Table of Contents

Contents are generated from article headings.

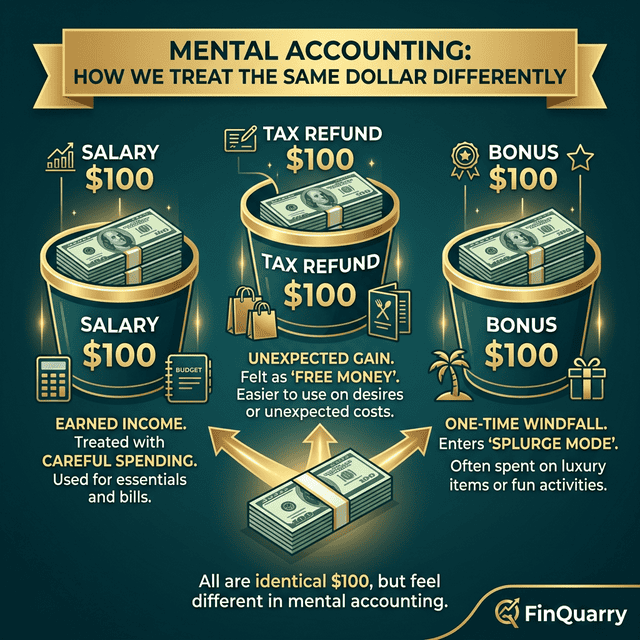

Mental accounting is the cognitive process through which people categorize, label, and evaluate their financial resources by assigning them to subjective “mental accounts” rather than treating all money as interchangeable. Mental accounting was first described by economist Richard Thaler in 1985 and further developed in his 1999 paper “Mental Accounting Matters.” Mental accounting explains why people treat a $500 tax refund differently from $500 in regular salary, why people keep money in low-interest savings while carrying high-interest credit card debt, and why people are more willing to gamble with “house money” (recent gains) than with their original capital — even though money is objectively fungible regardless of its source, label, or subjective category.

Mental accounting is not a flaw to be eliminated — it is a cognitive tool that evolved to simplify financial complexity. Without mental accounting, every financial decision would require evaluating the entire financial picture simultaneously, which is cognitively impractical. The problem is not that mental accounting exists; the problem is that the shortcuts mental accounting produces are systematically biased in ways that reduce financial efficiency.

Scope and Context: This content discusses mental accounting and its effects on financial behavior using behavioral economics research, established psychological frameworks, and consumer finance principles. Financial products, regulations, and tax treatments vary by jurisdiction and institution. Readers should evaluate the relevance of specific examples to their own financial and regulatory context.

What Is Mental Accounting?

Mental accounting is the set of cognitive operations that individuals use to organize, evaluate, and track their financial activities. Rather than maintaining a single, unified view of their total financial position — as standard economic theory assumes — people mentally divide their money into separate accounts based on criteria including the source of the money, its intended use, and the emotional associations attached to it.

The Fungibility Violation

The core mechanism of mental accounting is the violation of fungibility — the economic principle that all units of money are interchangeable and should be evaluated identically regardless of source, location, or label. Standard economic theory states that a dollar is a dollar: $100 in a savings account has exactly the same value and utility as $100 received as a gift, earned as overtime pay, or found on the street.

Mental accounting violates fungibility by assigning different psychological values to different dollars based on non-financial criteria. A person might refuse to use their “emergency fund” savings to pay off high-interest credit card debt, even though the interest cost of the debt exceeds the interest earned on the savings — because the money in the emergency fund is mentally labeled “safety” and the debt is mentally labeled “obligations,” and the two categories feel like they should not interact.

Richard Thaler’s Framework

Richard Thaler — who received the 2017 Nobel Memorial Prize in Economic Sciences for his contributions to behavioral economics — identified three key components of mental accounting: how outcomes are perceived and experienced (transaction utility), how activities are assigned to specific mental accounts, and how frequently accounts are evaluated (the evaluation period). Each component introduces systematic biases that deviate from the predictions of rational economic theory and helps explain why people make irrational money decisions.

How Mental Accounting Affects Spending Behavior

Mental accounting produces specific, predictable distortions in spending behavior by changing how people perceive the cost of a purchase depending on which mental account the expenditure is “charged” to.

The Source-of-Money Effect

People spend money differently based on how they acquired it, even when the amounts are identical. Windfall income — tax refunds, bonuses, inheritance, lottery winnings, cash gifts — is consistently spent more freely than earned income, because windfall money is mentally categorized as “extra” or “found” money rather than as part of the person’s core financial resources.

This source-of-money effect has measurable consequences. A person who receives a $3,000 tax refund may spend it on a vacation, while the same person would not withdraw $3,000 from their regular savings for the same purpose — even though both actions reduce their total financial position by the same amount. The refund feels different from savings because mental accounting assigns it to a different category, with different spending rules attached to that category.

Payment Method and the Pain of Paying

Mental accounting is influenced by the payment method because different payment mechanisms produce different levels of psychological spending friction — what behavioral economists call the “pain of paying.” Cash payments produce the highest pain of paying because they involve a visible, physical reduction in the payer’s resources. Credit card payments substantially reduce the pain of paying because the expenditure is decoupled from the moment of consumption — the cost is aggregated into a future bill rather than experienced at the point of purchase.

Digital payment methods (mobile wallets, one-click purchasing, automatic subscriptions) further reduce the pain of paying by abstracting the transaction to the point where the spender may barely register that money has been exchanged. This progressive reduction in payment friction — from cash to card to digital — systematically increases spending velocity because each step removes another layer of the psychological feedback that would otherwise moderate purchasing decisions. Understanding this mechanism is essential to managing emotional spending triggers.

Transaction Utility and “Good Deal” Bias

Mental accounting produces transaction utility — the psychological value a person derives from the perceived quality of a deal, independent of the item’s actual utility or worth. A person may buy an item they do not need because it is “50% off,” perceiving a gain (the savings) rather than a loss (the expenditure). The transaction utility (feeling of getting a deal) compensates for or masks the actual financial cost.

Transaction utility explains why discount framing is so effective in retail: presenting a price reduction relative to an anchor (original price) creates positive transaction utility even when the discounted price is not objectively favorable. This mechanism interacts with anchoring bias — the original price serves as the anchor, and mental accounting treats the difference between the anchor and the sale price as a “gain” in the shopper’s mental account.

Mental Accounting in Saving and Investing

Mental accounting affects saving and investing behavior by creating subjective compartments that prevent people from optimizing their total financial position.

The Savings-Debt Paradox

The most financially costly manifestation of mental accounting is the simultaneous maintenance of savings and high-interest debt. A person may keep $10,000 in a savings account earning 4% while carrying $10,000 in credit card debt at 22%. Mathematically, using the savings to eliminate the debt would produce an immediate net benefit of approximately 18 percentage points in annual interest differential. However, mental accounting assigns the savings and the debt to separate mental categories — “my safety net” and “my obligations” — and the person resists combining them because depleting the savings account feels like losing their financial cushion, even though eliminating the debt produces a larger net improvement in financial position.

This savings-debt paradox is widespread. Consumer financial surveys have documented that a significant portion of households simultaneously carry revolving debt and maintain liquid savings that could reduce or eliminate that debt — a pattern that rational economic theory cannot explain but mental accounting predicts precisely.

House Money Effect in Investing

The house money effect describes the tendency to take greater risks with money obtained from recent gains than with money from the original investment. The term originated in gambling — players who are “ahead” tend to bet more aggressively because they mentally categorize their gains as “the house’s money” rather than as their own money.

In investing, the house money effect causes investors to take disproportionately large risks with profits from previous successful trades. An investor who made $20,000 from a stock trade may invest that $20,000 in a highly speculative position that they would never have funded with their original capital — because the gains are mentally categorized as “bonus money” with a lower psychological attachment. The financial reality is that $20,000 in gains has the same purchasing power and investment potential as $20,000 in original capital, but mental accounting assigns them different risk tolerances.

Goal-Based Mental Accounts

Mental accounting creates goal-based savings categories — vacation fund, emergency fund, home down payment fund, college fund — that function as separate financial compartments with distinct rules about when and how the money can be used. While goal-based accounts can serve as useful self-control mechanisms (making saving more concrete and motivated), they also introduce inefficiency by preventing optimal allocation across the total portfolio.

A person with $5,000 in a vacation fund and $5,000 in an emergency fund may face an urgent $7,000 expense and feel unable to access the vacation fund for the emergency, instead turning to high-interest borrowing. The mental account labels create artificial constraints that prevent the person from treating their total $10,000 in liquid savings as a unified resource available for the highest-priority need.

How Businesses Exploit Mental Accounting

Businesses systematically exploit mental accounting by designing pricing, payment structures, and promotional strategies that align with — and take advantage of — the way consumers categorize and evaluate financial transactions.

Subscription and Bundling Strategies

Subscription models exploit mental accounting by converting variable expenses into fixed mental accounts. A person who would resist paying $15 per movie in a theater may readily commit to a $20/month streaming subscription that they use irregularly — because the subscription is mentally categorized as a fixed monthly expense (like utilities) rather than as a per-use entertainment cost. The fixed categorization reduces per-use evaluation, which reduces the scrutiny applied to whether the service provides proportional value.

Gift Card and Credit Strategies

Gift cards exploit mental accounting by converting money into a form that is psychologically pre-committed to spending. A person who receives a $50 gift card is more likely to spend the full amount — and may spend beyond it — than a person who receives $50 in cash, because the gift card is mentally categorized as “spending money” while cash would be partially categorized as “savings” or “regular income.” The mental account assignment changes the perceived purpose of the money, which changes spending behavior.

How to Counteract Mental Accounting Biases

Mental accounting biases can be reduced — though rarely eliminated — through strategies that increase financial transparency and counteract the natural tendency to compartmentalize money.

Consolidated Financial Tracking

Viewing all financial resources and obligations on a single dashboard — total assets, total liabilities, net worth — counteracts the compartmentalization that enables mental accounting biases. When a person can see their savings and their debt simultaneously, the irrationality of maintaining both becomes more visible. Consolidated tracking does not eliminate mental accounting, but it creates System 2 intervention opportunities by making the cost of compartmentalization explicit.

Rules-Based Spending Frameworks

Establishing percentage-based budgeting frameworks (such as allocating fixed percentages of income to spending, saving, and debt reduction) partially counteracts mental accounting by imposing consistent rules across categories. When the allocation system is automated, it further reduces the influence of mental accounting by removing the decision point where category-based biases would operate.

Pre-Commitment to Windfall Allocation

Deciding in advance how windfall income will be allocated — before the windfall is received — reduces the source-of-money effect that causes windfalls to be spent more freely. A pre-commitment rule such as “50% of any windfall goes to debt reduction, 30% to savings, 20% to discretionary spending” imposes structure on money that would otherwise be mentally categorized as “extra” and spent without the scrutiny applied to regular income.

What Is the Difference Between Mental Accounting and Budgeting?

Mental accounting is an unconscious cognitive process that categorizes money into subjective mental accounts based on source, timing, and emotional association. Budgeting is a deliberate financial planning activity that allocates income across defined spending categories based on financial goals and constraints. The key difference is that budgeting is intentional and can be optimized, while mental accounting operates automatically and often produces irrational allocations. Effective budgeting can partially override mental accounting by imposing systematic rules that apply consistently regardless of the subjective “feel” of different money categories.

Does Mental Accounting Always Lead to Bad Financial Outcomes?

Mental accounting does not always produce negative outcomes. The same categorization mechanism that causes irrational spending patterns can also function as an effective self-control tool. For example, mentally designating a specific account as an “emergency fund” and treating it as psychologically inaccessible for non-emergencies creates a commitment device that prevents the money from being spent on discretionary purchases. Similarly, money habits built around goal-based savings accounts leverage mental accounting to make abstract financial goals feel concrete and motivating. The key is whether the mental account structure supports or undermines the person’s financial objectives.

How Does Mental Accounting Affect Retirement Savings?

Mental accounting affects retirement savings by creating a temporal mental account — money for “future self” — that competes with mental accounts for present needs and desires. Because the present self and the future self are mentally categorized as almost separate entities, people tend to underfund retirement accounts relative to their long-term needs. Research in behavioral economics suggests that strategies making the future self more vivid and concrete — such as retirement projection calculators that show specific lifestyle outcomes — can partially counteract this temporal mental accounting bias.

Can Awareness of Mental Accounting Change Financial Behavior?

Awareness of mental accounting can change financial behavior, but only when combined with structural countermeasures. Simply knowing that mental accounting exists does not prevent it from operating, because the categorization process is automatic and pre-conscious. However, awareness enables a person to recognize when mental accounting may be influencing a decision — such as when they are about to spend a windfall more freely than regular income — and to deliberately engage analytical processing before acting. Combining awareness with systems like automated allocation rules, consolidated financial dashboards, and pre-commitment strategies produces the most effective countermeasure to mental accounting biases.