Table of Contents

Contents are generated from article headings.

A financial setback budget is a temporary recovery-phase financial plan designed for the period between a major financial disruption — job loss, medical emergency, divorce, business failure, or economic downturn — and the return to financial stability. Setback budgeting operates on fundamentally different principles than normal budgeting: it prioritizes stabilization over optimization, survival over growth, and psychological recovery alongside financial recovery.

Financial setback recovery differs from starting from scratch. Starting fresh carries no emotional weight — no loss narrative, no fear of repeated collapse. Rebuilding after setback requires engaging with money after money was the source of crisis. It requires building a new plan while processing the loss of the old one.

This content discusses financial recovery budgeting using financial planning principles, behavioral economics, and consumer research on financial resilience. Recovery timelines, available resources, and financial products vary by jurisdiction and individual circumstances. FinQuarry provides informational content only — this does not constitute personalized financial advice.

The Emotional Architecture of Financial Recovery

The Financial Grief Cycle

Financial setback triggers a grief process: denial (“this cannot be happening”), anger (“why me?”), bargaining (“if I work 80 hours I can fix this immediately”), depression (“I will never recover”), and acceptance (“this is my current reality and I need to build from here”).

The budget cannot be meaningfully rebuilt during denial, anger, or bargaining because these states produce unrealistic plans. Acceptance — realistic acknowledgment of the current financial position — is the emotional prerequisite for an effective recovery budget.

The Shame Spiral

Financial setback produces shame that is practically destructive, not just emotionally painful. The spiral — “I should have saved more, planned better” — redirects cognitive energy from problem-solving (“what is my reality now?”) to self-blame (“what is wrong with me?”). The budget does not care about blame. It cares about current numbers. Separating the setback from personal identity is financial planning advice, not therapy advice.

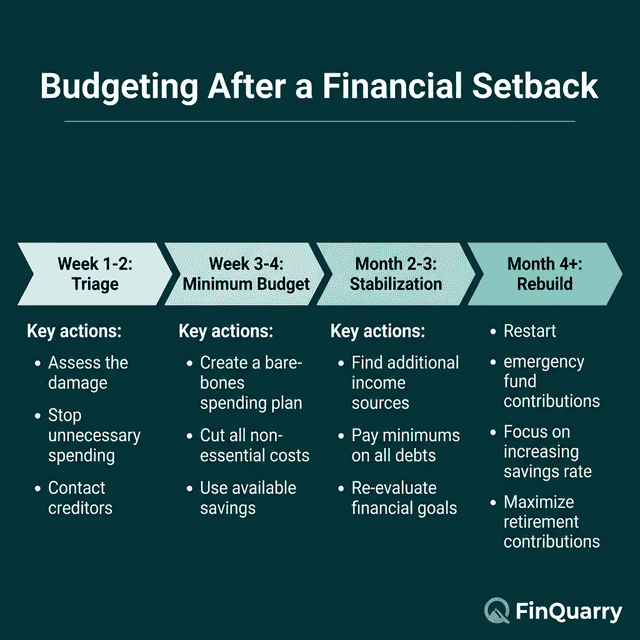

The 90-Day Stabilization Budget

Phase 1: Financial Triage (Days 1–14)

Before budgeting begins, assess damage:

- Current income (reduced, eliminated, or unchanged)

- Essential obligations (list every mandatory payment)

- Remaining savings

- New debts created by the setback

- Available assistance (unemployment benefits, insurance claims, hardship programs)

A person who lost a $4,500/month job now receiving $2,200/month in unemployment benefits has experienced a 51% income reduction. The budget must be rebuilt for $2,200, not managed as a temporary inconvenience within the $4,500 framework.

Phase 2: Survival Budget (Days 15–90)

The 90-day survival budget funds four categories only: housing, food, essential utilities, and medical needs. Other expenditures are suspended — not permanently, but for stabilization.

Contact creditors immediately to request hardship accommodation. Most offer payment deferrals, interest rate reductions, or temporary payment plan restructuring. This single action can reduce monthly obligations by $100–400 during recovery. Creditors generally offer better terms to borrowers who communicate early.

Phase 3: Recovery Budget (Day 91+)

Once income stabilizes (new employment, insurance settlement, benefits), transition to recovery budgeting. Reintroduce categories gradually: debt minimum payments first, then micro-savings ($25–50/month), then modest discretionary spending, then goal-directed saving.

Recovery budgets accept that financial life will not return to pre-setback levels immediately. Gradual, sustainable recovery produces better long-term outcomes than aggressive attempts that burn out and collapse.

Rebuilding Savings After Depletion

The $500 First Target (Again)

If savings were depleted, start with the same target recommended for people with no savings: $500. Achievable in 3–6 months of micro-contributions, this target provides immediate protective value and the first psychological win of recovery.

Overcoming the Cynicism Barrier

Rebuilding savings after watching savings disappear is emotionally harder than building for the first time. The person knows — from experience — that savings can be wiped out. This creates cynicism: “Why save if it’s going to disappear?”

The structural answer: the savings disappeared because an emergency consumed them — which is exactly what savings are designed to do. The emergency fund worked. It absorbed shock that would otherwise have produced lasting debt. Rebuilding is restocking the financial fire extinguisher after a fire — not futile repetition.

Managing New Setback Debt

Stabilize Before Accelerating

New debt created by a setback — medical bills, credit card charges for essentials, personal loans — should not be aggressively attacked during stabilization. Minimum payments maintain accounts in good standing. Aggressive repayment during unstable income risks depleting resources needed for daily survival.

A person with $6,500 in new setback debt on a $2,200/month recovery income should maintain minimums ($150/month across accounts) rather than directing $600 to debt and leaving insufficient funds for food and utilities.

Contact Creditors Early

Hardship programs exist at most major creditors but are rarely offered proactively. Contact every creditor within 30 days:

- Credit card companies offer temporary APR reduction (often to 0–6% for 6–12 months)

- Medical providers offer interest-free payment plans ($50–100/month)

- Mortgage servicers offer forbearance programs

- Auto lenders may defer 1–3 payments

How Long Does Recovery Take?

Recovery timelines for significant financial setbacks:

Minor setback ($2,000–5,000 unexpected expense): 6–12 months to return to pre-setback financial position.

Major setback (job loss, medical crisis): 18–36 months for full recovery (pre-setback savings, debt levels, spending stability).

Severe setback (divorce, business failure, extended unemployment): 24–48 months.

These timelines are not failures — they reflect the mathematical reality of rebuilding on finite income. The Consumer Financial Protection Bureau provides resources for financial recovery planning.

Should I Change Budgeting Methods Post-Setback?

If the pre-setback method was working, it will likely work again during recovery — with adjustments for the new reality. If the setback exposed structural weaknesses (no emergency fund, no irregular expense planning), the recovery is an opportunity to rebuild with those gaps addressed. The setback provides data about what the budget needs to withstand.

Is It Normal to Feel Like Recovery Is Impossible?

Yes. The feeling of permanent damage is one of the most common emotional responses to financial setback — and it is almost always temporary. The feeling reflects emotional impact, not mathematical trajectory. Recovery follows a predictable arc: despair → stabilization → gradual improvement → stability. The person in the despair phase cannot see the stability phase — but it exists on the same timeline.

Written by Marcus Tremblay, Senior Financial Analyst | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry