Table of Contents

Contents are generated from article headings.

Managing money effectively requires understanding how different expense types behave. Some costs stay constant regardless of activity levels. Others fluctuate based on usage, sales volume, or personal choices. Variable expenses change month-to-month based on consumption, business activity, or lifestyle decisions. Fixed expenses remain relatively stable over specific time periods regardless of usage patterns.

Budgeting for these expense types requires different approaches. Fixed expenses need consistent allocation. Variable expenses demand forecasting, monitoring, and adaptive planning strategies. This guide explains how variable and fixed expenses work, how they interact in budgets, and practical methods for managing both expense types effectively.

Scope Note: This content explains budgeting principles for variable and fixed expenses using general financial concepts. Specific tax rules, accounting standards, and regulatory requirements vary by country, business structure, and jurisdiction. This guidance is informational, not legal or tax advice.

What Is a Variable Expense in a Personal or Small Business Budget?

A variable expense is a cost that changes in amount from period to period based on usage, activity level, or consumption patterns. These expenses fluctuate rather than remaining constant across budget cycles.

Definition and Characteristics of Variable Expenses

Variable expenses respond directly to changes in behavior, production volume, or service usage. The amount spent varies based on decisions made during each budget period.

In personal budgets, variable expenses reflect consumption choices. Spending more on groceries one month increases that expense category. Reducing entertainment lowers those costs immediately.

Key characteristic: Variable expenses can be controlled or adjusted within each budget period through behavioral changes or usage modifications.

Business variable expenses often correlate with sales or production volume. Higher sales typically increase costs of goods sold. Lower production reduces raw material expenses proportionally.

Mathematical relationship: Many variable expenses show direct correlation between activity level and total cost incurred during specific periods.

Variable expenses differ from fixed expenses by responding to consumption changes. Fixed costs remain stable regardless of usage or activity levels within normal operating ranges.

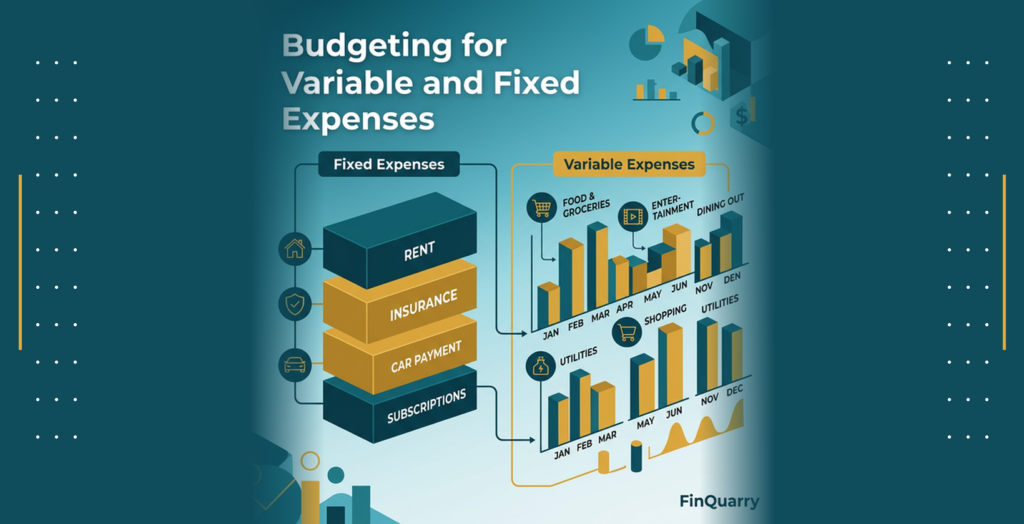

Examples of Variable Expenses in a Budget (Groceries, Utilities, Entertainment, Travel)

Personal variable expenses include groceries, utilities, gasoline, entertainment, dining out, clothing purchases, and discretionary subscription services. Each fluctuates based on usage patterns.

Grocery expenses vary by meal choices, household size changes, and shopping frequency. One month might cost $400, another $600 depending on purchasing decisions.

Utility bills often vary seasonally. Electricity costs increase during summer cooling or winter heating. Water usage changes based on household activities and weather patterns.

Business examples: Cost of goods sold, raw materials, sales commissions, shipping costs, and transaction fees all vary with business activity levels.

Travel expenses fluctuate based on trip frequency, destination choices, and transportation methods. These costs can range from zero to thousands monthly.

Entertainment and dining expenses represent highly variable categories. These costs can be reduced significantly or eliminated temporarily when budget constraints require adjustments.

When Should Fixed and Variable Monthly Budgeted Expenses Be Tracked?

Fixed and variable expenses should be tracked continuously throughout each budget period, not just at month-end. Continuous tracking reveals spending patterns early.

Variable expenses require more frequent monitoring than fixed expenses. Daily or weekly tracking catches overspending before monthly budgets break completely.

Tracking timing: Review variable expenses at least weekly during active budget periods. Check fixed expenses monthly to verify amounts remain consistent.

Mid-period tracking allows budget adjustments before money runs out. Waiting until month-end eliminates correction opportunities during the current budget cycle.

Business budgets benefit from real-time tracking systems that capture variable expenses as they occur. This enables immediate visibility into cost behavior patterns.

Best practice: Track variable expenses within 24-48 hours of occurrence. Track fixed expenses upon payment to confirm amounts match budgeted expectations.

How Variable Expenses Affect Overall Financial Planning

Variable expenses create budget uncertainty that requires planning margin. Unlike fixed costs, variable expenses cannot be predicted with complete accuracy.

Cash flow planning must account for variable expense fluctuations. Months with high variable spending need larger cash reserves than months with controlled consumption.

Planning impact: Variable expenses determine how much discretionary income remains after essential fixed obligations are covered each period.

Long-term financial goals become harder to achieve when variable expenses remain uncontrolled. Unpredictable spending reduces available money for savings, debt reduction, or investments.

Variable expenses offer adjustment flexibility that fixed expenses do not provide. Reducing variable costs creates immediate budget relief during financial stress periods.

Strategic consideration: Minimizing variable expenses as a percentage of total spending increases financial stability and reduces month-to-month budget volatility.

What Variable Expenses Are NOT

Variable expenses do not include costs that remain constant regardless of usage. Rent, loan payments, and insurance premiums are fixed, not variable.

Variable expenses are not unpredictable, though amounts fluctuate. Historical data and usage patterns enable reasonable forecasting despite month-to-month changes.

Critical distinction: Variable does not mean optional. Essential variable expenses like groceries and utilities must be funded despite fluctuating amounts.

Variable expenses are not always controllable in the short term. Some business variable costs directly correlate with revenue and cannot be eliminated without reducing sales.

Understanding what variable expenses are not helps prevent budgeting mistakes like treating essential variable costs as discretionary or assuming all variable expenses can be cut.

Understanding Fixed vs Variable Expenses for Accurate Budgeting

Fixed expenses remain relatively constant over specific time periods regardless of consumption or activity levels. Variable expenses change based on usage, behavior, or production volume.

Definition and Examples of Fixed Expenses (Rent, Loan Payments, Insurance)

Fixed expenses are costs that do not change in total amount within a given budget period, regardless of usage or activity variations.

Common personal fixed expenses include rent or mortgage payments, car loan payments, insurance premiums, subscription services, and lease agreements.

Key characteristic: Fixed expenses require payment of the same amount each period according to contractual or recurring obligations.

Business fixed expenses include salaries for salaried employees, rent for office or retail space, annual software licenses, and depreciation on equipment.

Fixed expenses provide budgeting predictability. Knowing exact amounts due each month simplifies cash flow planning and reduces budgeting complexity.

Time sensitivity: Fixed expenses remain stable for defined periods but may change when leases renew, rates adjust, or contracts expire.

Fixed Expenses vs Variable Expenses in Household and Business Budgets

The fundamental difference between fixed and variable expenses lies in their response to changes in consumption, production, or activity levels.

Fixed expenses maintain constant total amounts within budget periods. Variable expenses increase or decrease based on usage, sales, or behavioral choices.

Household context: Rent stays fixed at $1,500 monthly regardless of household activity. Grocery costs vary from $300 to $600 based on purchasing decisions.

Business budgets show this distinction clearly through cost behavior analysis. Fixed costs like rent remain constant whether business produces 100 or 1,000 units.

Variable costs like raw materials increase proportionally with production volume. Manufacturing 1,000 units costs more in materials than producing 100 units.

Budget planning difference: Fixed expenses require allocation of exact known amounts. Variable expenses need estimated ranges based on expected usage or activity.

Understanding this distinction enables more accurate budget forecasting and better cash flow management across different spending scenarios.

How Fixed and Variable Expenses Interact in Cash Flow and Profitability

Fixed and variable expenses together determine total spending levels and available discretionary income or business profit margins.

Total monthly expenses equal the sum of all fixed expenses plus all variable expenses during that period. Both categories must be funded for budgets to remain functional.

Cash flow impact: Fixed expenses create baseline cash requirements that must be met regardless of income or revenue variations.

Variable expenses add volatility to cash flow needs. Months with high variable spending require more cash than months with controlled variable costs.

Business profitability depends heavily on the relationship between fixed costs, variable costs, and revenue. Higher fixed costs require higher revenue to reach break-even.

Profit margin: Revenue minus variable costs equals contribution margin. Contribution margin minus fixed costs determines net profit or loss.

Household budgets work similarly. Income minus variable expenses shows available funds. Available funds minus fixed expenses reveals true discretionary money or shortfalls.

Understanding this interaction helps identify whether financial problems stem from fixed expense overload, variable expense overspending, or insufficient income.

Is Paying Rent a Variable Expense in Your Budget?

Rent is a fixed expense, not a variable expense. Rent amount stays constant each month according to lease terms regardless of household usage.

Fixed expenses like rent do not change based on how much you use the property. Living in an apartment 10 days or 30 days costs the same monthly rent.

Contractual nature: Rent amounts are set by lease agreements for specific time periods, typically six to twelve months.

Some people confuse “controllable” with “variable.” While you can choose different rental properties, the rent itself remains fixed once the lease is signed.

Variable housing-related expenses include utilities, which change based on consumption. Rent itself is the fixed component of housing costs.

Budgeting treatment: Always allocate rent as a fixed expense with the exact monthly amount required by the lease agreement.

How to Budget for Variable Expenses Effectively

Budgeting for variable expenses requires forecasting expected amounts, monitoring actual spending, and adjusting allocations based on observed patterns and changing needs.

Step-by-Step Method to Budget Variable Expenses (Tracking, Forecasting, Averaging)

Effective variable expense budgeting follows a systematic process that combines historical data, realistic forecasting, and continuous monitoring.

Step 1: Track all variable expenses for at least two to three months to establish baseline spending patterns across categories.

Step 2: Calculate average spending per category by totaling tracked amounts and dividing by the number of months tracked.

Step 3: Identify seasonal patterns or irregular spikes that affect certain variable expense categories during specific months.

Step 4: Set initial budget amounts slightly above calculated averages to provide margin for unexpected increases or forecasting errors.

Step 5: Monitor actual spending against budgeted amounts weekly to catch overspending early before monthly allocations are exhausted.

Step 6: Adjust future month budgets based on observed patterns, changing needs, and accuracy of previous forecasts.

This process creates increasingly accurate variable expense budgets over time as data accumulates and patterns become clearer.

Practical Ways to Budget for Variable Expenses in Monthly and Quarterly Budgets

Monthly budgeting for variable expenses works well for regular household expenses like groceries, utilities, and gasoline that occur frequently.

Monthly approach: Allocate specific amounts to each variable category based on expected usage patterns during that particular month.

Quarterly budgeting suits variable expenses that occur irregularly or in unpredictable patterns throughout the year.

Combine monthly and quarterly approaches by budgeting high-frequency variables monthly and low-frequency variables quarterly for comprehensive coverage.

Practical technique: Use the envelope method by setting aside budgeted amounts for variable expenses when income arrives, preventing overspending.

Digital envelope systems work similarly by creating separate account buckets or categories within budgeting apps for each variable expense type.

Buffer amounts added to variable expense budgets protect against forecasting errors and unexpected cost increases during budget periods.

Adjustment mechanism: Review actual spending mid-month and reallocate funds between variable categories based on current consumption patterns.

Using Historical Data and Spending Trends to Predict Variable Costs

Historical spending data provides the foundation for accurate variable expense forecasting. Past patterns generally predict future spending behavior.

Review 6-12 months of transaction records to identify typical spending ranges for each variable expense category.

Calculation method: Add all spending in one category across all months, then divide by number of months to find average monthly cost.

Identify highest and lowest spending months for each category. This range reveals normal variability and helps set realistic budget bounds.

Seasonal patterns significantly affect some variable expenses. Summer electricity costs often exceed winter costs in hot climates due to air conditioning.

Trend analysis: Compare current year spending to previous year same-period spending to detect increasing or decreasing consumption trends.

Business variable costs benefit from correlation analysis between sales volume and variable expense levels to improve forecasting accuracy.

Historical data becomes more valuable over time as longer tracking periods reveal patterns that short-term data cannot show clearly.

Risk Mitigation: Managing Unexpected Variable Expenses

Unexpected variable expense increases represent significant budget risk. Planning for these events prevents budget failure when costs spike unpredictably.

Primary mitigation: Build budget buffers equal to 10-20% of total variable expense budgets to absorb unexpected increases.

Create sinking funds for semi-variable expenses that occur irregularly but predictably, like car maintenance or seasonal clothing purchases.

Maintain emergency funds separate from monthly budgets to cover truly unexpected costs that exceed buffer capacity.

Behavioral strategy: Review spending daily or weekly to detect cost increases early, allowing immediate budget adjustments before month-end.

Identify which variable expenses show highest volatility and allocate larger buffers to those categories specifically.

Reduce discretionary variable expenses immediately when essential variable expenses spike unexpectedly, shifting funds between categories to maintain overall budget.

Business approach: Use flexible budgeting techniques that automatically adjust variable expense allocations based on actual revenue or production levels achieved.

Tools, Worksheets, and Templates to Budget Fixed and Variable Expenses

Structured tools help organize expense tracking, categorization, and budget planning for both fixed and variable costs.

Using Budget Fixed and Variable Expenses Worksheets for Accuracy

Budget worksheets provide structured formats for listing all expenses, categorizing them correctly, and tracking actual spending against planned amounts.

Paper worksheets work well for people who prefer manual budgeting methods. Digital worksheets offer calculation automation and easier updates.

Worksheet structure: Include columns for expense name, category (fixed or variable), budgeted amount, actual spending, and variance.

List all fixed expenses first with exact amounts. List variable expenses second with estimated amounts based on historical averages.

Track actual spending in real-time or daily, recording amounts in the actual spending column as expenses occur.

Variance calculation: Subtract budgeted amount from actual spending to reveal overspending (positive variance) or underspending (negative variance).

Weekly worksheet reviews enable mid-period corrections before budgets break completely. Monthly reviews inform next month’s budget adjustments.

Budget Fixed and Variable Expenses Worksheet Answers for Personal Finance

Worksheet answers demonstrate proper expense categorization and realistic budget amount assignments based on typical household spending patterns.

Fixed expense example: Rent $1,200, car payment $350, insurance $150, internet $60 monthly with no variation expected.

Variable expense example: Groceries $500 (range $400-$600), utilities $120 (range $80-$180), gasoline $180 (range $120-$240).

Total fixed expenses equal the sum of all fixed line items. This amount represents minimum monthly spending regardless of consumption.

Total variable expenses equal the sum of all variable category budgets. This amount fluctuates based on actual usage patterns.

Buffer allocation: Add 15% buffer to total variable expenses to account for forecasting errors and unexpected cost increases.

Complete worksheet answers show income minus total fixed expenses minus total variable expenses equals remaining discretionary money or required spending reductions.

Excel and Digital Templates to Track Variable Expenses Efficiently

Excel templates enable formula-based calculations that automatically sum categories, calculate variances, and track spending trends over time.

Template features: Built-in formulas for totaling expenses, calculating percentages of income, and identifying categories exceeding budgets.

Digital templates sync across devices, allowing expense entry from phones, tablets, or computers as spending occurs throughout the day.

Conditional formatting highlights overspending categories in red, making budget problems immediately visible without manual review.

Chart integration: Templates can generate graphs showing spending trends, category breakdowns, and budget versus actual comparisons.

Cloud-based templates enable shared access for household members, allowing multiple people to enter expenses and view budget status.

Template customization allows adding or removing categories, adjusting time periods, and creating personalized views matching individual budgeting preferences.

Automating Expense Tracking with Apps and Accounting Software

Budgeting apps automatically categorize transactions, track spending against budgets, and alert users when categories approach or exceed limits.

Personal apps: YNAB, Mint, EveryDollar, and Goodbudget offer variable expense tracking with category budgets and real-time spending updates.

Business accounting software like QuickBooks, FreshBooks, and Wave automatically categorizes variable expenses and generates expense reports.

Automation reduces manual entry effort by connecting directly to bank accounts and credit cards to import transactions automatically.

App benefits: Real-time spending visibility, automatic categorization learning, budget alerts, and historical trend analysis without manual calculations.

Some apps use envelope budgeting methods specifically designed for variable expense management, allocating specific amounts to each category.

Choose apps that clearly separate fixed and variable expenses, provide customizable categories, and offer forecasting based on historical patterns.

Calculations and Formulas for Variable Expense Management

Mathematical formulas help quantify variable expense behavior, measure cost efficiency, and identify spending problems requiring correction.

Variable Expense Ratio: Definition and Calculation

Variable expense ratio measures variable expenses as a percentage of total income or revenue during specific periods.

Formula: Variable Expense Ratio = (Total Variable Expenses ÷ Total Income) × 100

This ratio shows what portion of income goes toward variable costs. Lower ratios indicate more income available for savings or fixed obligations.

Example: $1,200 variable expenses ÷ $4,000 income × 100 = 30% variable expense ratio

Tracking this ratio monthly reveals whether variable spending is increasing or decreasing relative to income changes.

Business variable expense ratios compare variable costs to revenue. Lower ratios mean higher contribution margins available to cover fixed costs.

Interpretation: Variable expense ratios above 50% in personal budgets often indicate spending control problems requiring immediate attention.

Variable Expense Per Unit Formula for Business Budgeting

Variable expense per unit calculates average variable cost required to produce or deliver one unit of product or service.

Formula: Variable Expense Per Unit = Total Variable Expenses ÷ Number of Units Produced

This metric helps businesses understand cost behavior and set pricing that covers both variable and fixed expenses.

Example: $5,000 variable expenses ÷ 1,000 units produced = $5.00 variable expense per unit

Tracking per-unit variable expenses reveals cost changes over time and identifies efficiency improvements or cost increases requiring investigation.

Lower variable expenses per unit improve profit margins on each sale, increasing overall profitability at any given revenue level.

Application: Use per-unit variable expenses to calculate break-even points and determine minimum pricing needed to cover all costs.

Using Flexible Budget Variance to Identify Overspending on Variable Expenses

Flexible budget variance compares actual variable expenses to what variable expenses should have been given actual activity levels achieved.

Formula: Flexible Budget Variance = Actual Variable Expenses – (Budgeted Variable Expense Per Unit × Actual Units)

Positive variances indicate variable expenses exceeded expected amounts based on actual production or consumption levels achieved.

Example: Actual $6,000 – (Budgeted $5 per unit × 1,000 actual units) = $1,000 unfavorable variance

Unfavorable flexible budget variances signal cost control problems, price increases from suppliers, or waste in variable expense categories.

Favorable variances show variable expenses came in lower than expected, indicating cost savings, efficiency improvements, or reduced consumption.

Management use: Investigate large variances to identify root causes and implement corrective actions for future periods.

An Unfavorable Flexible-Budget Variance for Variable Expenses Indicates What?

An unfavorable flexible-budget variance for variable expenses indicates actual variable costs exceeded budgeted amounts adjusted for actual activity levels.

This variance signals potential problems like increased supplier prices, reduced efficiency, waste, or poor cost control during the period.

Root causes: Price increases, overconsumption, waste, theft, or measurement errors can all create unfavorable variable expense variances.

Unfavorable variances require investigation to determine whether causes are temporary or permanent, controllable or external.

Temporary variances from one-time events may not require budget changes. Permanent increases need budget adjustments to reflect new cost realities.

Action requirement: Unfavorable variances exceeding 10% of budgeted amounts generally warrant immediate investigation and corrective action.

Budgeting Strategies for Common Variable Expenses

Different variable expense types require tailored budgeting approaches based on consumption patterns, predictability levels, and control mechanisms.

Grocery and Household Expenses: Tracking and Planning

Grocery expenses represent highly controllable variable costs that respond directly to shopping frequency, meal choices, and purchasing decisions.

Budgeting approach: Set weekly grocery budgets rather than monthly amounts to maintain tighter control over this frequent variable expense.

Track all grocery spending immediately after shopping trips. Compare cumulative weekly totals against weekly budgets to catch overspending early.

Meal planning reduces grocery costs by eliminating impulse purchases and reducing food waste from buying items without specific usage plans.

Cost control: Shopping with lists, avoiding hungry shopping, and comparing unit prices reduces grocery spending without sacrificing nutrition.

Household supplies like cleaning products and paper goods follow similar patterns. Budget these separately or combine with groceries based on preference.

Seasonal variation affects grocery costs through produce price changes and holiday meal preparation. Adjust budgets for months with known seasonal increases.

Utilities and Bills: Seasonal and Usage Variability Management

Utility bills vary based on consumption, weather patterns, and seasonal factors that change throughout the year predictably.

Budgeting method: Use 12-month average utility costs as monthly budget amounts, then save surplus during low months for high months.

Electricity costs often peak during summer or winter depending on climate. Natural gas usage typically increases during winter heating months.

Water and sewer bills may vary based on irrigation, pool maintenance, or seasonal landscaping needs in addition to household consumption.

Smoothing technique: Budget billing programs offered by utilities charge the same amount monthly, eliminating seasonal variability from monthly budgets.

Track actual usage patterns separately from costs to identify consumption changes versus rate increases as causes of bill changes.

Energy efficiency improvements reduce variable utility costs permanently, lowering both consumption and associated expenses over time.

Travel and Leisure Expenses with Variable Pricing

Travel expenses fluctuate based on trip frequency, destinations, timing, and transportation choices, making them highly variable.

Budgeting approach: Use sinking funds for planned trips, setting aside monthly amounts toward future travel rather than budgeting trips monthly.

Daily travel costs like gasoline vary with vehicle usage, fuel prices, and driving patterns. Track mileage and fuel consumption to forecast accurately.

Vacation travel represents irregular large expenses that break monthly budgets if not planned in advance through dedicated savings.

Cost management: Booking travel during off-peak periods, comparing transportation options, and using rewards programs reduces variable travel costs.

Leisure activities like dining out, entertainment, and hobbies create pure discretionary variable expenses controllable through behavioral choices.

Set maximum spending limits for discretionary leisure categories. Stop spending when limits are reached regardless of month remaining.

Clothing, Entertainment, and Subscription Expenses

Clothing purchases vary seasonally and based on need replacement cycles, growth for children, and lifestyle changes.

Budgeting strategy: Annual clothing budgets divided by 12 provide monthly allocations that smooth irregular purchasing patterns.

Entertainment expenses including streaming services, events, and activities range from fixed subscriptions to variable one-time purchases.

Audit subscription services quarterly to eliminate unused services that create recurring fixed or variable expenses without delivering value.

Control mechanism: Implement waiting periods before discretionary variable purchases to reduce impulse spending that breaks budgets.

Subscription services occupy a middle ground between fixed and variable expenses. They recur predictably but can be canceled, making them semi-variable.

Composite Budgeting Approaches: Fixed and Variable Expenses Together

Comprehensive budgeting methods integrate both fixed and variable expenses into unified systems that address total spending holistically.

Zero-Based Budgeting for Fixed + Variable Expenses

Zero-based budgeting assigns every dollar of income to specific expense categories, savings, or debt payments, leaving zero unallocated.

Method: List all fixed expenses first with exact amounts. Allocate remaining income to variable expense categories based on priorities.

Every dollar gets assigned before the month begins. This prevents unplanned spending of leftover money after fixed expenses are covered.

Variable expenses receive specific allocations rather than unlimited spending until money runs out. This creates hard limits on variable categories.

Implementation: Income minus fixed expenses minus variable budgets minus savings equals zero when properly balanced.

Zero-based budgeting works especially well for variable expense control by making spending limits explicit rather than implied.

Adjust variable category allocations throughout the month by moving money between categories while maintaining the zero-based framework.

50/30/20 Budget Framework Incorporating Variable Costs

The 50/30/20 budget allocates 50% of income to needs, 30% to wants, and 20% to savings or debt payments.

Fixed vs variable: Needs category includes both fixed essentials like rent and variable essentials like groceries and utilities.

Wants category contains discretionary variable expenses like entertainment, dining out, and non-essential purchases.

This framework provides flexibility in managing variable expenses within percentage guardrails rather than tracking individual categories.

Application: Calculate 50% of after-tax income. Ensure all essential fixed and variable expenses fit within this limit.

Remaining 30% for wants allows discretionary variable spending without tracking every transaction, simplified budgeting for some people.

The 20% savings portion creates automatic financial progress regardless of variable expense fluctuations within allowed percentages.

Pay-Yourself-First Method for Balancing Fixed and Variable Expenses

Pay-yourself-first budgeting prioritizes savings by allocating specified amounts to savings before budgeting other expenses.

Process: Automatically transfer savings amounts when income arrives. Budget fixed and variable expenses from remaining funds.

This method ensures financial goals receive funding even when variable expenses increase unexpectedly during budget periods.

Variable expenses get squeezed when income is limited after savings and fixed expenses are covered, creating automatic spending discipline.

Advantage: Savings become effectively fixed expenses through automation, removing them from variable spending temptation.

Works best when combined with buffer funds that prevent savings withdrawals when variable expenses spike temporarily.

Briefly Summarize the Four Approaches to Budgeting for Variable Expenses

Four main approaches organize variable expense budgeting through different frameworks suited to various financial situations and preferences.

Envelope budgeting: Allocate specific cash or digital amounts to each variable category, stopping spending when envelopes empty.

Average-based budgeting: Use historical averages as monthly budgets, adjusting over time as patterns change or needs evolve.

Percentage budgeting: Allocate fixed percentages of income to variable categories, automatically scaling spending with income changes.

Flexible budgeting: Adjust variable expense budgets based on actual activity levels, income variations, or changing circumstances.

Each approach offers different balances between control, flexibility, and administrative complexity in managing variable expenses.

Practical Tips and Behavioral Changes to Reduce Variable Expenses

Reducing variable expenses requires both tactical cost-cutting actions and behavioral changes that modify consumption patterns over time.

Negotiating with Suppliers or Vendors for Lower Costs

Many variable expenses can be reduced through negotiation with service providers, vendors, or suppliers.

Negotiation targets: Insurance premiums, utility rates, subscription services, and service contracts often have negotiable pricing or discount programs.

Contact providers annually to request rate reviews, loyalty discounts, or competitive matching against alternative providers.

Business variable expenses like shipping costs, raw material prices, and transaction fees may decrease through volume discounts or contract renegotiation.

Timing strategy: Negotiate near contract renewal dates when providers are most motivated to retain customers rather than lose them.

Research competitive pricing before negotiations to demonstrate knowledge of market rates and strengthen negotiating positions.

Bundling services with single providers sometimes reduces total costs compared to purchasing services separately from multiple vendors.

Employee or Household Involvement in Identifying Cost Savings

Involving all household members or employees in cost awareness increases identification of waste and improves spending discipline.

Participation method: Share budget status regularly, explain financial goals, and request input on reducing variable expenses.

People who understand why spending reductions matter tend to modify behaviors more willingly than those excluded from financial decision-making.

Children can participate age-appropriately by understanding household budgets and making consumption choices that support family financial goals.

Business application: Employee suggestion programs that reward cost-saving ideas reduce variable expenses while increasing employee engagement.

Transparency about variable expense budgets creates shared responsibility rather than single-person burden for staying within limits.

Lifestyle Adjustments: Dining Out, Shopping, and Subscriptions

Dining out represents a highly variable expense that responds immediately to behavioral changes without affecting essential needs.

Reduction strategy: Set maximum monthly restaurant visit limits. Pack lunches for work instead of eating out daily.

Shopping behavior modifications include implementing 24-hour waiting periods before non-essential purchases to reduce impulse buying.

Subscription audits identify services no longer used or valued. Cancel subscriptions that don’t deliver value proportional to their cost.

Habit change: Replace expensive variable habits with lower-cost alternatives that provide similar satisfaction at reduced expense.

Lifestyle adjustments require balancing financial goals against quality of life. Extreme cuts often fail due to unsustainability.

Gradual reductions in discretionary variable expenses tend to last longer than dramatic cuts that feel punishing or unsustainable.

Using Cashback and Rewards Programs to Offset Variable Expenses

Cashback programs and rewards effectively reduce net variable expenses when used strategically without increasing spending.

Program types: Credit card cashback, store loyalty programs, and app-based reward systems return portions of spending as credits.

Maximize rewards by using cashback cards for variable expenses already budgeted rather than increasing spending to earn rewards.

Grocery rewards programs often offer fuel discounts or cashback that directly offset other variable expenses.

Warning: Rewards programs only reduce expenses if used for planned purchases. Spending more to earn rewards increases total expenses.

Calculate whether annual fee cards provide sufficient rewards to offset fees based on actual variable spending patterns.

Redeem rewards regularly to offset variable expenses or fund buffer accounts rather than accumulating unused rewards.

How Variable Expenses Impact Long-Term Financial Goals

Variable expense management directly affects achievement of financial goals by controlling how much money remains available for saving and investing.

Building Emergency Funds to Absorb Variable Expense Fluctuations

Emergency funds provide financial buffers that prevent variable expense spikes from derailing budgets or creating debt.

Fund purpose: Cover unexpected increases in variable expenses like car repairs, medical costs, or home maintenance without borrowing.

Target emergency fund size of 3-6 months’ worth of essential expenses, including both fixed and average variable expenses.

Build emergency funds gradually by allocating portions of income to savings until target amounts are reached over time.

Relationship to budgets: Strong emergency funds reduce pressure on monthly budgets by handling irregular large expenses outside normal variable allocations.

Without emergency funds, variable expense spikes force either debt accumulation or cutting essential spending from current budgets.

Separate buffer funds for expected variable expense volatility from true emergency funds reserved for major unexpected events.

Planning for Retirement, College, or Major Purchases with Variable Costs

Long-term financial goals require consistent contributions that variable expense volatility can disrupt if not managed properly.

Impact mechanism: High variable expenses reduce discretionary income available for retirement contributions, college savings, or major purchase funds.

Controlling variable expenses creates consistent surplus that can be directed toward long-term goals month after month.

Retirement planning requires decades of consistent saving. Variable expense control prevents interruptions in contribution consistency that harm long-term accumulation.

College savings: Regular contributions to education savings accounts depend on maintaining variable expenses within planned limits.

Major purchase planning through sinking funds requires consistent monthly deposits that variable expense overspending can prevent.

How Variable Expenses Affect Your Budget and Financial Stability

Variable expenses create budget uncertainty that requires planning margins, buffer funds, and adaptive management strategies.

Budgets with high percentages of variable expenses show more month-to-month volatility than budgets dominated by predictable fixed expenses.

Stability factor: Financial stability increases when variable expenses are controlled, predictable, and represent smaller portions of total spending.

Uncontrolled variable expenses create cascading problems including debt accumulation, missed savings goals, and reduced emergency fund building.

High variable expense ratios leave budgets vulnerable to unexpected increases that can quickly exhaust available income.

Measurement: Calculate variable expenses as percentage of total income. Ratios above 40-50% often indicate stability risks.

Monitoring and Adjusting Budgets Monthly or Quarterly

Regular budget reviews enable adjustments based on changing circumstances, income variations, or observed spending pattern changes.

Monthly review process: Compare actual variable expenses to budgets. Identify categories with consistent over or under-spending.

Adjust future month budgets based on observed patterns rather than maintaining unrealistic budgets that consistently fail.

Quarterly reviews identify seasonal patterns and trends that monthly reviews might miss in short-term noise.

Adjustment criteria: Change budgets when three consecutive months show consistent variance in the same direction for specific categories.

Life changes like household size changes, job changes, or relocations require immediate budget recalculations rather than waiting for review cycles.

Flexible budgeting approaches that adapt to reality tend to succeed more consistently than rigid budgets that ignore changing circumstances.

FAQs – Variable and Fixed Expenses in Personal and Small Business Budgets

What is a Variable Expense vs Fixed Expense?

A variable expense changes in amount from period to period based on usage, consumption, or activity levels. A fixed expense remains constant within budget periods regardless of usage variations.

Variable expenses respond to behavioral changes and consumption decisions. Fixed expenses are contractual or recurring obligations with set amounts.

Examples: Groceries are variable—spending more increases costs. Rent is fixed—using the apartment more does not increase monthly rent.

Examples of Variable Expenses in a Personal Budget

Common personal variable expenses include groceries, utilities, gasoline, entertainment, dining out, clothing, personal care, and household supplies.

Each of these expense categories varies month-to-month based on consumption levels, purchasing decisions, and lifestyle choices.

Business examples: Cost of goods sold, raw materials, sales commissions, shipping costs, and transaction fees all vary with business activity.

Should Variable Expenses Be Included in a Budget?

Yes, variable expenses must be included in budgets. Essential variable expenses like food and utilities represent mandatory spending despite fluctuating amounts.

Budgets that exclude variable expenses fail to reflect actual spending and provide incomplete financial planning.

Budget method: Include variable expenses using estimated amounts based on historical averages, seasonal patterns, and expected consumption during budget periods.

How Do You Track and Adjust Variable Expenses in a Budget?

Track variable expenses by recording all spending in each category as it occurs, using apps, worksheets, or receipt systems.

Compare actual spending to budgeted amounts weekly or bi-weekly to identify categories exceeding allocations before month-end.

Adjustment process: When variable expenses consistently exceed budgets, increase future allocations to realistic levels based on observed patterns.

When income decreases or fixed expenses increase, reduce variable expense budgets in discretionary categories to maintain budget balance.

Use mid-month budget adjustments to shift money between variable categories based on actual consumption patterns observed during the current period.

What Are Some Practical Ways to Budget for Variable Expenses?

Practical variable expense budgeting combines historical tracking, realistic forecasting, and active monitoring throughout budget periods.

Cash envelope method: Withdraw budgeted cash amounts for variable categories at month start. Spend only cash allocated, preventing overspending.

Digital envelope apps replicate this method electronically, creating virtual category limits that prevent spending beyond allocated amounts.

Average-based budgeting uses 3-6 month spending averages as baseline budgets, then adjusts for known seasonal variations or life changes.

Percentage allocation: Assign fixed percentages of income to variable categories. This automatically scales budgets when income fluctuates.

Build sinking funds for irregular but predictable variable expenses like car maintenance, saving monthly amounts toward expected future costs.

Track spending daily or weekly rather than monthly to maintain awareness and enable quick corrections when categories approach limits.

Buffer strategy: Add 10-15% margin to calculated average budgets, providing cushion for unexpected increases without breaking overall budget.

How to Make a Budget with Variable and Non-Variable Expenses

Creating comprehensive budgets requires systematically listing all income sources, categorizing expenses correctly, and allocating amounts appropriately.

Step 1: List all monthly income sources with exact after-tax amounts expected during the budget period.

Step 2: List all fixed expenses with exact amounts due, including rent, loan payments, insurance, and subscriptions.

Step 3: Calculate total fixed expenses by summing all items in the fixed category.

Step 4: List variable expense categories with estimated amounts based on historical averages or expected consumption.

Step 5: Calculate total variable expenses by summing all variable category budgets.

Step 6: Add fixed and variable totals. Compare to total income to verify expenses don’t exceed available funds.

Step 7: Adjust variable category allocations if total expenses exceed income, prioritizing essential variables over discretionary ones.

Step 8: Allocate any remaining income to savings, debt reduction, or buffer funds after all expenses are covered.

This systematic process ensures all expense types receive appropriate budget allocations based on their characteristics and importance.

Common Variable Expenses in Monthly Budgets

Identifying common variable expense categories helps ensure comprehensive budget coverage without omitting significant spending areas.

Food category: Groceries, dining out, coffee shops, and food delivery services all vary based on consumption choices.

Utilities: Electricity, natural gas, water, and sewer charges fluctuate based on usage and seasonal factors.

Transportation: Gasoline, parking fees, tolls, and ride-sharing costs vary with travel frequency and fuel prices.

Personal care: Haircuts, cosmetics, toiletries, and grooming services occur irregularly with varying costs.

Healthcare: Copays, prescriptions, and over-the-counter medications vary based on health needs during specific months.

Household: Cleaning supplies, maintenance items, and home repairs represent variable household operating costs.

Entertainment: Movie tickets, streaming rentals, events, and recreational activities create discretionary variable spending.

Clothing: Apparel purchases vary seasonally and based on need replacement cycles or style preferences.

Budgeting for Travel Expenses with Variable Pricing

Travel expenses show high variability based on timing, destination choices, booking methods, and travel frequency patterns.

Gasoline budgeting: Track mileage and fuel efficiency to forecast monthly gasoline needs based on expected driving patterns.

Fuel price fluctuations affect gasoline expenses independent of consumption. Monitor local prices and adjust budgets when significant changes occur.

Vacation travel requires separate planning from routine transportation. Use sinking funds that accumulate monthly toward planned trips.

Booking strategy: Advance booking and price comparison tools reduce travel costs for flights, hotels, and rental cars.

Seasonal pricing affects travel costs significantly. Off-peak travel delivers identical experiences at lower variable costs.

Business travel budgeting requires separating reimbursable travel from personal travel to accurately track actual expenses borne.

Mileage tracking: Record business mileage for tax deductions and expense reimbursement separate from personal vehicle operating costs.

Personal Budget Variable Expenses Examples

Real-world examples demonstrate how variable expenses appear in actual personal budgets across different household situations.

Single person example: Groceries $300, utilities $100, gasoline $150, entertainment $100, dining out $150, personal care $50.

Family example: Groceries $800, utilities $220, gasoline $300, childcare supplies $150, family entertainment $200, clothing $150.

Retiree example: Groceries $400, utilities $150, gasoline $80, healthcare copays $100, hobbies $120, dining out $180.

Each household shows different variable expense patterns based on size, lifestyle, location, and life stage factors.

Income relationship: Variable expenses typically consume 30-50% of household income depending on fixed expense levels and savings rates.

Tracking actual variable expenses reveals personalized patterns that differ from generic budget templates found online.

What Are Variable Expenses in a Budget (Complete List)

Comprehensive variable expense lists help identify all categories requiring budget allocations and tracking systems.

Essential variable expenses: Groceries, utilities, gasoline, prescriptions, household supplies, basic clothing, and essential maintenance.

Semi-essential variables: Phone charges beyond base plans, internet usage fees, basic personal care, and minimum entertainment.

Discretionary variables: Dining out, premium entertainment, hobby spending, non-essential shopping, luxury personal care, and elective travel.

Business variable expenses: Cost of goods sold, raw materials, packaging, shipping, sales commissions, transaction fees, and marketing costs.

Irregular variables: Car repairs, home maintenance, medical procedures, seasonal expenses, and annual fees spread across months.

Different households prioritize categories differently. Essential for one family may be discretionary for another based on circumstances and values.

Budget Fixed vs Variable Expenses (Complete Comparison)

Understanding precise differences between fixed and variable expenses enables accurate categorization and appropriate budgeting strategies.

Response to usage: Fixed expenses remain constant regardless of usage levels. Variable expenses change proportionally with consumption.

Predictability: Fixed expenses are highly predictable with exact known amounts. Variable expenses require estimation despite historical patterns.

Control mechanism: Fixed expenses change through contract renegotiation or service cancellation. Variable expenses adjust immediately through behavior changes.

Budget allocation: Fixed expenses get exact amount allocations. Variable expenses receive estimated ranges with buffer margins.

Time stability: Fixed expenses stay constant for contract periods. Variable expenses fluctuate month-to-month within categories.

Planning horizon: Fixed expenses enable long-term planning certainty. Variable expenses require adaptive short-term management.

Cash flow impact: Fixed expenses create baseline cash requirements. Variable expenses add volatility requiring buffer funds.

Semi-Variable Expenses Explained

Semi-variable expenses contain both fixed and variable components, requiring hybrid budgeting approaches.

Definition: Semi-variable expenses include a base fixed amount plus variable charges based on usage above baseline levels.

Phone bills often work this way—fixed monthly service charge plus overage fees for exceeding plan limits.

Business examples: Employee compensation with base salary (fixed) plus commission (variable), or electricity with minimum service charge plus usage fees.

Utility bills may have fixed connection fees plus variable consumption charges calculated per unit used.

Budgeting approach: Budget the fixed component as a fixed expense. Budget the variable component based on expected usage patterns.

Credit card minimum payments are fixed obligations. Amounts above minimums paid are variable choices affecting debt reduction speed.

Semi-variable expenses require attention to both components—managing the fixed baseline through service selection and variable portion through usage control.

How to Reduce Variable Expenses Without Sacrificing Quality of Life

Sustainable variable expense reduction balances financial goals with maintaining reasonable life satisfaction and avoiding extreme deprivation.

Substitution strategy: Replace expensive variable expenses with lower-cost alternatives providing similar benefits—home movies instead of theaters.

Gradual reduction prevents shock and allows adjustment to new spending patterns—reduce dining out from 12 to 8 times monthly.

Value analysis: Evaluate which variable expenses deliver highest satisfaction per dollar spent. Eliminate low-value spending first.

Negotiate better rates on unavoidable variable expenses like insurance or subscription services before cutting consumption.

Batch activities: Combine errands to reduce gasoline consumption. Bulk cooking reduces per-meal food costs.

Free or low-cost entertainment alternatives exist for most paid entertainment—libraries, parks, community events, and free museums.

Timing strategy: Shop sales cycles, use coupons strategically, and make seasonal purchases during discount periods.

Quality of life depends more on overall life satisfaction than individual expense categories. Smart cuts maintain happiness while reducing costs.

Summary

Budgeting for variable and fixed expenses requires understanding how each expense type behaves and applying appropriate management strategies.

Fixed expenses provide budgeting stability through predictable amounts. Variable expenses create flexibility but require active monitoring and control.

Core principle: Track spending patterns, forecast variable expenses using historical data, build buffers for volatility, and adjust budgets based on reality.

Effective variable expense management enables achievement of financial goals by ensuring discretionary income remains available for saving and investing.

Both expense types require attention—fixed expenses through periodic review and renegotiation, variable expenses through continuous tracking and behavioral adjustment.

Implementation strategy: Start with 2-3 months of expense tracking to establish baselines. Create realistic budgets slightly above averages to allow margins.

Build small buffer funds equal to 10-20% of variable expense budgets. This cushion prevents budget failure from forecasting errors.

Review budgets monthly and adjust based on observed patterns rather than maintaining unrealistic targets that consistently fail.

Success comes from balancing control without rigidity, using tools that match personal preferences, and adjusting approaches as circumstances change.

Variable expenses affect every budget. Managing them well tends to improve overall financial stability and reduce month-to-month financial stress.

Long-term benefit: Controlled variable expenses create consistent surplus for emergency funds, retirement savings, and major purchase planning.

Financial stability develops gradually through persistent attention to both fixed and variable expense management over extended time periods.