Table of Contents

Contents are generated from article headings.

Retiring in Antigua and Barbuda is financially feasible for retirees with stable foreign income, especially those seeking a low-tax Caribbean lifestyle. As of 2025, retirees are not required to pay tax on worldwide income if they avoid triggering tax residency status, and the country does not impose capital gains or inheritance taxes. However, retirement in Antigua and Barbuda depends on understanding residency rules, healthcare limitations, housing costs, and long-term insurance and import expenses. While the country offers a warm climate, English-speaking environment, and a stable USD-pegged currency, it is best suited for retirees who can afford private healthcare, manage hurricane risk, and plan income independently rather than rely on public pension systems.

Jurisdiction Scope: This analysis applies specifically to Antigua and Barbuda, a sovereign Caribbean nation. Retirement rules vary by nationality, residency status, tax residency classification, and international income source. This content does not assume US or EU-only frameworks and addresses retirement planning from a multi-jurisdictional perspective.

Temporal Validity: All information reflects conditions as of 2025. Areas prone to change include residency permit thresholds, Citizenship by Investment program requirements, tax treaties, healthcare costs, and insurance availability. Retirees should verify current regulations with Antigua and Barbuda’s Department of Immigration and Inland Revenue Department before making final decisions.

1. What Does “Retiring in Antigua and Barbuda” Legally Mean?

Retiring in Antigua and Barbuda refers to establishing long-term residence in the country while living primarily on foreign income, pensions, or investment returns rather than local employment. Unlike jurisdictions with formal retirement visa categories, Antigua and Barbuda does not offer a designated “retirement visa” program. Instead, retirees must navigate the country’s existing residency framework, which distinguishes between temporary visitor status, formal residency permits, and citizenship. Understanding these legal categories determines whether a retiree can stay long-term, access services, open bank accounts, and plan finances reliably.

Difference Between Tourist Stay, Residency, and Retirement Living

Tourist visa status allows visitors to stay in Antigua and Barbuda for up to six months without applying for formal residency. Many retirees initially use this visa-free or visa-on-arrival period to evaluate the country before committing to permanent relocation. However, tourist status does not permit legal residence beyond six months, and attempting to extend stay indefinitely through repeated exits and re-entries creates immigration complications and does not establish legal residency for tax or banking purposes.

Formal residency in Antigua and Barbuda requires applying for a residency permit through the Department of Immigration. This permit grants legal long-term stay and must be renewed annually at a cost of approximately $250. Residency permit holders can open local bank accounts, sign long-term rental agreements, and establish stable financial operations, but residency alone does not confer citizenship or voting rights.

Retirement living in Antigua and Barbuda typically means maintaining residency status while living on income generated outside the country. Since Antigua and Barbuda does not define “retiree” as a legal immigration category, individuals retiring to the island follow the same residency application process as other non-working foreign nationals. The key distinction is income source—retirees demonstrate financial self-sufficiency through pensions, investment income, or savings rather than local employment.

Who Is Considered a Retiree Under Antigua and Barbuda Law

Antigua and Barbuda law does not classify individuals as “retirees” based on age or employment history. Instead, retirement status is determined functionally by income structure and residency purpose. Retirees are foreign nationals who reside in Antigua and Barbuda without working locally and who support themselves through foreign pensions, Social Security payments, investment dividends, rental income from abroad, or accumulated savings.

This income-based reality means that younger individuals living on passive income or early retirees can legally reside in Antigua and Barbuda under the same framework as traditional retirees aged 65 and older. The absence of age-based restrictions provides flexibility but also means retirees must clearly demonstrate financial independence when applying for residency permits.

Common Misconceptions About Retiring in Antigua and Barbuda

One widespread misconception is that Antigua and Barbuda is a “no tax” jurisdiction for all retirees. While the country does not impose income tax on non-residents and offers favorable treatment for certain foreign income, retirees who spend 183 days or more in Antigua and Barbuda in a calendar year may trigger tax residency status. Tax residents are subject to different reporting requirements and potential taxation on worldwide income, though foreign pension income generally remains exempt under current policy. The “no tax” claim oversimplifies a more nuanced tax structure that depends on residency duration and income type.

Another common misunderstanding is that purchasing real estate in Antigua and Barbuda automatically grants residency or citizenship. Property ownership does not confer legal residency unless the purchase qualifies under the Citizenship by Investment program, which requires minimum investment thresholds of $200,000 in approved real estate projects. Retirees who buy property outside the CBI framework must still apply separately for residency permits and meet standard requirements.

Finally, many retirees assume citizenship is required to retire in Antigua and Barbuda. Citizenship is not necessary for long-term retirement living. Retirees can maintain permanent residency status indefinitely through annual permit renewals without pursuing citizenship, which involves separate legal processes, higher costs, and additional documentation.

2. How Residency Works for Retirees in Antigua and Barbuda

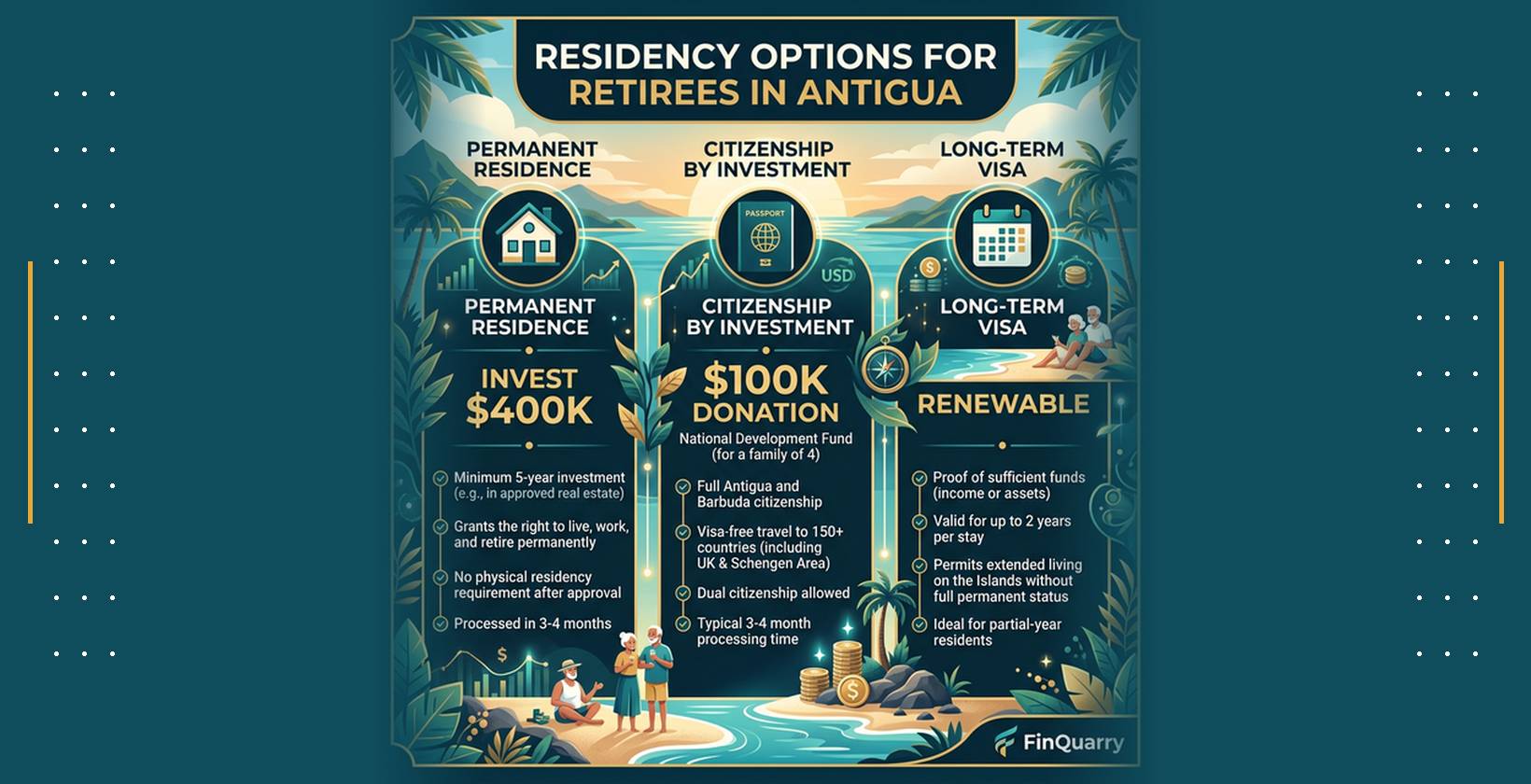

Residency in Antigua and Barbuda determines a retiree’s legal right to stay long-term, access services, and establish financial accounts. The country offers multiple pathways for retirees to achieve legal residency, ranging from annual visitor extensions to formal permanent residency permits and the Citizenship by Investment program. Each pathway carries different costs, documentation requirements, and long-term implications. Understanding these options allows retirees to choose the most appropriate legal status based on budget, length of intended stay, and estate planning needs.

Long-Stay Options Without Permanent Residency

Retirees who wish to test retirement in Antigua and Barbuda before committing to permanent residency can use the six-month visitor visa, which is granted on arrival to citizens of the United States, Canada, the United Kingdom, and most European Union countries. This visa allows initial stay without formal residency applications, providing time to evaluate housing, healthcare access, and lifestyle compatibility.

After the initial six-month period, retirees can apply for visa extensions through the Department of Immigration. Extensions are typically granted in three-month increments and require proof of financial self-sufficiency, such as bank statements showing adequate funds to support living expenses. While extensions allow prolonged stay, they do not establish formal residency status and must be renewed repeatedly, creating administrative burden and uncertainty.

Practical limitations of long-stay visitor status include difficulty opening local bank accounts, challenges signing long-term rental agreements, and inability to establish stable utility contracts under visitor classification. Repeated extensions also create immigration record complications that may affect future residency or citizenship applications. For retirees planning to stay beyond one year, formal residency permits provide greater stability and legal clarity.

Permanent Residency Pathways for Retirees

Permanent residency in Antigua and Barbuda is granted through application to the Department of Immigration and requires demonstrating financial self-sufficiency, clean criminal background, and intent to reside long-term without local employment. Retirees must submit financial documentation proving monthly income or savings sufficient to support living expenses without relying on public assistance or local employment. While specific income thresholds are not publicly codified, immigration officials generally expect retirees to demonstrate income equivalent to $2,500 to $3,000 per month minimum.

The residency permit application process requires submitting a completed application form, passport copies, police clearance certificates from countries of residence for the past five years, medical examination results, and proof of financial means. Processing time typically ranges from three to six months, and applicants may be required to attend an interview with immigration officials. Initial residency permits are valid for one year and must be renewed annually at a cost of approximately $250 per person.

Renewal obligations for permanent residency require maintaining legal presence in Antigua and Barbuda and demonstrating continued financial self-sufficiency. Retirees must avoid criminal convictions and ensure they do not become public charges. Long-term residency holders who maintain compliance for several years may eventually qualify for indefinite residency status, which reduces renewal frequency, though this remains at the discretion of immigration authorities.

Citizenship by Investment Program (CBI) and Retirement

The Antigua and Barbuda Citizenship by Investment program offers an accelerated pathway to citizenship for retirees willing to make substantial financial commitments. The CBI program requires a minimum investment of $100,000 as a non-refundable contribution to the National Development Fund, $200,000 in approved real estate projects, or $1.5 million in an approved business venture. Citizenship grants full rights including passport access, voting privileges, and elimination of residency permit renewal requirements.

CBI makes sense for retirees who value travel mobility, as the Antigua and Barbuda passport provides visa-free access to over 150 countries including the United Kingdom, Schengen Area countries, and Hong Kong. Retirees with significant assets who prioritize estate planning, second passport diversification, or multi-generational citizenship may find CBI worthwhile despite higher upfront costs.

However, CBI does not make financial sense for most retirees focused solely on residence and living costs. The program’s minimum $100,000 contribution far exceeds the cost of obtaining and maintaining residency permits, which total approximately $250 annually. Retirees who do not require citizenship benefits or enhanced travel privileges achieve legal residence more economically through standard residency permits. The distinction between retirement planning and wealth preservation planning is critical—CBI serves investment and estate planning goals, not cost-efficient retirement residence.

3. Cost of Living for Retirees in Antigua and Barbuda

Cost of living in Antigua and Barbuda determines retirement affordability and financial sustainability over time. The country’s island economy depends heavily on imported goods, which increases prices for food, household items, and consumer products compared to larger markets. While housing costs vary by location and property type, retirees must account for elevated utility expenses, mandatory insurance premiums, and import-related price volatility. Understanding realistic monthly budgets across different lifestyle tiers helps retirees assess whether Antigua and Barbuda aligns with their financial capacity.

Monthly Retirement Budget Breakdown (Low / Moderate / Comfortable)

A low-budget retirement in Antigua and Barbuda requires approximately $2,500 to $3,000 per month for a single retiree or $3,500 to $4,000 for a couple. This budget assumes modest rental housing in less central areas, limited dining out, basic private health insurance, and minimal discretionary spending. Housing in this tier typically means renting a one-bedroom apartment outside tourist zones for $800 to $1,200 monthly. Utilities including electricity, water, and internet add $300 to $400 monthly, with electricity costs particularly high due to air conditioning needs in tropical climates. Groceries for basic imported and local foods cost $400 to $600 monthly, while transportation using local buses or occasional taxis runs $100 to $150. Basic private health insurance for retirees under age 65 starts at $250 to $350 monthly, though premiums increase significantly for older retirees and those with pre-existing conditions.

A moderate retirement budget ranges from $4,000 to $5,500 monthly, providing more comfortable housing, regular restaurant meals, comprehensive health coverage, and greater lifestyle flexibility. Housing at this level includes two-bedroom apartments or small houses in safer, more convenient locations for $1,500 to $2,200 monthly. Utilities remain substantial at $400 to $600 due to increased space and cooling needs. Groceries and dining expenses rise to $800 to $1,000 monthly with more imported products and weekly restaurant visits. Comprehensive private health insurance with lower deductibles and broader coverage costs $400 to $600 monthly for retirees aged 55 to 65. Transportation expands to include a used vehicle, adding fuel, maintenance, and insurance costs totaling $300 to $400 monthly. Discretionary spending for entertainment, travel, and hobbies adds another $400 to $600.

A comfortable retirement budget requires $6,000 to $8,000 monthly or more, allowing premium housing, extensive dining and entertainment, comprehensive insurance, and financial cushion for unexpected expenses. Housing in desirable beachfront or hillside locations costs $2,500 to $4,000 monthly for well-maintained properties with ocean views and modern amenities. Utilities in larger homes with multiple air conditioning units reach $600 to $900 monthly. Food and dining expenses approach $1,200 to $1,800 with regular imported specialty products and frequent restaurant meals. Premium health insurance with international coverage and medical evacuation benefits costs $700 to $1,200 monthly for retirees over 65. Vehicle ownership at this level includes newer, more reliable cars with insurance and maintenance totaling $500 to $700 monthly. Household help, property maintenance, and lifestyle activities add $800 to $1,500.

Cost Differences by Location Within Antigua

Housing and living costs vary significantly between St. John’s, the capital and commercial center, coastal tourist areas, and rural or inland regions. St. John’s offers greater access to services, shopping, and healthcare facilities but commands premium rental prices. One-bedroom apartments in central St. John’s rent for $1,000 to $1,500 monthly, while two-bedroom units range from $1,800 to $2,500. Coastal areas popular with tourists and expatriates, including English Harbour, Jolly Harbour, and areas near major resorts, feature higher housing costs with one-bedroom rentals starting at $1,200 and two-bedroom properties reaching $2,000 to $3,000 monthly.

Rural and inland areas offer lower housing costs, with one-bedroom rentals available for $600 to $900 and two-bedroom houses for $1,000 to $1,500. However, these locations require vehicle ownership for accessing services, medical care, and shopping, which offsets some housing savings. Infrastructure quality declines outside main population centers, with more frequent power outages, slower internet speeds, and limited public services. Retirees prioritizing budget savings may find rural living viable if they accept reduced convenience and plan for transportation costs.

Hidden and Overlooked Retirement Costs

Import duties on household goods create significant unexpected expenses for retirees relocating with personal belongings. Antigua and Barbuda imposes import duties ranging from 15% to 20% on most household items, furniture, electronics, and personal effects brought into the country. Retirees shipping a container of belongings should budget $3,000 to $6,000 for duties, freight, and clearance fees beyond initial shipping costs. This expense is often underestimated and can strain relocation budgets.

Electricity costs in Antigua and Barbuda run substantially higher than North American or European averages due to island power generation relying on imported diesel fuel. Residential electricity rates range from $0.35 to $0.45 per kilowatt-hour, approximately three times the average US rate. Retirees living in tropical climates typically depend on air conditioning for comfort and health, driving monthly electricity bills to $200 to $600 for modest homes and $600 to $1,000 for larger properties. Water costs also exceed mainland standards, adding $50 to $150 monthly depending on usage and whether properties rely on municipal supply or private cisterns.

Insurance premiums for property, health, and vehicles increase for island residents due to hurricane exposure and limited local service infrastructure. Hurricane insurance is mandatory for mortgaged properties and costs 2% to 4% of property value annually. A home valued at $300,000 incurs $6,000 to $12,000 in annual hurricane insurance alone. Health insurance premiums for retirees age 65 and older often exceed $800 to $1,200 monthly for comprehensive coverage, with many policies excluding pre-existing conditions or requiring lengthy waiting periods. Vehicle insurance costs 30% to 50% more than comparable mainland rates due to higher repair costs and limited competition among insurers.

4. How Taxes Affect Retirees in Antigua and Barbuda

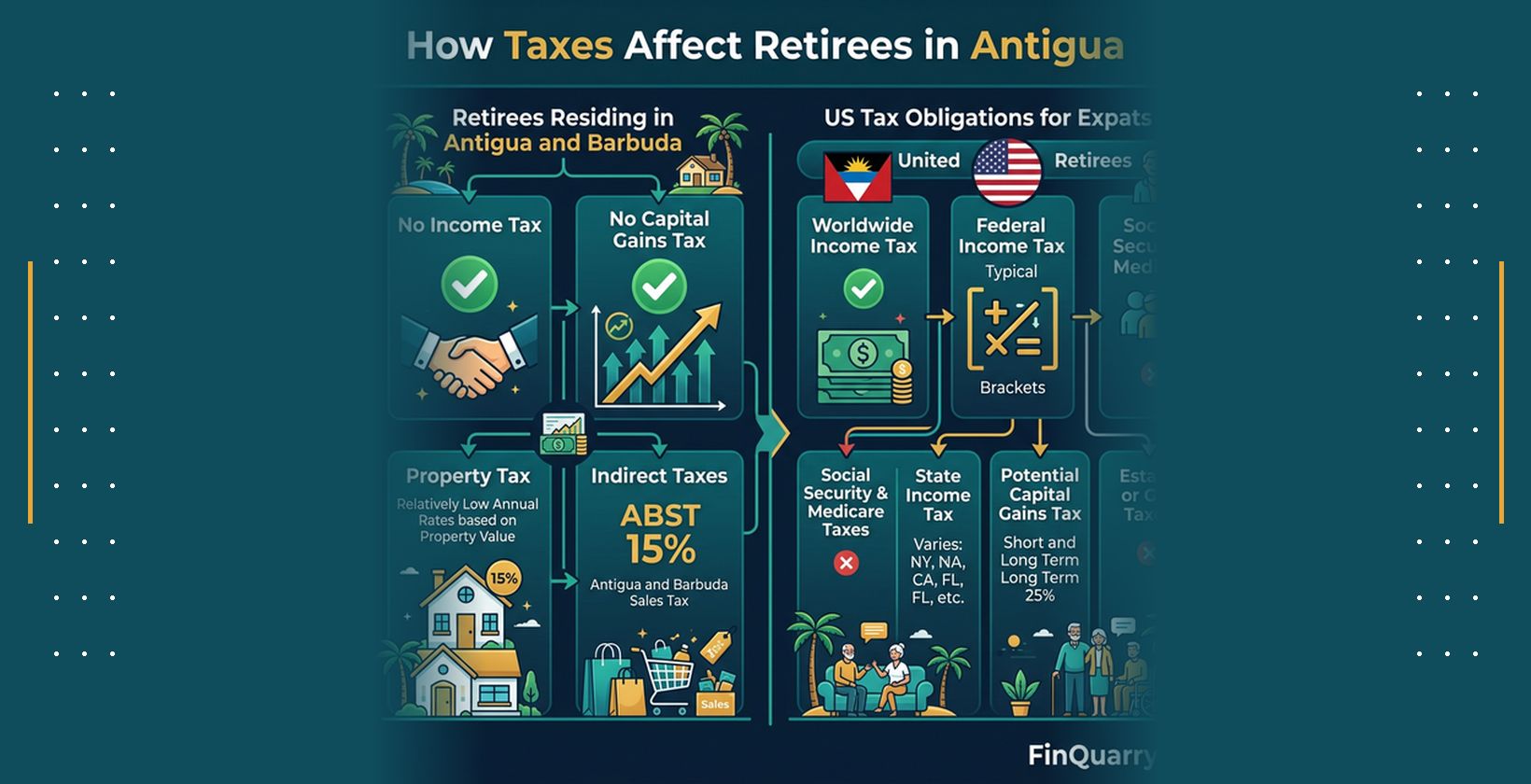

Taxation in Antigua and Barbuda influences retirement planning through residency-based rules that determine whether retirees owe taxes on foreign income, pensions, and investments. The country does not impose personal income tax on non-residents, and even tax residents benefit from exemptions on certain foreign income sources. However, retirees must understand tax residency thresholds, reporting requirements, and how their home country’s tax obligations interact with Antigua and Barbuda’s system. Proper tax planning prevents unexpected liabilities and ensures retirees maximize available exemptions.

Tax Residency Rules and Why They Matter

Tax residency in Antigua and Barbuda is determined primarily by physical presence rather than citizenship or residency permit status. Individuals who spend 183 days or more in Antigua and Barbuda during a calendar year are generally considered tax residents and become subject to the country’s tax filing and reporting requirements. This threshold applies cumulatively across the year, meaning retirees who spend six months and one day or longer trigger tax residency regardless of how that time is distributed.

Tax residency matters because it determines whether retirees must report worldwide income to Antigua and Barbuda tax authorities and whether certain income sources become taxable. However, Antigua and Barbuda’s tax system offers substantial exemptions even for tax residents, particularly regarding foreign pension income and Social Security payments. Retirees who remain below the 183-day threshold each year generally face no Antigua and Barbuda tax obligations, though they must still fulfill tax requirements in their country of citizenship or primary tax residence.

Practical enforcement of tax residency rules in Antigua and Barbuda remains relatively lenient compared to jurisdictions with sophisticated tax monitoring systems. The country lacks comprehensive entry-exit tracking systems that automatically calculate presence days, and enforcement focuses primarily on individuals who establish obvious permanent residence through property ownership, business activities, or long-term rental agreements. Retirees maintaining formal residency permits should assume tax authorities will count them as tax residents and plan accordingly.

Treatment of Foreign Income, Pensions, and Investments

Foreign pension income received by retirees living in Antigua and Barbuda is generally exempt from Antigua and Barbuda income tax, regardless of tax residency status. This exemption applies to government pensions such as US Social Security, UK State Pension, and Canadian Pension Plan benefits, as well as private employer pensions and individual retirement account distributions. The exemption creates significant tax advantages for retirees whose primary income consists of pension payments, as they avoid both source country taxation in many cases and host country taxation in Antigua and Barbuda.

Investment income including dividends from foreign stocks, interest from foreign bank accounts, and rental income from properties located outside Antigua and Barbuda receives varied treatment depending on tax residency status. Non-tax residents pay no Antigua and Barbuda tax on foreign investment income. Tax residents may technically owe tax on worldwide investment income, though in practice enforcement is minimal and many tax residents report only locally-sourced income. Retirees with substantial investment portfolios should consult cross-border tax advisors to determine actual reporting obligations and potential treaty benefits.

Capital gains from selling stocks, bonds, real estate, or other investments remain completely exempt from Antigua and Barbuda taxation regardless of residency status. The country imposes no capital gains tax on any asset class, making it attractive for retirees who plan to liquidate investment positions during retirement. However, retirees must still consider capital gains tax obligations in their country of citizenship, as most countries tax their citizens on worldwide capital gains regardless of residence location.

Taxes That Do NOT Apply (With Context)

Antigua and Barbuda does not impose wealth taxes, net worth taxes, or annual asset reporting requirements on individuals. Retirees can hold substantial savings, investment portfolios, and property without facing taxes based solely on asset ownership. This absence of wealth taxation benefits retirees with significant accumulated assets who generate modest annual income.

Inheritance and estate taxes do not exist in Antigua and Barbuda, allowing retirees to transfer assets to heirs without local tax consequences. This benefit applies to both movable assets like financial accounts and immovable property located in Antigua and Barbuda. However, retirees must consider estate and inheritance tax obligations in their country of citizenship, as many countries tax estates of their citizens regardless of asset location.

One important limitation to Antigua and Barbuda’s favorable tax treatment involves property transfer taxes and stamp duties. While capital gains on property sales are exempt, buyers pay stamp duty ranging from 2.5% to 7.5% of property value depending on purchase price, and sellers may face property transfer taxes. These transaction costs effectively function as indirect taxation on real estate activities, though they apply only at the point of sale rather than annually.

5. Healthcare Access and Medical Costs for Retirees

Healthcare availability in Antigua and Barbuda determines whether retirees can safely age in place or face medical limitations requiring relocation or evacuation. The country operates a two-tier system with public facilities serving basic needs and private clinics handling routine care for those who can afford out-of-pocket costs or private insurance. However, the island lacks specialized geriatric services, advanced surgical facilities, and intensive care capacity necessary for serious health events common among older adults. Understanding these limitations and planning for medical evacuation scenarios is essential for retiree health security.

Public Healthcare System: Capabilities and Limits

The public healthcare system in Antigua and Barbuda centers on Mount St. John’s Medical Centre, the country’s main government hospital located near St. John’s. This facility handles emergency care, basic surgery, maternity services, and general medical treatment for residents and visitors. Public healthcare is available to retirees holding residency permits, though non-emergency services often involve long wait times and limited appointment availability.

Mount St. John’s Medical Centre provides adequate care for common health issues including minor injuries, infections, routine diagnostic testing, and stabilization of emergency cases. However, the facility faces significant limitations affecting retiree healthcare needs. Specialized departments for cardiology, oncology, neurology, and orthopedics operate with limited equipment and specialist availability. Complex diagnostic procedures including advanced imaging beyond basic X-rays and ultrasounds often require off-island referral. The hospital’s intensive care unit has restricted capacity and cannot handle severe cases requiring prolonged critical care support.

Chronic disease management presents particular challenges in the public system. Retirees with conditions such as diabetes, hypertension, heart disease, or chronic respiratory conditions can access basic monitoring and medication management, but advanced treatments, specialist consultations, and comprehensive disease management programs are limited. The public system generally lacks geriatric specialists trained in age-specific health concerns, and services specifically designed for elderly patients remain underdeveloped.

Private Healthcare and Insurance Requirements

Private healthcare in Antigua and Barbuda operates through small clinics staffed by general practitioners and a limited number of specialists. Adelin Medical Centre, the most established private facility, offers outpatient services, routine diagnostic testing, and specialist consultations in fields including internal medicine, general surgery, and obstetrics. Private clinics provide faster access, more personalized care, and better appointment availability than public facilities, but costs are substantially higher and most services require upfront payment or valid private insurance.

Private health insurance becomes practically mandatory for retirees planning extended residence in Antigua and Barbuda, as medical costs paid out-of-pocket quickly become unsustainable. International health insurance plans designed for expatriates typically cost $400 to $600 monthly for retirees aged 55 to 65 with no major pre-existing conditions. Premiums increase sharply after age 65, often reaching $800 to $1,200 monthly, and many insurers either exclude coverage for pre-existing conditions or impose 12 to 24-month waiting periods before covering related treatments.

Retirees must specifically verify that private insurance policies include medical evacuation coverage, as standard expatriate health plans frequently exclude or limit evacuation benefits. Medical evacuation insurance covering air ambulance transport to Miami, Puerto Rico, or Barbados costs an additional $200 to $400 annually when purchased as a standalone policy, though some comprehensive international health plans include evacuation coverage in higher-tier options. Without evacuation coverage, retirees facing serious medical emergencies must pay $25,000 to $50,000 out-of-pocket for air ambulance services.

Medical Evacuation and Regional Healthcare Planning

Medical evacuation becomes necessary when health conditions exceed local treatment capabilities, which occurs frequently for serious cardiac events, strokes, cancer diagnosis and treatment, major orthopedic injuries, and conditions requiring intensive care beyond basic stabilization. The nearest advanced medical facilities capable of tertiary care are located in San Juan, Puerto Rico (approximately 300 miles), Miami, Florida (approximately 1,300 miles), and Bridgetown, Barbados (approximately 300 miles).

Air ambulance evacuation involves coordinating with specialized medical transport companies, obtaining clearance from receiving hospitals, and arranging ground transportation at the destination. The process typically takes 6 to 24 hours from initial request to departure, depending on weather conditions, aircraft availability, and medical team assembly. Costs for medical evacuation vary by destination and patient condition, with San Juan evacuations typically costing $20,000 to $35,000, Miami evacuations ranging from $35,000 to $50,000, and Barbados evacuations falling between $15,000 and $25,000.

Retirees with chronic conditions requiring specialist care, those with history of cardiac disease, cancer survivors needing ongoing monitoring, and individuals over age 75 face higher probability of requiring medical evacuation during Antigua and Barbuda residence. These retirees should factor evacuation costs and insurance coverage into retirement budgets and ensure family members or designated contacts understand evacuation procedures and have access to necessary financial resources. Medical evacuation insurance that covers transport costs and coordinates logistics provides essential risk mitigation for retirees aging in environments with limited medical infrastructure.

6. Housing and Real Estate Considerations for Retirees

Housing in Antigua and Barbuda shapes both retirement budgets and long-term financial security. Retirees face decisions between renting for flexibility and buying for stability, each carrying distinct advantages, risks, and cost structures. Property ownership involves additional considerations including foreign buyer licensing requirements, ongoing maintenance expenses elevated by tropical climate conditions, and hurricane-related insurance obligations. Understanding these housing dynamics helps retirees make informed decisions aligned with their financial capacity and retirement timeline.

Renting vs Buying for Retirement

Renting provides flexibility for retirees uncertain about long-term commitment to Antigua and Barbuda or those who prefer preserving capital for other uses. Monthly rental costs range from $800 to $1,200 for modest one-bedroom apartments in non-tourist areas, $1,500 to $2,500 for comfortable two-bedroom homes in convenient locations, and $2,500 to $4,500 for premium properties in desirable coastal or hillside settings. Rental agreements typically require first and last month’s rent plus security deposit equivalent to one month’s rent, creating initial outlays of three times monthly rent.

Renting eliminates property maintenance responsibilities, hurricane insurance costs, and property tax obligations, shifting these expenses to landlords. Renters avoid capital lock-in and can relocate easily if health needs, family situations, or financial circumstances change. However, rental costs represent pure expense with no equity accumulation, and lease renewals expose retirees to rent increases that can erode fixed income budgets over time. Long-term renters also face periodic relocation stress when landlords choose not to renew leases or sell properties.

Buying property offers stability, equity building, and protection against rental market volatility but requires substantial capital commitment and ongoing expenses. Entry-level homes and condominiums start at $150,000 to $200,000 for modest properties in less central locations. Mid-range properties in safe, convenient areas cost $250,000 to $400,000, while premium beachfront or hillside homes range from $500,000 to $1,500,000 or more. Property ownership requires paying annual property taxes of approximately 0.2% to 0.5% of assessed value, mandatory hurricane insurance costing 2% to 4% of property value annually, and ongoing maintenance that runs 20% to 30% higher than comparable properties in temperate climates due to tropical weather effects on building materials.

Property Ownership Rules for Foreign Retirees

Foreign nationals purchasing property in Antigua and Barbuda must obtain an Alien Land Holding License from the government before completing real estate transactions. This license serves as authorization for non-citizens to own land and property in the country and applies to all foreign buyers regardless of residency status or purchase value. The licensing requirement protects local property markets while generating government revenue from foreign real estate investment.

The Alien Land Holding License application requires submitting property purchase agreements, proof of funds, passport copies, and application fees. Processing typically takes 8 to 12 weeks, and approval is generally granted for legitimate property purchases by financially qualified buyers. License fees operate on a sliding scale based on property value, starting at approximately $15,000 for properties valued under $400,000 and increasing to $25,000 or more for higher-value purchases. These fees represent one-time costs paid at purchase but constitute significant expenses beyond property price and standard closing costs.

Additional property purchase expenses include legal fees for attorneys who handle title searches and transaction documentation, typically 2% to 3% of purchase price, plus stamp duty charged at rates from 2.5% to 7.5% of property value depending on price tier. Total transaction costs for foreign buyers frequently reach 15% to 20% of property purchase price when combining license fees, legal costs, stamp duties, and inspection expenses. Retirees must factor these substantial upfront costs into property purchase budgets and understand they reduce effective return on real estate investments.

Long-Term Housing Risks Retirees Should Understand

Property maintenance costs in Antigua and Barbuda’s tropical climate exceed temperate region standards due to accelerated deterioration of building materials, increased pest control needs, and frequent repair requirements. Constant high humidity promotes mold growth, corrodes metal fixtures, and degrades paint and wood surfaces faster than drier climates. Salt air in coastal areas accelerates corrosion of metal roofing, window frames, and outdoor fixtures. Annual maintenance budgets for property owners typically run $5,000 to $12,000 depending on property size and condition, with major repairs for roof replacement, pest damage remediation, or storm damage adding $10,000 to $30,000 every 5 to 10 years.

Hurricane exposure represents the most significant housing risk for retirees in Antigua and Barbuda. The island lies within the Atlantic hurricane belt, experiencing peak storm risk from June through November each year. While direct hurricane strikes remain relatively infrequent, tropical storms and near-miss hurricanes create property damage through high winds, heavy rainfall, and flooding. Hurricane insurance is mandatory for mortgaged properties and strongly advisable for all property owners, but coverage comes with high deductibles often set at 2% to 5% of insured value and exclusions for certain damage types including flood damage requiring separate policies.

Insurance availability fluctuates based on recent hurricane activity, with insurers restricting new policy issuance or dramatically increasing premiums following major regional storm events. Retirees who purchase property during calm periods may find insurance costs doubling or coverage becoming unavailable entirely after major hurricanes affect the region. Property values in hurricane-prone Caribbean locations also experience higher volatility than mainland markets, with prices declining sharply after storms and recovering slowly as reconstruction progresses and insurance markets stabilize. Retirees viewing property as primary wealth storage or expecting stable appreciation should account for hurricane-related value volatility in long-term financial planning.

7. Lifestyle, Infrastructure, and Daily Living for Retirees

Daily life quality in Antigua and Barbuda depends on infrastructure reliability, transportation accessibility, and social integration opportunities that shape retiree satisfaction beyond financial considerations. The island’s small size limits amenities and services compared to larger countries, while tropical climate and island geography create unique lifestyle patterns. Understanding these practical realities helps retirees set realistic expectations and determine whether Antigua and Barbuda’s lifestyle matches their preferences.

Climate, Utilities, and Infrastructure Reliability

Antigua and Barbuda features tropical maritime climate with temperatures ranging from 75°F to 85°F year-round, moderated by trade winds that provide natural cooling. The dry season from December through May offers lower humidity and minimal rainfall, while the wet season from June through November brings higher humidity, frequent afternoon showers, and hurricane risk. Retirees from temperate climates should expect year-round heat and humidity requiring air conditioning for comfortable indoor living, particularly for those with heat sensitivity or medical conditions affected by high temperatures.

Electrical infrastructure in Antigua and Barbuda operates at 230 volts / 60 Hz using both US-style and UK-style outlets depending on building age. Power supply comes from diesel generators operated by the Antigua Public Utilities Authority, making electricity costs significantly higher than grid-based systems. Power outages occur regularly, particularly during storms or high-demand periods, with disruptions lasting from minutes to several hours. Retirees dependent on medical equipment requiring continuous power should invest in backup generators or battery systems costing $2,000 to $8,000 depending on capacity.

Water supply varies by location, with some areas receiving municipal water and others relying on private cisterns or trucked water delivery. Municipal water service experiences periodic interruptions during dry seasons or infrastructure maintenance. Water quality generally meets safety standards for consumption, though many residents use filtration systems or bottled water for drinking. Internet service is available through fiber optic and cable providers in main population centers, offering speeds adequate for video streaming, remote work, and communication. However, service reliability decreases in rural areas, and island-wide internet outages occasionally occur during severe weather events.

Transportation, Accessibility, and Mobility in Retirement

Personal vehicle ownership provides the most practical transportation solution for retirees in Antigua and Barbuda, as public transportation options are limited and inconsistent. The island operates bus services along major routes during daytime hours, but service frequency is irregular, coverage excludes many residential areas, and evening and weekend schedules are minimal. Bus fares cost $1 to $3 per trip, making public transport affordable but unreliable for retirees requiring predictable mobility for medical appointments, shopping, and daily activities.

Taxi services operate throughout the island with vehicles identifiable by “TX” license plates. Taxis use fixed route-based fares rather than meters, with prices negotiable before departure. Common routes cost $10 to $30, while longer trips or airport transfers range from $30 to $50. Taxis provide flexible transportation but become expensive for regular use, and availability decreases in less populated areas. Ride-sharing services like Uber do not operate in Antigua and Barbuda as of 2025.

Purchasing a used vehicle costs $8,000 to $15,000 for reliable transportation, with ongoing expenses including fuel at approximately $5 per gallon, insurance averaging $1,200 to $2,000 annually, and maintenance running higher than mainland costs due to limited parts availability and higher mechanic labor rates. Road conditions vary from well-maintained main highways to pothole-filled secondary roads, requiring vehicles with adequate ground clearance and suspension. Retirees with mobility limitations should ensure vehicles have appropriate accessibility features and verify that their living location provides manageable access to essential services.

Social Life, Expat Communities, and Cultural Integration

Antigua and Barbuda hosts a modest expatriate community concentrated in coastal areas and tourist zones including English Harbour, Jolly Harbour, and areas near major resorts. Expat social networks exist informally through yacht clubs, churches, volunteer organizations, and informal gatherings, but the community remains smaller and less organized than expatriate hubs in larger countries like Mexico, Costa Rica, or Spain. Retirees seeking extensive expatriate social infrastructure and organized activities may find options limited compared to more established retirement destinations.

Cultural integration varies by individual effort and openness. Antiguans generally welcome foreign residents respectfully but maintain distinct local culture and social patterns. English language use throughout the island eliminates language barriers and facilitates basic integration, but retirees should expect social circles to develop gradually rather than instantly. The island’s small population of approximately 100,000 creates close-knit communities where newcomers may initially feel outside established social networks.

Entertainment and cultural activities focus on outdoor recreation, water sports, beach activities, and informal social gatherings rather than extensive arts, theater, or organized cultural programming. The island hosts annual events including Carnival in late July and August, sailing week in late April, and various music festivals, but day-to-day entertainment options remain modest. Retirees expecting extensive restaurants, shopping, museums, or performing arts should adjust expectations to match small-island realities. Those who thrive in quiet, nature-focused environments with limited commercial entertainment typically adapt well, while retirees requiring frequent cultural stimulation or diverse dining options may find Antigua and Barbuda isolating over time.

8. Financial and Environmental Risks Retirees Must Plan For

Risk exposure in Antigua and Barbuda extends beyond typical retirement financial concerns to include environmental hazards, currency dynamics, and aging infrastructure limitations that can disrupt retirement security. Understanding these risks allows retirees to implement appropriate insurance coverage, maintain adequate emergency reserves, and make informed decisions about whether Antigua and Barbuda supports long-term retirement sustainability.

Hurricane and Climate Risk for Retirees

Hurricane season in Antigua and Barbuda runs officially from June 1 through November 30 each year, with peak activity occurring from August through October. While direct hurricane strikes on Antigua remain statistically infrequent compared to islands farther north in the Caribbean, the island experiences tropical storm impacts, near-miss hurricanes, and peripheral effects from storms passing nearby. These events create property damage, power outages lasting days to weeks, water supply disruptions, and temporary closure of businesses and services.

Hurricane insurance for property owners operates with high deductibles typically set at 2% to 5% of property value, meaning a home insured for $300,000 carries deductibles of $6,000 to $15,000 that owners must pay before insurance coverage applies. Many policies exclude flood damage, requiring separate flood insurance with additional premiums and deductibles. Combined hurricane and flood insurance costs reach 3% to 5% of property value annually, representing $9,000 to $15,000 per year for a $300,000 property, significantly impacting retirement budgets.

Retirees must maintain emergency preparedness including evacuation plans, supply stockpiles, and temporary housing arrangements for storm displacement periods. Hurricane evacuation from Antigua and Barbuda becomes difficult during storm approach due to limited airport capacity and flight availability. Retirees with mobility limitations, those requiring continuous medical care, or individuals with anxiety about storm exposure should carefully consider whether hurricane risk aligns with their risk tolerance and emotional capacity for managing regular storm threats.

Currency, Inflation, and Import Dependency Risks

The Eastern Caribbean Dollar (XCD) used in Antigua and Barbuda maintains a fixed exchange rate pegged to the US Dollar at XCD $2.70 = USD $1.00. This peg creates exchange rate stability for US-based retirees receiving income in US Dollars, eliminating currency fluctuation risk and simplifying budget planning. However, the peg does not protect against domestic inflation or the effects of Antigua and Barbuda’s import-dependent economy on cost of living.

Antigua and Barbuda imports approximately 90% of consumer goods including most food products, household items, vehicles, building materials, and manufactured products. Import dependency makes local prices vulnerable to international commodity costs, shipping rate fluctuations, and supply chain disruptions. Local inflation has historically run 3% to 5% annually, eroding purchasing power of fixed retirement incomes over time. Retirees living on fixed pensions or annuity payments without cost-of-living adjustments face declining real income as import costs rise.

Periodic supply chain disruptions create temporary shortages of specific products, forcing retirees to accept substitute products or pay premium prices for scarce items. Hurricane events in neighboring countries, global shipping constraints, or international trade disruptions can reduce product availability and spike prices rapidly. Retirees should maintain flexibility in consumption patterns and budget buffers of 10% to 15% above baseline expenses to accommodate price volatility and temporary shortages.

Aging-in-Place Challenges in Antigua and Barbuda

Antigua and Barbuda lacks assisted living facilities, nursing homes, and specialized senior care services available in larger countries. Retirees who develop mobility limitations, cognitive decline, or chronic conditions requiring daily assistance must rely on private home care workers, family support, or relocation to countries with established elder care infrastructure. Private home care workers can be hired for $8 to $15 per hour, but availability of trained caregivers with experience managing dementia, complex medical needs, or severe mobility limitations remains limited.

Medical equipment and mobility aids including wheelchairs, walkers, hospital beds, and specialized bathroom equipment face limited local availability and high costs due to import requirements. Retirees requiring such equipment often must order from overseas suppliers, pay import duties and shipping costs, and wait weeks for delivery. Home modifications for accessibility including ramps, grab bars, widened doorways, and roll-in showers require specialized contractors with limited availability and higher costs than mainland markets.

Retirees planning to age in place in Antigua and Barbuda should establish contingency plans including potential relocation to countries with elder care services, arrangements with family members for caregiving support, and sufficient financial reserves to fund private care workers or medical evacuation for long-term care facility placement elsewhere. The island works well for healthy, independent retirees but presents significant challenges for those who become frail or develop serious age-related health conditions requiring institutional care.

9. Who Should and Should NOT Retire in Antigua and Barbuda

Retirement suitability in Antigua and Barbuda depends on matching individual financial resources, health status, lifestyle preferences, and risk tolerance with the country’s specific advantages and limitations. Certain retiree profiles thrive in Antigua and Barbuda’s environment, while others face significant challenges that outweigh potential benefits. Honest assessment of fit prevents costly mistakes and ensures retirees choose locations aligned with their actual needs rather than idealized expectations.

Retirees Who Are a Good Fit

Financially secure retirees with monthly income of $4,000 or more for singles or $6,000 or more for couples can comfortably afford Antigua and Barbuda’s cost structure including housing, utilities, insurance, and discretionary spending. These income levels provide sufficient margin to absorb unexpected costs, maintain adequate insurance coverage, and enjoy lifestyle quality without constant budget stress. Retirees with substantial savings beyond monthly income can weather financial shocks from hurricane damage, medical events, or temporary income disruptions.

Health-wise, retirees in good overall health without chronic conditions requiring specialist care or complex medication management adapt best to Antigua and Barbuda’s limited medical infrastructure. Those under age 70, with stable health histories, who require only routine preventive care and minor illness treatment find local healthcare adequate. Retirees willing and financially able to purchase comprehensive international health insurance with medical evacuation coverage effectively mitigate healthcare limitations through access to regional medical facilities.

Lifestyle compatibility favors retirees who prefer quiet, nature-focused living over extensive urban amenities and cultural programming. Those who enjoy water activities, beach relaxation, outdoor recreation, and informal social patterns find Antigua and Barbuda deeply satisfying. Retirees comfortable with limited shopping, dining, and entertainment options and who do not require constant stimulation or variety thrive in the island’s slower-paced environment. Self-directed individuals who create their own structure and activities rather than relying on organized retirement communities succeed in Antigua and Barbuda’s independent living culture.

Retirees Who Should Reconsider

Budget-constrained retirees with monthly income below $3,000 for singles or $4,500 for couples face financial stress managing Antigua and Barbuda’s elevated costs for utilities, insurance, and imported goods. Those relying solely on Social Security or modest pensions without additional savings or investment income should reconsider, as thin margins leave no room for unexpected expenses, hurricane-related costs, or medical events requiring evacuation. Retirees who cannot afford comprehensive health insurance with evacuation coverage expose themselves to catastrophic financial risk.

Health-dependent retirees with chronic conditions requiring regular specialist care, complex medication regimens, or those with history of cardiac disease, cancer, or neurological conditions requiring monitoring face significant limitations. The island’s healthcare system cannot provide specialized geriatric care, advanced diagnostics, or complex treatment management necessary for serious chronic conditions. Retirees over age 75 or those with declining health trajectories should seriously question whether Antigua and Barbuda supports safe aging in place or creates medical risk.

Climate-sensitive individuals who struggle with heat, humidity, or tropical weather patterns will find Antigua and Barbuda uncomfortable or unhealthy. Those with anxiety about hurricane threats face annual stress from June through November that diminishes quality of life. Retirees requiring extensive social infrastructure, organized activities, diverse cultural programming, or proximity to family support systems should recognize these elements are largely absent in Antigua and Barbuda’s small-island environment. Those uncomfortable with infrastructure limitations including periodic power outages, water disruptions, and limited shopping variety will experience ongoing frustration that outweighs lifestyle benefits.

Final Decision Summary

Retiring in Antigua and Barbuda offers legitimate advantages for financially secure retirees seeking low-tax Caribbean living with stable currency, English-language environment, and tropical climate. The country’s exemption of foreign pension income from taxation, absence of capital gains and inheritance taxes, and relatively straightforward residency permit process create attractive conditions for income security and simplified tax planning. However, these benefits exist alongside significant trade-offs including elevated cost of living driven by import dependency, limited healthcare infrastructure requiring medical evacuation planning, mandatory hurricane risk management, and absence of aging-in-place support services.

Successful retirement in Antigua and Barbuda requires income of at least $3,500 to $4,000 monthly for modest living or $5,000 to $7,000 monthly for comfortable retirement. Retirees must budget for comprehensive international health insurance, maintain emergency reserves for hurricane-related expenses, and accept healthcare limitations that necessitate medical evacuation coverage for serious health events. Property ownership involves substantial upfront costs including Alien Land Holding License fees and ongoing hurricane insurance obligations that significantly impact total cost of ownership.

The decision to retire in Antigua and Barbuda should center on realistic assessment of financial capacity, health status, lifestyle preferences, and risk tolerance rather than romanticized visions of Caribbean paradise. Retirees who thrive are typically healthy, financially secure, comfortable with quiet island living, and willing to proactively manage risks through adequate insurance and contingency planning. Those dependent on extensive medical services, operating on tight budgets, or requiring robust social infrastructure should carefully weigh whether Antigua and Barbuda truly serves their long-term retirement needs or whether alternative destinations provide better alignment with their actual requirements.

Retirement planning for Antigua and Barbuda should include extended exploratory visits during both dry and hurricane seasons, consultation with cross-border tax advisors, review of comprehensive health insurance options with evacuation coverage, and honest evaluation of whether the island’s specific characteristics match individual priorities. This planning-focused approach, grounded in transparent assessment of both benefits and limitations, increases the likelihood of sustainable, satisfying retirement outcomes while avoiding costly misalignment between expectations and reality.