Table of Contents

Contents are generated from article headings.

Investment discipline is the consistent adherence to a structured investment plan, combining goal-setting, systematic portfolio management, cost control, and behavioral awareness to achieve long-term financial success. It involves maintaining predetermined asset allocations, rebalancing systematically, resisting emotional impulses during market volatility, and staying invested through complete market cycles. Disciplined investors follow evidence-based strategies rather than reacting to short-term market movements, media narratives, or fear-driven speculation.

The foundation of investment discipline rests on four interconnected pillars: clear financial goals, balanced asset allocation, rigorous cost management, and behavioral self-regulation. Goals provide direction and motivation, translating abstract investment plans into concrete objectives with measurable timelines. Asset allocation establishes the strategic framework that determines long-term returns and risk exposure, while systematic rebalancing maintains this framework despite market fluctuations. Cost management preserves returns by minimizing fees, taxes, and unnecessary trading expenses that compound negatively over decades. Behavioral discipline prevents cognitive biases—such as loss aversion, recency bias, and herd mentality—from triggering impulsive decisions that undermine long-term strategies.

Investment discipline does not guarantee profits, eliminate market risk, or require perfect market timing. Rather, it increases the probability of achieving financial objectives by aligning investor behavior with evidence-based principles that have historically supported wealth accumulation. Vanguard’s analysis of global market returns from 1901 to 2022 demonstrates that disciplined investors who maintained diversified portfolios and stayed invested through volatility achieved median annual returns of 7-10%, while those who attempted market timing or chased performance underperformed by 2-4% annually. This performance gap compounds significantly over multi-decade timeframes, representing hundreds of thousands of dollars in potential wealth difference for typical retirement savers.

Scope Note: This content explains the mathematical and behavioral mechanisms of investment discipline using general financial principles. Investment outcomes, tax treatment, interest rates, and results vary by country, regulation, financial system, and individual circumstances. This guidance is educational, not financial advice.

What Is Investment Discipline in Investing?

Investment discipline is the systematic application of predefined investment rules and strategies regardless of emotional impulses, market sentiment, or short-term performance fluctuations. It operates as a decision-making framework that separates investment choices from psychological biases, ensuring actions align with long-term objectives rather than immediate market conditions.

Disciplined investing requires establishing explicit criteria for asset selection, allocation percentages, rebalancing triggers, and exit conditions before emotional pressures arise. This pre-commitment approach creates behavioral guardrails that prevent reactive decisions during periods of market stress or euphoria. When markets decline sharply, disciplined investors follow predetermined rules rather than abandoning strategies based on fear. During market bubbles, discipline prevents overconcentration in speculative assets driven by greed or herd behavior.

The micro-behavioral foundation of investment discipline involves habit formation, where repeated adherence to investment rules reduces the cognitive effort required for future decisions. Early-stage discipline demands conscious effort and willpower to resist temptation, but sustained practice automates these behaviors, transforming discipline from an active struggle into a passive default. Investors who automate contributions, establish rebalancing schedules, and document decision-making criteria in written Investment Policy Statements reduce reliance on willpower and increase consistency over multi-decade periods.

Investment discipline is not rigidity or blind adherence to failing strategies. Discipline requires periodic review and adjustment as life circumstances change—such as approaching retirement, experiencing major income shifts, or facing health challenges that alter risk tolerance. The distinction lies between systematic, planned adjustments based on predetermined criteria versus impulsive reactions to market movements or emotional discomfort. Disciplined investors modify strategies when fundamental assumptions change, not when quarterly performance disappoints or media headlines generate anxiety.

Why Values-Based and Integrity-Driven Approaches Enhance Investment Discipline

Values-based investing integrates personal ethical principles and long-term objectives into investment frameworks, creating alignment between financial strategies and deeply held beliefs that reinforces behavioral commitment. When investment choices reflect core values—such as environmental sustainability, social responsibility, or specific exclusionary criteria—investors experience reduced cognitive dissonance during market volatility, strengthening adherence to long-term plans.

Ethical investment frameworks establish intrinsic motivation beyond profit maximization, which behavioral research demonstrates creates more durable commitment than purely financial incentives. Investors who articulate why specific strategies align with personal values develop stronger psychological ownership of their plans, increasing resilience during periods when discipline is tested. This values-driven foundation functions as an additional commitment device, supplementing traditional financial discipline with moral and philosophical reinforcement.

Integrity-driven investment processes at the firm level enhance client discipline through transparent communication, consistent methodology application, and aligned incentive structures. Investment advisors and fund managers who demonstrate process integrity—following stated strategies during both favorable and challenging periods—build client trust that reduces the likelihood of panic-driven withdrawals during downturns. Firms that maintain discipline in their own investment processes model the behavior they recommend, creating social proof that reinforces client adherence.

Corporate governance structures that prioritize long-term client outcomes over short-term asset gathering tend to produce more disciplined investment cultures. Firms with employee ownership, long-term compensation structures, and risk management protocols that prevent style drift demonstrate institutional discipline that cascades to client relationships. Investment committees that enforce systematic review processes, document decision rationale, and maintain accountability for deviations from stated strategies create organizational discipline that supports individual investor behavior.

Client-advisor alignment on values and objectives clarifies expectations and reduces misunderstandings that often trigger discipline breakdowns. When advisors explicitly discuss client values, risk tolerance boundaries, and acceptable trade-offs between competing objectives, they establish shared understanding that prevents misaligned reactions during market stress. This values-based alignment enables advisors to remind clients of their stated priorities during emotional moments, using the client’s own articulated values as behavioral anchors.

How Disciplined Investment Processes Improve Portfolio Quality

Disciplined investment processes improve portfolio quality by applying consistent, evidence-based screening criteria that filter opportunities through fundamental analysis rather than momentum, sentiment, or speculation. Quality-focused processes evaluate companies based on durable competitive advantages, sustainable earnings, strong balance sheets, and rational capital allocation—characteristics that tend to outperform over complete business cycles while exhibiting lower volatility during downturns.

Systematic quality screens prevent emotional biases from influencing security selection. Investors without disciplined processes often gravitate toward recent high-performers (performance chasing), exciting narratives (story bias), or familiar companies (home bias and availability heuristic), creating portfolios concentrated in overvalued, cyclical, or geographically concentrated positions. Disciplined processes apply valuation disciplines, diversification requirements, and risk controls systematically, reducing exposure to these behavioral traps.

Portfolio construction discipline establishes allocation rules that maintain diversification across asset classes, sectors, geographic regions, and market capitalizations. These rules prevent concentration in any single risk factor, reducing portfolio vulnerability to sector-specific downturns or regional economic challenges. Disciplined rebalancing enforces these allocation targets mechanically, selling outperforming positions that have grown beyond target weights and buying underperforming positions that have fallen below targets—a systematic implementation of “buy low, sell high” that occurs without requiring market timing skill.

Quality-focused discipline also manifests in holding period discipline, where investors maintain positions through normal business cycle fluctuations rather than reacting to quarterly earnings volatility or temporary operational challenges. Research by investment firms practicing patient, quality-focused strategies demonstrates that low portfolio turnover—typically under 10-20% annually—reduces trading costs, minimizes tax consequences, and allows fundamental value to compound without interruption from unnecessary trading.

Trend avoidance through disciplined processes protects portfolios from bubble participation and subsequent crashes. Disciplined investors recognize that trending sectors exhibiting parabolic price appreciation, extreme valuation multiples, and widespread media enthusiasm represent elevated risk regardless of compelling narratives. By maintaining valuation discipline and diversification requirements, systematic processes prevent overconcentration in speculative trends, preserving capital during inevitable reversions to historical valuation norms.

Role of Disciplined Fund Managers in Long-Term Returns

Disciplined fund managers achieve superior long-term risk-adjusted returns by maintaining process consistency through complete market cycles, resisting performance pressures that tempt style drift or strategy abandonment during periods of underperformance. Managers who document investment philosophies, establish explicit decision-making criteria, and adhere to these frameworks regardless of short-term results create the conditions for long-term alpha generation.

Process discipline at the manager level requires resisting institutional pressures to chase recent performance trends or modify strategies to attract asset flows during periods when the manager’s approach underperforms popular alternatives. Many fund managers abandon disciplined value approaches during late-stage bull markets when growth strategies dominate, only to miss the subsequent market rotation that vindicates their original methodology. Managers who maintain discipline through these challenging periods capture the full cycle returns that justify their stated investment philosophy.

Performance monitoring frameworks that emphasize process adherence over short-term results support managerial discipline. Investment committees and boards that evaluate managers based on consistency with stated strategies, risk management effectiveness, and decision-making quality—rather than quarterly performance rankings—create environments where discipline can flourish. This process-focused evaluation reduces pressure to make reactionary changes that frequently harm long-term results.

Client alignment represents another critical factor in manager discipline. Managers working with clients who understand and accept the manager’s investment philosophy demonstrate higher process consistency because they face fewer redemption pressures during inevitable periods of underperformance. This alignment allows managers to maintain contrarian positions, implement rebalancing disciplines, and execute long-term strategies without capital flight undermining their ability to realize strategy benefits.

Disciplined managers typically exhibit low portfolio turnover, concentrated conviction positions within diversified frameworks, and willingness to hold meaningful cash positions when valuation discipline prevents finding attractively priced opportunities. These characteristics distinguish process-driven managers from closet indexers who maintain high active share only during favorable market conditions or momentum-driven managers who chase recent winners without fundamental discipline.

Manager tenure and organizational stability also correlate with disciplined investing. Firms with long-tenured investment teams, stable ownership structures, and compensation systems aligned with long-term performance create institutional memory and culture that reinforces discipline. High turnover among investment professionals disrupts process consistency and institutional knowledge, reducing the likelihood of sustained disciplined execution.

How Firms Maintain Discipline in Investment Strategies

Investment firms maintain strategic discipline through corporate governance structures, investment committee oversight, compliance frameworks, and cultural norms that prioritize process consistency over short-term performance or asset gathering. Effective governance establishes clear accountability for strategy adherence, documents decision rationale, and reviews deviations from stated methodologies systematically.

Investment committee structures that separate portfolio management from sales and marketing functions reduce conflicts of interest that pressure managers to modify strategies for commercial rather than investment reasons. Committees with independent oversight, documented decision-making protocols, and systematic review cycles create institutional discipline that transcends individual portfolio manager preferences or market sentiment.

Risk management frameworks embedded in firm-level processes enforce discipline by establishing guardrails that prevent excessive concentration, leverage, or deviation from stated risk parameters. Automated compliance systems monitor portfolio characteristics continuously, flagging violations of diversification requirements, position size limits, or sector concentration thresholds before they materialize into significant risks. These systematic controls function as organizational commitment devices that make undisciplined behavior operationally difficult rather than relying solely on individual restraint.

Regular strategy review cycles—typically quarterly or annually—assess whether investment processes remain aligned with stated objectives, whether market or regulatory changes require methodology updates, and whether performance outcomes reflect skill or luck. These structured reviews distinguish between systematic process failures requiring modification and temporary underperformance representing normal strategy variation. By documenting review findings and decision logic, firms create institutional memory that prevents cyclical repetition of past mistakes.

Cultural factors significantly influence firm-level discipline. Organizations that celebrate long-term thinking, reward process excellence over short-term performance, and maintain transparency about investment rationale during challenging periods build cultures where discipline flourishes. Conversely, firms emphasizing short-term rankings, incentivizing asset gathering regardless of strategy capacity, or avoiding accountability for strategy deviations create environments where discipline erodes under commercial pressure.

Employee compensation structures aligned with long-term results rather than quarterly performance or annual asset flows support disciplined decision-making. Deferred compensation, equity ownership in the firm, and multi-year performance measurement periods reduce incentives for short-term risk-taking or strategy abandonment during temporary underperformance. These alignment mechanisms create personal financial consequences for undisciplined behavior, reinforcing institutional discipline through self-interest.

How Behavioral Discipline Supports Investment Strategies

Behavioral discipline prevents cognitive biases and emotional impulses from undermining evidence-based investment strategies, functioning as the psychological foundation that enables adherence to long-term plans during periods of market stress or euphoria. Without behavioral discipline, technically sound investment strategies fail because investors abandon them at precisely the moments when discipline matters most.

Loss aversion—the tendency to experience losses approximately twice as intensely as equivalent gains—drives disproportionate emotional reactions to portfolio declines that trigger panic selling near market bottoms. During the 2008-2009 financial crisis, investors who sold equity positions in March 2009 locked in losses exceeding 50% and missed the subsequent recovery that restored portfolios to previous highs within five years. Loss aversion caused these investors to violate fundamental discipline principles, selling low after experiencing maximum psychological pain rather than maintaining allocation discipline or rebalancing into discounted assets.

Recency bias causes investors to overweight recent market performance when forming expectations about future returns, creating cyclical patterns of excessive optimism after bull markets and extreme pessimism following downturns. This bias manifests in performance chasing, where investors allocate disproportionately to asset classes or strategies that performed well recently, buying high after appreciation has already occurred. Research demonstrates that the typical investor underperforms the funds they invest in by 2-4% annually because recency bias drives poor timing decisions—buying after strong performance and selling after poor performance.

Herd mentality—the psychological pressure to conform to crowd behavior—intensifies during market extremes, driving bubble participation and panic selling. During speculative manias, investors experience social pressure to join trending investments regardless of valuation discipline, fearing they will miss out on continued gains (FOMO—fear of missing out). During crashes, herd behavior triggers coordinated selling that amplifies declines beyond fundamental justification. Disciplined investors recognize these social pressures and implement pre-commitment strategies—such as Investment Policy Statements and automatic rebalancing—that create behavioral distance from crowd dynamics.

Overconfidence bias leads investors to overestimate their market timing ability, stock-picking skill, and capacity to outperform professional managers, resulting in excessive trading that increases costs and taxes while generally producing inferior returns. Studies of brokerage account data demonstrate that the most actively trading investors underperform the least active investors by approximately 6% annually, with the performance gap primarily attributable to transaction costs and poor timing decisions driven by overconfidence.

Confirmation bias filters information processing to preferentially accept data supporting existing beliefs while dismissing contradictory evidence, preventing investors from objectively reassessing positions when fundamentals deteriorate. This bias causes investors to hold losing positions too long, interpreting negative news through optimistic lenses that preserve existing convictions. Disciplined investment processes implement systematic review criteria that force objective evaluation regardless of emotional attachment to positions.

Anchoring bias fixates on arbitrary reference points—such as purchase price or historical highs—when making selling decisions, preventing rational evaluation based on current valuations and forward prospects. Investors anchored to purchase prices often refuse to sell losing positions until “breaking even,” even when capital would achieve higher returns in alternative investments. Similarly, anchoring to historical portfolio highs creates unrealistic expectations during normal market fluctuations, triggering dissatisfaction and strategy abandonment.

The disposition effect—the tendency to sell winning positions prematurely while holding losing positions too long—directly contradicts optimal tax and portfolio management. This bias causes investors to realize taxable gains on appreciating positions while deferring tax-loss harvesting on declining positions, creating tax inefficiency. From a portfolio perspective, the disposition effect increases concentration in underperforming positions while reducing exposure to outperformers, systematically degrading portfolio quality.

Behavioral discipline mitigates these biases through habit formation, pre-commitment devices, automated processes, and systematic decision frameworks that remove discretion at moments of peak emotional intensity. By recognizing that human psychology predictably generates wealth-destroying impulses during market extremes, disciplined investors design systems that protect them from themselves.

Step-by-Step Framework for Building Personal Investment Discipline

Building personal investment discipline requires systematic implementation of behavioral, structural, and procedural elements that collectively create resilience against emotional impulses and cognitive biases. This framework progresses from goal clarity through automation and monitoring.

Step 1: Establish SMART Investment Goals

Investment goals must be Specific, Measurable, Achievable, Relevant, and Time-bound to provide actionable direction and create accountability. Vague aspirations like “grow wealth” or “retire comfortably” lack the precision necessary to guide allocation decisions or measure progress. Effective goals specify dollar amounts, timelines, and success criteria: “Accumulate $1.5 million in retirement accounts by age 65 to support $60,000 annual inflation-adjusted withdrawals using a 4% withdrawal rate.”

Specific goals enable selection of appropriate asset allocations, contribution requirements, and risk tolerance boundaries. A 25-year-old with 40-year time horizon can tolerate higher equity allocations and short-term volatility than a 60-year-old approaching retirement, because the younger investor has decades to recover from downturns. Goals also establish priority hierarchies when resources are limited, clarifying trade-offs between competing objectives like retirement savings, education funding, or home purchase.

Measurable goals create feedback loops that reinforce discipline by demonstrating progress or highlighting needed adjustments. Quarterly or annual progress reviews comparing actual portfolio values against projected trajectories provide concrete evidence that discipline is working, strengthening commitment during periods when market volatility creates emotional discomfort. Conversely, significant deviations from projected paths trigger systematic reviews to determine whether increased contributions, allocation modifications, or goal adjustments are necessary.

Step 2: Determine Asset Allocation and Diversification Rules

Asset allocation determines 80-90% of long-term portfolio returns and volatility, making it the most critical strategic decision investors make. Disciplined allocation establishes target percentages across major asset classes—stocks, bonds, real estate, commodities—based on time horizon, risk tolerance, income needs, and tax circumstances. These targets function as behavioral anchors that guide rebalancing decisions and prevent emotional allocation shifts during market cycles.

Diversification rules specify allocation across subcategories within asset classes: domestic vs. international stocks, large-cap vs. small-cap, growth vs. value, government vs. corporate bonds. Systematic diversification reduces concentration risk and ensures portfolio exposure to multiple return drivers rather than depending on narrow sectors or geographic regions. Home bias—the tendency to overweight domestic investments—represents a common diversification failure that increases portfolio volatility and reduces expected returns relative to globally diversified alternatives.

Rebalancing triggers establish mechanical rules for when and how to restore target allocations after market movements create drift. Common approaches include calendar-based rebalancing (annually or semi-annually regardless of drift magnitude) or threshold-based rebalancing (when any asset class deviates more than 5% from target). Both approaches enforce discipline by removing discretion and emotion from rebalancing timing, ensuring that the discipline of “selling high and buying low” occurs systematically.

Step 3: Automate Contributions and Rebalancing

Automation removes decision points that create opportunities for discipline failures, transforming adherence from an active choice requiring willpower into a passive default that occurs without ongoing effort. Automatic payroll deductions or bank transfers ensure consistent contributions regardless of market sentiment, eliminating the temptation to reduce savings during downturns or delay contributions while waiting for “better” entry points.

Dollar-cost averaging through automated contributions implements discipline by purchasing more shares when prices are low and fewer when prices are high, without requiring market timing skill. This systematic approach prevents the common mistake of reducing equity purchases during declines (when valuations are attractive) while increasing purchases during rallies (when valuations are elevated). Over multi-decade periods, dollar-cost averaging tends to produce superior outcomes compared to attempting to time market entry points.

Automated rebalancing through target-date funds, robo-advisors, or brokerage platform features maintains allocation discipline without requiring manual monitoring or execution. These systems detect allocation drift, calculate required transactions, and execute rebalancing trades according to predetermined schedules or thresholds. Automation also prevents procrastination and inertia—powerful forces that cause investors to delay rebalancing even when they intellectually recognize its importance.

Step 4: Monitor Costs, Fees, and Tax Efficiency

Investment costs compound negatively over time, reducing portfolio values by amounts that often exceed the impact of individual investment decisions. A 1% annual fee difference compounds to approximately 25% reduction in terminal wealth over 30 years, making cost management a critical discipline component. Disciplined investors systematically compare fund expense ratios, advisor fees, trading commissions, and tax consequences, selecting low-cost alternatives when they provide equivalent exposure.

Tax efficiency requires coordinating asset location (which accounts hold which assets), withdrawal sequencing, and tax-loss harvesting strategies to minimize lifetime tax burden. Tax-inefficient investments like actively managed funds generating short-term capital gains should be held in tax-deferred accounts, while tax-efficient investments like index funds or municipal bonds can be held in taxable accounts. This asset location discipline can add 0.3-0.5% to annual after-tax returns without increasing risk.

Tax-loss harvesting maintains discipline during downturns by systematically realizing losses to offset gains elsewhere in the portfolio, reducing current tax liability while maintaining desired asset allocation through substantially identical replacement positions. This process transforms temporary market declines into permanent tax benefits, creating silver linings during volatile periods that reinforce discipline by producing tangible benefits from adhering to long-term strategies.

Step 5: Document Decisions and Track Behavioral Adherence

Investment Policy Statements (IPS) formalize investment goals, allocation targets, rebalancing rules, and behavioral commitments in written documents that serve as commitment devices during emotional periods. IPS documents answer key questions prospectively: What allocation will I maintain? When will I rebalance? Under what circumstances will I modify my strategy? What behaviors will I avoid? By documenting these decisions during calm, rational periods, investors create reference points that counter emotional impulses during market extremes.

Behavioral tracking quantifies discipline through metrics such as contribution consistency (% of periods where planned contributions occurred), allocation drift (average deviation from target allocation), rebalancing frequency (adherence to stated rebalancing schedule), and trading frequency (compared to stated turnover targets). These metrics transform abstract discipline into measurable behaviors that can be monitored and improved systematically. Regular review of these metrics—quarterly or annually—provides feedback that reinforces positive behaviors and identifies areas requiring additional commitment devices or automation.

Decision journaling documents the rationale behind significant investment decisions, creating accountability and learning opportunities. By recording why specific positions were purchased, what would constitute a selling criterion, and what evidence would invalidate the investment thesis, investors create objective standards that prevent rationalization and confirmation bias from perpetuating mistakes. Periodic journal reviews comparing actual outcomes to documented expectations calibrate decision-making and identify recurring behavioral patterns requiring correction.

How Staying Invested Reinforces Discipline and Wealth Accumulation

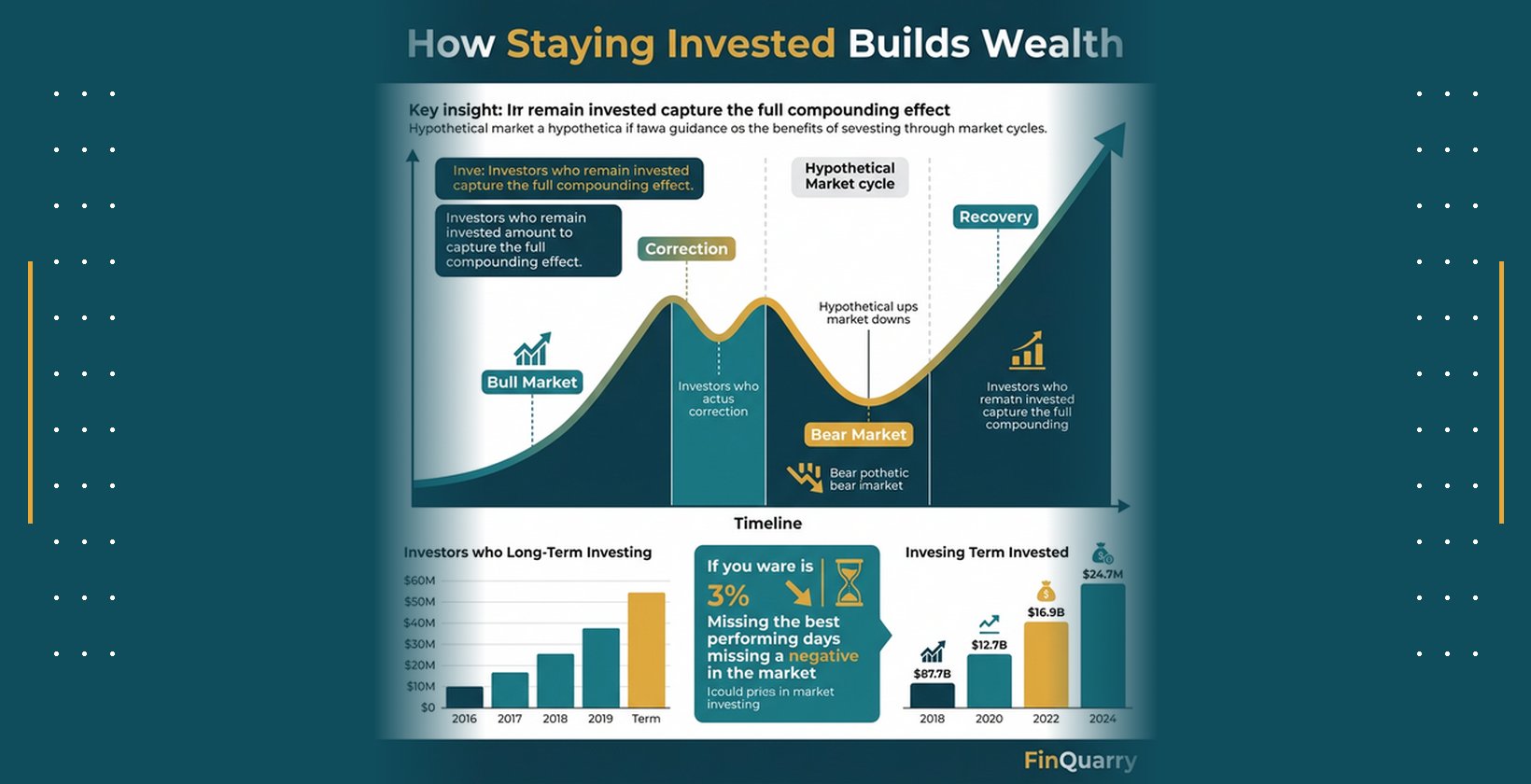

Staying invested through complete market cycles captures the full compounding effect of long-term returns, which occur disproportionately during brief periods of exceptional performance that are impossible to predict. Market timing attempts—shifting between stocks and cash based on economic forecasts or technical indicators—consistently underperform buy-and-hold strategies because timing systems inevitably miss the best-performing days that drive long-term returns.

Analysis of S&P 500 returns from 1970 to 2020 demonstrates that missing just the 10 best-performing days would have reduced total returns by approximately 50%, transforming a $10,000 initial investment worth roughly $700,000 into approximately $350,000. These best days often occur during periods of extreme volatility and frequently cluster near market bottoms, making them particularly likely to be missed by investors who exit during downturns. The impossibility of reliably predicting these critical days argues strongly for continuous market exposure.

Staying invested also avoids the psychological trap of attempting to time re-entry after exiting during downturns. Investors who sell during declines face the dual challenge of when to repurchase—a decision fraught with fear that prices will decline further and regret over missing recovery rallies. Research demonstrates that investors who exit markets during downturns typically reinvest only after significant recovery has occurred, missing substantial portions of the rebound and locking in permanent losses from poor timing.

Dollar-cost averaging through continuous contributions during all market conditions implements stay-invested discipline while providing psychological comfort during downturns. Rather than experiencing declines as pure losses, investors making systematic contributions can reframe volatility as opportunities to purchase shares at discounted prices. This perspective shift—viewing downturns as sales rather than disasters—reinforces discipline by creating positive associations with periods that would otherwise trigger panic.

Historical evidence demonstrates that market timing strategies, on average, underperform simple buy-and-hold approaches by 2-4% annually after accounting for transaction costs, taxes, and missed recovery days. This performance gap compounds to massive wealth differences over multi-decade periods, representing the tangible cost of abandoning stay-invested discipline. Investors who maintain continuous market exposure accept temporary unrealized losses during downturns in exchange for capturing the full recovery and subsequent growth that historically follows every major market decline.

The stay-invested discipline extends beyond equity markets to rebalancing behavior. During the 2020 COVID-19 market crash, disciplined investors who maintained allocations or rebalanced into declining equities captured the rapid recovery that restored markets to new highs within months. Those who fled to cash or reduced equity exposure experienced permanent losses from selling low and missing the recovery, demonstrating the wealth consequences of discipline failures during peak emotional stress.

How Cost Management Supports a Disciplined Investment Approach

Cost management directly impacts long-term wealth accumulation by preserving returns that would otherwise be consumed by fees, commissions, taxes, and unnecessary trading expenses. The compounding effect of costs works against investors with the same mathematical force that compound returns work in their favor, making cost discipline essential to achieving financial goals.

Investment expense ratios ranging from 0.05% for low-cost index funds to 1.5% for actively managed funds create dramatic return differences over multi-decade periods. A $100,000 investment growing at 8% annually with 0.1% costs produces approximately $1.48 million after 30 years, while the same investment with 1.0% costs produces approximately $1.22 million—a $260,000 difference attributable solely to fees. This cost drag intensifies during lower-return environments, potentially consuming 15-25% of total returns.

Transaction costs from frequent trading compound through explicit commissions, bid-ask spreads, and market impact costs that collectively reduce portfolio values. Turnover also triggers tax consequences that convert unrealized long-term capital gains into realized short-term gains taxed at higher ordinary income rates. Research demonstrates that high-turnover portfolios underperform low-turnover alternatives by amounts approximating their excess trading costs, providing no value for the additional expenses incurred.

Tax efficiency represents a critical but often overlooked cost discipline. Investors in taxable accounts who fail to coordinate asset location, harvest tax losses, or manage withdrawal timing forfeit significant wealth to unnecessary tax payments. Tax-aware investing strategies can add 0.5-1.0% to annual after-tax returns without increasing risk, representing substantial compounding benefits over decades. Disciplined investors prioritize tax-efficient index funds in taxable accounts, hold tax-inefficient bonds in retirement accounts, and systematically harvest losses to offset gains.

Advisory fees, when not aligned with value provided, represent another cost requiring discipline. Percentage-of-assets fees on large portfolios can exceed $10,000-$50,000 annually, making it essential to evaluate whether services received justify costs incurred. Disciplined investors periodically assess advisor value, negotiate fee reductions for large account balances, or transition to lower-cost alternatives when services no longer align with needs. Robo-advisors and low-cost index providers offer sophisticated portfolio management at fractions of traditional advisory costs, providing viable alternatives for cost-conscious investors.

Platform fees, account maintenance fees, and fund minimum balance requirements create additional cost layers that disciplined investors systematically minimize by consolidating accounts, selecting no-fee platforms, and choosing funds without hidden charges. While individually small, these costs accumulate across multiple accounts and decades to meaningful amounts that reduce terminal wealth unnecessarily.

Metrics and Tools to Measure Investment Discipline

Quantifying investment discipline transforms abstract behavioral concepts into measurable metrics that enable systematic improvement and accountability. Effective discipline metrics track adherence to stated plans, identify behavioral deviations requiring correction, and provide feedback that reinforces positive habits.

Portfolio drift percentage measures the average deviation between current allocations and target allocations, quantifying rebalancing discipline. Drift is calculated by summing absolute deviations across all asset classes and dividing by the number of classes: Drift = (|Actual Stock % – Target Stock %| + |Actual Bond % – Target Bond %| + …) / Number of Asset Classes. Disciplined portfolios typically maintain drift below 3-5%, while undisciplined portfolios often exceed 10-15% as behavioral biases prevent rebalancing.

Contribution consistency tracks the percentage of planned contribution periods where intended amounts were actually invested, measuring savings discipline. A score of 100% indicates perfect adherence to planned contributions, while lower scores identify periods where discipline failures occurred. This metric highlights behavioral patterns, such as reduced contributions during market downturns driven by fear or delayed contributions during rallies while waiting for corrections.

Rebalancing frequency compliance compares actual rebalancing events against stated rebalancing schedules, identifying procrastination or inertia. Investors committed to annual rebalancing who actually rebalance only every 2-3 years demonstrate discipline failures driven by psychological discomfort with selling winners or buying losers. This metric creates accountability for following stated processes rather than rationalizing deviations.

Trading turnover relative to benchmarks measures excessive activity that increases costs without improving returns. Disciplined long-term investors typically maintain turnover below 10-20% annually, while undisciplined investors often exceed 50-100% as performance chasing, panic selling, and overconfidence drive unnecessary transactions. Comparing personal turnover to stated targets quantifies overtrading and its associated costs.

Behavioral decision scoring evaluates the quality of significant investment decisions using predefined criteria documented in Investment Policy Statements. After sufficient time passes to observe outcomes, investors review whether decisions followed stated processes, whether evidence supported actions taken, and whether emotional biases influenced choices. This retrospective analysis identifies recurring behavioral patterns—such as systematically selling during downturns or chasing recent winners—requiring targeted interventions.

Investment dashboard tools provided by modern portfolio management platforms automate many discipline metrics, displaying allocation drift, contribution patterns, fee totals, and performance attribution in visual formats that facilitate monitoring. These tools reduce the effort required to track discipline, making measurement a passive process rather than requiring manual calculation. Automated alerts when drift exceeds thresholds or contributions are missed create real-time discipline feedback that enables rapid correction.

Behavioral tracking apps and spreadsheets allow investors to log emotional states during decision points, creating data that reveals psychological patterns. Recording fear levels during downturns, confidence levels during rallies, and temptation levels when considering strategy changes produces longitudinal data showing how emotions correlate with discipline quality. This self-awareness enables targeted behavioral interventions like additional automation, commitment devices, or professional advisor engagement during predictable vulnerability periods.

Real-World Examples of Firms and Funds Practicing Investment Discipline

Real-world case studies of disciplined investment firms demonstrate how systematic processes, behavioral awareness, and long-term orientation produce superior risk-adjusted returns across complete market cycles. These examples illustrate discipline principles in action and provide benchmarks for evaluating other investment approaches.

Polen Capital Growth Fund maintains exceptional portfolio discipline through concentrated holdings (typically 20-30 companies), low turnover (often below 10% annually), and patient holding periods averaging 5-10 years. The fund’s investment philosophy emphasizes quality businesses with durable competitive advantages, strong management, and consistent earnings growth, held through normal business cycle volatility. This discipline enabled the fund to generate annualized returns exceeding 13% over multiple decades while maintaining lower volatility than broader market indices. Polen’s success demonstrates how concentrated conviction, combined with behavioral discipline to resist selling during temporary underperformance, produces long-term alpha.

Jensen Quality Growth Fund exemplifies valuation discipline through strict quality and price criteria that frequently result in significant cash positions when few companies meet investment standards. Rather than forcing capital deployment into suboptimal opportunities, Jensen maintains discipline by holding cash until attractive investments appear, even when this approach causes short-term underperformance during speculative rallies. The fund’s low turnover (typically under 15% annually) and willingness to underperform during late-stage bull markets reflect process discipline that protects capital during subsequent downturns.

Cardinal Capital Management demonstrates rebalancing discipline through systematic value investing that purchases out-of-favor stocks trading below intrinsic value and sells positions that appreciate to fair value or above. This disciplined approach requires buying when others are fearful and selling when others are greedy—emotionally challenging behaviors that systematic processes enforce without requiring heroic willpower. Cardinal’s contrarian discipline produced strong long-term returns by avoiding overvalued growth stocks during bubbles and accumulating discounted positions during market panics.

ClearBridge Investments maintains sector and style discipline through defined investment universes and systematic screening processes that prevent style drift during periods when their approach underperforms. Rather than chasing momentum or abandoning value disciplines during growth rallies, ClearBridge’s institutional framework enforces strategy consistency, allowing their approach to capture full cycle returns that justify their investment philosophy. This firm-level discipline protects against the career risk pressures that cause many managers to abandon disciplined processes during challenging periods.

Vanguard’s index fund operations demonstrate ultimate cost and tracking discipline through systematic replication of benchmark indices with minimal tracking error and exceptionally low expense ratios. By removing discretionary portfolio management and focusing on mechanical index implementation, Vanguard creates investment products that enforce buy-and-hold discipline at the fund level, preventing manager behavioral biases from undermining investor outcomes. The firm’s structure as a client-owned mutual company aligns incentives toward cost minimization and long-term investor success rather than profit maximization.

These examples share common characteristics: documented investment philosophies, systematic decision processes, low turnover, willingness to underperform during periods when their approach is out of favor, and organizational structures that support long-term discipline over short-term commercial pressures. They demonstrate that discipline requires both individual behavioral control and institutional frameworks that make disciplined behavior the path of least resistance.

Cross-Domain Lessons from Investment Discipline

Investment discipline principles transfer across domains beyond financial markets, applying to career development, skill acquisition, business building, and personal goal achievement through shared mechanisms of delayed gratification, compound benefits, and behavioral consistency.

Career capital accumulation mirrors investment discipline through systematic skill development, professional network cultivation, and strategic position selection that compounds value over decades. Just as investment discipline requires resisting short-term performance chasing in favor of long-term asset allocation, career discipline requires resisting salary maximization in early career stages in favor of learning opportunities and skill development that enable larger compensation growth over time. Professionals who systematically build rare and valuable skills through deliberate practice create career options and earning potential that far exceed those focused on immediate compensation.

Skill compounding operates through the same mathematical principles as investment returns, where abilities build upon previous capabilities to create accelerating competence. A programmer who systematically masters fundamental algorithms, data structures, and software design patterns creates a foundation that makes advanced specializations accessible, while those chasing trending technologies without foundational discipline struggle to adapt when trends shift. This compound skill effect rewards early discipline with expanding capability advantages over time.

Entrepreneurial discipline applies investment principles to business capital allocation, requiring systematic evaluation of opportunities, diversification across revenue streams or customer segments, and patient reinvestment of profits into growth initiatives with long-term payoffs. Business owners who maintain financial discipline during profitable periods—avoiding lifestyle inflation and instead reinvesting in durable competitive advantages—create compound business value similar to investment discipline’s wealth compounding. Conversely, entrepreneurs who consume all profits or chase every trend without strategic focus dissipate resources that could fund sustainable growth.

Behavioral discipline in non-financial contexts encounters identical psychological challenges: loss aversion makes cutting failed projects painful, sunk cost fallacy perpetuates resource commitment to losing initiatives, confirmation bias filters feedback to preserve current approaches, and recency bias drives overreaction to recent setbacks or successes. Recognition that these biases transcend finance enables application of investment discipline’s behavioral tools—pre-commitment devices, systematic review processes, decision journaling, and external accountability—across all goal-pursuit domains.

Habit formation frameworks from behavioral psychology apply equally to investment discipline and personal development. The cue-routine-reward loop that automates investment behaviors (cue: paycheck arrives → routine: automatic contribution → reward: portfolio growth) functions identically for professional habits (cue: workday starts → routine: focused deep work session → reward: progress on meaningful project). Understanding these mechanisms enables systematic discipline building across life domains using proven behavioral architecture principles.

Physical fitness provides particularly clear discipline analogies: consistent exercise and nutrition compound into health benefits over decades, short-term sacrifice (workout discomfort, dietary restriction) produces long-term gains, and behavioral consistency matters more than periodic heroic efforts. Fitness discipline faces identical challenges to investment discipline—temptation to quit during difficult periods, social pressure to follow trends, and difficulty maintaining motivation when progress seems slow. Solutions transfer directly: automated routines, measurable goals, tracking systems, and commitment devices.

Common Pitfalls and How to Avoid Breaking Investment Discipline

Investment discipline failures follow predictable patterns driven by cognitive biases, emotional reactions, and environmental pressures that create systematic deviations from stated plans. Understanding these pitfalls and implementing targeted countermeasures prevents wealth-destroying mistakes during vulnerable periods.

Panic selling during market downturns represents the most costly discipline failure, locking in losses and missing subsequent recoveries. During the 2008-2009 financial crisis, investors who sold equity positions between October 2008 and March 2009 crystallized losses exceeding 40-50% and many failed to reinvest until markets had recovered substantially, missing the 2009-2012 bull market. This pattern repeated during the March 2020 COVID crash, where panicked sellers exited near the bottom and missed the rapid recovery. Countermeasures include predetermined rebalancing rules that frame downturns as buying opportunities, automatic contribution continuation that prevents freeze responses, and documented Investment Policy Statements that commit to staying invested during volatility.

Performance chasing drives investors to allocate disproportionately to recent high-performers, systematically buying high after appreciation has occurred. This behavior manifests in sector rotation chasing (overweighting technology after tech rallies, overweighting energy after commodity booms) and fund selection based on trailing returns rather than process quality. The inevitable mean reversion that follows exceptional performance produces losses that exceed the gains from correctly timing rare continued outperformance. Discipline requires allocation decisions based on long-term strategic considerations rather than recent performance, typically implemented through systematic rebalancing that sells outperformers mechanically.

Overconfidence in market timing ability causes investors to hold excessive cash positions while waiting for better entry points, foregoing compound returns during waiting periods. Studies demonstrate that market timing attempts underperform invested strategies by 2-4% annually because the “right” entry point rarely arrives, and waiting costs compound. The discipline failure intensifies when cash positions are maintained through strong market rallies, creating regret and sometimes triggering subsequent performance chasing at elevated valuations. Solutions include systematic dollar-cost averaging that removes timing discretion and recognition that time in market exceeds market timing for long-term outcomes.

Recency bias creates cycles of extreme optimism following bull markets and excessive pessimism after downturns, driving systematic buy-high-sell-low behavior patterns. Investors extrapolate recent trends linearly, expecting recent returns to continue indefinitely despite overwhelming evidence of mean reversion. This bias creates the emotional foundation for bubbles and crashes, as crowds simultaneously abandon discipline based on recent experience. Countermeasures include explicit focus on valuation metrics rather than price trends, systematic rebalancing schedules that enforce contrarian behavior, and recognition that discomfort during rebalancing (selling winners, buying losers) indicates correct discipline application.

Confirmation bias prevents objective reassessment of failing positions, causing investors to selectively interpret evidence to preserve existing convictions. This bias manifests in holding losing positions too long while rationalizing negative developments, refusing to implement stop-loss disciplines, and seeking information sources that confirm rather than challenge current positions. Systematic review processes using predetermined exit criteria, independent analyst opinions, and decision journaling create accountability that breaks confirmation bias patterns.

Social pressure and herd behavior intensify during market extremes, creating powerful emotional forces that overwhelm individual discipline. During speculative manias, investors experience fear of missing out (FOMO) as colleagues, media, and social networks celebrate extraordinary gains from trending investments. During crashes, panic becomes contagious as widespread fear triggers coordinated selling. Disciplined investors recognize these social dynamics and implement behavioral distance through reduced financial media consumption during volatile periods, focus on long-term planning documents rather than short-term performance, and advisor relationships that provide objective counsel during emotional periods.

Impatience and short-term thinking undermine discipline by creating unrealistic expectations about return timelines and overreactions to normal volatility. Investors expecting linear growth become frustrated during inevitable periods of sideways movement or temporary declines, triggering premature strategy changes that prevent long-term compounding. Recognition that wealth accumulation occurs over decades rather than months, combined with focus on process metrics (contribution consistency, allocation discipline) rather than outcome metrics (quarterly performance), maintains discipline during frustrating periods.

Lifestyle inflation and consumption pressure threaten savings discipline by expanding spending in response to income increases rather than maintaining consistent savings rates as income grows. Without systematic commitment devices like automatic contribution escalations tied to raises, investors often fail to increase savings proportionally with income, reducing the rate of wealth accumulation. Solutions include automating savings rate increases parallel to income growth, separating spending accounts from investment accounts to reduce visibility of investment balances, and regular recalculation of contribution requirements to maintain goal trajectories.

Key Takeaways – How to Achieve Long-Term Financial Success Through Discipline

Investment discipline creates long-term financial success through consistent adherence to evidence-based principles that align investor behavior with mathematical realities of compounding returns, risk management, and behavioral finance. Success requires integration of goal clarity, strategic allocation, systematic processes, cost awareness, and behavioral self-regulation into cohesive frameworks that function across complete market cycles.

Clear, measurable financial goals provide direction and motivation that sustains discipline during challenging periods when emotional impulses suggest abandoning plans. Goals transform abstract investment strategies into concrete objectives with observable progress, creating feedback loops that reinforce commitment. SMART goal frameworks establish specific targets, timelines, and success criteria that guide allocation decisions and enable systematic progress monitoring.

Strategic asset allocation determines the majority of long-term returns and volatility, making allocation discipline the foundation of investment success. Disciplined allocation establishes target percentages across asset classes based on risk tolerance, time horizon, and objectives, then maintains these targets through systematic rebalancing despite market movements. This approach captures diversification benefits, prevents concentration risk, and mechanically implements buy-low-sell-high behavior without requiring market timing skill.

Staying fully invested through complete market cycles maximizes exposure to the disproportionate returns that occur during brief periods of exceptional performance impossible to predict. Missing the best 10-20 market days over multi-decade periods reduces terminal wealth by 50-75%, demonstrating the catastrophic cost of market timing attempts. Dollar-cost averaging through continuous contributions during all market conditions implements stay-invested discipline while providing psychological comfort during downturns by reframing volatility as opportunity.

Cost management preserves returns by minimizing fees, taxes, and unnecessary trading expenses that compound against investors with the same force that returns compound in their favor. Selecting low-cost index funds over expensive actively managed alternatives, coordinating asset location for tax efficiency, and harvesting tax losses systematically can add 0.5-1.5% to annual after-tax returns without increasing risk. Over decades, these cost savings compound to wealth differences exceeding hundreds of thousands of dollars for typical retirement portfolios.

Behavioral discipline prevents cognitive biases—loss aversion, recency bias, herd mentality, overconfidence, confirmation bias, and others—from triggering impulsive decisions that undermine long-term strategies. Recognition that human psychology predictably generates wealth-destroying impulses during market extremes enables implementation of countermeasures: automated processes remove discretion at vulnerable moments, Investment Policy Statements create pre-commitments that constrain emotional reactions, and systematic review processes enforce objective evaluation despite psychological pressures.

Automation transforms discipline from active choices requiring willpower into passive defaults that occur without ongoing effort. Automatic contributions, rebalancing systems, and portfolio management platforms remove decision points where discipline typically fails, making adherence the path of least resistance. This approach acknowledges that human willpower is finite and unreliable under stress, designing systems that succeed despite psychological limitations rather than depending on heroic self-control.

Measurement and tracking quantify discipline through metrics that transform abstract behavioral concepts into observable data enabling improvement. Portfolio drift percentage, contribution consistency, rebalancing frequency, and turnover relative to targets provide feedback that identifies discipline failures and reinforces positive behaviors. Regular metric review—quarterly or annually—creates accountability loops that systematically improve adherence over time.

Professional guidance from fiduciary advisors aligned with long-term client success can reinforce individual discipline by providing objective counsel during emotional periods, implementing systematic processes, and maintaining accountability for stated commitments. Effective advisor relationships establish shared understanding of values, objectives, and acceptable trade-offs, enabling advisors to remind clients of their own stated priorities when behavioral impulses suggest deviations.

Long-term financial success ultimately derives from recognizing that investment discipline is not optional or secondary to strategy selection—discipline IS the strategy. Technical allocation decisions, security selection, and timing considerations matter far less than consistent adherence to sound principles over decades. Investors who maintain disciplined behavior with mediocre technical strategies typically outperform those with sophisticated strategies undermined by behavioral failures. This reality suggests that energy devoted to improving discipline—through better habits, stronger commitment devices, reduced exposure to emotional triggers, and systematic processes—produces higher returns on effort than energy devoted to finding marginally superior investment products or market timing systems.

Final Note: Investment discipline does not guarantee profits, eliminate market risk, or prevent temporary losses. Markets remain inherently uncertain, and disciplined investors experience portfolio volatility during downturns equally with undisciplined investors. The critical difference emerges in behavioral responses: disciplined investors maintain strategies through volatility, capturing eventual recoveries and long-term compound growth, while undisciplined investors abandon strategies at market bottoms, locking in permanent losses. This behavioral distinction, compounded over decades, creates the wealth gap between successful and unsuccessful investors despite exposure to identical market conditions.