Table of Contents

Contents are generated from article headings.

Financial anxiety is a persistent emotional response where engaging with personal finances — checking account balances, opening bills, making spending decisions, or building a budget — triggers anxiety symptoms including avoidance, dread, racing thoughts, or physical tension. Financial anxiety operates independently of actual financial health: a person with adequate income and manageable debt can experience severe financial anxiety, while a person in genuine financial difficulty may not.

Financial anxiety and budgeting exist in a paradox: the tool designed to reduce financial uncertainty (the budget) requires engaging with the exact stimulus (money awareness) that triggers the anxiety response. Resolution requires adapting the budgeting process to work within anxiety’s constraints rather than demanding that anxiety disappear before budgeting begins.

This content discusses financial anxiety and adapted budgeting approaches using behavioral economics, financial psychology research, and financial planning principles. Individual anxiety responses vary based on personal history, mental health, and economic circumstances. This is informational content, not clinical advice. FinQuarry does not provide mental health diagnosis or treatment.

How Financial Anxiety Disrupts Budgeting

The Avoidance Loop

Financial anxiety produces avoidance — not checking balances, not opening statements, not engaging with the budget. Avoidance temporarily reduces anxiety but allows financial problems to compound undetected. When the person finally engages (often forced by a crisis), the situation is worse than it would have been with earlier attention — which reinforces the belief that engaging with money produces bad outcomes, deepening the avoidance loop.

A person who avoids checking a credit card balance for three months may discover $800 in interest charges that could have been prevented with a payment adjustment made in month one. The avoidance did not prevent damage — it prevented awareness of damage that was accumulating regardless.

The Catastrophizing Cycle

Financial anxiety amplifies negative possibilities. A $50 budget overage in groceries becomes “I’m terrible with money.” A $400 unexpected car repair becomes “I’ll never be financially stable.” These cognitive distortions convert manageable financial events into identity-level crises, making each interaction with the budget emotionally threatening.

The Perfectionism Trap

Some anxiety-driven budgeters become hyper-vigilant — tracking every cent, obsessing over small variances, checking accounts multiple times daily. This over-engagement is not healthy budgeting. It is anxiety wearing a budget’s operating system. The budget becomes a control mechanism fed by anxiety rather than a planning tool serving financial goals.

The Anxiety-Adapted Budgeting Framework

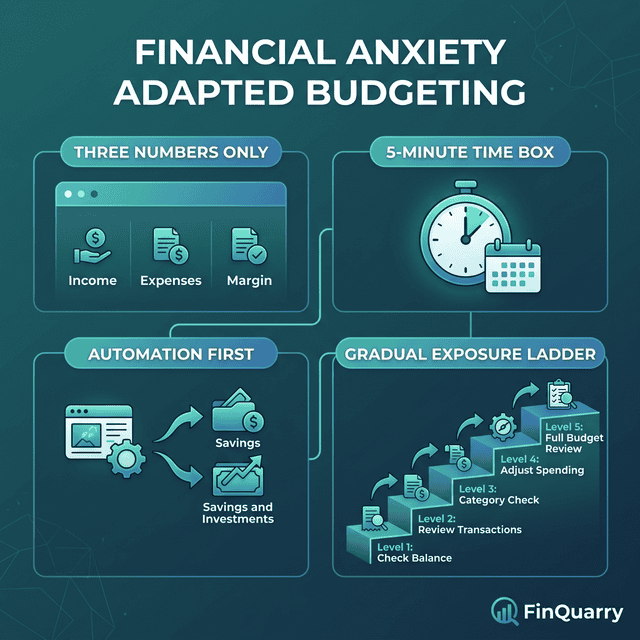

Principle 1: Three Numbers Only

Reduce the entire budget to three numbers: total monthly income, total essential costs, and what is left. No 15-category spreadsheet. No transaction tracking. Three numbers.

A person earning $3,600/month with $2,800 in essential costs has $800 remaining. That $800 covers variable spending and savings. For an anxiety-adapted budget, this level of information is sufficient — it answers the only question that matters: “Am I okay?”

Principle 2: Time-Box Financial Engagement

Rather than open-ended financial review (which anxiety will extend indefinitely), set a specific time limit: 10 minutes, once per week. Open the bank app, note the checking account balance, assess whether it is consistent with expectations, and close the app. Ten minutes. Not more.

Anxiety-adapted budgeting follows the exposure therapy principle: short, controlled interactions build tolerance. Weekly 10-minute check-ins produce adequate financial awareness without the extended engagement that triggers anxiety escalation.

Principle 3: Automate Everything Possible

Every financial decision automated is a financial decision removed from the anxiety trigger cycle. Auto-pay all fixed bills. Auto-transfer savings on payday. Auto-pay minimum debt payments.

The goal: a financial system that functions correctly even during weeks when the person cannot emotionally engage with money at all. Automation is not avoidance — it is structural protection that ensures financial obligations are met regardless of emotional state.

Principle 4: Gradual Engagement Expansion

Start with the three-number budget and weekly check-ins. After one month, add one additional data point (savings balance). After two months, add another (debt balance). Gradual engagement expansion builds financial confidence without overwhelming the anxiety response.

When Financial Anxiety Is Not “Just” Anxiety

Rational Financial Anxiety

Some financial anxiety is proportionate to the situation. A person with $0 savings, $8,000 in debt, and $200/month between income and essential expenses has genuine financial vulnerability. The anxiety is rational — it accurately reflects the risk. For this person, anxiety reduction comes from structural financial improvement, not cognitive reframing.

The budget’s job here is building the first $500 buffer — concrete progress that provides both financial protection and anxiety reduction through evidence that the situation is improving.

Clinical Financial Anxiety

When anxiety prevents any financial engagement — cannot open bank apps, cannot discuss money, loses sleep over financial thoughts, experiences panic when bills arrive — the condition has moved beyond budgeting-addressable anxiety into clinical territory. Financial therapists (certified professionals specializing in money-related emotional issues) provide treatment that targets the anxiety itself rather than the financial behaviors it disrupts.

The Financial Therapy Association maintains a directory of certified financial therapists.

Practical Anxiety-Reduction Tactics

The Balance Exposure Ladder

Build tolerance by structured exposure: check the checking account balance (week 1), then check savings (week 2), then review one credit card statement (week 3), then review the monthly budget summary (week 4). Each step increases financial awareness within a controlled, sequential process.

The “Good Enough” Standard

Replace budget perfectionism with the “good enough” standard: if the checking account is positive, bills are paid, and savings received its transfer, the budget is performing. Variances under 10% per category are normal operational fluctuation. The budget producing guilt over a $12 grocery overage is not helpful — it is anxiety amplifying insignificant data into disproportionate emotional weight.

The Accountability Partner

For people whose anxiety isolates them from financial engagement, a trusted accountability partner — spouse, friend, sibling, financial counselor — provides a supportive structure for review. The partner’s role is presence and support, not criticism.

Is Financial Anxiety Permanent?

Financial anxiety is not fixed. Research on anxiety treatment and financial behavior indicates that gradual exposure, structural automation, and progressive engagement reduce anxiety intensity over time. The person who currently cannot open a bank statement may, through structured practice, become comfortable with monthly budget reviews within 6–12 months. Progress is measured not by the absence of anxiety but by the ability to function financially despite it.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry