Table of Contents

Contents are generated from article headings.

When a parent dies, adult children generally are not responsible for their parents’ debt. In most cases, outstanding debt becomes the legal obligation of the deceased person’s estate, not their surviving family members. The estate uses available assets to pay creditors during probate, and if the estate lacks sufficient funds to cover all debts, most remaining obligations are written off rather than transferred to heirs.

However, specific situations create exceptions to this general rule. Children may become personally liable if they cosigned loans, held joint accounts with the deceased parent, or live in one of the states with filial responsibility laws that apply to certain medical debts. Additionally, voluntary actions such as agreeing to pay a debt or making partial payments can sometimes create legal responsibility where none previously existed.

Understanding the distinction between being an heir to an estate and being legally liable for debt is critical for protecting personal finances after a parent’s death. This guide explains how debt is handled after death, when liability passes to surviving family members, and what actions to take, or avoid, when creditors make contact.

1. How Debt Is Handled After a Parent Dies (Estate Basics)

When a parent dies, their financial obligations do not automatically transfer to children or other family members. Instead, debt becomes a claim against the deceased person’s estate, which consists of all assets and liabilities left behind at death.

1.1 What Happens to Debt When Someone Dies

Debt remains the legal responsibility of the person who incurred it, even after death. When someone dies, their debts become claims against their estate rather than obligations of surviving family members. Creditors must file claims with the estate during probate to recover money owed, and these claims are paid from estate assets according to state-specific priority rules. If the estate cannot pay all debts in full, creditors typically receive partial payment or nothing, depending on available funds and claim priority.

1.2 What an Estate Is and Why It Matters

An estate consists of all assets and liabilities a person owns at the time of death, including bank accounts, real property, personal belongings, and outstanding debts. The estate serves as a legal entity during probate that holds assets and settles obligations before distributing remaining property to heirs or beneficiaries. Assets that pass outside probate—such as life insurance proceeds, payable-on-death accounts, and transfer-on-death accounts—generally bypass the estate and are not available to creditors for debt collection.

1.3 How Probate Determines Who Gets Paid First

Probate is the legal process through which a court oversees estate administration, validates the will if one exists, and ensures debts are paid before heirs receive assets. During probate, the executor or personal representative notifies creditors of the death and establishes a creditor claim period, typically ranging from four to six months depending on state law. Creditors who file valid claims within this timeframe are paid according to state priority rules, which generally place funeral expenses, estate administration costs, and tax obligations ahead of unsecured debts like credit cards.

1.4 What Happens If the Estate Has More Debt Than Assets (Insolvent Estate)

An insolvent estate occurs when total debts exceed the value of all estate assets available to pay creditors. When insolvency exists, the executor pays claims according to state priority order until estate funds are exhausted, at which point remaining creditors receive nothing. Unpaid creditors generally cannot pursue heirs or beneficiaries for the shortfall unless those individuals have separate legal obligations such as cosigning or joint account ownership. Most unsecured debts, including credit card balances and medical bills, are discharged when an insolvent estate closes without full payment.

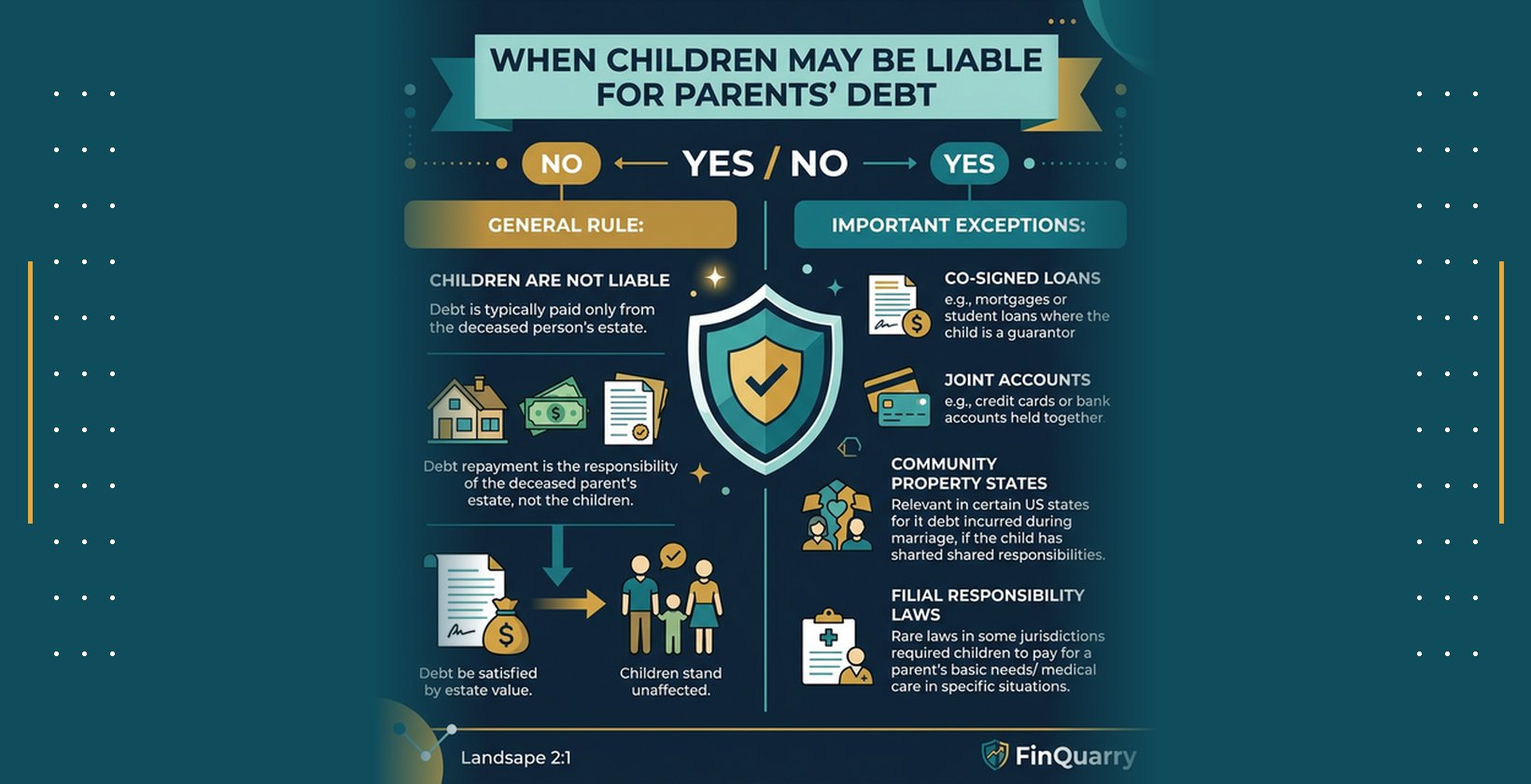

2. Are Children Automatically Responsible for Their Parents’ Debt? (General Rule)

The default legal principle in the United States is that children do not inherit their parents’ debt obligations. This principle protects adult children from automatic liability for debts they did not personally incur or contractually agree to pay.

2.1 Why Adult Children Usually Do NOT Inherit Debt

Adult children are not automatically responsible for a parent’s debt because debt is a contractual obligation between the creditor and the borrower only. Unless a child signed a loan agreement, credit application, or other binding contract, they have no legal duty to repay the parent’s obligations. The estate bears responsibility for settling debts, and once probate concludes, unpaid debts from an insolvent estate are typically written off by creditors rather than pursued against family members.

2.2 Difference Between Being an Heir and Being Liable

Being an heir means a person is entitled to inherit assets from an estate, while being liable means having a legal obligation to repay debt. These roles are legally distinct and do not overlap unless a specific contractual relationship exists. Heirs receive assets remaining after the estate pays valid debts and expenses, but they do not assume responsibility for debts that exceed estate assets. This distinction protects heirs from creditor claims beyond the value of assets they actually receive.

2.3 Moral Responsibility vs Legal Responsibility

Creditors sometimes appeal to a sense of moral obligation or family duty when contacting surviving relatives about unpaid debts. However, moral pressure does not create legal liability. Legal responsibility arises only from contractual agreements, joint ownership, cosigning, or specific state laws such as filial responsibility statutes. Heirs should understand that feeling morally compelled to pay a parent’s debt does not mean they are legally required to do so, and voluntary payments can sometimes create unintended legal consequences.

2.4 What Creditors Are Allowed — and NOT Allowed — to Do

Creditors may contact the executor or personal representative of an estate to file claims and request payment from estate assets. However, the Fair Debt Collection Practices Act (FDCPA) restricts debt collectors from misleading heirs about their legal obligations or implying that family members are responsible for debts they did not cosign. Creditors cannot threaten to sue heirs for a deceased parent’s debt unless the heir has a separate legal obligation, and they must provide debt validation if requested. Violating these rules can result in penalties and legal action against the debt collector.

3. The Exact Situations Where You MAY Be Responsible for Your Parents’ Debt

While the general rule protects children from inheriting parental debt, specific legal and financial relationships create exceptions where personal liability does arise.

3.1 Cosigning a Loan: When Debt Becomes Yours

Cosigning a loan creates a contractual obligation that survives the primary borrower’s death. When someone cosigns a loan, they agree to full repayment responsibility if the primary borrower cannot pay, and death qualifies as non-payment. The lender can demand full repayment from the cosigner immediately after death or continue collecting scheduled payments, depending on loan terms and state law. Cosigners remain liable for the entire outstanding balance regardless of whether they receive any inheritance from the deceased parent’s estate.

3.2 Joint Accounts and Shared Credit Cards

Joint account holders share equal legal responsibility for account balances and debts, which continues after one account holder dies. On joint credit cards, the surviving account holder remains liable for the full balance, including charges made by the deceased. This differs from being an authorized user, which does not create legal liability—authorized users can use the account but are not contractually obligated to repay debt. Joint bank accounts and jointly owned property may also be accessible to creditors seeking payment for debts incurred by the deceased account holder.

3.3 Inheriting a House With a Mortgage

When heirs inherit real property with an outstanding mortgage, the mortgage debt remains secured by the property regardless of ownership transfer. Heirs must decide whether to continue making mortgage payments and keep the property, sell the property to pay off the loan, or allow foreclosure if they cannot or will not maintain payments. Federal law through the Garn-St. Germain Act generally allows heirs to assume mortgages without triggering due-on-sale clauses, but the heir is not personally liable for mortgage debt unless they formally assume the loan or held joint ownership with the deceased.

3.4 Reverse Mortgages and Heir Obligations

A reverse mortgage becomes due when the borrower dies, requiring full repayment of the outstanding loan balance. Heirs who want to keep the property must repay the reverse mortgage balance or refinance into a traditional mortgage, typically within six months of the borrower’s death. If heirs choose not to keep the property, they can sell it to satisfy the debt, and if the sale proceeds exceed the loan balance, the excess goes to the estate. When the loan balance exceeds the property value, heirs can walk away without personal liability because reverse mortgages are non-recourse loans, meaning lenders can only collect from the property itself.

3.5 Filial Responsibility Laws (Medical and Long-Term Care Debt)

Filial responsibility laws exist in approximately 30 states and impose a legal duty on adult children to pay for indigent parents’ basic needs, including medical and long-term care expenses. These laws are rarely enforced, but certain states including Pennsylvania have allowed nursing homes and healthcare providers to sue adult children for unpaid bills when the parent’s estate cannot pay. Enforcement typically requires proof that the parent is indigent and cannot pay, and that the adult child has sufficient financial means. Most filial responsibility claims involve nursing home debt rather than other medical expenses, and many states have not actively enforced these statutes in decades.

3.6 When Voluntary Payments Create Legal Responsibility

Making voluntary payments on a deceased parent’s debt can create legal liability where none previously existed. When a family member pays part of a debt or agrees to a payment plan, some courts interpret this action as acknowledgment of personal responsibility for the debt. Additionally, verbal statements agreeing to pay debt or acknowledging it as personal responsibility can be used by creditors to establish liability. Heirs should avoid making any payments or agreements before consulting with an attorney, as these actions may waive legal protections against creditor claims.

4. How Different Types of Debt Are Treated After Death

Different debt categories are governed by distinct legal frameworks that determine how they are handled during estate settlement and whether heirs face any exposure.

4.1 Credit Card Debt (Unsecured Debt)

Credit card debt is unsecured debt, meaning it is not backed by collateral and represents a contractual obligation based only on the borrower’s promise to repay. When a credit card holder dies, the outstanding balance becomes a claim against the estate and is paid during probate if sufficient assets exist. If the estate is insolvent, credit card companies typically write off the remaining balance rather than pursue collection, as heirs are not responsible for unsecured debt unless they were joint account holders or cosigners. Authorized users on credit cards are not liable for balances because they did not sign the credit agreement.

4.2 Mortgage and Auto Loans (Secured Debt)

Secured debt is backed by collateral—real property for mortgages and vehicles for auto loans—which gives creditors the right to repossess or foreclose if payments stop. When the borrower dies, the lender’s security interest in the collateral continues, meaning the estate or heirs must continue payments to retain ownership or allow the lender to take the property. Heirs who inherit secured property can choose to assume payments, refinance the loan, sell the asset to pay off the debt, or surrender the property to the lender. Personal liability for deficiency balances—when the collateral value is less than the debt owed—depends on state law and whether the heir formally assumed the loan.

4.3 Medical Bills and Hospital Debt

Medical bills and hospital debt are generally unsecured claims against the estate that must be paid during probate before heirs receive assets. Healthcare providers can file claims with the estate, and these claims typically receive higher priority than credit card debt but lower priority than funeral expenses and estate administration costs. In states with filial responsibility laws, adult children may face potential liability for unpaid medical bills if the parent was indigent and the estate cannot pay, though enforcement remains uncommon. Additionally, Medicaid Estate Recovery Programs allow states to seek repayment from estates for long-term care costs paid by Medicaid during the deceased person’s lifetime.

4.4 Federal vs Private Student Loans

Federal student loans are discharged automatically upon the borrower’s death, meaning no further payments are required and the estate is not responsible for remaining balances. The loan servicer requires proof of death, typically a death certificate, to process the discharge. Private student loans, however, are treated as standard unsecured debt and become claims against the estate unless the lender offers death discharge as a policy benefit. Cosigners on private student loans remain fully liable for the outstanding balance after the primary borrower dies, as cosigning creates a binding contractual obligation that survives death.

4.5 Tax Debt and Government Claims

Tax debt owed to the Internal Revenue Service or state tax agencies receives priority status during probate, typically ahead of most other creditor claims. The executor must file final income tax returns for the deceased and pay any taxes owed from estate assets before distributing property to heirs. Estate tax obligations, when applicable, must also be settled from estate funds. Government claims for unpaid taxes can survive beyond probate if the estate is insolvent, and in some cases, tax liens can attach to property transferred to heirs, though personal liability for the deceased’s tax debt does not generally transfer unless specific circumstances like joint filing or fraudulent transfers exist.

5. What to Do If Creditors Contact You After Your Parent Dies

When creditors contact surviving family members after a parent’s death, understanding legal rights and proper response procedures protects against harassment and unintended liability.

5.1 What Debt Collectors Can Legally Ask You

Debt collectors can contact family members to locate the executor or personal representative of the estate and to obtain contact information for that person. They may ask about the existence of an estate, whether probate has been opened, and who is handling estate administration. However, collectors cannot discuss the specific debt details with anyone other than the executor, the deceased’s spouse, or the deceased’s attorney. Collectors who contact family members for information must not imply that relatives are responsible for the debt or request payment from anyone other than the estate’s legal representative.

5.2 What You Should NEVER Say or Agree To

Family members should never verbally acknowledge personal responsibility for a deceased parent’s debt or agree to make payments, as these statements can create legal liability. Saying “I’ll take care of this” or “I’ll pay what I can” may be interpreted as acceptance of debt responsibility. Similarly, making even small partial payments can constitute acknowledgment of the debt as a personal obligation. When creditors contact family members, the safest response is to refer them to the executor or estate attorney without discussing the debt itself, payment ability, or any willingness to help settle the obligation.

5.3 How to Request Proof or Validation of Debt

Under the Fair Debt Collection Practices Act, family members who are contacted about a deceased person’s debt have the right to request debt validation. A debt validation request requires the collector to provide written proof that the debt exists, the amount owed, and the original creditor’s identity. The request should be made in writing within 30 days of the first contact, and collectors must stop collection activity until they provide the requested documentation. This process helps identify illegitimate claims, time-barred debts beyond the statute of limitations, and debts that have already been paid or discharged.

5.4 When to Refer Creditors to the Estate Executor

All creditor communications regarding the deceased person’s debts should be directed to the estate’s executor or personal representative, who has the legal authority to review claims and authorize payments from estate assets. Family members who are not serving as executor should provide only the executor’s contact information and decline to discuss financial details or estate assets. If no executor has been appointed or probate has not yet opened, family members can inform creditors of this status without providing additional information about assets or potential inheritance. The executor bears the legal responsibility for reviewing creditor claims, verifying their validity, and determining payment priority according to state law.

5.5 How Consumer Protection Laws Apply to Surviving Family Members

The Fair Debt Collection Practices Act prohibits debt collectors from using deceptive, abusive, or harassing tactics when contacting anyone about a debt, including family members of deceased debtors. Collectors cannot falsely imply that family members are legally obligated to pay a deceased person’s debt, cannot contact family members repeatedly or at unreasonable hours, and cannot threaten legal action they do not intend to take or cannot legally pursue. Family members who experience FDCPA violations can file complaints with the Consumer Financial Protection Bureau and may have grounds to sue the debt collector for damages. State consumer protection laws often provide additional protections beyond federal requirements.

6. How to Avoid Being Stuck With Your Parents’ Debt (Prevention & Planning)

Proactive financial planning and understanding of estate mechanics help families avoid unintended debt liability and protect inherited assets from creditor claims.

6.1 Why Estate Planning Reduces Debt Risk

Proper estate planning reduces debt risk for heirs by clarifying asset ownership, establishing clear creditor claim procedures, and maximizing assets that pass outside probate. When parents create comprehensive estate plans including wills, trusts, and beneficiary designations, the estate settlement process tends to proceed more smoothly with less confusion about creditor rights. Estate planning also allows parents to purchase life insurance or establish funds specifically designated to pay final debts, which protects assets intended for heirs from creditor depletion during probate.

6.2 Beneficiary Designations vs Probate Assets

Assets with beneficiary designations—including life insurance policies, retirement accounts, and payable-on-death bank accounts—transfer directly to named beneficiaries and bypass probate entirely. Because these assets do not enter the estate, they generally are not available to creditors seeking payment for the deceased’s debts. This protection makes beneficiary-designated assets a valuable estate planning tool for ensuring specific assets reach intended heirs regardless of estate debts. However, in some states, creditors may challenge beneficiary transfers if the estate is insolvent and the deceased transferred assets to beneficiaries specifically to avoid creditor claims.

6.3 Risks of Adding Parents to Your Bank Accounts

Adding a parent as a joint owner on bank accounts creates shared ownership, which can expose the account holder’s funds to the parent’s creditors both during life and after death. Joint ownership differs from power of attorney designation—joint owners have equal legal claim to funds, while power of attorney merely grants authority to manage another person’s accounts without creating ownership rights. When a joint owner dies, creditors may claim that the deceased owned a portion of the account and attempt to collect from those funds. To avoid this risk, adult children should use power of attorney or payable-on-death designations rather than joint ownership when helping parents manage finances.

6.4 When Refusing an Inheritance Makes Sense

Heirs can disclaim or refuse an inheritance through a legal process that treats them as if they predeceased the decedent, causing assets to pass to the next beneficiary in line. Disclaimer of inheritance may make sense when accepting the inheritance would expose the heir to debt liability, tax consequences, or means-tested benefit eligibility issues. Disclaimers must be executed properly through written legal documents filed within a specific timeframe, typically nine months from death for federal tax purposes. Once assets are disclaimed, the heir has no control over who receives them, as distribution follows the will or state intestacy laws rather than the disclaiming heir’s preferences.

6.5 When to Talk to an Estate Attorney or Financial Advisor

Consulting an estate attorney becomes necessary when the deceased’s estate includes significant debt, when creditors make aggressive collection attempts against family members, or when questions arise about personal liability for specific debts. Attorneys who specialize in estate administration and probate law can clarify state-specific creditor claim procedures, determine whether filial responsibility laws apply, and protect heirs from improper collection tactics. Financial advisors can help heirs evaluate decisions about inheriting property with secured debt, understand tax implications of estate assets, and coordinate estate settlement with the heir’s broader financial planning goals.

Final Note: While children generally are not responsible for their parents’ debt after death, specific situations including cosigning, joint accounts, and state filial responsibility laws create exceptions. Understanding the estate settlement process, recognizing when personal liability exists, and knowing how to respond to creditor contact helps protect personal finances during an already difficult time. When uncertainty exists about debt responsibility or creditor claims, consulting qualified legal and financial professionals provides clarity and protection against unintended financial obligations.