Table of Contents

Contents are generated from article headings.

Liability for a hacked bank account is shared between the account holder and the bank, determined by fraud type, reporting timeliness, negligence assessment, and applicable consumer protection regulations. In most jurisdictions, banks bear primary responsibility for unauthorized transactions when account holders report fraud promptly and demonstrate reasonable security practices. However, gross negligence—such as sharing credentials, ignoring security alerts, or delaying fraud notification—may shift liability partially or fully to the account holder.

Regulatory frameworks establish baseline protections. In the United States, Regulation E limits consumer liability for electronic fund transfers to $50 if reported within two business days, increasing to $500 if reported within 60 days, and potentially unlimited beyond that timeframe. In the European Union, the Payment Services Directive 2 (PSD2) caps customer liability at €50 for unauthorized transactions reported promptly, with exceptions for gross negligence. The UK’s Financial Conduct Authority provides similar protections, requiring banks to reimburse fraud victims unless negligence is proven.

The core determining factors are timing, documentation, and behavioral compliance with reasonable security standards. Account holders who enable multi-factor authentication, monitor transactions regularly, and report suspicious activity immediately generally receive full reimbursement. Those who share passwords, ignore login alerts, or delay reporting may face partial or total denial of claims. Understanding these liability thresholds and taking proactive protective measures reduces financial exposure and strengthens legal standing when fraud occurs.

Understanding Bank Account Hacking and Liability

Bank account hacking occurs when an unauthorized party gains access to account credentials or devices to withdraw funds, initiate transfers, or steal sensitive financial information. Common methods include phishing attacks that trick users into revealing passwords, SIM swap fraud that redirects authentication codes to attacker-controlled phones, malware that captures keystrokes or credentials, and credential stuffing attacks that exploit leaked password databases from unrelated breaches.

Phishing typically involves fraudulent emails, text messages, or phone calls impersonating banks or trusted institutions, requesting login credentials or directing victims to counterfeit websites. SIM swap attacks convince mobile carriers to transfer a victim’s phone number to a new device controlled by the attacker, allowing interception of SMS-based authentication codes. Malware includes keyloggers, remote access trojans, and banking trojans that monitor user activity or manipulate transactions invisibly.

Credential leaks from third-party data breaches enable attackers to test stolen username-password combinations across multiple financial platforms, exploiting users who reuse credentials. Each attack vector exploits different vulnerabilities, but all share the goal of unauthorized access to account funds or information, triggering liability determinations based on how the breach occurred and how the victim responded.

Types of Fraud and Who May Be Liable

Liability allocation depends on whether transactions were authorized, the fraud mechanism, and contractual terms governing the account. Authorized transactions—where the account holder willingly provides credentials or approves transfers under false pretenses—typically receive less protection than purely unauthorized access where credentials were stolen without user participation.

Card-present fraud involves physical card theft or skimming at point-of-sale terminals, while card-not-present fraud occurs through online purchases or phone orders using stolen card details. Banks generally assume greater liability for card-not-present fraud because merchants lack physical verification, whereas card-present fraud may involve shared responsibility if the account holder failed to report card loss promptly.

Account type also influences liability. Business accounts often have weaker consumer protections than personal accounts, with commercial account agreements frequently placing more responsibility on the account holder for implementing security controls and monitoring activity. Joint accounts may complicate liability when one holder’s negligence enables fraud affecting both parties. Understanding these distinctions helps account holders assess their exposure and take appropriate precautions based on account structure and usage patterns.

Regulatory Protections by Region

United States: Regulation E, implemented by the Federal Reserve and enforced by the Consumer Financial Protection Bureau (CFPB), governs electronic fund transfers and establishes tiered liability based on reporting speed. Account holders who notify banks within two business days of discovering unauthorized transactions face maximum liability of $50. Notification within 60 days increases potential liability to $500. Beyond 60 days, liability may extend to all unauthorized transfers occurring after the 60-day window, potentially resulting in total loss of stolen funds.

The Federal Trade Commission provides additional guidance on fraud reporting and identity theft recovery, recommending immediate notification to financial institutions, credit bureaus, and law enforcement. These federal protections apply broadly to consumer accounts but may offer limited coverage for business accounts or transactions not classified as electronic fund transfers.

European Union: The Payment Services Directive 2 (PSD2), implemented by the European Banking Authority, limits consumer liability to €50 for unauthorized transactions, provided the account holder reports fraud without undue delay upon discovering it. Banks must reimburse the full amount if the account holder was not negligent and reported promptly. However, gross negligence—defined as intentional or severely careless conduct such as writing down passwords in accessible locations or responding to obvious phishing attempts—may void protection entirely.

PSD2 also mandates strong customer authentication for electronic payments, requiring banks to implement multi-factor authentication combining at least two independent elements: knowledge (password), possession (device), or inherence (biometric). This regulatory framework shifts more security responsibility to banks while maintaining accountability for account holder behavior.

United Kingdom: The Financial Conduct Authority oversees fraud protection, requiring banks to reimburse unauthorized transactions unless they can prove gross negligence. The UK has introduced new legislative powers enabling banks to delay suspicious payments up to 72 hours for additional verification, strengthening fraud prevention capabilities. Account holders can report fraud through Action Fraud, the UK’s national reporting center, which coordinates with law enforcement and financial institutions.

These regulatory protections establish baseline rights but do not eliminate the need for individual vigilance, documentation, and timely reporting to maximize reimbursement likelihood.

Account Holder Responsibilities and Best Practices

Account holder responsibilities extend beyond simply maintaining passwords to encompass comprehensive security hygiene, behavioral awareness, and proactive monitoring. Fulfilling these responsibilities not only reduces fraud occurrence but also strengthens legal standing when unauthorized transactions occur. Courts and banks consistently evaluate whether account holders met reasonable care standards when determining reimbursement eligibility.

Timely Reporting of Fraudulent Activity

Timely reporting directly determines maximum liability exposure and reimbursement eligibility. Most regulatory frameworks impose escalating liability the longer fraud goes unreported, creating strong incentives for immediate notification upon discovering suspicious activity.

In practice, timely reporting means contacting the bank within hours or days of discovering unauthorized transactions, not weeks or months. Many banks maintain 24/7 fraud hotlines, mobile app reporting features, and online dispute submission portals to facilitate rapid notification. Delay increases both financial liability under regulatory frameworks and practical recovery difficulty, as stolen funds may be transferred multiple times or withdrawn as cash, making recovery more complex.

Documentation of the notification is critical. Account holders should record the date, time, representative name, and case number assigned to fraud reports. Email confirmations or written dispute letters supplement phone calls, creating verifiable evidence of timely reporting if disputes arise later. Immediate reporting also enables banks to freeze accounts, block additional unauthorized transactions, and initiate investigation while evidence remains fresh.

Documentation and Evidence Collection

Comprehensive documentation strengthens fraud claims and protects against denial based on insufficient evidence. Essential documentation includes complete transaction histories showing unauthorized withdrawals or transfers, screenshots of suspicious emails or text messages used in phishing attempts, records of login alerts or security notifications, and all communications with the bank regarding the fraud investigation.

Transaction histories should cover periods before and after the fraud to establish baseline spending patterns and highlight anomalies. Banks rely on this context when assessing whether transactions appear consistent with account holder behavior or represent clear deviations suggesting unauthorized access. Screenshots should capture full headers, sender information, and content of fraudulent communications to support claims about the attack vector.

Account holders should preserve all physical evidence, including compromised cards, devices potentially infected with malware, or documentation of SIM swap notifications. Forensic examination of devices may be necessary in complex cases where banks dispute negligence claims or when significant amounts are at stake. Organized, chronological documentation demonstrates diligence and strengthens credibility during investigations and potential disputes.

Cybersecurity Hygiene

Multi-factor authentication (MFA) prevents unauthorized access by requiring additional verification beyond passwords. MFA typically combines something the user knows (password), something the user has (smartphone or hardware token), and sometimes something the user is (fingerprint or facial recognition). Enabling MFA significantly reduces account compromise risk because attackers must breach multiple independent authentication factors rather than just stealing a single password.

Strong password practices include using unique, complex passwords for each financial account, storing them in password manager applications rather than browsers or written notes, and changing passwords immediately upon suspicion of compromise. Password managers generate cryptographically random passwords and encrypt storage, reducing both reuse and memorization vulnerabilities.

Device security requires maintaining updated operating systems and applications, installing reputable antivirus software, avoiding public Wi-Fi for financial transactions, and using virtual private networks (VPNs) when remote access is necessary. Phishing awareness involves scrutinizing unexpected communications, verifying sender authenticity through independent channels rather than embedded links, and recognizing common tactics like urgent language, suspicious attachments, or requests for credential confirmation.

Behavioral practices that reduce risk include regularly reviewing account statements for anomalies, setting up transaction alerts for large or unusual activity, and limiting financial application installations to trusted sources. These practices align with reasonable security standards that courts and banks evaluate when assessing negligence in fraud cases.

Avoiding Gross Negligence

Gross negligence is defined as conduct that demonstrates extreme carelessness or willful disregard for security responsibilities, sufficient to void regulatory protections and shift full liability to the account holder. Common behaviors classified as gross negligence include sharing account credentials with third parties, even trusted family members or friends, because doing so violates fundamental security assumptions underlying bank liability.

Ignoring repeated security alerts or login notifications from unfamiliar locations signals reckless disregard for account security. Banks send these alerts specifically to enable rapid response, and systematic failure to investigate or act on them demonstrates negligence sufficient to undermine fraud claims. Delayed reporting beyond reasonable timeframes—such as waiting weeks or months after discovering unauthorized transactions—similarly constitutes negligence by allowing additional losses that timely action would have prevented.

Writing passwords in accessible locations, responding to obvious phishing attempts despite clear warning signs, or disabling security features like MFA without legitimate justification further exemplify gross negligence. Courts and financial institutions distinguish these behaviors from ordinary negligence or simple mistakes, imposing harsher liability consequences when account holder conduct falls far below reasonable security standards. Understanding this threshold helps individuals avoid actions that would void otherwise strong consumer protections.

Bank Responsibilities in Fraud Cases

Banks must balance fraud prevention with customer experience, implementing security controls that protect accounts without creating excessive friction for legitimate users. Regulatory expectations increasingly hold financial institutions accountable for preventable fraud that robust monitoring systems should detect. When banks fail to meet these obligations, they bear greater liability regardless of account holder conduct.

Fraud Detection and Monitoring Systems

Banks maintain automated fraud detection systems that monitor transaction patterns, flag anomalies, and trigger alerts when activity deviates from established behavioral baselines. These systems employ machine learning algorithms trained on historical fraud patterns to identify suspicious transactions based on factors such as unusual geographic locations, atypical transaction amounts, rapid successive withdrawals, or access from unfamiliar devices.

Real-time monitoring enables banks to block potentially fraudulent transactions before completion, sending immediate alerts to account holders for verification. Multi-layered detection includes velocity checks that flag unusually frequent transactions, geolocation analysis that identifies impossible travel patterns, and device fingerprinting that detects access from previously unknown hardware. Advanced systems analyze transaction context, such as whether a large withdrawal follows immediately after a password change or occurs during unusual hours inconsistent with account holder habits.

Banks bear responsibility for implementing robust detection systems and responding promptly to identified threats. Regulatory frameworks increasingly hold financial institutions accountable for preventable fraud that sophisticated monitoring could have detected and blocked. However, detection systems cannot prevent all fraud, particularly when attackers successfully mimic legitimate user behavior or exploit account holder negligence.

Investigation and Reimbursement Process

Bank fraud investigations typically follow standardized procedures that verify claim legitimacy, assess negligence, and determine reimbursement amounts. Upon receiving a fraud report, banks assign case numbers, freeze affected accounts to prevent additional unauthorized activity, and request documentation from account holders detailing the suspected fraud.

Investigation teams review transaction logs, authentication records, IP addresses, device information, and communication histories to reconstruct the fraud sequence and identify how unauthorized access occurred. They compare reported unauthorized transactions against account holder spending patterns, looking for evidence of legitimate use that might undermine fraud claims or indicators of negligence such as credential sharing or ignored security alerts.

Reimbursement decisions depend on these findings. Cases involving clear unauthorized access with no account holder negligence typically result in full reimbursement within 10 business days under Regulation E or similar frameworks. Borderline cases where negligence is ambiguous may result in partial reimbursement or extended investigations. Cases demonstrating gross negligence generally result in denial, with appeals processes available through bank dispute resolution departments or regulatory complaint mechanisms.

Bank policies and account agreements establish specific timelines, documentation requirements, and appeal procedures that supplement regulatory minimums. Understanding these contractual terms helps account holders navigate investigations effectively and escalate disputes when necessary.

Insurance and Coverage Options

Many banks offer fraud protection programs as account features, providing additional reimbursement beyond regulatory minimums or covering fraud types excluded from baseline protections. These programs may include zero-liability guarantees for debit card fraud, identity theft insurance, credit monitoring services, and reimbursement for expenses incurred during fraud recovery such as legal fees or document replacement costs.

Account insurance through the Federal Deposit Insurance Corporation (FDIC) in the United States or similar programs internationally protects deposits against bank failure but does not cover fraud losses. Separate fraud insurance policies, available through homeowners insurance, standalone identity theft policies, or credit card issuer programs, may provide supplemental coverage when bank reimbursement is denied or insufficient.

Credit card fraud generally receives stronger protection than debit card fraud under U.S. law, with the Fair Credit Billing Act limiting cardholder liability to $50 regardless of reporting delay. Many issuers voluntarily provide zero-liability policies exceeding legal requirements. These enhanced protections make credit cards preferable to debit cards for online transactions and situations with elevated fraud risk.

Understanding available insurance and protection options enables account holders to assess total coverage, identify gaps, and make informed decisions about supplemental policies or account type selection based on risk tolerance and usage patterns.

Risk and Failure Scenarios

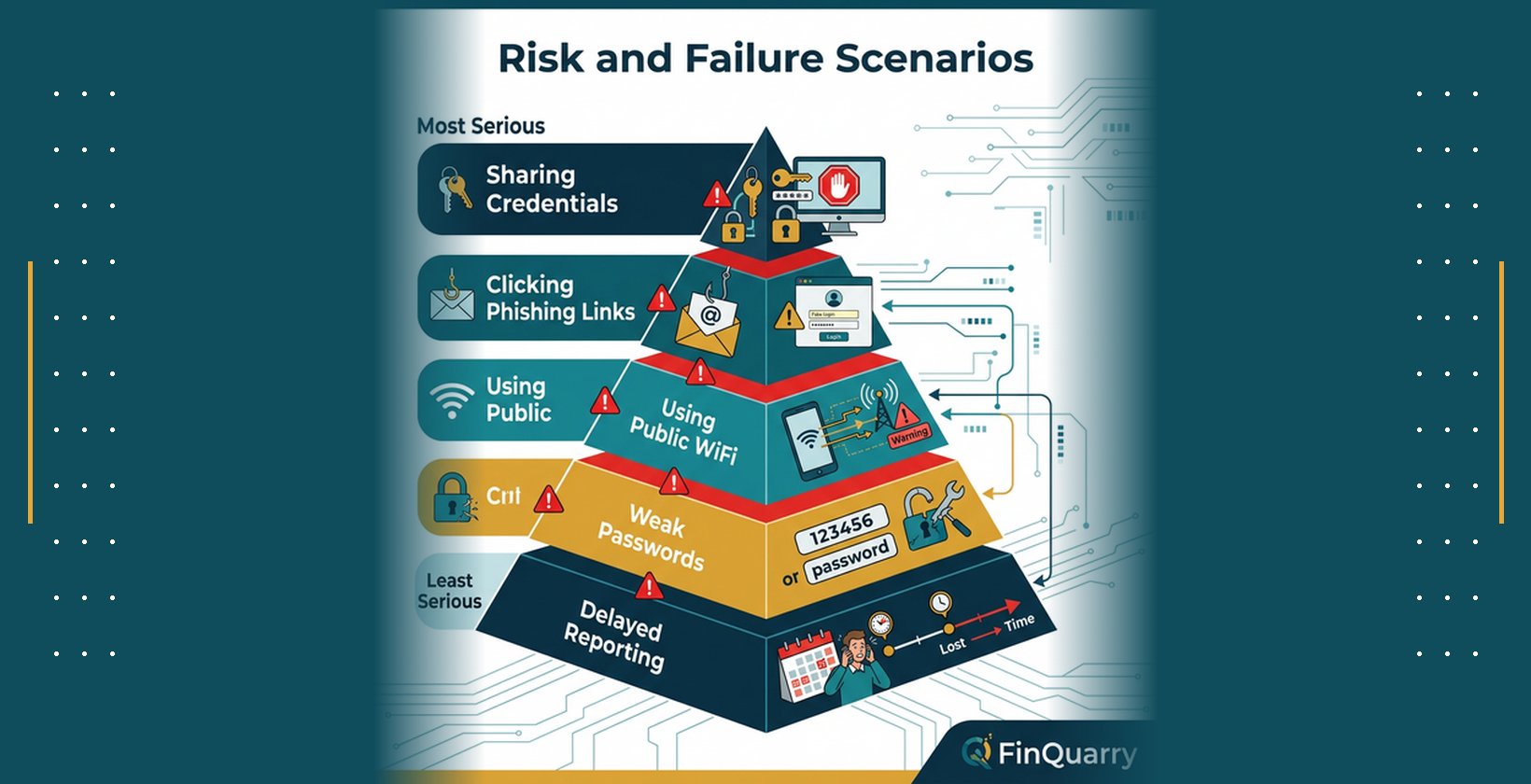

Understanding common failure patterns helps account holders avoid behaviors that void fraud protection and increase financial exposure. Each risk scenario demonstrates how specific actions—or inactions—create vulnerability that banks and courts evaluate when assessing negligence. Recognizing these patterns enables proactive risk mitigation before fraud occurs.

Delayed Reporting → Denied or Reduced Reimbursement

Delayed reporting represents the single most common reason for reduced or denied fraud reimbursement. Regulatory frameworks establish escalating liability tiers specifically to incentivize rapid notification, recognizing that immediate reporting enables banks to freeze accounts, trace stolen funds, and prevent additional unauthorized transactions.

Account holders who discover unauthorized activity but wait days or weeks before reporting often face partial loss recovery, particularly when delay allows attackers to drain accounts completely or transfer funds through multiple intermediaries. Banks may argue that losses occurring after reasonable notification time would have prevented them are the account holder’s responsibility, not the bank’s.

In practice, discovering fraud and reporting within 24 hours generally ensures maximum protection. Delays beyond one week significantly weaken claims, while delays exceeding 60 days under Regulation E or similar frameworks may result in unlimited liability for subsequent unauthorized transactions. Psychological factors such as embarrassment, confusion about reporting procedures, or assumption that small initial fraudulent transactions are errors contribute to delayed reporting, but these explanations do not reduce legal liability.

Weak Authentication / No MFA → Unauthorized Access

Accounts without multi-factor authentication face substantially higher compromise risk and weaker fraud protection. When account holders disable MFA or fail to enable it despite bank recommendations, they may be deemed negligent in fraud investigations, particularly if unauthorized access exploited the absence of this widely available security control.

Password-only authentication is vulnerable to phishing, keylogging, credential stuffing, and social engineering attacks that bypass single-factor protections. Attackers who obtain passwords through these methods gain immediate account access when MFA is absent, enabling rapid fund theft before detection. Banks increasingly view MFA enablement as a baseline reasonable security measure, and its absence may shift liability assessments toward account holder negligence.

Weak passwords—such as dictionary words, personal information, or reused credentials from other accounts—compound vulnerability. Data breaches affecting unrelated services frequently expose username-password combinations that attackers test across banking platforms. Without unique, strong passwords and MFA protection, these attacks succeed at higher rates, and banks may argue that preventable negligence contributed to the compromise.

Shared Credentials → Account Compromise

Sharing account credentials with family members, friends, or third-party service providers fundamentally violates security assumptions and typically voids fraud protection. Bank account agreements universally prohibit credential sharing, and doing so may constitute breach of contract sufficient to deny all reimbursement regardless of other circumstances.

Even when shared credentials are not directly exploited by the recipient, their disclosure increases exposure through multiple pathways: credentials may be intercepted if communicated electronically, stored insecurely by recipients, or inadvertently exposed through compromised recipient devices. Each additional person with credential knowledge multiplies the attack surface and weakens any claim that unauthorized access occurred without account holder participation.

Courts consistently uphold bank denials of fraud claims when credential sharing is proven, reasoning that the account holder voluntarily eliminated security controls designed to protect against unauthorized access. This principle extends to business contexts where employees share credentials, personal contexts where family members access accounts, and service contexts where third-party financial management requires credential disclosure.

Ignoring Alerts → Delayed Detection, Financial Loss

Security alerts serve as early warning systems that enable rapid response to potential compromises. Banks send login notifications, unusual transaction alerts, and suspicious activity warnings specifically to trigger account holder verification before significant losses occur. Systematically ignoring these alerts demonstrates negligence that weakens fraud claims and may increase liability.

Account holders who routinely dismiss login alerts from unfamiliar locations or ignore notifications about large withdrawals miss opportunities to detect fraud in its early stages when recovery is most feasible. By the time fraud is eventually noticed through other means—such as account balance discrepancies or declined transactions—attackers may have drained accounts or transferred funds beyond practical recovery.

Establishing alert response protocols—such as investigating any unfamiliar login immediately or verifying large transactions before dismissing notifications—reduces both fraud occurrence and liability exposure. Documented history of responding to alerts strengthens claims that unauthorized transactions represent genuine fraud rather than authorized activity later disputed.

Overconfidence → Neglecting Protective Measures

Overconfidence bias leads individuals to underestimate personal fraud risk, believing “it won’t happen to me” despite widespread fraud prevalence. This psychological pattern often manifests as failure to enable available security features, delayed security updates, or casual credential management under the assumption that basic precautions suffice.

Statistics demonstrate that fraud affects millions of account holders annually across all demographic groups, suggesting that individual risk is substantial regardless of perceived personal invulnerability. Overconfidence that prevents adoption of MFA, password managers, or regular statement review increases actual vulnerability while simultaneously weakening legal protections by demonstrating negligence if fraud occurs.

Behavioral economics research shows that individuals consistently underestimate low-probability, high-impact risks like account hacking, leading to insufficient preventive action. Recognizing this cognitive bias and implementing protective measures despite perceived low risk aligns behavior with statistical reality and legal expectations for reasonable security conduct.

Legal Recourse and Consumer Protection

Legal recourse provides essential remedies when banks improperly deny fraud claims or fail to meet regulatory obligations. Regulatory complaint mechanisms often succeed where direct bank appeals fail, particularly when denials rest on questionable negligence assessments. Understanding available escalation pathways ensures account holders can pursue all recovery options when initial reimbursement requests are rejected.

Filing Complaints with Regulators

When banks deny fraud claims or reimbursement is insufficient, account holders may file complaints with regulatory authorities that oversee financial institutions and enforce consumer protection laws. In the United States, the Consumer Financial Protection Bureau (CFPB) accepts complaints about banks, credit unions, and other financial companies, investigating disputes and facilitating resolution.

The complaint process typically requires submitting detailed information about the fraud, documentation of bank interactions, and explanation of why the bank’s response was inadequate. The CFPB forwards complaints to the financial institution, which must respond within specified timeframes and attempt resolution. Complaint statistics become part of the institution’s regulatory record, creating reputational and compliance incentives for fair treatment.

In the United Kingdom, the Financial Conduct Authority provides similar oversight, with account holders able to escalate unresolved disputes to the Financial Ombudsman Service, which offers free, independent dispute resolution. The FCA has issued guidance on fraudulent payments and reimbursement standards, requiring banks to demonstrate that account holders were grossly negligent before denying claims.

European Union member states maintain national financial authorities that enforce PSD2 requirements and process consumer complaints. Cross-border fraud involving accounts in multiple jurisdictions may require coordination among regulators, with resolution timelines potentially extending beyond domestic cases.

Filing regulatory complaints does not guarantee reimbursement but creates formal records, triggers mandatory bank responses, and may reveal patterns of problematic conduct that support legal action. Regulatory intervention often succeeds where direct bank appeals fail, particularly when denials rest on questionable negligence assessments.

Litigation and Dispute Resolution

Legal action becomes appropriate when regulatory complaints fail to resolve disputes and losses exceed small claims thresholds or involve significant financial hardship. Hiring legal counsel experienced in consumer finance and fraud cases helps assess claim strength, navigate procedural requirements, and pursue recovery through formal litigation or arbitration.

Small claims court offers accessible dispute resolution for losses below jurisdictional limits, typically ranging from $2,500 to $10,000 depending on state or country. These courts permit self-representation, streamlined procedures, and faster resolution than traditional litigation, making them practical options for moderate fraud losses. Evidence requirements remain substantial—documented timelines, bank communications, and regulatory complaint histories strengthen cases significantly.

Formal litigation in civil courts applies when losses exceed small claims limits or when cases involve complex legal questions about negligence standards, contractual interpretation, or regulatory compliance. Class action litigation may be available when banks engage in systematic improper denial of fraud claims affecting numerous account holders similarly.

Many bank account agreements include mandatory arbitration clauses requiring disputes to be resolved through private arbitration rather than courts. Arbitration procedures vary but generally involve submitting disputes to neutral arbitrators who render binding decisions. Understanding whether arbitration clauses apply and how they affect legal options is essential before pursuing litigation.

Successful legal recovery requires proving that banks violated regulatory obligations, breached account agreements, or improperly assessed negligence. Legal costs may exceed recovery amounts in smaller cases, making consultation with attorneys important before committing to litigation.

Understanding Account Terms and Policies

Bank account agreements establish contractual obligations, liability allocations, and dispute procedures that supplement regulatory protections. These agreements specify account holder responsibilities for credential security, notification timelines for unauthorized transactions, bank investigation procedures, and limitations on liability.

Liability clauses may impose stricter timelines or documentation requirements than regulatory minimums, creating contractual obligations that exceed legal baselines. Fraud disclaimers often clarify circumstances where banks disclaim responsibility, such as losses resulting from credential sharing, failure to maintain updated contact information, or use of unsecured networks.

Account policies also govern dispute resolution procedures, including internal appeals processes, arbitration requirements, and timeframes for complaint submission. Understanding these contractual terms before fraud occurs enables account holders to comply with procedural requirements and preserve legal rights.

Periodic policy updates may change terms, and account holders typically consent to modifications by continuing to use accounts after notification. Reviewing updated agreements helps identify changed responsibilities or weakened protections that might warrant switching financial institutions or account types.

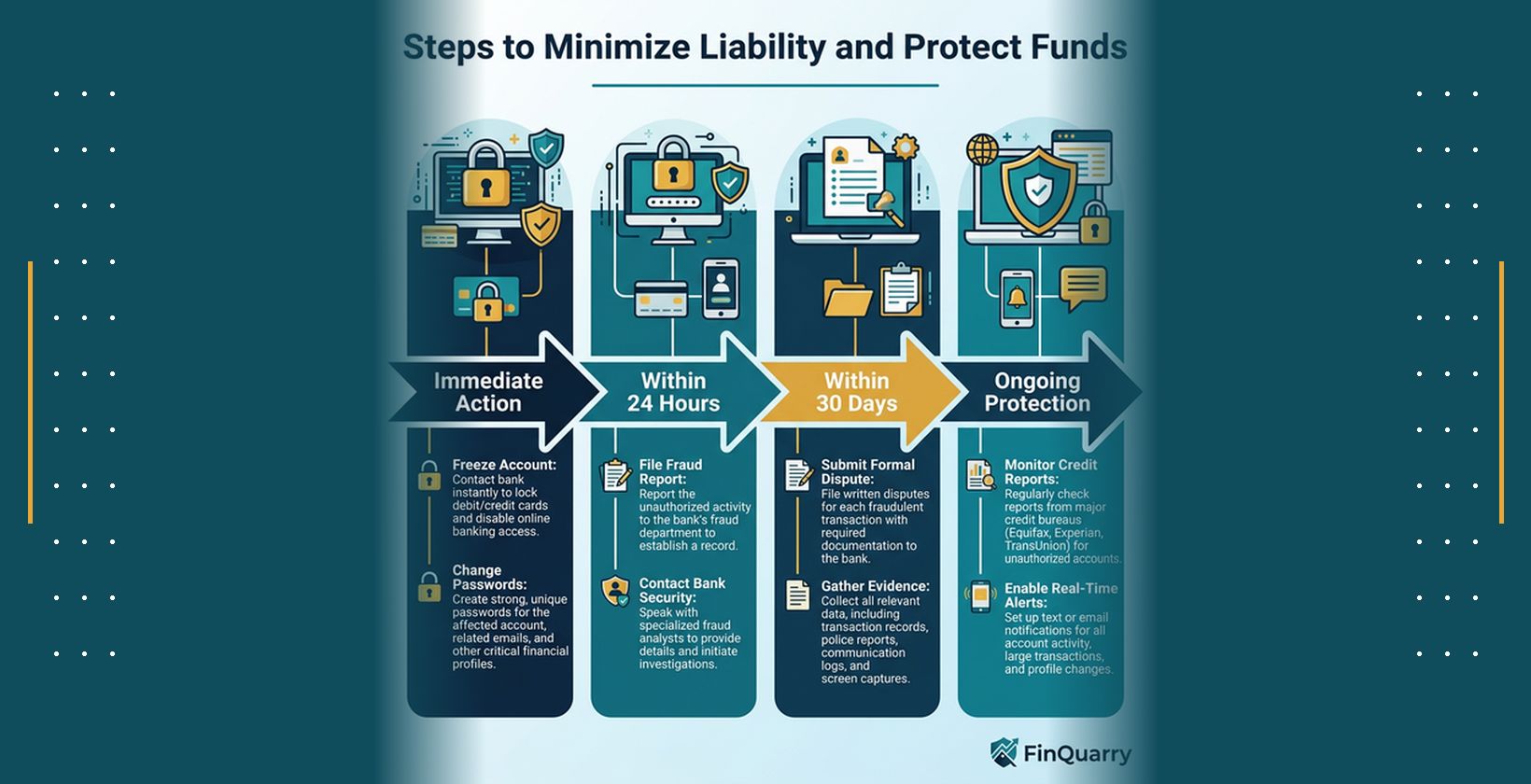

Practical Steps to Minimize Liability and Protect Funds

Implementing these practical steps transforms abstract security principles into concrete protective actions that reduce both fraud occurrence and legal liability. Each measure addresses specific attack vectors while simultaneously demonstrating reasonable care that strengthens reimbursement claims if fraud occurs. Consistent application of these practices creates layered security that significantly reduces account compromise risk.

Enable multi-factor authentication on all financial accounts using authenticator apps or hardware tokens rather than SMS-based codes vulnerable to SIM swap attacks. Multi-factor authentication prevents unauthorized access even when passwords are compromised, representing the single most effective individual security control available.

Monitor transactions daily through mobile banking apps, email alerts, or account aggregation services that consolidate activity across multiple institutions. Daily monitoring enables detection of unauthorized transactions within hours rather than weeks, maximizing reimbursement eligibility under regulatory frameworks and minimizing total losses.

Report suspicious activity immediately upon discovery, documenting notification through multiple channels including phone calls, secure messages through banking portals, and written correspondence. Immediate reporting triggers account freezes, initiates investigations while evidence is fresh, and establishes compliance with regulatory and contractual notification requirements.

Keep documentation of all communications with banks, including case numbers, representative names, dates, and summaries of conversations. Written confirmation of verbal reports, screenshots of online dispute submissions, and organized chronological records strengthen fraud claims and support escalation if disputes arise.

Understand bank and regulatory protections applicable to specific account types and jurisdictions, including liability limits, reporting timelines, and negligence standards. Knowledge of rights and obligations enables proactive compliance and informed decision-making about account selection and security practices.

Consider account fraud insurance through homeowners policies, standalone identity theft coverage, or bank-offered protection programs that supplement regulatory minimums. Insurance provides additional financial protection when bank reimbursement is denied or insufficient, particularly for business accounts with weaker consumer protections.

What happens if I report fraud late?

Late reporting increases liability exposure under tiered regulatory frameworks like Regulation E, which escalates maximum liability from $50 if reported within two business days to $500 within 60 days, and potentially unlimited for unauthorized transactions occurring more than 60 days after account statements are provided. Banks may also deny reimbursement entirely if delay prevented investigation or recovery efforts, arguing that timely reporting would have limited losses. Practical consequences include reduced likelihood of full reimbursement, weaker legal standing in disputes, and potential classification of delay as negligence contributing to losses.

Does MFA guarantee full protection?

Multi-factor authentication significantly reduces unauthorized access risk but does not provide absolute protection or guarantee reimbursement. Sophisticated attacks such as man-in-the-middle phishing that intercepts authentication codes in real-time, social engineering that manipulates users into approving fraudulent login requests, or malware that compromises devices can bypass MFA protections. However, MFA enablement demonstrates reasonable security practices that strengthen fraud claims and reduce negligence findings, improving reimbursement likelihood even when attacks succeed through advanced methods.

Who is liable in digital-only banks?

Digital-only banks and neobanks generally operate under the same regulatory frameworks as traditional banks, including Regulation E in the United States and PSD2 in the European Union, providing comparable consumer protections. However, lack of physical branches may complicate fraud reporting and investigation procedures, potentially affecting resolution timelines. Account holders should verify that digital banks maintain regulatory compliance, offer fraud protection programs, and provide accessible customer service channels for reporting unauthorized transactions. Liability allocation follows the same negligence and reporting timeline standards regardless of bank type.

How does negligence affect reimbursement?

Negligence assessment determines whether account holders receive full reimbursement, partial reimbursement, or denial. Ordinary negligence—such as using weak but not egregiously poor passwords or briefly delaying fraud reporting—may result in partial liability under regulatory frameworks, while gross negligence such as credential sharing or systematically ignoring security alerts typically voids protection entirely. Banks must prove negligence to deny claims under PSD2 and similar frameworks, shifting burden of proof to financial institutions. Documentation of security practices, timely reporting, and compliance with reasonable care standards strengthens reimbursement claims and reduces negligence findings.

Are business accounts treated differently from personal accounts?

Business accounts typically receive weaker fraud protection than personal consumer accounts, with Regulation E and similar frameworks often excluding commercial accounts or providing reduced protection. Business account agreements frequently impose stricter security requirements, documentation obligations, and reporting timelines, with liability terms negotiated based on account size and transaction volume. Businesses should implement enhanced security controls including multi-user authentication, transaction limits, and dedicated fraud monitoring services to compensate for reduced regulatory protection. Understanding contractual liability terms before opening business accounts enables informed risk management decisions.

Can I recover money from cross-border fraud?

Cross-border fraud recovery depends on jurisdictional treaties, account location, and fraud destination. Funds transferred internationally may be subject to different recovery mechanisms, often requiring coordination among multiple regulatory authorities and extended investigation timelines. International wire transfers completed before fraud detection are particularly difficult to reverse, as receiving banks in foreign jurisdictions may have limited obligations to cooperate with recovery efforts. Account holders should report cross-border fraud to domestic regulators, local law enforcement, and international fraud reporting networks. Recovery success rates are generally lower for international fraud than domestic cases, emphasizing prevention importance.

How to escalate unresolved claims to regulators?

Escalation begins by exhausting internal bank dispute resolution procedures, typically involving initial fraud reports, appeals to fraud investigation departments, and formal written complaints to executive customer service offices. After receiving final denial or unsatisfactory resolution, account holders may file complaints with appropriate regulatory authorities: the CFPB for U.S. consumer accounts, the FCA or Financial Ombudsman Service in the UK, or national financial authorities in EU member states. Complaints should include comprehensive documentation of fraud, bank communications, and explanation of why bank resolution was inadequate. Regulatory complaints trigger mandatory bank responses and independent review, often succeeding where direct appeals fail. Additional options include reporting fraud to Action Fraud in the UK or consulting consumer protection organizations for guidance on escalation procedures.

Summary of Responsibility and Action Plan

Liability for bank account hacking is distributed between account holders and banks based on fraud type, account holder conduct, reporting timeliness, and applicable regulatory frameworks. Banks bear primary responsibility for implementing robust fraud detection systems, investigating unauthorized transactions, and reimbursing losses when account holders comply with reasonable security expectations. Account holders bear responsibility for enabling available security features, monitoring accounts regularly, reporting fraud immediately, and avoiding gross negligence behaviors that void protections.

Timely reporting, multi-factor authentication, strong passwords, and comprehensive documentation form the foundation of effective fraud protection and liability minimization. These behavioral practices align with regulatory expectations for reasonable security conduct, strengthening reimbursement claims and reducing vulnerability to negligence findings that shift liability.

Regulatory protections under Regulation E, PSD2, and FCA guidance establish baseline rights but require proactive compliance. Understanding jurisdiction-specific rules, reporting deadlines, and documentation requirements enables account holders to maximize protection and preserve legal recourse when fraud occurs.

When bank reimbursement is denied or insufficient, escalation through regulatory complaints, legal consultation, and formal dispute resolution mechanisms provides additional recovery pathways. Recent UK legislative changes have strengthened bank powers to combat fraud, while FCA guidance on fraudulent payments clarifies reimbursement obligations and negligence standards.

Account holder vigilance reduces loss severity and improves recovery outcomes, but does not eliminate fraud risk entirely. Maintaining security best practices, understanding contractual and regulatory rights, and acting decisively when unauthorized activity is detected collectively minimize both financial loss and legal liability in bank account hacking cases.

Disclaimer: This content explains general principles of bank account hacking liability using regulatory frameworks, banking policies, and cybersecurity standards current as of 2026. Actual outcomes, reimbursement amounts, and legal consequences vary by jurisdiction, specific bank policies, account type, and individual circumstances. Always consult legal counsel or financial advisors for guidance specific to your situation.