Table of Contents

Contents are generated from article headings.

Fear of losing money is a psychological response to potential financial loss that influences how people spend, save, invest, and make career decisions. This fear exists because humans perceive losses more intensely than equivalent gains, a phenomenon studied extensively in behavioral finance research.The fear affects financial decisions by triggering avoidance behaviors. People may hold excessive cash, avoid investing, panic-sell during market downturns, or stay in unsatisfying jobs to maintain income security.

Critical distinction: Fear of losing money focuses on avoiding loss, not creating wealth. This defensive orientation often conflicts with long-term wealth-building strategies that require accepting calculated risks.This article explains the psychological mechanisms behind financial loss fear, how this fear affects observable behaviors, when fear serves protective purposes versus when it becomes financially harmful, and evidence-based approaches to managing fear without ignoring legitimate risks.

Scope Note: This content explains the psychological and behavioral mechanisms behind fear of financial loss using general principles from behavioral finance and psychology. Individual experiences, financial outcomes, and risk tolerance vary by personal circumstances, financial systems, and market conditions. This guidance is educational, not financial or psychological advice.

What Is the Fear of Losing Money?

Fear of losing money is an emotional and cognitive response to anticipated financial loss that occurs before any actual loss happens. This fear drives protective but often suboptimal financial behaviors across spending, saving, and investing decisions.

Definition in Personal Finance Context

Fear of financial loss represents anxiety about potential future loss rather than response to losses already realized. The fear activates when people imagine scenarios where their wealth decreases.

Key distinction: Anticipated loss creates fear. Realized loss creates regret. These are different psychological states requiring different responses.

Anticipated loss triggers avoidance behaviors before decisions are made. Realized loss triggers coping behaviors after outcomes occur.

The fear of losing money in personal finance manifests as reluctance to take actions that could reduce current wealth, even temporarily. This includes avoiding stock market investing, excessive emergency fund building, or career stagnation.

How This Fear Differs From Being Financially Unstable

Having insufficient income or facing financial hardship is a condition, not a fear. Fear of losing money is a psychological state that can exist regardless of actual financial position.

High-income individuals often experience intense fear of financial loss despite objectively secure positions. Income level does not eliminate loss sensitivity.

Financial instability: Current inadequate resources to meet obligations and needs.

Fear of losing money: Anticipatory anxiety about potential future resource reduction, independent of current financial adequacy.

People experiencing financial instability may or may not fear losing money. Conversely, financially secure individuals may experience paralyzing fear of loss.

The fear originates from perceived vulnerability, not actual vulnerability. This explains why wealth accumulation alone rarely eliminates the fear entirely.

What Fear of Losing Money Is NOT

Fear of losing money is not identical to risk aversion, though the concepts overlap. Risk aversion describes preference for certainty over uncertainty. Loss fear specifically targets downside outcomes.

This fear does not equal poverty or low income. Wealthy individuals frequently report strong fear of financial loss despite substantial assets.

Common misconception: Fear of losing money is the same as being careful with money. Careful money management involves planning and discipline. Fear involves emotional avoidance and decision paralysis.

Fear of losing money does not guarantee financial safety. Excessive fear often creates worse outcomes through inflation erosion, missed opportunities, and suboptimal asset allocation.

Why Humans Fear Losing Money More Than Gaining It

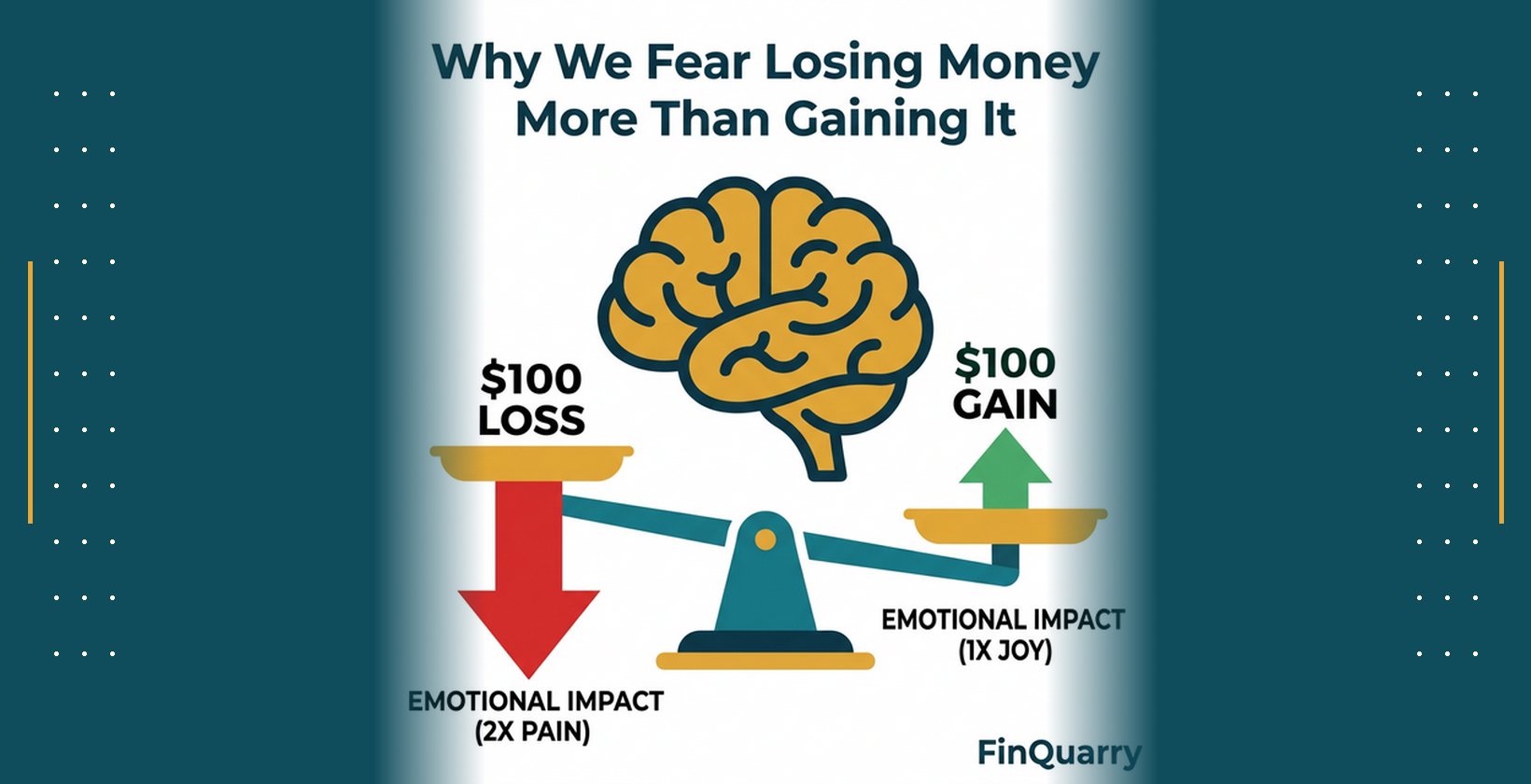

Humans process financial losses and gains asymmetrically. The psychological pain from losing money typically feels approximately twice as intense as the pleasure from gaining an equivalent amount. This asymmetry, established through decades of behavioral research, explains why loss fear dominates financial decision-making even when mathematically irrational.

Loss Aversion Explained (Behavioral Finance Mechanism)

Loss aversion is a cognitive bias where people weigh losses more heavily than equivalent gains when making decisions. Research by Daniel Kahneman and Amos Tversky established this principle as a cornerstone of Prospect Theory.

The typical ratio shows losses feel approximately 2× more impactful than gains. Losing $100 creates roughly twice the emotional intensity as gaining $100 generates satisfaction.

Mechanism: When evaluating potential outcomes, the brain assigns disproportionate negative weight to possible losses compared to possible gains.

This bias affects decisions across timeframes. People reject favorable bets like 50% chance to win $110 versus 50% chance to lose $100, despite positive expected value.

Loss aversion operates unconsciously. People often make fear-driven decisions without recognizing the bias influencing their choices.

Financial impact: Loss aversion drives excessive conservatism in portfolio allocation, premature selling after declines, and avoidance of beneficial opportunities carrying any downside risk.

Brain-Level Response to Financial Loss

The amygdala, a brain structure responsible for threat detection, activates strongly when people face potential financial losses. This creates an immediate emotional response before rational analysis occurs.

The prefrontal cortex, which handles logical reasoning and long-term planning, typically activates more slowly than the amygdala. Fear responses precede rational evaluation.

Neurological sequence: Perceived loss → amygdala activation → fear response → prefrontal cortex attempts override → frequent failure of logical override under stress.

Why logic fails under perceived loss: The amygdala generates powerful emotional states that the prefrontal cortex must actively suppress. This suppression requires cognitive effort and often fails when fear is intense.

Brain imaging studies show that financial losses activate pain-processing regions, not just decision-making areas. The brain treats financial loss partly like physical threat.

Evolutionary Origin of Loss Sensitivity

Evolutionary psychology suggests loss sensitivity provided survival advantages in resource-scarce ancestral environments. Avoiding resource loss mattered more than acquiring extra resources for immediate survival.

Survival bias: Ancestors who protected existing food, shelter, and tools survived more reliably than those who took risks for additional resources.

Modern financial environments differ drastically from ancestral scarcity, but psychological mechanisms evolved over millennia persist. Brains still treat financial loss like a survival threat.

Resource protection instincts evolved stronger than resource accumulation instincts. This asymmetry made sense when losing winter food stores meant death, but gaining extra stores provided limited incremental survival benefit.

Contemporary investing requires accepting temporary losses for long-term gains, directly conflicting with evolved loss-avoidance programming. This evolutionary mismatch explains persistent fear despite logical understanding.

How the Fear of Losing Money Affects Financial Behavior

Fear of financial loss creates observable patterns across multiple decision domains. These patterns typically prioritize short-term security over long-term wealth optimization, often resulting in worse financial outcomes despite protective intent. Understanding these behavioral manifestations helps identify when fear drives decisions rather than rational analysis.

Spending Decisions

Fear of losing money often creates excessive spending restriction that reduces quality of life without proportional financial benefit. People may deny reasonable purchases due to anxiety about depleting resources.

Over-restriction pattern: Avoiding all discretionary spending even when financially sustainable, driven by fear rather than budget constraints.

Guilt-driven consumption avoidance emerges when people feel intense negative emotions after spending on non-essentials, regardless of actual financial impact or budget adherence.

The fear creates mental accounting distortions. Money designated for enjoyment gets mentally reclassified as emergency reserves, preventing its intended use.

Behavioral outcome: Chronic underspending relative to financial capacity, accompanied by persistent anxiety that spending reduction never fully resolves.

Saving and Cash Hoarding

Excessive emergency fund accumulation represents a common fear-driven behavior. People may hold 12-24 months of expenses in cash despite traditional 3-6 month guidelines.

Opportunity cost blindness: Focus on loss avoidance prevents recognition of wealth erosion through inflation and foregone investment returns.

Cash hoarding feels safe because nominal dollar amounts remain stable. The fear obscures purchasing power decline and long-term wealth damage.

People experiencing intense loss fear often cannot articulate how much savings feels “enough.” The target expands as wealth grows because fear, not math, drives the decision.

Financial consequence: Inflation erodes cash value approximately 2-3% annually in stable economies. Large cash positions lose substantial purchasing power over decades.

Investing Behavior

Panic selling during market declines locks in unrealized losses and prevents participation in subsequent recoveries. Fear transforms temporary price drops into permanent wealth reduction.

Market avoidance: Many people avoid stock market investing entirely due to loss fear, despite historical long-term return advantages over bonds and cash.

Preference for “safe” assets like savings accounts or short-term bonds creates opportunity cost. The fear of volatility overrides consideration of long-term purchasing power risk.

Excessive portfolio conservatism relative to time horizon and goals reduces expected returns. A 30-year-old holding 80% bonds demonstrates fear-driven rather than goal-optimized allocation.

Behavioral finance observation: Loss fear causes investors to focus on short-term price fluctuations rather than long-term value accumulation, worsening investment outcomes through poor timing.

Career and Life Decisions

Fear of losing money keeps people in dissatisfying jobs that offer income security. Career changes carrying temporary income reduction get rejected despite better long-term prospects.

Risk avoidance: Calculated career risks like entrepreneurship, education investments, or industry transitions get avoided due to income uncertainty fear.

Staying in unfulfilling work due to loss fear creates long-term costs: reduced lifetime earnings from foregone advancement, health impacts from chronic job stress, and opportunity costs from underdeveloped skills.

The fear creates decision paralysis around major life choices. People delay or avoid decisions like career changes, relocations, or education because uncertainty triggers loss anxiety.

When the Fear of Losing Money Is Rational vs Harmful

Fear of financial loss serves protective functions in some contexts but causes substantial harm in others. Distinguishing rational caution from destructive fear requires evaluating actual risk, time horizon, and financial position. This section provides decision clarity for assessing when loss fear appropriately guides choices versus when it undermines financial wellbeing.

Situations Where the Fear Is Rational

Income instability justifies heightened loss caution. People with irregular paychecks, commission-based income, or employment insecurity face genuine downside risk requiring defensive positioning.

High debt exposure: Large debt obligations relative to income create real vulnerability where additional losses could trigger cascading financial problems including default or bankruptcy.

Short time horizons make loss avoidance rational. People needing capital within 2-3 years should prioritize preservation over growth because insufficient recovery time exists after potential losses.

Near-retirement or in-retirement individuals have legitimate reasons for higher loss sensitivity. Limited earning years remain to rebuild wealth after significant portfolio declines.

Rational fear characteristics: Specific identified risks, proportional defensive responses, temporary duration tied to risk period, does not prevent all growth-oriented actions.

When the Fear Becomes Financially Harmful

Long-term wealth erosion occurs when fear drives permanent avoidance of growth assets. Holding only cash or bonds for 20+ year horizons typically underperforms diversified portfolios substantially.

Inflation-adjusted loss: “Safe” assets often lose purchasing power over time. A 2% return with 3% inflation creates 1% annual real loss compounding over decades.

Missed compounding represents opportunity cost from fear-driven avoidance. Stock market historical returns near 10% annually mean decades of cash-holding sacrifice significant terminal wealth.

The fear becomes harmful when it creates worse outcomes than the feared scenario. Avoiding all investment risk often produces greater long-term wealth reduction than temporary market declines.

Harm threshold: Fear becomes destructive when protective actions cause more damage than reasonable worst-case outcomes from the avoided action.

Decision paralysis from fear prevents any action, including beneficial ones. Total financial inaction typically produces worse results than imperfect action with moderate risk.

Common Financial Mistakes Driven by Fear of Loss

Specific behavioral errors emerge consistently from loss fear across different financial domains. Each mistake follows a similar pattern: short-term loss avoidance creates larger long-term costs. Recognizing these errors helps identify when fear rather than analysis drives decisions.

Selling Assets After Losses

Panic selling converts temporary paper losses into permanent realized losses. Market declines create fear that triggers selling, eliminating potential recovery participation.

Mechanism: Price drops activate amygdala fear response. The brain interprets market volatility as immediate threat requiring protective action.

Selling after declines means buying high and selling low, the reverse of profitable investing. Fear inverts optimal behavior.

Historical market patterns show most significant gains occur during early recovery periods. Panic sellers miss these gains after absorbing the full decline.

Research finding: Studies of investor behavior show that those who panic-sold during major declines underperformed those who maintained positions by substantial margins over subsequent recovery periods.

Avoiding Investing Entirely

Complete market avoidance eliminates volatility but guarantees inflation-adjusted loss over long periods. Fear of temporary decline creates certainty of permanent purchasing power erosion.

Opportunity cost: A 30-year period with stocks returning 9% versus cash at 2% creates dramatic wealth differences—roughly 13× versus 1.8× initial investment.

The fear of “losing money in the stock market” focuses on short-term volatility while ignoring long-term purchasing power loss in cash.

People avoiding all investing often cannot articulate their alternative wealth-building strategy. The fear blocks consideration of how to achieve financial goals without growth assets.

Over-Insuring Low-Impact Risks

Excessive insurance spending on unlikely or low-impact risks drains resources from higher-priority uses. Fear drives coverage of scenarios that, if realized, would create manageable financial strain.

Example pattern: Purchasing insurance for minor appliances, low-deductible policies when high-deductible options better fit finances, or excessive coverage layers.

Insurance serves legitimate risk transfer purposes, but fear-driven over-insurance transforms from protection into wealth drain. Premium costs accumulate while most policies never pay claims.

The appropriate insurance principle covers catastrophic risks that would create financial ruin, not every possible loss. Fear blurs this distinction.

Keeping All Wealth in Cash

Maintaining 100% cash positions for extended periods guarantees purchasing power loss through inflation. The nominal stability feels safe while real value declines.

Mathematical reality: 3% inflation halves purchasing power every 24 years. A 30-year-old keeping retirement savings entirely in cash loses approximately 60% of purchasing power by age 65.

The fear of volatility overrides recognition of certain inflation damage. Temporary price fluctuations feel more threatening than slow, steady erosion.

Diversified portfolios historically outperform cash over periods exceeding 10 years. The fear of market risk trades known inflation loss for feared but unlikely permanent portfolio loss.

How to Reduce the Fear of Losing Money (Without Ignoring Risk)

Managing loss fear requires structural interventions, not motivational willpower. Effective approaches reduce fear’s decision-making influence while maintaining appropriate risk awareness. These methods draw from behavioral finance research and psychological principles applied to financial contexts.

Separating Short-Term Loss From Long-Term Risk

Time horizon reframing helps distinguish temporary volatility from permanent loss. Market declines typically reverse within several years, making multi-decade timeframes fundamentally different from short-term exposures.

Reframing technique: View 1-3 year declines as noise within 20-30 year wealth accumulation. Portfolio values matter at withdrawal, not at interim points.

Historical analysis shows that rolling 20-year stock market periods produce positive returns in nearly all cases, while 1-year periods show high volatility. Time changes risk characteristics.

Short-term losses only become permanent when assets are sold. Unrealized losses in diversified long-term portfolios typically reverse, converting to gains.

Psychological shift: Redefining “loss” from any decline to permanent capital destruction reduces fear response to normal market volatility.

Using Probabilistic Thinking Instead of Emotional Thinking

Expected value calculations compare likely outcomes mathematically rather than emotionally. This replaces worst-case fixation with weighted probability assessment.

Probabilistic approach: Instead of “I could lose money,” think “There’s X% probability of Y% loss over Z timeframe, versus A% probability of B% gain.”

Emotional thinking focuses exclusively on worst scenarios regardless of likelihood. Probabilistic thinking weighs all outcomes by their probability.

Most feared financial scenarios carry low probability. The amygdala treats all threats equally; probability weighting requires conscious prefrontal cortex engagement.

Implementation: Before fear-driven decisions, explicitly list possible outcomes with rough probability estimates. This activates analytical thinking over emotional reaction.

Structural Tools That Reduce Fear

Diversification lowers portfolio volatility through asset class mixing, reducing perceived risk without eliminating growth potential. Lower volatility typically reduces fear response intensity.

Mechanism: Diversified portfolios experience smaller drawdowns than concentrated positions, creating less amygdala activation during market stress.

Automation removes active decision-making from emotionally charged moments. Pre-set investment contributions continue regardless of market conditions or fear levels.

Automated systems prevent panic selling by eliminating real-time choice. Money invests according to plan, not current emotional state.

Rules-based decisions: “I rebalance twice yearly regardless of market conditions” provides structure that overrides fear. The rule becomes the decision-maker.

Financial Planning as Psychological Risk Control

Comprehensive financial plans reduce uncertainty about future outcomes. Uncertainty amplifies fear; planning provides specific scenarios that feel more controllable.

Psychological benefit: Plans answer “what if” questions that otherwise generate anxiety. Knowing responses to market declines, job loss, or expense shocks reduces fear.

Plans do not eliminate risk or guarantee outcomes. They reduce uncertainty by establishing decision frameworks for various scenarios.

The planning process itself reduces loss fear by demonstrating survival paths through feared scenarios. Seeing that portfolio decline X still allows goal achievement reduces scenario fear.

Research observation: Studies show that people with written financial plans report lower financial anxiety despite similar objective financial positions to those without plans.

Does the Fear of Losing Money Ever Go Away?

Fear of financial loss represents a fundamental aspect of human psychology rooted in brain structure and evolutionary history. Complete elimination is unrealistic, but the fear’s intensity and decision-making influence can change substantially. Honest expectation-setting prevents frustration from pursuing impossible goals while enabling achievable fear management improvements.

Why the Fear Never Fully Disappears

The amygdala’s threat-detection functions operate automatically and unconsciously. No amount of knowledge or experience completely overrides these evolutionarily ancient responses.

Neurological reality: Brain structures generating fear responses predate logical reasoning structures by millions of years evolutionarily. Newer systems modulate but cannot eliminate older systems.

Loss aversion appears across cultures, ages, and income levels. The universality suggests hardwired psychological mechanisms not eliminated through environmental changes.

Even sophisticated investors and financial professionals experience loss fear. Expertise reduces fear’s decision-making influence but does not eliminate the emotional experience.

Psychological permanence: Fear of loss serves adaptive functions in appropriate contexts. Complete elimination would remove useful caution along with harmful anxiety.

What Changes With Financial Knowledge

Financial education shifts fear from generalized anxiety to specific risk recognition. Understanding market mechanics helps distinguish temporary volatility from fundamental problems.

Knowledge impact: Educated investors still feel fear during declines but increasingly recognize the emotion as distinct from actual threat assessment.

Experience with market cycles reduces panic response intensity. After surviving several market downturns, the pattern becomes familiar rather than existentially threatening.

Understanding that others experience identical fears (herd behavior recognition) helps identify when fear rather than analysis drives market movements.

Behavioral improvement: Knowledge does not eliminate fear but increasingly prevents fear from controlling decisions. The gap between feeling fear and acting on fear widens.

Managing Fear Instead of Eliminating It

Effective fear management accepts fear’s presence while preventing it from dictating financial choices. The goal becomes decision-making despite fear, not fearless decision-making.

Management approach: “I feel afraid, but I recognize this as loss aversion, and my plan accounts for this scenario.”

Structural interventions work better than willpower. Automation, rules-based systems, and pre-commitment mechanisms remove real-time choice when fear is most intense.

Regular exposure to feared scenarios in controlled ways (reviewing portfolio during volatility, reading about market history) reduces fear response intensity over time through habituation.

Long-term pattern: Fear becomes a recognized signal requiring conscious evaluation rather than an automatic decision trigger. The response to fear changes more than fear itself.

Key Takeaways: Fear of Losing Money and Better Financial Decisions

Fear of losing money is a psychological response to potential loss, not a mathematical calculation. The brain processes potential losses approximately twice as intensely as equivalent gains.

Loss avoidance focuses on preventing wealth reduction. This differs fundamentally from wealth creation, which requires accepting calculated risks and temporary volatility.

Structural interventions: Automation, diversification, rules-based systems, and comprehensive planning reduce fears’ influence on decisions more effectively than attempting fear elimination.

Decisions improve when loss is contextualized within time horizons, probability distributions, and alternative opportunity costs. Fear focuses on worst-case scenarios; effective decision-making weighs all outcomes.

The fear of losing money never disappears completely but becomes manageable through knowledge, experience, and structural systems. The goal is preventing fear from controlling choices while maintaining appropriate risk awareness.

Final principle: Distinguishing rational caution from destructive fear requires evaluating whether protective actions create better outcomes than the feared scenario. When fear-driven avoidance produces greater long-term harm than potential losses from action, fear has become financially destructive.