Table of Contents

Contents are generated from article headings.

Fear and greed are the two dominant emotional forces that shape financial decisions across all income levels, investment types, and economic conditions. Fear and greed do not operate as occasional disruptions to otherwise rational financial behavior — they function as persistent, opposing forces that systematically bias financial choices toward extremes. Understanding how fear and greed influence money choices is essential for recognizing when emotional intensity, rather than objective analysis, is driving a financial decision.

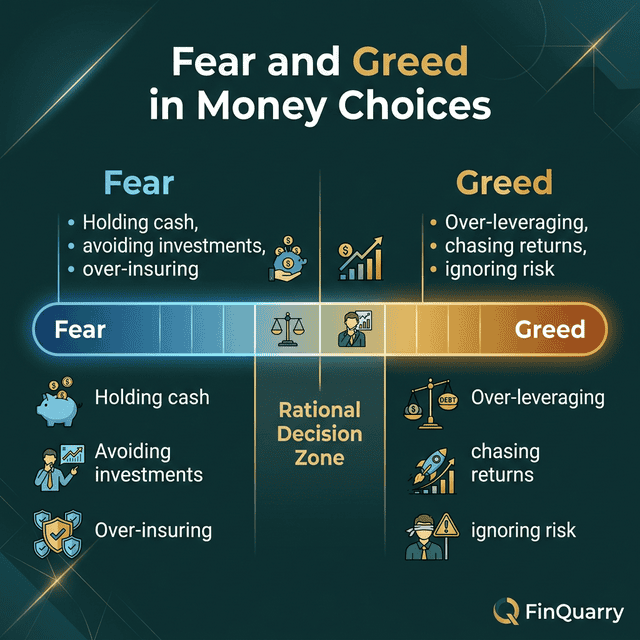

Fear drives financial decisions toward excessive caution — selling investments during downturns, hoarding cash, avoiding any exposure to risk. Greed drives financial decisions toward excessive risk — chasing speculative returns, ignoring diversification, over-leveraging. Neither emotional extreme produces optimal financial outcomes. The most damaging financial decisions typically occur at the points of maximum emotional intensity: peak fear drives panic selling at market bottoms, while peak greed drives euphoric buying at market tops.

Scope and Context: This content discusses behavioral finance principles and market psychology using academic research, regulatory publications, and historical market data. Financial regulations, investment products, and consumer protections vary by jurisdiction and institution. Research findings cited reflect conditions as of their publication dates; market dynamics are historically consistent but past patterns do not guarantee future outcomes. Readers should evaluate strategies in the context of their own financial circumstances and consult qualified financial professionals for personalized advice.

The Neurological Basis of Fear and Greed in Financial Decisions

Fear and greed are not abstract concepts in the context of financial decision-making — they are neurological states that alter how the brain processes risk, reward, and uncertainty. Understanding the brain mechanisms behind these emotions explains why even financially sophisticated people make emotion-driven money choices.

How Fear Activates the Threat Response System

Financial fear activates the amygdala — the brain structure responsible for detecting threats and initiating the fight-or-flight response. When a person observes a portfolio declining in value, receives an unexpected bill, or hears alarming economic news, the amygdala triggers a cascade of physiological responses: elevated cortisol, increased heart rate, narrowed attention, and a cognitive shift from analytical processing to reactive processing.

This threat response evolved to handle physical dangers — predators, environmental hazards, conflict — where rapid reaction often determines survival. Financial threats, however, rarely require the speed that the amygdala prioritizes. A declining stock portfolio does not require a decision within seconds, but the amygdala responds to financial loss signals with the same urgency it applies to physical threats. This mismatch between the speed of the threat response and the time horizon of financial decisions is a primary mechanism through which fear distorts money choices. Understanding this mechanism is foundational to money psychology and explains why individuals with substantial financial knowledge still make fear-driven decisions.

How Greed Activates the Reward System

Greed operates through the brain’s dopamine reward system — the same circuitry that produces pleasure from food, social connection, and novelty. When a person anticipates financial gain — watching an investment rise, imagining future wealth, hearing about someone else’s profitable trade — the brain releases dopamine, which creates a feeling of pleasure and motivation to pursue more of the same stimulus.

The dopamine system has a critical feature relevant to financial behavior: it responds more strongly to anticipated rewards than to received rewards, and it escalates its demands over time (a process called tolerance). This means that the emotional intensity of greed tends to increase as gains accumulate — a person who has made money feels compelled to make more, with each successive gain producing less satisfaction and requiring larger gains to reproduce the same emotional reward. This escalation dynamic explains why speculative bubbles accelerate rather than self-correct: greed intensifies precisely when rational analysis would suggest increasing caution.

The Fear-Greed Cycle in Financial Markets

Fear and greed do not operate independently — they function as a cycle that drives predictable patterns in both individual financial behavior and collective market movements. Understanding this cycle provides a framework for recognizing when emotional forces, rather than fundamental analysis, are driving market conditions and personal financial decisions.

The Stages of the Market Emotion Cycle

The market emotion cycle maps the psychological states that investors collectively experience as asset prices rise and fall. The complete cycle moves through identifiable stages:

Accumulation phase: Following a market downturn, prices stabilize at levels below intrinsic value. Fear is the dominant emotion, and most investors avoid buying. The few investors who act during this phase — buying while fear keeps others away — typically capture the largest gains when the cycle eventually turns.

Growth phase: As prices begin to rise, optimism replaces fear. Early gains attract attention, and media coverage shifts from negative to positive. Investors who missed the initial recovery begin entering the market, driven by a combination of optimism and the emerging concern that they may be “missing out.”

Euphoria phase: Sustained gains produce widespread confidence that escalates into euphoria. Greed becomes the dominant emotion. Investors abandon caution, ignore diversification principles, and take on leverage to maximize exposure to rising prices. Historical examples include the dot-com bubble peak in early 2000, the housing bubble peak in 2006–2007, and various cryptocurrency bubbles. During euphoria phases, prices typically exceed any defensible valuation based on fundamentals — a condition that is visible in retrospect but obscured by emotional intensity in real time.

Correction and panic phase: When prices begin to decline, euphoria converts rapidly to anxiety and then to fear. The speed of emotional transition is asymmetric — fear builds faster than greed — because loss aversion makes losses feel approximately twice as painful as equivalent gains feel pleasurable, as established by Kahneman and Tversky’s prospect theory. As losses mount, fear escalates to panic, driving investors to sell at prices that would have looked like bargains months earlier.

Capitulation phase: At the bottom of the cycle, fear reaches its maximum intensity. Investors who held through the decline sell at the worst possible prices, driven by the emotional need to end the pain of watching further losses. The DALBAR Quantitative Analysis of Investor Behavior (QAIB) has documented this pattern quantitatively: the average equity fund investor earned 16.54% in 2024 compared to the S&P 500’s 25.02% return, an 8.48 percentage-point gap attributable primarily to emotionally timed buying and selling — extending a 15-consecutive-year streak of individual investor underperformance.

This cycle then resets as accumulation begins again. The Financial Crisis Inquiry Commission’s 2011 report documented how this cycle operated during the 2008 financial crisis, identifying herd behavior amplified by fear and greed among both institutional and retail investors as contributing factors.

Why the Cycle Repeats

The fear-greed cycle repeats because each generation of investors believes their situation is fundamentally different from previous cycles — a cognitive bias known as the “this time is different” fallacy. Additionally, the cycle is self-reinforcing at its extremes: during euphoria phases, investors who remain cautious experience social and psychological pressure (fear of missing out), while during panic phases, investors who remain invested experience isolation and doubt (fear of further loss).

How Fear Distorts Specific Financial Decisions

Fear affects financial decisions beyond investment markets. Understanding the specific mechanisms through which fear operates across different financial contexts reveals opportunities for structural countermeasures.

Loss Aversion and Portfolio Paralysis

Loss aversion — the tendency to weigh potential losses more heavily than equivalent potential gains — is the most well-documented fear-based bias in financial decision-making. Kahneman and Tversky’s research, synthesized in Kahneman’s Thinking, Fast and Slow (2011), established that losses feel approximately twice as intense as equivalent gains, though the exact ratio varies by context.

Loss aversion produces portfolio paralysis: the inability to make investment changes because any potential loss feels disproportionately threatening. An investor who holds a declining stock position — refusing to sell and reallocate — is exhibiting the disposition effect, a direct consequence of loss aversion. The investor is not making a rational judgment about the stock’s future potential; they are avoiding the psychological pain of realizing a loss. This same mechanism explains why people experiencing financial anxiety often keep excessive cash reserves in low-yield accounts rather than investing in diversified portfolios with higher expected returns.

Fear-Driven Financial Avoidance

Financial fear can manifest as complete avoidance of financial engagement — refusing to check account balances, ignoring bills, postponing financial planning conversations, or declining to open retirement accounts. Financial avoidance differs from procrastination: procrastination involves delaying a task that the person intends to complete, while avoidance involves actively evading a task because engagement with it produces anxiety.

Financial avoidance based on fear produces compounding negative consequences. An unopened bill incurs late fees. An unmonitored account may suffer unauthorized charges. An unopened retirement account means years of foregone compounding. Each avoided task grows in magnitude while being ignored, making the eventual confrontation more distressing and reinforcing the avoidance pattern.

Fear of Missing Out (FOMO) as Inverted Fear

Fear of missing out (FOMO) represents a distinct category where fear and greed converge. FOMO is technically a fear response — fear of being excluded from gains that others are capturing — but it drives greed-like behavior: impulsive buying, abandonment of investment strategy, and excessive risk-taking. FOMO is particularly powerful during the late growth and euphoria phases of the market emotion cycle, when social media, news coverage, and peer conversations amplify the visibility of other people’s gains.

FOMO-driven decisions are among the most reliably destructive in personal finance because they cause people to enter investments at their most expensive — after gains have already occurred — while simultaneously abandoning the diversification and risk management principles that protect against the inevitable correction.

How Greed Distorts Specific Financial Decisions

Greed-driven financial decisions share a common characteristic: they prioritize maximum return over risk management, treating potential gains as certain while treating potential losses as unlikely. This asymmetric risk assessment is a cognitive distortion, not a rational strategy.

Overconfidence and Excessive Trading

Greed produces overconfidence — the belief that one’s ability to predict financial outcomes exceeds what evidence supports. Overconfident investors trade more frequently, maintain less diversified portfolios, and hold more extreme positions than their information would justify. Behavioral finance research from Brad Barber and Terrance Odean, published in the Journal of Finance (2000), demonstrated that individual investors who traded most actively earned significantly lower net returns than those who traded least — a finding they titled “Trading Is Hazardous to Your Wealth.”

The mechanism is straightforward: each trade incurs transaction costs, and the selection of which assets to buy and sell is driven more by emotional conviction than by information advantage. Greed intensifies trading frequency by making each potential trade feel like an opportunity that cannot be missed — the same urgency mechanism that drives emotional spending in consumer contexts.

Leverage and Amplified Risk

Greed drives the use of financial leverage — borrowing money to increase investment exposure. Leverage amplifies both gains and losses proportionally, but greed biases the person’s assessment toward the gains side of the equation. A person using 2:1 leverage on a stock position doubles their gains if the stock rises but also doubles their losses if it falls. Under the influence of greed, the potential for doubled gains feels vivid and probable, while the potential for doubled losses feels abstract and unlikely.

Leverage-driven losses are disproportionately common during market transitions — the moment when euphoria converts to anxiety — because leveraged positions face margin calls that force selling at precisely the worst moment. This timing amplifies the fear-greed cycle: greed drives leverage during euphoria, and fear drives forced liquidation during correction.

Speculation Versus Investment

The distinction between speculation and investment often reduces to the influence of greed on the decision-making process. Investment involves allocating capital based on analysis of fundamental value, expected returns, and risk-adjusted outcomes over a defined time horizon. Speculation involves allocating capital based on the expectation that prices will rise because other people will pay more in the future — regardless of underlying value.

Greed converts investors into speculators by shifting focus from “What is this asset worth?” to “How much higher will the price go?” This shift is particularly visible in asset classes with limited fundamental valuation frameworks — including cryptocurrency, collectibles, and initial public offerings — where price momentum becomes the primary basis for purchase decisions. Research from the Consumer Financial Protection Bureau has documented that speculative financial products marketed during periods of greed-driven enthusiasm disproportionately harm less experienced investors.

Structural Strategies for Managing Fear and Greed

Awareness of fear and greed is necessary but insufficient for managing their effects on financial decisions. Effective management requires structural interventions that reduce the influence of emotional extremes on action.

Rules-Based Systems and Emotional Circuit Breakers

Rules-based financial systems — predefined investment strategies, automatic rebalancing schedules, predetermined buy/sell criteria — function as emotional circuit breakers that interrupt the fear-greed cycle before it reaches decision-altering intensity. A person who has predetermined that they will not sell any investment unless their original investment thesis has fundamentally changed has a structural defense against panic selling during market downturns.

Similarly, a person who has established that they will not invest more than a predetermined percentage of their portfolio in any single asset has a structural defense against greed-driven concentration.

Dollar-Cost Averaging as a Fear-Greed Neutralizer

Dollar-cost averaging — investing a fixed amount at regular intervals regardless of market prices — is structurally designed to neutralize the timing effects of fear and greed. By investing regardless of price, dollar-cost averaging ensures that market entries are distributed across various emotional phases rather than concentrated at emotional extremes.

Dollar-cost averaging is particularly effective for people who recognize their susceptibility to market timing impulses. It converts the question “Is now a good time to invest?” — which triggers fear-greed analysis — into the statement “I invest on this date every month” — which requires no emotional evaluation.

The Role of Financial Advisors as Behavioral Buffers

Financial advisors serve a behavioral function that extends beyond portfolio construction and tax optimization. An advisor acts as a buffer between the investor’s emotional state and their financial actions — providing a deliberation step between the impulse to act and the execution of a trade. This buffer function is particularly valuable during periods of extreme fear or extreme greed, when emotionally driven decisions are most likely and most costly.

The Financial Therapy Association recognizes the intersection of emotional and financial decision-making, maintaining a directory of practitioners trained to address both dimensions. For individuals whose fear or greed patterns produce recurring negative financial outcomes, the combination of behavioral intervention and financial planning may be more effective than either approach alone.

What Is the Fear and Greed Index?

The Fear and Greed Index, most commonly associated with CNN Business, is a market sentiment indicator that aggregates seven factors — including market momentum, stock price strength, put-call ratio, market volatility (VIX), junk bond demand, safe haven demand, and stock price breadth — to produce a single score between 0 (extreme fear) and 100 (extreme greed). The index is designed to quantify the emotional state of market participants at any given time, providing a contrarian signal: extreme fear readings often coincide with market bottoms (potential buying opportunities), while extreme greed readings often coincide with market tops (potential selling opportunities). The index does not predict specific price movements but serves as a behavioral awareness tool.

Can a Person Eliminate the Influence of Fear and Greed on Financial Decisions?

Fear and greed cannot be eliminated from financial decision-making because they are fundamental features of human neurology — the amygdala and dopamine reward system are structural components of the brain, not software that can be updated. However, the influence of fear and greed on financial outcomes can be substantially reduced through structural interventions (automated investing, predefined rules, diversification), behavioral awareness (recognizing emotional states before acting on them), and professional support (financial advisors and financial therapists who provide an external perspective during periods of emotional intensity).

How Does Social Media Amplify Fear and Greed in Financial Decisions?

Social media amplifies fear and greed through three mechanisms: speed (financial news and market movements are communicated instantly), selectivity (people share gains more than losses, creating a distorted picture of investment outcomes), and social proof (visible consensus creates pressure to conform to either the fearful or the greedy narrative). These mechanisms increase the frequency and intensity of emotional triggers while reducing the deliberation time between trigger and action.

What Historical Events Demonstrate the Fear-Greed Cycle?

Major historical examples of the fear-greed cycle include the Dutch Tulip Mania (1637), the South Sea Bubble (1720), the 1929 stock market crash, the dot-com bubble (1995–2001), the 2008 financial crisis, and multiple cryptocurrency booms and busts (2017–2018 and 2021–2022). Each event followed the same emotional sequence: early adoption driven by genuine value, greed-driven escalation beyond fundamental value, a triggering event that converted greed to fear, and panic-driven selling that produced losses concentrated among late entrants.