Table of Contents

Contents are generated from article headings.

Financial anxiety is a persistent emotional response to real or perceived threats to a person’s financial security. Financial anxiety affects how people spend, save, invest, and plan — not through rational recalculation but through stress-driven cognitive shifts that systematically alter financial behavior. Understanding the mechanism that connects financial anxiety to money behavior is the first step toward interrupting patterns that compound financial stress rather than resolve it.

Financial anxiety is not simply “worrying about money.” Financial anxiety activates the same neurological stress pathways — the hypothalamic-pituitary-adrenal (HPA) axis and the amygdala-mediated threat response — that evolved to handle physical danger. When these systems activate in response to financial uncertainty, they shift cognitive processing from deliberate analysis to reactive, emotion-driven decision-making. This shift explains why financially anxious people often make choices that contradict their own stated goals: the brain is prioritizing immediate threat reduction over long-term financial optimization.

Scope and Context: This content discusses financial anxiety and its effects on financial behavior using peer-reviewed psychological research, government survey data, and established behavioral finance frameworks. Financial regulations, consumer protections, and available mental health resources vary by jurisdiction and institution. Research findings cited reflect conditions as of their publication dates; readers should evaluate strategies in the context of their own financial situation, local services, and current economic conditions.

How Widespread Is Financial Anxiety?

Financial anxiety affects a majority of adults across income levels, age groups, and geographic regions. The scale of the problem determines why financial anxiety is a systemic behavioral driver, not a personal failing limited to people with low incomes.

Survey Data on Financial Stress Prevalence

The American Psychological Association’s “Stress in America 2024” survey found that money is a significant source of stress for 64% of U.S. adults, with the economy cited as a stressor by 73% of adults. Financial stress disproportionately affects younger demographics: 66% of adults aged 18–25 and 69% of those aged 26–39 identified money as a significant stressor.

The scope extends beyond the United States. A Bankrate survey conducted in March 2024 found that 47% of U.S. adults reported that money negatively impacts their mental health. The CFPB’s “Making Ends Meet in 2024” report documented a decline in overall financial well-being from a score of 51.0 in 2023 to 48.7 in 2024 on the CFPB’s 100-point scale, with 43% of families reporting difficulty paying bills — up from 38% in 2023. A Northwestern Mutual study released in 2025 found that 69% of Americans believe personal financial uncertainty contributes to feelings of depression and anxiety, an increase from 61% in 2023.

These numbers establish that financial anxiety is a normative experience — the majority of adults report it — which means that money psychology must account for anxiety as a baseline condition rather than an exception.

Who Is Most Affected by Financial Anxiety?

Financial anxiety does not affect all demographics equally. Younger adults — particularly Gen Z and Millennials — report the highest rates of financial anxiety, driven by factors including student debt, housing affordability challenges, and economic uncertainty during formative career years. According to a 2025 survey by Included Health, 71% of Gen Z and 68% of Millennials reported experiencing financial anxiety, compared to lower but still significant rates among Gen X (69%) and Baby Boomers.

Lower-income households experience financial anxiety at disproportionately high rates, but financial anxiety is not exclusive to lower incomes. Middle- and upper-income individuals also report significant financial stress, often driven by lifestyle inflation, fear of income loss, and the psychological pressure of maintaining financial obligations that scale with earnings. This distribution pattern demonstrates that financial anxiety is a psychological phenomenon influenced by — but not determined by — objective financial conditions.

How Financial Anxiety Alters Spending Behavior

Financial anxiety does not simply cause people to spend less. Anxiety reshapes spending behavior in complex, often contradictory ways — simultaneously driving excessive caution in some areas and impulsive spending in others.

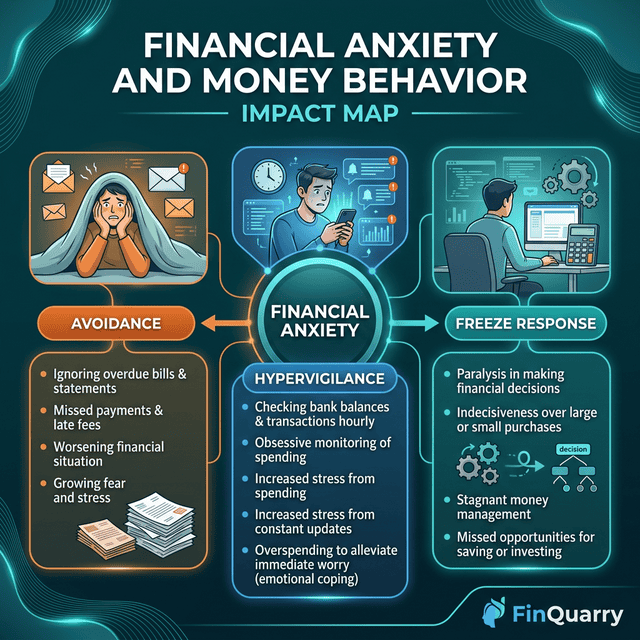

Avoidance Spending and Financial Paralysis

Financial anxiety frequently manifests as financial avoidance — the deliberate postponement or evasion of financial decisions because engaging with them produces emotional distress. A person experiencing financial avoidance may ignore bills, delay opening bank statements, avoid checking account balances, or refuse to create a budget — not because they are unaware of the importance of these actions but because the act of confronting financial reality triggers anxiety that the brain interprets as a threat to be avoided.

Financial avoidance creates a compounding cycle: avoiding financial decisions prevents the person from addressing manageable problems before they escalate, which produces larger financial consequences, which generates more anxiety, which reinforces the avoidance behavior. This cycle explains why people sometimes describe “suddenly” discovering they are in severe debt — the debt accumulated gradually during an avoidance period that felt psychologically necessary but was financially destructive.

Stress-Triggered Spending and Emotional Compensation

Paradoxically, financial anxiety also drives increased spending through a mechanism called emotional compensation. When financial stress becomes chronic, the brain seeks dopamine-driven relief through activities that provide immediate reward — and purchasing is one of the most accessible dopamine triggers in a consumer environment. This mechanism is the core driver behind emotional spending, where purchases serve a psychological function rather than a practical one.

Stress-triggered spending is particularly damaging because it operates in direct opposition to the person’s financial goals. A person who is anxious about not having enough savings may spend impulsively to temporarily relieve that anxiety, which further depletes savings, which intensifies the anxiety — creating a self-reinforcing cycle. Research from a LendingTree survey on emotional spending documented that approximately 50% of emotional spenders identify stress as their primary spending trigger.

How Anxiety Affects Purchasing Decisions

Financial anxiety systematically distorts the cognitive processes involved in purchasing decisions. Under anxiety conditions, consumers tend to:

- overweight the certainty of immediate costs while underweighting the probability of future benefits, leading to underinvestment in preventive measures (insurance, maintenance, health care)

- anchor more heavily to price rather than value, choosing cheaper options that may cost more over time due to lower durability or effectiveness

- exhibit choice paralysis when facing multiple options, defaulting to inaction or the most familiar choice rather than conducting comparative analysis

- engage in “doom spending” — purchasing items as a response to perceived hopelessness about the future, particularly observed among younger adults during periods of economic uncertainty

These patterns demonstrate that financial anxiety does not produce a single behavioral response. Instead, anxiety disrupts the balance between System 1 (fast, emotional) and System 2 (slow, analytical) processing described in how psychology affects financial decisions, with different manifestations depending on the individual’s coping style, financial literacy, and environmental context.

How Financial Anxiety Undermines Saving and Investment

Financial anxiety creates specific obstacles to saving and investing that operate differently from the obstacles created by insufficient income. Even people with adequate income to save often fail to do so when financial anxiety is present, because anxiety distorts the psychological calculations involved in deferred gratification.

The Anxiety-Savings Paradox

One of the most counterintuitive effects of financial anxiety on behavior is the anxiety-savings paradox: people who are most anxious about financial security are often the least likely to take actions that would improve it. This paradox occurs because saving requires tolerating the short-term discomfort of reduced spending in exchange for future security — and financial anxiety reduces the brain’s capacity for exactly this type of delayed-reward processing.

The CFPB’s 2024 data showed that financial well-being deteriorated across demographic groups, with more households reporting an inability to cover one month of expenses if they lost their primary income source. Meanwhile, the Federal Reserve’s Survey of Household Economics and Decision-making has consistently documented that a significant percentage of Americans — roughly 27% in October 2024 — describe their financial situation as “just getting by” or “finding it difficult to get by,” a state that simultaneously makes saving urgent and psychologically difficult.

Why Anxious Investors Underperform

Financial anxiety produces specific investment behaviors that reduce long-term returns. Anxious investors tend to sell during market downturns (crystallizing temporary losses into permanent ones), avoid re-entering markets after downturns (missing the recovery), maintain excessively conservative allocations that fail to keep pace with inflation, and check portfolio values with a frequency that increases emotional reactivity without improving decision quality.

The behavioral mechanism connecting anxiety to investment underperformance involves fear of losing money, which activates loss aversion — the tendency to weigh potential losses approximately twice as heavily as equivalent potential gains. Under conditions of financial anxiety, loss aversion intensifies, making any investment risk feel intolerable even when the expected return justifies the risk. This dynamic explains why financially anxious people often keep large cash reserves in savings accounts earning below the inflation rate: the psychological comfort of capital preservation outweighs the mathematical reality that inflation is eroding purchasing power.

The Neurological Basis of Financial Anxiety

Understanding why financial anxiety produces irrational financial behavior requires examining the neurological mechanisms that connect stress to decision-making. Financial anxiety is not a character flaw or a knowledge deficit — it is a neurological state that physically alters how the brain processes financial information.

Cortisol, the Prefrontal Cortex, and Decision Quality

Chronic financial stress elevates cortisol — the body’s primary stress hormone — on a sustained basis. Elevated cortisol impairs the prefrontal cortex, the brain region responsible for executive functions including planning, impulse control, working memory, and cost-benefit analysis. Simultaneously, elevated cortisol increases activity in the amygdala, which processes threat detection and emotional responses.

This neurological shift means that a person under chronic financial stress is literally processing financial information with a different brain configuration than a person who is financially calm. The stressed brain prioritizes threat avoidance over opportunity evaluation, short-term safety over long-term gain, and familiar options over novel ones — even when the novel option would produce better financial outcomes. This explains why people make irrational money decisions under stress that they would not make in calm conditions.

The Scarcity Mindset and Cognitive Bandwidth

Research by Sendhil Mullainathan and Eldar Shafir, documented in their book Scarcity: Why Having Too Little Means So Much (2013), demonstrated that financial scarcity — whether real or perceived — consumes cognitive bandwidth. Their research showed that financial worry occupies working memory, reducing the mental resources available for other cognitive tasks by an amount equivalent to losing approximately 13 IQ points.

This “bandwidth tax” means that people experiencing financial anxiety have fewer cognitive resources available for the complex reasoning that budgeting, investment analysis, and long-term financial planning require. The bandwidth tax is not a metaphor — it is a measurable reduction in cognitive performance that affects financial decisions, work productivity, parenting, and health behaviors simultaneously.

Breaking the Cycle: Evidence-Based Approaches to Financial Anxiety

Reducing the impact of financial anxiety on money behavior requires interventions that address both the psychological roots and the structural environment of financial decision-making. Knowledge-based interventions alone are insufficient because financial anxiety impairs the cognitive processes needed to apply financial knowledge.

Automation as an Anxiety-Reduction Strategy

Automation-based financial strategies are particularly effective for people with financial anxiety because they remove the decision point where anxiety would otherwise interfere. Automated savings transfers, automatic bill payments, and auto-enrollment in employer retirement plans all work by making the financially beneficial action the default — requiring effort to stop the positive behavior rather than effort to start it.

Research by Brigitte Madrian and Dennis Shea demonstrated that automatic enrollment in retirement plans increases participation from approximately 60% to over 90%. For people with financial anxiety, this kind of automation is especially valuable because it bypasses the avoidance behavior that anxiety produces.

Financial Therapy and Professional Support

When financial anxiety produces persistent patterns of avoidance, emotional spending, relationship conflict, or impaired daily functioning, professional intervention may be appropriate. Financial therapy — a specialized discipline that integrates psychological techniques with financial planning — addresses the emotional roots of financial behavior rather than treating money management as a purely mathematical exercise.

The Financial Therapy Association maintains a directory of practitioners trained in both psychological and financial disciplines. Professional support is particularly valuable when financial anxiety co-occurs with anxiety disorders, depression, or trauma-related conditions, as these clinical factors amplify the behavioral effects of financial stress.

Graduated Exposure and Financial Engagement

Cognitive behavioral approaches to financial anxiety include graduated exposure — systematically increasing engagement with financial tasks in manageable increments. A person experiencing financial avoidance might begin by checking their bank balance once per week, then progress to reviewing monthly statements, then to actively categorizing expenses, and finally to creating and maintaining a budget.

Graduated exposure works because it breaks the avoidance cycle without overwhelming the anxiety response. Each successful engagement with a financial task produces evidence that the feared outcome (emotional distress) is manageable, gradually reducing the anxiety associated with financial engagement.

What Is the Difference Between Financial Anxiety and Financial Stress?

Financial stress is a normal response to specific, identifiable financial pressures such as an unexpected expense, job loss, or debt obligation. Financial anxiety is a more persistent, generalized state of worry about financial security that may not be proportional to actual financial circumstances. A person can experience financial anxiety even when their objective financial situation is stable, because anxiety is driven by perceived threats and catastrophic thinking patterns rather than by current financial reality. Both states affect financial behavior, but anxiety tends to produce more chronic and pervasive behavioral distortions than situational stress.

Can Financial Anxiety Affect Physical Health?

Financial anxiety produces measurable physical health effects through the sustained activation of the body’s stress response system. Chronic financial stress has been linked to sleep disorders, cardiovascular strain, headaches, digestive problems, weight fluctuations, and weakened immune function. The APA’s Stress in America research consistently identifies money as one of the top sources of stress affecting Americans’ physical and mental health. These health effects can themselves create additional financial burden through medical costs and reduced work capacity, establishing a feedback loop between financial anxiety and physical well-being.

Does Financial Literacy Reduce Financial Anxiety?

Financial literacy can reduce certain components of financial anxiety — particularly anxiety driven by uncertainty about how financial systems work or what financial options are available. However, financial literacy alone does not eliminate financial anxiety because anxiety is primarily an emotional and neurological response, not a knowledge deficit. A person can understand compound interest, asset allocation, and budgeting principles intellectually while still experiencing anxiety that impairs their ability to apply that knowledge. The most effective approaches combine financial education with psychological techniques that address the emotional dimension of money behavior.

When Should a Person Seek Professional Help for Financial Anxiety?

Professional help may be appropriate when financial anxiety produces persistent avoidance of financial responsibilities, recurring emotional spending patterns that create debt, relationship conflict over money, difficulty sleeping due to financial worry, or impaired work performance. If financial anxiety is accompanied by symptoms of clinical anxiety or depression — including persistent worry, difficulty concentrating, irritability, or feelings of hopelessness — a mental health professional can help determine whether an anxiety disorder is amplifying the financial stress response. Financial therapy specifically addresses the intersection of emotional and financial well-being.