Table of Contents

Contents are generated from article headings.

Credit utilization measures the percentage of available revolving credit currently in use, calculated by dividing total credit card balances by total credit limits. This ratio represents one of the most influential factors in credit scoring models, accounting for approximately 30 percent of FICO scores and similar weight in VantageScore calculations. Understanding how credit utilization works helps consumers manage credit responsibly and maintain strong credit profiles.

The concept applies specifically to revolving credit accounts such as credit cards and home equity lines of credit, not installment loans like mortgages or auto financing. Lenders and credit scoring models evaluate utilization both at the aggregate level across all revolving accounts and at the individual account level for each credit card. These dual evaluation methods create nuanced effects on credit scores that many consumers overlook when managing their credit.

Credit utilization does not represent credit card spending volume or payment behavior directly. Rather, utilization reflects the snapshot balance reported to credit bureaus relative to available credit limits at specific reporting times. Two consumers with identical spending patterns can show vastly different utilization ratios based solely on when their statements close and when they make payments relative to bureau reporting cycles.

Jurisdiction and temporal scope notice: Credit utilization principles described here reflect general U.S. credit scoring practices as of 2026. Specific impacts on credit scores may vary by scoring model version, credit bureau, and individual credit profile characteristics. Lender evaluation criteria differ across institutions and loan types.

Revolving vs Installment Credit

Revolving credit accounts allow borrowers to carry balances that fluctuate over time, with credit limits that reset as balances are paid down. Credit cards represent the most common form of revolving credit, along with home equity lines of credit and certain personal lines of credit. These accounts have no fixed repayment timeline, and borrowers can choose to pay the full balance or make minimum payments while carrying remaining balances forward.

Installment credit operates under fundamentally different mechanics. Installment loans such as mortgages, auto loans, and student loans establish fixed loan amounts with predetermined repayment schedules. Borrowers receive the full loan amount upfront and repay through regular installment payments until the balance reaches zero. These accounts do not reset or allow additional borrowing without new loan applications.

Credit utilization calculations apply only to revolving credit accounts because these accounts have stated credit limits that create measurable utilization ratios. Installment loans lack comparable credit limits, making utilization ratio calculations inapplicable. A borrower with a 20,000 dollar auto loan and 15,000 dollar remaining balance does not have 75 percent utilization in credit scoring terms, as installment balances are evaluated through different scoring factors.

Per-Card vs Aggregate Utilization

Aggregate utilization combines all revolving account balances divided by all revolving credit limits to produce an overall utilization percentage. A consumer with three credit cards showing 2,000 dollars total balances across 10,000 dollars total limits has 20 percent aggregate utilization regardless of how balances distribute across individual cards.

Per-card utilization calculates the ratio separately for each revolving account, revealing how close individual cards come to their respective limits. Credit scoring models evaluate both aggregate and per-card utilization independently, with high utilization on any single card potentially lowering scores even when aggregate utilization appears healthy. A consumer with 1,000 dollar balance on a 1,200 dollar limit card shows 83 percent utilization on that account, signaling maxed-out risk despite low overall utilization.

The distinction matters because lenders interpret high per-card utilization as indicating financial stress or credit line exhaustion, even when total available credit remains substantial. Multiple credit cards with low individual balances generally produce better credit outcomes than concentrating balances on one or two cards, assuming identical aggregate utilization. This dual evaluation structure rewards balanced credit distribution across available accounts.

Why Lenders Care About Credit Utilization

Lenders use credit utilization as a risk indicator predicting default probability and payment reliability. High utilization correlates with increased financial stress, suggesting borrowers may struggle to manage existing obligations or may be accumulating debt faster than income growth supports. Statistical data across large borrower populations shows that consumers with utilization above 80 percent default at rates substantially higher than those maintaining utilization below 30 percent.

Utilization also provides a real-time risk signal that updates monthly as account balances change. Unlike credit score factors such as payment history or account age that reflect past behavior, utilization ratios respond immediately to current financial conditions. A borrower experiencing income loss or unexpected expenses typically shows rising utilization before missed payments occur, giving lenders an early warning signal of deteriorating financial health.

The mechanism through which utilization affects lending decisions extends beyond credit score impacts. Lenders often evaluate utilization directly during underwriting processes, particularly for mortgage applications and other major credit decisions. A loan applicant with excellent payment history but 70 percent credit card utilization may face additional scrutiny or higher interest rates compared to an applicant with identical credit scores but 15 percent utilization.

How Credit Utilization Is Calculated

Credit utilization calculation follows a straightforward formula applied to revolving credit accounts. The basic calculation divides current account balance by credit limit, then multiplies by 100 to express the result as a percentage. A credit card with 1,500 dollar balance and 5,000 dollar limit shows 30 percent utilization through this calculation.

The timing of when balances are measured significantly affects calculated utilization. Credit card issuers report account information to credit bureaus according to their own reporting schedules, typically once monthly around the statement closing date. The balance present when the issuer reports to bureaus becomes the utilization figure reflected in credit scores, regardless of whether borrowers pay balances in full after statement generation.

Formula and Numeric Examples

Single account utilization equals balance divided by credit limit multiplied by 100. A cardholder with 800 dollar balance on a 4,000 dollar limit card calculates utilization as 800 divided by 4,000 equals 0.20, multiplied by 100 equals 20 percent. This per-card ratio applies individually to each revolving account.

Aggregate utilization sums all revolving balances and divides by summed credit limits. A consumer with three cards showing balances of 500 dollars, 1,200 dollars, and 300 dollars against limits of 3,000 dollars, 5,000 dollars, and 2,000 dollars respectively calculates aggregate utilization as 2,000 dollars total balance divided by 10,000 dollars total limits equals 0.20, or 20 percent overall.

The same aggregate utilization can produce different credit score effects based on per-card distribution. Twenty percent aggregate utilization spread evenly as 200 dollars on a 1,000 dollar card, 600 dollars on a 3,000 dollar card, and 1,200 dollars on a 6,000 dollar card maintains consistent 20 percent per-card ratios. Alternatively, concentrating 2,000 dollars on one 2,500 dollar limit card while leaving others at zero balance creates 80 percent utilization on the active card despite identical 20 percent aggregate utilization.

Reporting Timing Effects

Credit card issuers typically report account information to credit bureaus monthly, with most using statement closing dates as reporting triggers. The balance present on the statement closing date becomes the reported balance, regardless of payment timing within the billing cycle. A cardholder who charges 3,000 dollars during a billing period but pays the balance to 500 dollars before the statement closes may show only 500 dollars utilization in credit reports.

This timing mechanism creates strategic opportunities for utilization management. Consumers who make payments before statement closing dates lower their reported utilization compared to those who wait until payment due dates after statements generate. A borrower with consistent spending patterns might show 40 percent utilization if paying after statement close but only 10 percent utilization if paying immediately before statement generation.

Reporting date variation across different credit card issuers adds complexity to utilization management. Not all cards report on the same day of the month, meaning utilization snapshots occur at different times for different accounts. A consumer managing multiple cards must track individual statement closing dates to optimize reported utilization across all accounts simultaneously.

Some issuers report mid-cycle or on schedules unrelated to statement dates, though this practice remains less common. When issuers use non-standard reporting timing, cardholders lose predictability about which balance will appear in credit reports, making strategic utilization management more difficult.

Differences Between FICO and VantageScore

FICO scoring models weight credit utilization at approximately 30 percent of total score calculation, representing the second-largest factor after payment history. Within this utilization component, FICO evaluates both aggregate utilization across all revolving accounts and individual account utilization separately. High utilization on even one account can lower scores meaningfully under FICO methodology.

VantageScore models also weight utilization heavily, though the exact percentage varies by model version. VantageScore 3.0 and 4.0 combine utilization with overall credit usage patterns into a category called “credit usage” that represents roughly 20 to 40 percent of score calculation depending on individual credit profile characteristics. The models evaluate similar metrics but may respond differently to specific utilization thresholds.

The practical scoring differences emerge most clearly at utilization extremes. FICO models tend to penalize utilization above 30 percent more aggressively than VantageScore in some profile types, while VantageScore may show greater sensitivity to very low utilization near zero percent. These variations mean the same utilization ratio can produce different score outcomes depending on which model a lender uses.

Both scoring families update utilization impact monthly as new credit report data arrives. Unlike factors such as derogatory marks that persist for years, utilization effects reflect current reported balances and can improve immediately when balances decrease. A consumer who reduces utilization from 80 percent to 20 percent typically sees score increases within one to two billing cycles as updated balances report to bureaus.

Why Credit Utilization Matters

Credit utilization affects financial outcomes through multiple mechanisms beyond direct credit score impacts. The relationship between utilization ratios and creditworthiness extends into lending decisions, interest rate determinations, and long-term financial flexibility. Understanding these broader implications helps consumers prioritize utilization management within overall credit strategies.

The significance of utilization varies by credit profile maturity and credit goals. Consumers actively seeking new credit approvals or rate-sensitive financing face more immediate utilization pressure than those maintaining credit without near-term borrowing needs. However, maintaining healthy utilization provides ongoing benefits through preserved borrowing capacity and improved financial optionality.

Impact on Credit Score

Credit utilization directly influences credit scores through the amounts owed category in FICO models and credit usage evaluation in VantageScore systems. Movement from very low utilization around 5 percent to moderate utilization near 30 percent typically reduces scores by 10 to 30 points depending on overall credit profile strength. Increases from 30 percent to 50 percent or higher often trigger score decreases of 30 to 80 points as utilization crosses into high-risk territory.

The score impact operates on a gradient rather than fixed thresholds. Utilization at 29 percent does not categorically differ from 31 percent in scoring impact, though general patterns show accelerating score penalties as utilization rises above 30 percent, 50 percent, and 70 percent marks. Very high utilization above 90 percent signals severe financial stress and typically produces the largest score reductions.

Zero percent utilization does not maximize credit scores under most scoring models. Models interpret complete absence of revolving balance activity as potentially indicating inactive credit use rather than excellent credit management. Optimal utilization for score maximization typically falls between 1 percent and 10 percent, demonstrating active credit use while maintaining very low balance-to-limit ratios.

Per-card utilization can override favorable aggregate ratios in score determination. A consumer with 15 percent overall utilization but one card at 95 percent utilization experiences score damage from the maxed-out account despite low aggregate usage. This individual account sensitivity explains why distributing balances across multiple cards often produces better scores than concentrating debt on fewer accounts.

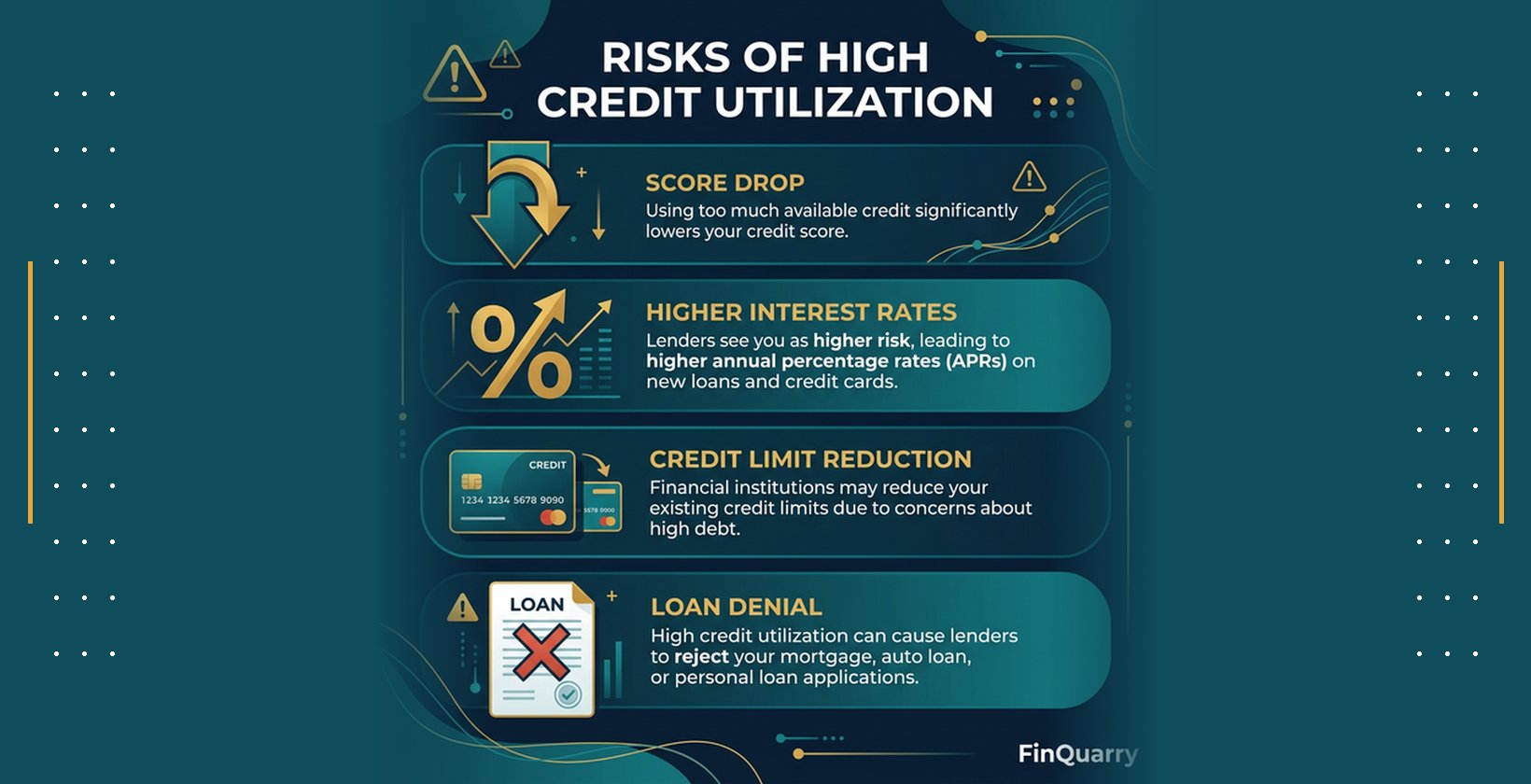

Influence on Loan Approval and Interest Rates

Lenders evaluate credit utilization during loan underwriting independently of credit scores, using utilization as a direct risk assessment tool. Mortgage lenders commonly scrutinize credit card balances and utilization ratios when calculating debt-to-income ratios and assessing borrower financial capacity. High utilization may trigger additional documentation requirements, larger down payment needs, or interest rate adjustments even when credit scores meet minimum thresholds.

Auto lenders and personal loan underwriters similarly consider utilization when determining approval and pricing. A borrower with 60 percent credit card utilization faces higher perceived default risk than one with 10 percent utilization at identical credit scores, potentially resulting in interest rate differences of 1 to 3 percentage points or more depending on loan type and lender criteria.

The relationship between utilization and loan costs compounds over loan terms. A borrower who receives a mortgage at 6.5 percent APR due to high utilization instead of 6.0 percent with lower utilization pays approximately 15,000 dollars more in interest over a 30-year term on a 300,000 dollar loan. These incremental rate differences create substantial long-term cost implications that exceed the immediate inconvenience of elevated utilization.

Credit card issuers also use utilization patterns to adjust terms on existing accounts. Consumers who consistently carry high utilization may experience credit limit decreases, interest rate increases, or account closures if issuers perceive rising default risk. These adverse actions create feedback loops where utilization increases further as available credit shrinks, potentially accelerating financial deterioration.

Long-Term Financial Health Implications

Sustained high utilization typically reflects underlying financial imbalances between income and spending. Consumers who routinely carry balances exceeding 50 percent of available credit often face structural budget deficits where expenses exceed income over extended periods. This pattern creates debt accumulation cycles where interest charges compound balances faster than minimum payments reduce principal.

The interest cost burden from high utilization directly reduces available income for saving, investing, or other financial goals. A consumer carrying 10,000 dollars in credit card debt at 20 percent APR pays approximately 2,000 dollars annually in interest charges, representing lost financial capacity that could otherwise build emergency savings or retirement assets. Over decades, these opportunity costs compound into substantial wealth differences.

High utilization also constrains financial flexibility and emergency response capacity. Consumers who already use most available credit lack buffer capacity to handle unexpected expenses without further increasing balances or seeking new credit sources. This vulnerability increases financial stress and limits options during income disruptions or emergency situations.

Conversely, maintaining low utilization preserves borrowing capacity for strategic opportunities or emergencies while minimizing interest costs. Consumers with substantial unused credit limits can leverage credit for beneficial purposes such as balance transfers to lower rate cards, business investments, or temporary cash flow management without approaching credit limits or triggering utilization penalties.

Risks of High or Mismanaged Utilization

Credit utilization mismanagement creates multiple risk pathways that extend beyond simple score reduction. These risks range from immediate credit score damage to longer-term financial vulnerability and reduced access to credit when most needed. Understanding specific failure patterns helps consumers avoid common utilization traps.

The consequences of high utilization often compound through interconnected mechanisms. Initial score decreases lead to higher interest rates on existing variable-rate accounts, increasing balances through higher interest charges, which further elevates utilization in self-reinforcing cycles. Breaking these patterns typically requires deliberate intervention rather than passive balance management.

Over-Utilization and Score Drops

Utilization above 80 percent triggers severe credit score penalties in most scoring models, often reducing scores by 80 to 150 points compared to optimal utilization levels. This threshold represents a critical risk zone where lenders interpret utilization as indicating maxed-out credit lines and imminent financial distress. Scores in this range typically fall into subprime or near-subprime territories even when payment history remains perfect.

The speed of score recovery after utilization reduction varies by individual credit profiles. Consumers with otherwise strong credit histories may see scores rebound by 50 to 100 points within one to two months of reducing utilization from 80 percent to 20 percent. Those with thinner credit files or existing derogatory marks typically experience slower recovery as utilization improvement competes with other negative factors.

Sudden utilization spikes from large purchases or emergency expenses create temporary score drops that persist until balances decrease. A consumer who makes a 5,000 dollar emergency purchase on a 6,000 dollar limit card immediately jumps to 83 percent utilization on that account, likely reducing credit scores by 40 to 80 points until the balance pays down. The timing of when this occurs relative to credit applications significantly affects access to new credit.

Ignoring Per-Card Differences

Maintaining low aggregate utilization while allowing individual cards to approach their limits creates hidden credit score damage that many consumers fail to recognize. A borrower with 15 percent overall utilization might assume their credit profile appears healthy, but if this results from one card at 90 percent utilization and others at zero, credit scores reflect the maxed-out card more than the favorable aggregate ratio.

Lenders view high individual card utilization as signaling inability to manage that specific credit line effectively, raising concerns about whether the borrower lacks sufficient income to support current obligations. A consumer with six credit cards totaling 30,000 dollars in limits who concentrates 5,000 dollars on one 5,500 dollar limit card demonstrates different risk characteristics than one distributing the same 5,000 dollars across all six cards proportionally.

The per-card penalty applies even when high utilization results from deliberate strategy rather than financial stress. Consumers who intentionally use one rewards card heavily while leaving others dormant face score penalties identical to those experiencing genuine financial difficulty, as scoring models cannot distinguish intentional concentration from capacity constraints.

Balance concentration also creates vulnerability to sudden credit limit decreases. Issuers who see consistently maxed accounts may reduce limits to match current balances, immediately converting 90 percent utilization to 100 percent and triggering additional score damage plus potential over-limit fees if limits drop below existing balances.

Impact of Missed Payments Combined With High Utilization

High utilization combined with late payments creates compounding credit score damage exceeding either factor independently. A consumer with 70 percent utilization who misses a payment experiences score decreases potentially reaching 150 to 200 points or more, as payment delinquency represents the most severe negative factor while high utilization signals existing financial stress. This combination typically drops scores into deep subprime ranges.

The dual impact persists for extended periods. While utilization damage can reverse quickly through balance reduction, late payment marks remain on credit reports for seven years from the delinquency date. Consumers face sustained score suppression even after resolving high balances if payment history shows recent delinquencies.

Lenders interpret the combination as indicating severe financial distress requiring immediate risk mitigation. Credit card issuers may respond to this pattern with credit limit decreases, interest rate increases to penalty levels, or account closures. These actions further constrain available credit and can force the consumer into higher-cost credit alternatives.

The pattern also affects debt resolution options. Consumers attempting to qualify for debt consolidation loans or balance transfer cards typically face denial when credit reports show both high utilization and recent late payments, leaving them trapped with existing high-rate debt without access to more favorable refinancing alternatives.

How to Optimize Your Credit Utilization

Strategic utilization management focuses on maintaining ratios that maximize credit scores while preserving financial flexibility. Effective optimization requires understanding how different reduction methods affect utilization timing, considering both immediate score impacts and long-term credit capacity preservation. The optimal approach varies by individual financial circumstances and credit goals.

Utilization optimization differs from simple balance reduction by considering reporting timing, per-card distribution, and opportunity costs of different payment strategies. Consumers seeking immediate score improvement for pending credit applications employ different tactics than those gradually improving utilization without time pressure.

Paying Off Balances Strategically

Making payments before statement closing dates reduces reported utilization more effectively than paying after statements generate but before due dates. A cardholder who charges 2,000 dollars monthly but pays it down to 200 dollars before the statement closes shows only 10 percent utilization on a 2,000 dollar limit despite identical 2,000 dollar monthly spending as someone who pays after statement close.

This timing strategy proves particularly valuable when consumers cannot pay balances to zero but can significantly reduce them before reporting occurs. Even partial payments timed to statement closing dates lower reported utilization proportionally to payment amounts, providing score benefits without requiring full balance elimination.

Multiple payment cycles within billing periods can further reduce reported balances. Making mid-cycle payments to lower balances before large planned purchases prevents temporary utilization spikes. A consumer planning a 1,500 dollar purchase on a card with 1,000 dollar existing balance and 3,000 dollar limit could pay down to 300 dollars before the purchase, keeping utilization near 60 percent rather than approaching 83 percent.

Prioritizing high utilization accounts when distributing available payment funds maximizes per-card utilization improvement. A borrower with 500 dollars available to pay toward balances achieves greater score benefit by eliminating a 500 dollar balance on a 600 dollar limit card showing 83 percent utilization than by reducing a 3,000 dollar balance on a 10,000 dollar limit card from 30 percent to 25 percent.

Requesting Credit Limit Increases

Credit limit increases directly reduce utilization ratios without requiring balance reduction. A cardholder with 2,000 dollar balance on a 5,000 dollar limit showing 40 percent utilization who receives a limit increase to 8,000 dollars immediately drops to 25 percent utilization without changing balance. This mechanical reduction can improve credit scores by 20 to 40 points or more depending on starting utilization levels.

Most credit card issuers allow limit increase requests through online account interfaces or customer service calls. Some issuers conduct hard credit inquiries when evaluating increase requests, temporarily reducing scores by 5 to 10 points, while others use soft inquiries that do not affect scores. Consumers should verify inquiry type before requesting increases when scores are sensitive.

Automatic limit increases from issuers provide utilization benefits without consumer action or credit inquiries. Many issuers review accounts periodically and grant increases to cardholders showing responsible payment behavior and income growth. These automatic increases reduce utilization instantly upon implementation and carry no downside risks.

The strategy works best when applied to accounts with moderate balances and reasonable existing limits. Requesting increases on maxed accounts with poor payment history frequently results in denial and wasted hard inquiries. Conversely, requesting increases on zero-balance accounts provides minimal benefit since utilization already approaches optimal levels.

Opening New Credit Lines Carefully

Adding new revolving accounts increases total available credit, lowering aggregate utilization across all accounts. A consumer with 5,000 dollars total credit card balances across 15,000 dollars in limits showing 33 percent utilization who opens a new card with 5,000 dollar limit instantly drops to 25 percent aggregate utilization at unchanged balances.

New account opening creates offsetting effects on credit scores that require careful timing consideration. The utilization benefit occurs immediately but competes with score reductions from hard inquiries and decreased average account age. Consumers typically experience net score decreases of 10 to 30 points initially, followed by recovery and potential improvement as the account ages and utilization benefits compound.

This approach proves most effective for consumers with utilization problems but otherwise strong credit profiles. Opening new accounts when credit scores already suffer from late payments or other derogatory marks often results in denial or low credit limits that provide minimal utilization benefit. The strategy works best for those with good payment history seeking to expand total credit capacity.

Maintaining zero or very low balances on new accounts maximizes their utilization benefit. The added credit limit reduces aggregate utilization even when the new card carries no balance, while keeping the new account at low utilization prevents creating new high per-card utilization problems. Using new cards lightly for occasional purchases with immediate payoff demonstrates account activity without sacrificing utilization advantages.

Balance Transfer and Debt Consolidation

Balance transfers move existing credit card debt to new accounts offering promotional interest rates, typically zero percent APR for 12 to 21 months. This strategy reduces interest costs while providing time to pay down principal without accumulating new interest charges. However, balance transfers temporarily create high utilization on receiving accounts, potentially offsetting score benefits until balances decrease.

The utilization impact depends on transferred amount relative to new account limits. Transferring 5,000 dollars to a new card with 10,000 dollar limit creates 50 percent utilization on that account, likely reducing scores despite unchanged aggregate balances. Transferring the same balance to a 20,000 dollar limit card maintains 25 percent per-card utilization with better score outcomes.

Balance transfer cards typically charge fees of 3 to 5 percent of transferred amounts, adding immediate costs that must balance against interest savings. A consumer transferring 8,000 dollars at 4 percent fee pays 320 dollars upfront, which remains worthwhile only if interest savings exceed this cost within the promotional period. Failing to eliminate balances before promotional rates expire often results in higher interest costs than the original debt.

Debt consolidation loans convert revolving credit card debt into installment loans with fixed repayment terms. This eliminates credit card utilization entirely by paying off revolving balances, often producing immediate score increases of 50 to 100 points when high utilization resolves. The installment loan appears as a separate credit category that does not calculate into utilization ratios.

Threshold-Based Guidance and Best Practices

Credit utilization impact operates along a continuum rather than discrete thresholds, but certain ranges correlate with meaningfully different credit outcomes. Understanding these utilization zones helps consumers set appropriate targets based on credit goals and financial capacity. The optimal utilization level varies by individual circumstances and timing relative to credit needs.

Industry data and scoring model behaviors suggest that utilization between 1 percent and 10 percent typically maximizes credit scores for most profiles. Utilization from 10 percent to 30 percent maintains healthy scores with modest penalties compared to very low utilization. Utilization above 30 percent triggers progressively larger score reductions, with impacts accelerating above 50 percent and 70 percent thresholds.

Ideal Utilization Ranges

Utilization between 1 percent and 10 percent generally produces optimal credit scores across FICO and VantageScore models. This range demonstrates active credit use without approaching levels that signal financial stress. A consumer with 10,000 dollars total credit limits should aim for balances between 100 dollars and 1,000 dollars reporting to credit bureaus for maximum score benefit.

Zero percent utilization may produce slightly lower scores than very low positive utilization, as some scoring models interpret complete balance absence as indicating inactive credit rather than excellent management. The score difference typically measures 5 to 15 points between zero and 5 percent utilization, though this varies by overall credit profile characteristics.

Utilization from 10 percent to 30 percent represents a safe zone where scores remain strong without requiring extreme balance management. Most consumers find this range achievable through normal credit card use with monthly full payment. The score difference between 10 percent and 25 percent utilization typically ranges from 10 to 25 points, representing modest penalties that may not matter for borrowers without imminent credit needs.

Utilization above 30 percent enters moderate risk territory where score penalties become more substantial. Moving from 30 percent to 50 percent typically reduces scores by 30 to 60 points, while increases from 50 percent to 70 percent trigger additional 40 to 70 point decreases. Utilization above 80 percent signals severe financial stress and creates maximum score damage often exceeding 100 points compared to optimal levels.

Per-Card vs Aggregate Management Strategy

Maintaining balanced per-card utilization across multiple accounts generally produces better credit outcomes than concentrating balances even when aggregate utilization remains identical. A consumer with 3,000 dollars debt across three cards ideally distributes balances proportionally to credit limits rather than maximizing use of one card while leaving others dormant.

Strategic balance distribution requires calculating target balances for each card based on individual limits. A borrower with cards showing limits of 5,000 dollars, 3,000 dollars, and 2,000 dollars totaling 10,000 dollars who wants to maintain 20 percent aggregate utilization with 2,000 dollars total balance should aim for approximately 1,000 dollars, 600 dollars, and 400 dollars respectively on each card to maintain consistent 20 percent per-card ratios.

The per-card strategy becomes most important when managing necessary debt that cannot immediately pay to zero. Consumers carrying revolving balances due to cash flow timing or deliberate low-interest financing should spread balances across available accounts to minimize individual card utilization rather than concentrating debt on preferred or rewards-earning cards.

Exceptions to balance spreading include zero-interest promotional periods and rewards optimization. Consumers with specific cards offering zero percent APR may rationally concentrate debt on promotional accounts while maintaining low utilization on others, accepting temporary per-card utilization penalties in exchange for interest savings. Similarly, those maximizing rewards might use high-reward cards more heavily when score impacts are acceptable.

When to Apply vs When to Wait

Consumers planning major credit applications such as mortgages or auto loans within three to six months should prioritize utilization reduction to maximize scores at application time. Reducing utilization from 40 percent to 10 percent approximately 60 days before applying allows score improvements to reflect in credit reports when lenders pull scores, potentially improving loan terms significantly.

The optimal waiting period varies by how quickly balances can decrease and when issuers report to credit bureaus. Consumers who can pay balances down substantially within one billing cycle might wait 45 to 60 days before applying to allow updated utilization to report. Those requiring multiple months to reduce balances should delay applications accordingly to avoid submitting with suboptimal scores.

Unexpected credit opportunities or urgent credit needs sometimes require applying despite high utilization. In these cases, consumers should still attempt rapid balance reduction before application even if full optimization remains incomplete. Reducing utilization from 70 percent to 40 percent within two weeks before applying provides meaningful score benefit despite remaining above ideal levels.

Non-urgent credit applications when utilization is high should generally wait for improvement. Applying for new credit cards or increasing existing limits while showing 60 percent utilization often results in denial or minimal approved limits that provide little benefit. Waiting until utilization falls below 30 percent substantially improves approval odds and initial credit line sizes.

Special Cases: Business Credit, Student Cards, New Profiles

Business credit cards using personal guarantees often report to both business and personal credit bureaus, affecting personal credit utilization. Entrepreneurs should verify reporting practices before using business cards heavily, as balances on cards reporting to personal credit count toward personal utilization ratios. Some business cards report only delinquencies to personal credit, allowing high utilization without personal score impact.

Student credit cards and secured cards typically carry lower credit limits, making utilization management more challenging with modest balances. A student card with 500 dollar limit reaches 30 percent utilization with just 150 dollar balance, requiring careful spending control or strategic payment timing. These cardholders benefit most from limit increase requests and mid-cycle payments to manage restricted capacity.

Consumers with new credit profiles or thin files face amplified utilization sensitivity. Individuals with only one or two credit cards lack diversification that moderates utilization impact, meaning any single balance significantly affects both per-card and aggregate ratios. New credit users should prioritize maintaining very low utilization until building additional credit capacity through account aging and additional account openings.

Authorized users on other people’s credit card accounts inherit those accounts’ utilization in their credit reports. An authorized user on a parent’s card showing 80 percent utilization experiences score damage despite no payment responsibility. Those optimizing credit should request removal from high-utilization authorized user accounts or verify that card issuers report authorized user status separately from primary account holder responsibility.

Credit Utilization and Credit Score Modeling

Credit scoring models incorporate utilization through complex algorithms that evaluate both reported balance levels and utilization patterns over time. The exact utilization impact varies across FICO model versions, VantageScore generations, and individual credit profile characteristics. Understanding how different models treat utilization helps consumers anticipate score effects across various lending contexts.

Lenders select specific scoring models based on loan type, risk tolerance, and institutional preferences. Mortgage lenders commonly use older FICO models such as FICO Score 2, 4, or 5, while credit card issuers might use FICO Score 8 or 9. Auto lenders often employ FICO Auto Scores that weight credit history differently than general-purpose models. These model variations create situations where identical utilization produces different scores depending on which lender pulls credit reports.

FICO Auto Score vs General FICO Models

FICO Auto Score models weight prior auto loan payment history more heavily than general FICO models, but utilization calculations remain fundamentally similar across versions. Both model families treat credit card utilization as a major scoring component representing approximately 30 percent of score calculation. The primary differences emerge in how models weight other credit types rather than utilization mechanics.

Auto lenders using FICO Auto Scores still penalize high credit card utilization despite the model’s focus on auto loan history. A consumer with perfect auto loan payments but 70 percent credit card utilization faces lower FICO Auto Scores than one with identical auto history and 15 percent utilization. The utilization impact may measure slightly less in Auto Score versions compared to FICO Score 8, but the directional effect remains consistent.

Consumers seeking auto financing should still prioritize utilization management despite Auto Score’s emphasis on auto payment history. Reducing credit card utilization from 60 percent to 20 percent typically improves FICO Auto Scores by 40 to 70 points even when auto loan history remains unchanged, potentially affecting loan approval and interest rate offerings.

VantageScore Considerations

VantageScore 3.0 and 4.0 combine utilization with overall credit usage into a single factor category rather than isolating utilization as distinctly as FICO models do. This integration means VantageScore may respond somewhat differently to specific utilization thresholds compared to FICO, though both model families penalize high utilization substantially.

VantageScore models appear more sensitive to very recent credit behavior including current utilization levels, while FICO models balance current utilization with longer-term patterns more heavily. Consumers might observe faster score recovery under VantageScore when reducing utilization quickly, as recent improvements weigh more prominently in score calculation.

The practical differences between FICO and VantageScore utilization treatment typically produce score variations of 20 to 50 points at identical utilization levels depending on other profile characteristics. A consumer with 40 percent utilization might score 680 under FICO Score 8 but 710 under VantageScore 3.0, though exact outcomes vary widely by individual credit history composition.

Lender model preferences determine which scoring variation matters most. Consumers should verify which models their target lenders use, though this information is not always readily available. When model preference is unknown, optimizing utilization benefits scores across all model families since the directional relationship between lower utilization and higher scores remains consistent.

Interaction With Payment History, Length of Credit, and Credit Mix

Credit utilization interacts with other scoring factors through complex model algorithms that consider complete credit profiles holistically. A consumer with perfect payment history extending 15 years experiences less severe score damage from 60 percent utilization than one with recent late payments and short credit history at identical utilization levels. Payment history strength moderates utilization penalties by signaling overall creditworthiness despite current high balances.

Length of credit history similarly affects utilization impact. Established credit users with aged accounts showing long-term responsible management can sustain higher utilization with less score damage than new credit users carrying similar balance ratios. Scoring models interpret high utilization differently when accompanied by decades of successful credit management versus months of limited history.

Credit mix diversity provides additional context for utilization interpretation. Consumers with varied credit types including installment loans, mortgages, and credit cards may experience slightly less utilization sensitivity than those with only revolving accounts. The presence of successfully managed installment debt suggests creditworthiness beyond current credit card utilization levels.

These interaction effects explain why consumers with similar utilization ratios sometimes show different credit scores. A borrower with 50 percent utilization, 20 years credit history, perfect payment record, and diverse credit mix might score 720, while another with identical 50 percent utilization but 3 years history, one recent late payment, and only credit cards scores 620. Utilization impact compounds with or moderates based on complete profile strength.

Scenario Examples: Multiple Numeric Utilization Effects

A consumer with 10,000 dollars total credit limits carrying 500 dollars balance shows 5 percent utilization, typically producing credit scores in the excellent range if other factors are strong. This low utilization demonstrates active credit use without approaching capacity limits, optimizing the utilization component of credit scores.

Increasing balances to 3,000 dollars on the same 10,000 dollar total limit creates 30 percent utilization, generally reducing scores by 15 to 35 points compared to 5 percent utilization. This threshold represents the upper boundary of commonly recommended utilization ranges, where scores remain healthy but begin showing modest penalties for increased balance-to-limit ratios.

Balances of 5,000 dollars against 10,000 dollars limits produce 50 percent utilization and typically reduce scores by 50 to 90 points compared to optimal 5 percent levels. This mid-range utilization signals moderate financial stress to scoring models and lenders, triggering meaningful score penalties that affect credit access and pricing.

Carrying 9,000 dollars balance on 10,000 dollars total limits creates 90 percent utilization, resulting in severe score penalties often measuring 100 to 150 points below optimal utilization scores. This near-maximum utilization indicates maxed-out credit lines and imminent financial crisis to lenders, placing scores in subprime ranges even with otherwise clean credit histories.

Tools and Monitoring for Credit Utilization

Active utilization monitoring enables consumers to track balance-to-limit ratios across accounts and identify optimization opportunities before credit reports update. Various tools and services provide utilization tracking capabilities ranging from simple calculators to automated alert systems that notify users of approaching threshold crossings. Regular monitoring prevents unintended utilization spikes from large purchases or statement timing issues.

Effective utilization management requires understanding current ratios, projected changes from planned spending, and timing of bureau reporting cycles. Manual calculation provides baseline awareness, while automated monitoring tools offer real-time tracking that adjusts as transactions post to accounts.

Credit Monitoring Services

Credit monitoring services from providers such as Experian, Equifax, and TransUnion offer utilization tracking as part of broader credit report monitoring packages. These services display current credit card balances, credit limits, and calculated utilization ratios alongside credit scores and report contents. Many provide historical utilization tracking showing how ratios change over months or years.

Free credit monitoring through credit card issuers and financial institutions has become widely available. Services such as Capital One CreditWise, Chase Credit Journey, and Discover Credit Scorecard provide complimentary access to credit scores, utilization information, and basic monitoring features without requiring paid subscriptions. These services typically update monthly as new credit report information arrives.

Paid monitoring services often include additional features such as three-bureau monitoring, daily credit report updates, and identity theft protection alongside utilization tracking. Premium services from myFICO provide access to multiple FICO score versions and detailed score factors explaining current utilization impact. The value of paid services depends on whether consumers need comprehensive monitoring beyond free alternatives.

Monitoring services cannot predict future utilization changes from pending transactions. These tools display only posted balances that have cleared through payment networks, meaning recent purchases made but not yet posted remain invisible until processing completes. Consumers should supplement monitoring services with direct account tracking for most accurate current utilization estimates.

Calculators and Apps

Standalone utilization calculators available through financial education websites allow manual entry of credit card balances and limits to compute per-card and aggregate utilization ratios. These simple tools help consumers understand current position and model the impact of potential balance reduction or limit increase scenarios without affecting credit.

Budgeting and personal finance apps such as Mint, YNAB, and Personal Capital often incorporate credit utilization tracking alongside expense management and account aggregation features. These integrated tools display utilization within broader financial dashboards, connecting spending patterns directly to credit utilization outcomes.

Credit card issuer mobile apps increasingly show real-time utilization calculations for individual accounts as transactions post. These in-app displays update continuously rather than monthly, helping cardholders track approaching utilization thresholds before statement closing dates. Some issuers provide spending alerts or warnings when balances approach preset utilization targets.

Manual spreadsheet tracking provides maximum customization for consumers managing complex credit situations across multiple cards with varying limits and statement dates. Spreadsheets enable scenario modeling such as testing how different payment allocations affect overall utilization or projecting future ratios based on planned spending patterns.

Alerts for Risk and Opportunity

Automated alerts through credit monitoring services can notify consumers when utilization crosses specific thresholds such as 30 percent, 50 percent, or custom levels. These proactive warnings enable immediate response through accelerated payments or spending adjustments before high utilization reports to credit bureaus and affects scores.

Credit limit increase notifications from card issuers represent opportunities for automatic utilization reduction without balance changes. Accepting issuer-initiated limit increases instantly lowers utilization ratios, often improving credit scores within one to two billing cycles as updated limits report to bureaus.

Statement closing date reminders help consumers time payments strategically to minimize reported utilization. Setting calendar alerts three to five days before each card’s statement closing date creates windows for pre-statement payments that reduce reported balances without requiring balance elimination.

Balance approaching credit limit warnings from issuers prevent over-limit situations that trigger fees and severe utilization penalties. These real-time alerts allow consumers to pause spending or make immediate payments before transactions push balances above credit limits.

Does per-card utilization matter more than overall utilization?

Both per-card and aggregate utilization affect credit scores through independent evaluation pathways in most scoring models. High utilization on any single card can reduce scores significantly even when overall utilization across all accounts remains low. A consumer with 10 percent aggregate utilization but one card at 90 percent utilization typically experiences score penalties from the maxed-out account despite favorable overall ratio. Optimal credit management maintains both low aggregate utilization below 30 percent and individual card utilization below similar thresholds across all accounts.

Can zero percent utilization hurt my credit score?

Complete zero percent utilization may produce slightly lower credit scores than very low positive utilization such as 1 to 5 percent in some scoring models. Scoring algorithms can interpret complete absence of revolving balances as indicating inactive credit rather than excellent credit management. The score difference between zero and low single-digit utilization typically measures 5 to 15 points, representing a modest penalty that matters minimally for most consumers. Maintaining occasional small balances that pay in full monthly demonstrates active credit use while preserving very low utilization ratios.

How quickly do utilization changes affect my credit score?

Utilization changes typically reflect in credit scores within one to two billing cycles after credit card issuers report updated balances to credit bureaus. Most issuers report monthly around statement closing dates, meaning balance reductions made after statement close appear in credit reports approximately 30 to 45 days later. Consumers seeking immediate score improvement for pending credit applications should reduce balances at least 45 to 60 days before applying to ensure updated utilization reflects in lender credit pulls.

Does business credit card utilization affect personal credit scores?

Business credit cards affect personal credit scores only when issuers report account information to personal credit bureaus. Some business cards report balances and payment history to both business and personal credit bureaus, making utilization count toward personal credit ratios. Others report only delinquencies or payment defaults to personal credit, allowing high utilization without personal score impact. Cardholders should verify reporting practices with issuers before using business cards heavily if maintaining personal credit scores is important.

What utilization level triggers credit card limit decreases?

Credit card issuers may decrease credit limits when accounts consistently show very high utilization above 80 to 90 percent, particularly when combined with other risk indicators such as late payments on other accounts or overall credit score declines. No universal utilization threshold triggers automatic limit decreases across all issuers, as each institution applies proprietary risk management criteria. Maintaining utilization below 50 percent on all accounts generally minimizes limit decrease risk, while sustained utilization above 70 percent increases probability of adverse credit line actions.

Final Note: Credit utilization represents one of the most controllable credit score factors because it responds immediately to balance changes unlike payment history or credit age that reflect past behavior over extended periods. Consumers can improve utilization within days through strategic payments or limit increases, making this factor particularly valuable for those seeking rapid score improvements. Understanding the complete mechanism including reporting timing, per-card effects, and scoring model variations enables more effective credit management aligned with individual financial circumstances and credit goals.