Table of Contents

Contents are generated from article headings.

Variable-income budgeting is a financial management system designed for income that fluctuates month-to-month — affecting freelancers, commission workers, seasonal employees, gig workers, and sales professionals. Variable income invalidates the core assumption of standard budgets: that the same amount of money arrives every month. Without that assumption, budgeting requires priority-based allocation that adapts to whatever income actually materializes.

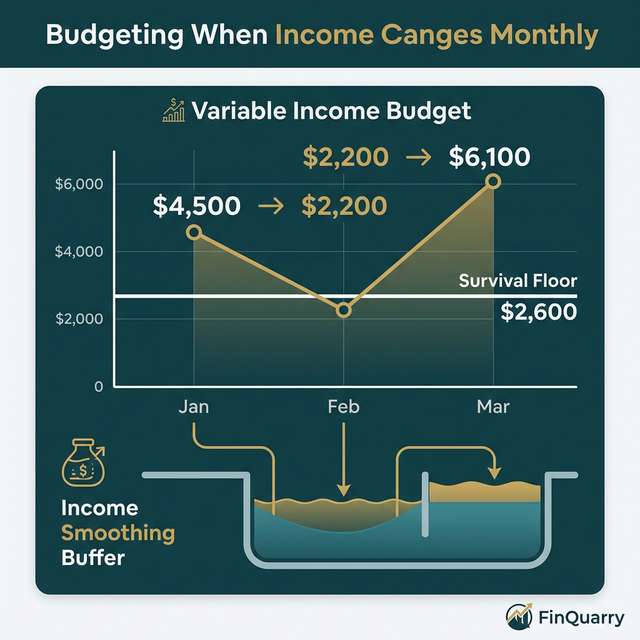

The Bureau of Labor Statistics estimates that approximately 6.3% of workers hold multiple jobs and millions more earn variable income through commission, tips, or project-based work. For these earners, a $4,500 month may follow a $2,200 month, making any fixed-allocation budget mathematically incompatible with the income pattern.

This content discusses variable-income budgeting using financial planning principles and labor market data. Income patterns, tax obligations, and available benefits vary by jurisdiction and employment type. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Why Standard Budgets Fail on Variable Income

The Fixed-Target Problem

A standard budget allocating $1,400 to housing, $450 to food, $200 to transportation assumes those dollars are available every month. When March income is $4,500 and April drops to $2,200, the $2,050 in fixed obligations that fit March income cannot be fully funded in April.

The budget did not fail. The budget was structurally incompatible with the income it was applied to.

The Feast-Famine Cycle

Without structural controls, high-income months produce elevated spending (the “feast”) while low-income months produce financial stress (the “famine”). A commission worker earning $6,200 in March who spends proportionally has no surplus to cover April’s $2,800. The cycle repeats indefinitely, producing the paradox of adequate annual income with chronic monthly instability.

The Priority Waterfall System

When variable income arrives, allocate it through a ranked priority sequence:

Priority 1: Non-Negotiable Obligations

Housing, utilities, minimum debt payments, insurance, essential food, essential transportation. Calculate this precisely from actual costs. A variable earner with $2,400 in non-negotiable obligations has a clear minimum threshold — any month below this amount triggers emergency protocols.

Priority 2: Tax Reserve

Variable earners with self-employment income must reserve 25–35% of gross income for estimated quarterly taxes. A freelancer earning $4,500 in March transfers $1,125–1,575 to the tax reserve immediately — before any other allocation. The IRS imposes penalties for underpayment.

Priority 3: Buffer Replenishment

If the income buffer (one month of survival expenses in a dedicated account) is depleted, surplus funds replenish it before flowing to lower priorities.

Priority 4: Debt Acceleration + Savings

Above-minimum debt payments and savings contributions happen only after priorities 1–3 are funded.

Priority 5: Discretionary

Variable spending, quality-of-life purchases, and goal-directed saving happen only after the upper priorities are fully funded.

The Income Smoothing Buffer

How It Works

Build one month of essential expenses ($2,400–3,500 depending on survival floor) in a dedicated checking account. Live on last month’s income while this month’s income accumulates in the buffer.

March’s $4,500 goes into the buffer. April’s living expenses are paid from March’s income. April’s $2,800 goes into the buffer. May’s living expenses are paid from April’s $2,800. The month-to-month variation is absorbed by the buffer — daily financial life feels stable regardless of income fluctuation.

Building the Buffer

Start by directing surplus from any above-average month entirely to the buffer account. At $200–500/month of surplus, the buffer fills in 5–12 months. Once established, the buffer converts variable income into functionally stable monthly cash flow.

Managing Income Emotionally

Detaching Spending From Income

The hardest discipline in variable-income budgeting: keeping spending constant regardless of income level. A $6,200 month must produce the same spending behavior as a $3,500 month. The surplus from high months funds the buffer, taxes, and acceleration — not lifestyle inflation.

The Scarcity Response

Low-income months trigger a scarcity mindset that produces either panic spending (buying now before money runs out) or paralysis (avoiding all financial decisions). The buffer account counteracts both responses by ensuring that this month’s expenses are already funded regardless of this month’s income.

How Much Emergency Fund Does Variable Income Need?

Variable-income earners need 6–12 months of survival floor expenses in emergency reserves — substantially more than the 3–6 months recommended for salaried employees. The extended target reflects the reality that income recovery from a client loss or market downturn can take months, not weeks.

Written by Marcus Tremblay, Senior Financial Analyst | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry