Table of Contents

Contents are generated from article headings.

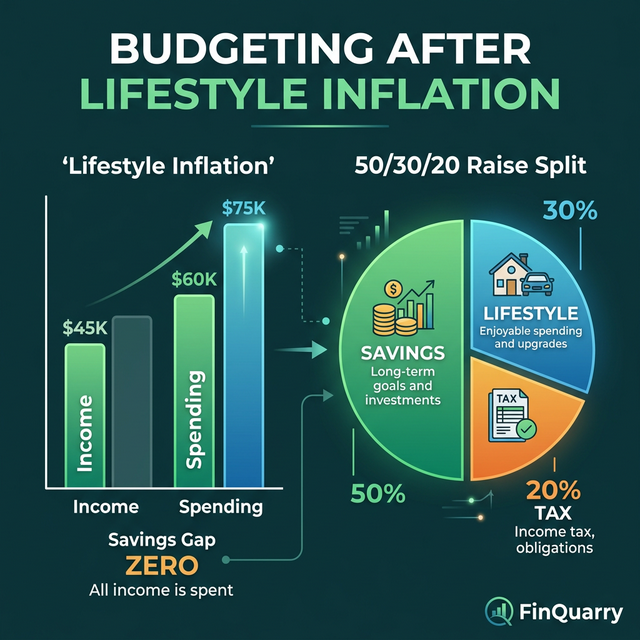

Lifestyle inflation is the gradual, often unconscious increase in spending that accompanies income growth — producing the paradox where a person earning $75,000 feels as financially constrained as they did earning $45,000. Lifestyle inflation does not require extravagance. It operates through incremental upgrades: slightly nicer restaurants, slightly higher grocery quality, a slightly better apartment, one more subscription — each individually reasonable, collectively consuming the entire raise.

A CNBC survey found that one-third of households earning $200,000+ report living paycheck to paycheck. This is not a spending control failure — it is lifestyle inflation operating at scale.

This content discusses lifestyle inflation and recovery budgeting using behavioral economics and consumer finance data. Individual spending patterns, income trajectories, and cost of living vary. FinQuarry provides informational content only — this does not constitute personalized financial advice.

How Lifestyle Inflation Happens

The Invisible Upgrade Path

No single purchase signals lifestyle inflation. The mechanism: a $15/month increase in coffee quality, a $200/month increase in dining frequency, a $300/month increase in housing when the lease renews, a $50/month increase in grocery quality. Each decision is individually rational and subjectively justified. Collectively: $565/month or $6,780/year of spending expansion that exactly absorbed the last raise — producing zero additional savings despite meaningfully higher income.

The Hedonic Adaptation Trap

Behavioral economics describes hedonic adaptation: satisfaction from a purchase or upgrade returns to baseline within 2–6 months. The nicer apartment provides elevated satisfaction for weeks — then becomes the new normal. The upgraded car produces excitement for months — then becomes “just the car.” Each adaptation requires the next upgrade to restore satisfaction, creating an escalating baseline that income struggles to sustain.

The Selective Deflation Strategy

Reversing lifestyle inflation does not require returning to a previous standard of living. It requires identifying which upgrades produce lasting satisfaction and which were absorbed without conscious recognition.

The Satisfaction Test

Review the last 3 years of spending increases. For each upgrade, ask: “If this were removed tomorrow, would I genuinely miss it or barely notice?”

Common results:

- Would miss: Better food quality, gym membership, reliable car ($0 reversion value — keep these)

- Would barely notice: Premium streaming tier versus basic ($10/month savings), delivery versus pickup ($40–60/month savings), convenience grocery versus planned shopping ($80–120/month savings)

Most people discover that 30–50% of accumulated lifestyle inflation can be reversed without meaningful satisfaction reduction.

The Selective Downgrade

Not “cut everything” but “cut what you don’t notice.” Downgrade the streaming bundle ($30 to $15). Switch from delivery to pickup twice weekly ($80/month savings). Comparison shop insurance annually ($50–100/month savings). Cook one additional meal per week ($60/month savings).

Total recovery from selective downgrade: $200–350/month redirected to savings or debt — without feeling deprived.

The Raise Allocation Rule

Prevent future lifestyle inflation by pre-committing raises before they arrive:

The 50/30/20 raise split: 50% of every raise goes to savings/debt, 30% funds intentional lifestyle improvement, 20% covers tax increase and inflation.

A person receiving a $500/month raise allocates: $250 to increased auto-savings, $150 to one deliberate upgrade (chosen, not drifted into), $100 to tax and inflation adjustment. This produces genuine financial progress from income growth — which full lifestyle inflation would have consumed entirely.

The Lifestyle Audit

Step 1: Compare Current Spending to Two-Year-Ago Spending

Pull spending data from 24 months ago and compare category by category to current. The delta reveals exactly where lifestyle inflation occurred and its magnitude.

Step 2: Rank Upgrades by Satisfaction

Each identified upgrade receives a satisfaction ranking: essential (produces daily value), appreciated (produces weekly value), forgotten (cannot articulate the benefit). Target forgotten upgrades for removal first.

Step 3: Redirect Recovered Spending

Every dollar recovered from lifestyle deflation must be redirected to a specific target — emergency fund, debt payoff, investment contributions, sinking funds. Recovered spending without redirection will be re-absorbed into lifestyle within 90 days.

Is Lifestyle Inflation Always Bad?

No. Intentional lifestyle improvement — spending more on things that genuinely increase life quality — is a legitimate use of income growth. The problem is unintentional lifestyle inflation: spending that grew without decision, consumed the raise without awareness, and produced no lasting satisfaction. The distinction is consciousness: did you choose the upgrade, or did it just happen?

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry