Table of Contents

Contents are generated from article headings.

A household budget is a multi-person financial plan that allocates shared income across fixed obligations, variable expenses, savings goals, and individual spending autonomy — accounting for multiple people’s needs, competing priorities, and the emotional complexity of financial decisions that affect more than one person. Household budgets differ structurally from individual budgets because they must manage interpersonal financial dynamics alongside the numbers.

Household budgets fail most often not from mathematical error but from unaddressed human dynamics. A budget that balances on paper while household members disagree about spending priorities produces conflict that leads to covert spending, budget sabotage, and eventual abandonment.

This content discusses household budget planning using financial planning principles and family finance research. Household compositions, tax situations, and costs vary by jurisdiction. FinQuarry provides informational content only — this does not constitute personalized financial advice.

What Makes Household Budgets Different

The Competing Priorities Problem

In a two-adult household, one person may prioritize debt repayment while the other prioritizes quality-of-life spending. Both positions are financially legitimate.

For example, a couple earning $7,200/month combined with $2,800 in fixed costs and $15,000 in credit card debt faces a concrete allocation decision. Directing $800/month extra toward debt eliminates it in 19 months but leaves $400/month less for family activities. Directing $400/month to debt extends payoff to 38 months but preserves lifestyle. The budget must make this trade-off explicit — because implicit trade-offs generate resentment that undermines the budget from inside.

The Visibility Gap

Household members often have incomplete visibility into total finances. One person handles bills. One manages savings. Neither has the complete picture. A functioning household budget makes full finances visible to all contributing adults — reducing anxiety for the uninformed party and burden for the party carrying financial stress alone.

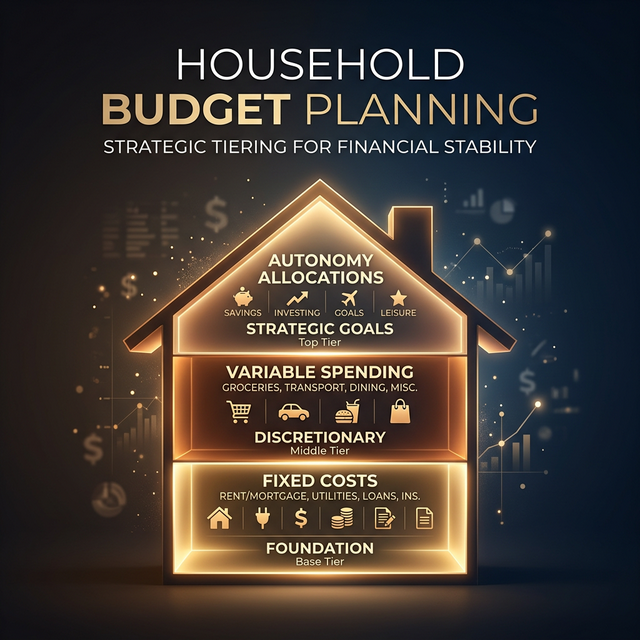

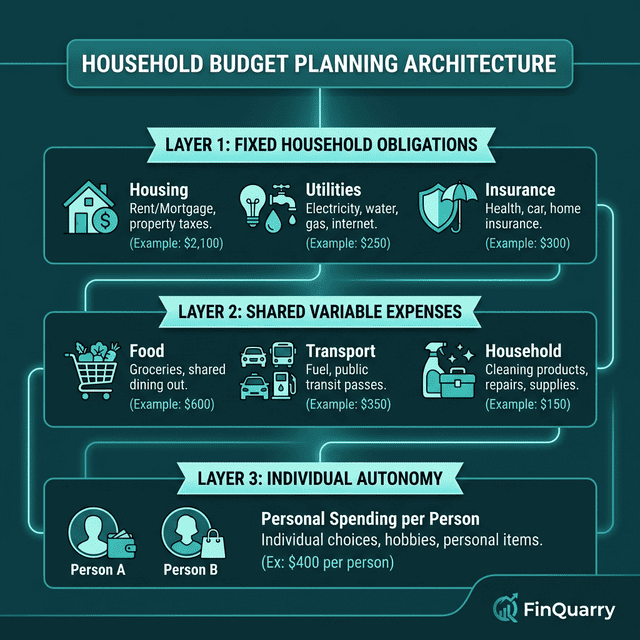

The Three-Layer Budget Architecture

Layer 1: Fixed Household Obligations

The foundation contains every non-negotiable cost: mortgage/rent, utilities, insurance (home, health, auto), minimum debt payments, property taxes, internet, phone, childcare, and transportation. These should auto-pay where possible.

A household with $7,200/month combined income might have $3,400 in fixed obligations: rent ($1,650), utilities ($220), car payments ($480), insurance ($350), minimum debt ($250), phone/internet ($150), childcare ($300). This consumes 47% of income — within a manageable range for the 50/30/20 framework.

Layer 2: Variable Household Spending

Shared spending that fluctuates: groceries ($600–800), household supplies ($80–120), maintenance ($50–200), fuel ($200–280), medical co-pays ($0–150), family dining ($100–200). This layer requires the most active management and is where household members most commonly disagree about what qualifies as necessary.

Use the three-month average for each variable category and add a 10% buffer. If grocery history shows $620, $680, and $740, the average is $680 and the budgeted amount is $748.

Layer 3: Individual Autonomy Allocations

Each adult receives a defined personal spending amount — controlled without justification or oversight. This layer is not optional luxury. It is structural protection.

A household allocating $200/person/month for autonomy spending ($400 total) prevents the resentment cascade that builds when every purchase requires shared approval. Adults without financial autonomy in a shared budget tend to develop hidden spending patterns that damage the budget more than funded, visible discretionary spending.

Building the Household Budget

Step 1: Full Financial Transparency

Before entering numbers, every contributing adult needs full visibility: all income sources, all debt balances, all savings accounts, all recurring obligations. This session is often uncomfortable but essential.

Step 2: Aggregate All Income

Total every source: salaries, secondary employment, side income, benefits, child support. Use after-tax, after-deduction amounts. If one income is variable, budget from the lowest recent month.

Step 3: Build by Layer

Fixed obligations first. Variable household spending second (using 3-month averages). Individual autonomy allocations third. Savings and debt acceleration from the remainder.

Step 4: Agree on Savings and Debt Strategy

This step is a conversation. The household must agree on emergency fund targets, debt priority, and savings goals. Disagreement on financial priorities is normal — the budget makes compromises explicit rather than implicit.

Step 5: Schedule Monthly Budget Meetings

A 30-minute monthly review where both adults compare actual spending to plan, discuss upcoming expenses, and make adjustments. The meeting should use data, not memory, and focus on information, not blame.

Managing Children’s Expenses

The Volatility Challenge

Children’s expenses are the most unpredictable household budget category. School fees, extracurriculars, sports equipment, birthday parties, field trips, growth-driven clothing replacement — these costs arrive irregularly and are emotionally difficult to deny.

A family spending $300–500/month on children’s expenses needs a dedicated budget line at the 3-month average ($400 if recent months were $350, $420, and $430). This absorbs volatility without disrupting other categories.

Financial Education Through Budget Participation

A teenager involved in choosing between a $2,500 family vacation hotel and a $1,800 option learns trade-offs, decision-making, and financial awareness through lived experience — more effective than abstract instruction. This is applied financial literacy.

One Income vs. Two: Different Structures

Single-Income Households

A single-income household carries zero income redundancy. Budget architecture must prioritize financial safety — 6–9 month emergency fund targets, conservative spending allocations, and a clearly defined survival floor.

Dual-Income Households

Two incomes create coordination complexity and an surplus illusion. A couple earning $8,000 combined may feel comfortable spending $200 on dining — but after $5,800 in obligations and $600 in savings, the actual discretionary pool is $1,600, making that $200 represent 12.5% of available money, not the 2.5% the gross number suggests.

Income Disparity Between Partners

Income disparity creates a fairness question with no universal answer. Equal contribution (50/50) strains the lower earner. Proportional contribution (each pays their income share percentage) creates fairness but concentrates financial burden on the higher earner.

The budget’s function is making the chosen model transparent and consistent — so the arrangement is a conscious agreement rather than an unspoken resentment source.

The Simplest Household Budget That Works

Three accounts: one joint account for all shared fixed and variable expenses (funded proportionally), and one individual account per adult for autonomy spending. On payday, each person transfers their contribution to joint. Fixed bills auto-pay from joint. Variable spending tracks against the joint balance. Individual spending requires no tracking or approval.

This structure provides shared financial management with individual freedom — the combination that sustains household budgets longest.

Written by Marcus Tremblay, Senior Financial Analyst | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry