Table of Contents

Contents are generated from article headings.

An irregular-income budget is a financial plan designed for income that varies in amount and timing — common among freelancers, commission-based workers, gig economy participants, seasonal employees, and small business owners. Irregular-income budgets replace fixed monthly allocations with priority-based allocation systems that fund categories in sequence based on importance, adapting automatically to whatever income actually arrives.

Standard budgeting advice assumes predictable paychecks arriving on predictable dates. For irregular earners, this assumption breaks immediately: March income might be $5,200 while April drops to $2,800 and May rebounds to $6,100. A budget designed for $4,000/month fails in two of those three months — underfunding savings in April and leaving surplus unallocated in May.

This content discusses irregular-income budgeting using financial planning principles and self-employment finance data. Tax obligations, benefits access, and income patterns vary by jurisdiction and employment type. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Why Standard Budgets Fail on Irregular Income

The Fixed-Allocation Problem

A standard budget allocates $1,400 to housing, $400 to food, $300 to transportation — totals that assume the same income arrives monthly. When March income is $5,200 and April income is $2,800, the $4,500 in fixed allocations that worked in March cannot be funded in April. The budget did not fail — it was structurally incompatible with the income pattern.

The Timing Uncertainty

Irregular income arrives on irregular schedules. A freelancer invoicing a client on March 15 may receive payment April 3, April 20, or May 1. Bills due April 1 cannot wait for payment timing. This timing uncertainty requires a buffer account — a cash reserve that pays current-month bills while income for next month accumulates.

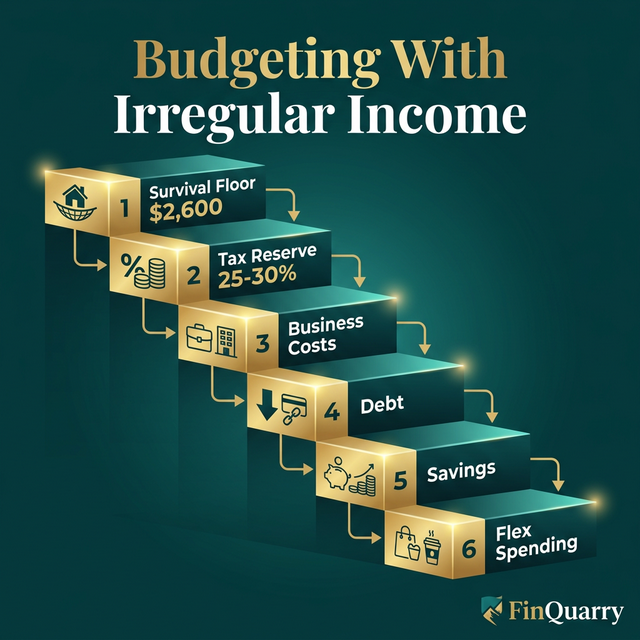

The Priority Waterfall System

The priority waterfall replaces fixed monthly allocations with a ranked sequence. As income arrives, it flows through the priority stack in order:

Priority 1: Survival Floor ($X)

Housing, utilities, minimum debt payments, basic food, insurance, essential transportation. This number is calculated precisely — not estimated — from actual costs. A freelancer with a $2,600 survival floor knows that any month with income below $2,600 requires emergency action.

Priority 2: Tax Reserve (25–35% of gross)

Self-employed earners owe estimated quarterly taxes. Every dollar earned should route 25–35% (depending on tax bracket and jurisdiction) to a dedicated tax account. A freelancer earning $5,200 in March should transfer $1,300–1,820 to the tax reserve account immediately — before any other allocation.

The IRS requires quarterly estimated payments. Failing to set aside tax reserves is the most common irregular-income budgeting failure.

Priority 3: Emergency Buffer Replenishment

If the emergency fund is below target (3–6 months of survival floor expenses), direct surplus here. A freelancer with a $2,600 survival floor needs $7,800–15,600 in emergency reserves — higher than W-2 employees because income disruption can last months, not weeks.

Priority 4: Debt Acceleration

After survival, taxes, and emergency buffer, surplus funds go to debt acceleration beyond minimum payments.

Priority 5: Discretionary and Goals

Only after priorities 1–4 are funded does money flow to discretionary spending, short-term goals, and quality-of-life spending.

The Income Smoothing Strategy

The Buffer Month Method

Build one month of living expenses ($3,500–5,000 depending on costs) in a dedicated checking account. Live on last month’s income while this month’s income accumulates. This converts irregular income into functionally regular income by introducing a one-month delay.

A freelancer earning $2,800 in April and $6,100 in May: April’s expenses are funded by March’s $5,200 income (already in the buffer), while April’s $2,800 and May’s $6,100 fund future months. The month-to-month income variation becomes invisible to daily spending.

The Baseline Budget

Calculate the average of the lowest 3 income months over the past year. This is the baseline — the amount the budget is designed to function on. Any income above baseline is surplus allocated through the priority waterfall.

A freelancer whose lowest 3 months were $2,800, $3,100, and $3,400 has a baseline of $3,100. The monthly budget is designed for $3,100. Months producing $5,000+ create surplus that funds higher priorities.

Managing High-Income Months

The temptation during high-income months is to increase spending proportionally — $6,100 income month feels like permission for $6,100 worth of spending. This behavior produces the feast-famine cycle that makes irregular income feel permanently unstable.

High-income months should fund: tax reserves, emergency buffer replenishment, sinking funds for annual expenses, and financial goal acceleration. Discretionary spending stays at the baseline level regardless of income fluctuation.

Quarterly Tax Management

Self-employed earners pay estimated taxes quarterly (April 15, June 15, September 15, January 15). The tax reserve account should accumulate 25–35% of all gross income and disburse quarterly.

A freelancer earning $48,000 annually owes approximately $12,000–16,800 in combined federal and state income tax plus self-employment tax. Quarterly payments of $3,000–4,200. Without the tax reserve, these quarterly obligations arrive as “surprises” that devastate the operating budget.

Is Irregular Income Budgeting Harder Than Regular?

Yes — irregular income budgeting is structurally more demanding because it requires both priority-based allocation (which standard budgets do not) and income smoothing (which standard budgets do not need). The additional complexity is compensated by the buffer month system, which — once established — makes day-to-day money management feel nearly identical to salaried budgeting.

Written by Marcus Tremblay, Senior Financial Analyst | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry