Table of Contents

Contents are generated from article headings.

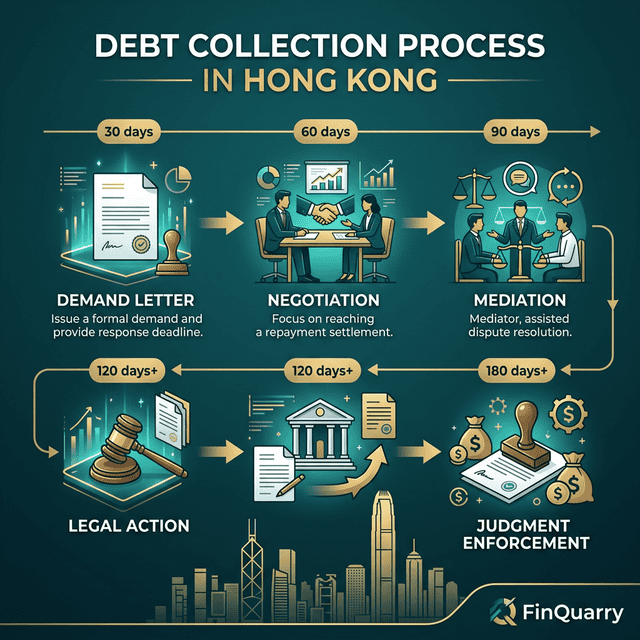

The debt collection process in Hong Kong progresses through sequential stages escalating from informal communication to formal legal proceedings and compulsory enforcement, with each stage involving specific activities, timeframes, and cost implications. Understanding this progression helps creditors set realistic expectations, allocate resources appropriately, and make informed decisions about collection strategy escalation.

Step 1 – Pre-Collection Contact

Pre-collection contact involves informal communication with debtors before formal collection activities commence, confirming debt validity, updating contact information, and exploring voluntary payment without agency involvement. This stage typically occurs internally before engaging external collection agencies, though some creditors bypass internal efforts and immediately outsource to professionals.

Activities include reviewing account records to verify debt amounts, contract terms, and payment histories, confirming debtor contact information remains current and accurate, sending informal payment reminder notices or account statements, and offering payment flexibility such as deadline extensions or installment arrangements. Pre-collection contact succeeds when debtors simply overlooked payment due to administrative errors, dispute amounts or terms requiring clarification before payment, or request accommodation addressing temporary cash flow constraints.

This stage generally spans 7-30 days before formal collection referral, allowing creditors to resolve simple oversights, identify disputed claims requiring investigation, and preserve positive customer relationships when payment occurs voluntarily. Costs remain minimal, limited to internal staff time and communication expenses.

Step 2 – Formal Demand Letters

Formal demand letters constitute the initial professional collection communication, sent by collection agencies or attorneys to notify debtors of outstanding obligations, payment expectations, and consequences of non-payment. Well-crafted demand letters balance firmness with professionalism, clearly stating facts while avoiding inflammatory language or prohibited harassment.

Effective demand letters include complete debt details specifying original creditor, debt amount, invoice or contract reference numbers, and transaction dates, breakdown of principal amounts, interest charges, and collection fees if applicable, payment deadline typically 7-14 days from letter date, payment instructions specifying acceptable methods and remittance addresses, and consequences of non-payment such as legal action, credit reporting, or additional fees. Letters should be delivered via methods providing proof of receipt such as registered mail or courier services with delivery confirmation.

Demand letters elicit debtor responses including immediate payment arrangements, disputes challenging debt validity or amounts, requests for documentation supporting claims, or complete non-response. Collection agencies assess responses to determine appropriate next steps: accepting partial payments and negotiating installment plans, providing requested documentation to resolve disputes, or escalating to direct debtor contact when letters generate no response.

This stage typically spans 14-30 days allowing reasonable time for debtor receipt, internal processing, and response. Costs include letter preparation, postage or courier fees, and administrative time documenting communications. Success rates vary from 10-30% of debts depending on debt age, debtor circumstances, and prior relationship quality.

Step 3 – Negotiation & Settlement Options

Negotiation involves direct communication between collection agencies and debtors to explore payment arrangements, settlement terms, or dispute resolution acceptable to both parties. Skilled negotiators balance firmness about payment obligations with flexibility accommodating genuine debtor constraints, seeking mutually acceptable outcomes avoiding costly legal proceedings.

Negotiation tactics include payment plans dividing total debt into affordable installments over defined periods, lump-sum settlements accepting reduced payments immediately rather than pursuing full amounts through prolonged legal action, secured payment arrangements obtaining collateral or guarantors reducing default risk on installment agreements, and dispute mediation addressing contested amounts through evidence review and compromise. Successful negotiations result in written settlement agreements documenting terms, payment schedules, consequences of default, and mutual releases of claims upon full performance.

Agencies assess debtor credibility through information verification, financial disclosure requests, and payment performance monitoring. Red flags indicating negotiation futility include repeated broken payment promises without valid explanations, refusal to provide basic financial information supporting claimed inability to pay, disappearance or evasion after agreement negotiation, or evidence of asset dissipation suggesting fraudulent debtor conduct.

Negotiation stages typically span 30-90 days depending on debtor responsiveness, settlement complexity, and payment plan duration. Costs include staff time for calls and meetings, documentation preparation for agreements, and monitoring resources tracking payment compliance. This stage resolves 30-50% of debts that survive initial demand letters, achieving recoveries averaging 60-80% of debt face value through discounted settlements.

Step 4 – Legal Action & Court Enforcement

Legal action commences when amicable collection fails, debtors refuse to engage meaningfully, or circumstances indicate only legal compulsion will secure payment. The process varies by claim amount, legal complexity, and chosen court jurisdiction, with procedures ranging from simplified Small Claims Tribunal hearings to formal High Court litigation.

Small Claims Tribunal handles debts up to HK$75,000 through streamlined procedures designed for self-represented parties, with filing fees of HK$95-HK$445 based on claim value. Procedures include filing claim forms with supporting documents, tribunal-scheduled hearings typically within 3-6 months, informal hearings where adjudicators review evidence and hear parties, and judgments issued promptly after hearings. Legal representation is prohibited except for corporate claimants or with tribunal permission in complex cases, reducing litigation costs.

District Court jurisdiction covers claims from HK$75,001 to HK$3,000,000, employing formal civil procedures with legal representation typically required for effective navigation. Timelines extend 6-12 months from filing to judgment, with costs including court fees proportional to claim amounts, legal representation fees if attorneys are retained, and enforcement costs for post-judgment collection. High Court handles claims exceeding HK$3,000,000 or involving complex legal issues, with procedures and costs similar to District Court but higher complexity and professional representation requirements.

Post-judgment enforcement mechanisms compel payment through asset seizure or income interception when debtors fail to satisfy judgments voluntarily. Options include garnishee orders freezing debtor bank accounts or intercepting salaries payable by third parties, charging orders securing judgment debts against real property preventing sale or refinancing without payment, bailiff warrants authorizing seizure and public auction of movable property, bankruptcy petitions forcing individual debtor insolvency and asset distribution to creditors, and winding-up petitions liquidating corporate debtors and distributing proceeds to creditors.

Step 5 – Post-Collection Reporting & Monitoring

Post-collection activities involve documenting collection outcomes, monitoring ongoing payment arrangements, and analyzing performance metrics informing future collection strategy. Systematic reporting provides creditors visibility into portfolio health, agency effectiveness, and opportunities for process improvement.

Reporting elements include recovery rates showing percentages of attempted debts successfully collected, aging analysis tracking how debt age affects recovery likelihood, cost efficiency metrics calculating net recoveries after agency fees and expenses, and disposition categorization classifying debts as paid, settled, in litigation, uncollectible, or disputed. Regular reporting enables creditors to identify underperforming agencies, assess whether internal credit policies require adjustment to reduce bad debt exposure, and allocate resources toward highest-value collection opportunities.

Monitoring active payment plans ensures debtor compliance with installment agreements, triggering enforcement escalation when defaults occur. Activities include payment receipt verification, default notification to debtors breaching agreements, and legal action resumption exercising contractual rights to accelerate remaining balances upon default. Effective monitoring maximizes plan completion rates while limiting time between defaults and enforcement responses.