Table of Contents

Contents are generated from article headings.

A stark divergence is emerging in the global credit and payments landscape this month. While consumer borrowing shows distinct signs of fatigue amid lingering macroeconomic headwinds, the B2B fintech sector—specifically corporate spend management—is experiencing a massive influx of capital and strategic consolidation.

For financial professionals, CFOs, and fintech observers, the data highlights a clear shift: the market is currently rewarding platforms that optimize existing corporate capital over those reliant on consumer credit expansion.

Consumer Credit: Revolving Debt Contracts

The latest data from the Federal Reserve reveals a cautious American consumer. While total consumer credit increased at a seasonally adjusted annual rate of 1.9% in January (reaching $5.11 trillion), the underlying metrics tell a different story.

- Revolving Credit Decline: Revolving credit, which largely reflects credit card debt, decreased at an annual rate of 4.3%.

- Non-Revolving Growth: Non-revolving credit (such as student and auto loans) increased by 1.1%, heavily supported by Federal government holdings.

This consumer hesitation is mirrored by institutional sentiment. The American Bankers Association’s (ABA) latest Credit Conditions Index remained soft at 37.5 for Q1 2026. Because any reading below 50 indicates an expected deterioration, this marks the fifth consecutive quarter that bank economists anticipate weakening credit conditions, citing persistent inflation and subdued labor growth.

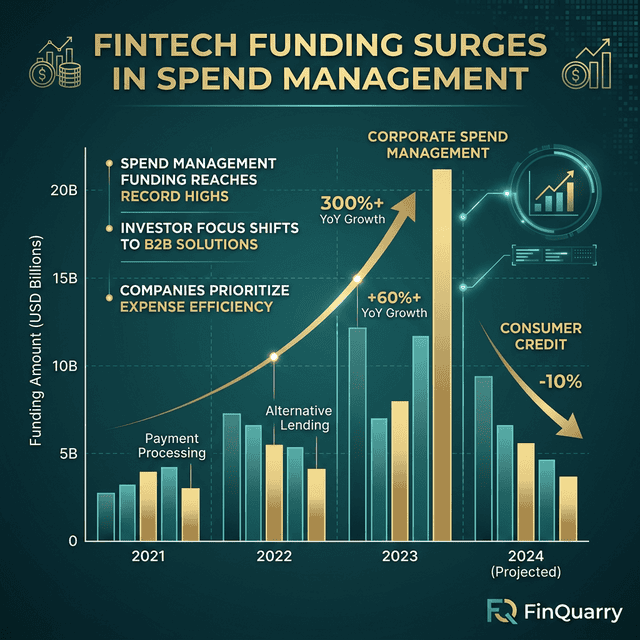

The B2B Boom: Capitalizing on Efficiency

In sharp contrast to the consumer sector, B2B fintechs specializing in corporate spend management, treasury, and embedded finance are successfully raising capital and forming aggressive global partnerships. As borrowing costs remain a focus, enterprises are turning to software to automate accounts payable, enforce expense policies, and generate yield on idle cash.

Key market moves in March 2026 underscore this momentum:

- European Expansion: Swedish fintech Mynt closed a €22 million Series B round to scale its API-based spend management platform. Rather than just issuing cards, Mynt is embedding its infrastructure directly into ERPs and traditional banks.

- Latin American Growth: Clara secured $70 million in debt financing from BBVA Spark and the IFC. The capital will fuel the expansion of its corporate credit card and bill-pay ecosystem across Mexico and Colombia.

- Strategic Consolidation: Global payments giant Adyen announced partnerships with Medius and Mesh Payments. This move pushes Adyen beyond standard merchant acquiring and directly into the CFO’s workflow, tying corporate card issuance to cashback rewards and cross-border expense management.

The Shift to the “Always-On” Treasury

The unifying theme across these B2B developments is the shift toward an “always-on” treasury. Businesses are increasingly demanding real-time liquidity management and borderless capital access. Fintechs that combine corporate cards with automated workflows and real-time cross-border settlements are proving highly resilient, even as the broader venture capital market normalizes from its past peaks.

Ultimately, while the retail consumer is actively working to pay down expensive revolving debt, corporate finance teams are doubling down on platforms that promise operational efficiency and granular spend control.