clear title. In limited circumstances, taxpayers may use lien avoidance procedures in Chapter 13 for certain types of liens, but federal tax liens on real property and substantial personal property generally cannot be avoided through bankruptcy.

Tax Refunds and Bankruptcy

Tax refunds become assets of the bankruptcy estate and may be claimed by the bankruptcy trustee to pay creditors, depending on the bankruptcy chapter and available exemptions.

Tax Refunds in Chapter 7

Tax refunds the debtor is entitled to receive at the bankruptcy filing date become property of the bankruptcy estate in Chapter 7. The trustee can claim the refund to distribute to creditors, though debtors may protect some or all of the refund using available exemptions under state or federal law. Refunds for tax years ending before bankruptcy are clearly estate property, while refunds for the year in which bankruptcy is filed may be prorated between pre-filing and post-filing periods. Debtors expecting large refunds should consult bankruptcy counsel about filing timing to maximize exemption protection.

Tax Refunds in Chapter 13

Tax refunds during a Chapter 13 case typically must be turned over to the bankruptcy trustee as additional disposable income available to pay creditors. Chapter 13 debtors generally must file annual tax returns with the trustee and surrender refunds throughout the plan period. Some courts allow debtors to retain small refunds or adjust withholding to avoid refunds, while others require all refunds be paid into the plan. Failure to surrender required tax refunds can result in case dismissal and loss of bankruptcy protection.

Should You File Bankruptcy Before or After Filing Taxes?

Bankruptcy law imposes tax return filing requirements that must be satisfied before filing bankruptcy and maintained throughout the case. Noncompliance can result in case dismissal.

Filing Requirements for Chapter 7

Chapter 7 requires that debtors file all tax returns for tax periods ending within four years of the bankruptcy filing date. The bankruptcy court may dismiss the case if returns are not filed, and the IRS can request dismissal if the debtor fails to file required returns. Debtors should ensure all recent tax returns are filed before initiating bankruptcy to avoid dismissal. Additionally, debtors must provide filed returns to the bankruptcy trustee and creditors upon request.

Filing Requirements for Chapter 13

Chapter 13 imposes stricter filing requirements, demanding that all tax returns for the four tax periods preceding bankruptcy be filed before the case begins. Courts may refuse to confirm a Chapter 13 plan if returns are not current. During the Chapter 13 plan period, debtors must continue filing annual tax returns on time and provide copies to the trustee. Failure to maintain current filings during the plan can result in case dismissal, immediate resumption of creditor collection activity, and loss of discharge eligibility.

Alternatives to Bankruptcy for Tax Debt

Several IRS programs provide tax debt relief without bankruptcy, and in some cases, these alternatives offer better outcomes with fewer long-term consequences.

IRS Installment Agreements

IRS installment agreements allow taxpayers to repay tax debt through monthly payments over extended periods, typically up to six years. The IRS offers streamlined installment agreements for debts below $50,000 that require minimal financial disclosure and approval formalities. Installment agreements avoid bankruptcy’s impact on credit and public records, though the IRS continues assessing interest and penalties during the repayment period. Taxpayers who can afford monthly payments may prefer installment agreements over bankruptcy when tax debt is manageable and discharge eligibility is uncertain.

Offer in Compromise

An Offer in Compromise allows taxpayers to settle tax debt for less than the full amount owed based on inability to pay. The IRS evaluates the taxpayer’s income, expenses, and asset equity to determine reasonable collection potential, and may accept payment of that amount to satisfy the entire tax liability. Offers in Compromise require detailed financial disclosure and IRS approval, which is granted in limited circumstances. Successful offers avoid bankruptcy and settle tax debt for reduced amounts, though the application process is complex and many offers are rejected.

When Bankruptcy Is the Last Resort

Bankruptcy becomes the appropriate choice when tax debt meets discharge requirements and the debtor has other significant dischargeable debts that bankruptcy can eliminate simultaneously. Bankruptcy also makes sense when the debtor needs immediate collection relief through the automatic stay and cannot negotiate acceptable IRS payment terms. Conversely, bankruptcy may not be worthwhile when tax debt is the only significant liability, all tax debt is nondischargeable, or IRS alternatives offer comparable relief with less impact on credit and financial records.

Common Mistakes That Prevent Tax Debt Discharge

Several taxpayer errors permanently disqualify tax debt from discharge or create unexpected complications during bankruptcy.

Filing bankruptcy too early, before tax debt satisfies the three-year, two-year, and 240-day requirements, leaves the debt nondischargeable and forces the taxpayer to either repay through Chapter 13 or remain liable after bankruptcy. Missing or late tax return filings prevent satisfaction of the two-year rule and may delay discharge eligibility for years. Paying recent tax debt with credit cards to create dischargeable credit card debt instead fails because courts may rule such charges nondischargeable as fraud. Hiding income, underreporting earnings, or concealing assets during bankruptcy can constitute bankruptcy fraud, result in case dismissal, and create criminal liability beyond the tax issues.

When to Talk to a Bankruptcy or Tax Attorney

Complex tax situations require professional legal analysis to evaluate discharge eligibility, protect assets, and navigate bankruptcy procedures correctly.

Situations Requiring Legal Review

Large tax balances exceeding $25,000 generally warrant professional review to evaluate all available options and ensure optimal strategy selection. Business owners with payroll tax liabilities, trust fund recovery penalties, or sales tax debts face complex nondischargeability issues that require specialized advice. Taxpayers with IRS liens on real property must understand lien survival and property implications before filing bankruptcy. Individuals under IRS audit, facing criminal tax investigations, or with suspected fraud issues should not file bankruptcy without thorough legal counsel, as bankruptcy can complicate ongoing tax disputes and create additional legal exposure.

Frequently Asked Questions About Bankruptcy and Tax Debt

Can bankruptcy erase IRS penalties and interest? Penalties and interest on dischargeable tax debt are discharged along with the principal amount if the underlying tax qualifies for discharge. However, penalties related to fraud or nondischargeable tax obligations remain after bankruptcy.

Does bankruptcy clear state tax debt? State income tax debt follows similar discharge rules as federal income taxes and may be discharged if the tax meets the three-year, two-year, and 240-day requirements. State tax procedures and priority rules vary by jurisdiction.

Can business owners discharge tax debt? Business owners can discharge personal income taxes through bankruptcy if discharge requirements are met, but payroll taxes, trust fund recovery penalties, and certain business taxes are generally nondischargeable regardless of circumstances.

Will bankruptcy stop IRS wage garnishment? Filing bankruptcy immediately triggers an automatic stay that stops IRS wage garnishment during the bankruptcy case. However, garnishment can resume after the case closes if tax debt is not discharged.

How long after bankruptcy does IRS collection resume? The IRS can resume collection on nondischargeable tax debt immediately after Chapter 7 concludes, typically four to six months after filing. In Chapter 13, collection is paused throughout the three- to five-year plan period.

Key Takeaways

Bankruptcy can eliminate income tax debt that meets strict age and filing requirements, providing significant relief for taxpayers with qualifying old tax obligations. The three-year, two-year, and 240-day rules determine discharge eligibility, and all three must be satisfied for income taxes to be erased. Tax liens generally survive bankruptcy even when the underlying tax debt is discharged, requiring payment to clear property titles. Chapter 7 fully discharges qualifying tax debt without repayment, while Chapter 13 allows repayment of nondischargeable taxes over time with collection protection. Professional legal and tax advice is critical for evaluating whether bankruptcy offers meaningful relief for specific tax situations and for avoiding costly mistakes that permanently prevent discharge.

Final Note: Tax debt bankruptcy involves complex legal requirements and significant consequences. This content explains general principles under U.S. federal law as of 2026. Consult qualified bankruptcy and tax professionals for advice specific to your circumstances before making bankruptcy decisions.