Table of Contents

Contents are generated from article headings.

PEX is a card-first spend management platform that enables companies to issue prepaid or commercial cards to employees, enforce real-time spending controls, capture receipts at the point of purchase, and synchronise transaction data to accounting systems. Evaluating PEX for employee expense reimbursement requires assessing whether PEX’s prepaid card model aligns with your company’s spending workflows, policy enforcement requirements, accounting integration needs, and security standards. A feature list comparison does not constitute a vendor evaluation; operational due diligence covering ROI modeling, compliance verification, and fit assessment does.

Jurisdiction and Temporal Scope: Expense reimbursement rules, tax treatment, per diem limits, and recordkeeping requirements vary by country, state, and industry. This guide explains evaluation criteria using general principles applicable to US-based businesses; always confirm requirements with your finance, tax, and legal team. As of 2026, spend management platforms frequently update features, compliance certifications, and pricing. Validate current pricing, security reports, and integration support directly with PEX during your vendor review process.

What “Employee Expense Reimbursement” Means in 2026 and Where PEX Fits

Employee expense reimbursement refers to the structured process by which companies recover employee-incurred business costs through a defined workflow of spend, receipt submission, manager approval, accounting code assignment, and repayment or balance settlement. In 2026, finance teams evaluate this process across three model types: traditional post-spend reimbursement, card-first spend management, and hybrid approaches combining both. Understanding which model a platform represents determines whether the platform solves the right problem for a given organisation.

Manual Reimbursement vs Card-First Spend Management

Traditional expense reimbursement operates on a post-spend basis. Employees pay out of pocket using personal funds or personal credit cards, submit expense reports with attached receipts, wait for manager and finance approval, and receive repayment via payroll or ACH transfer. This model places cash flow burden on employees, delays finance team close cycles, and enforces policy after spending has already occurred. Card-first spend management replaces this sequence by issuing company-controlled cards to employees before spending occurs, shifting policy enforcement from post-spend audit to pre-spend control at the transaction level.

Where PEX Sits in the Expense Management Ecosystem

PEX operates as a card-centric spend automation platform positioned between simple prepaid card programs and full enterprise travel and expense suites. PEX issues physical and virtual cards to employees, configures spending rules at the card or employee level, captures receipts via mobile application, and routes transaction data to accounting integrations. PEX does not function primarily as a reimbursement tool for out-of-pocket personal spending. Finance teams evaluating PEX to replace a post-spend reimbursement workflow need to confirm whether their employees will accept a card-first model before proceeding with technical evaluation.

When Companies Typically Evaluate PEX

Finance teams tend to evaluate PEX when existing expense processes produce measurable inefficiency or control failures. Common trigger scenarios include policy leakage where employees consistently spend outside approved categories, slow monthly close cycles caused by incomplete or late expense report submissions, fraud risk from duplicate receipt submissions or fictitious expenses, and scaling team size that makes manual expense report review unsustainable. PEX evaluation tends to produce the strongest ROI case when the organisation has high transaction volume, distributed teams, and existing difficulty enforcing expense policy through post-spend audits.

How PEX Works for Expense Reimbursement (Mechanism Walkthrough)

PEX’s operational model centres on four interconnected components: card issuance with spend controls, receipt capture and transaction matching, approval workflow routing, and accounting system synchronisation. Each component addresses a distinct friction point in the traditional expense management process. Finance teams evaluating PEX benefit from understanding each component as a mechanism rather than a feature, because mechanism understanding reveals where PEX creates genuine workflow change versus where it replicates existing manual steps in a different interface.

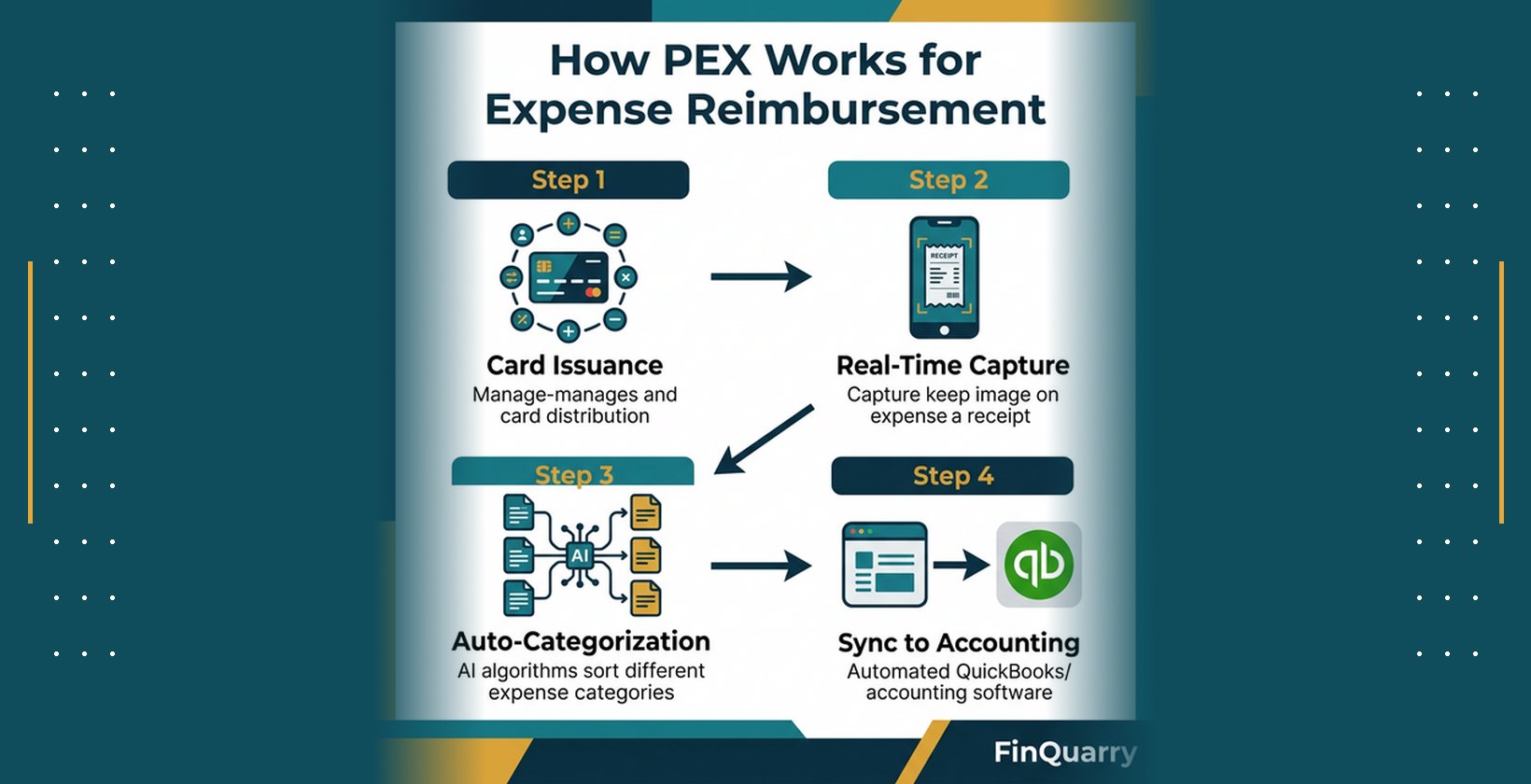

Card Issuance and Spend Controls (MCC, Limits, Restrictions)

PEX issues physical or virtual cards funded through a company-loaded balance or commercial card program. Finance teams configure spending controls at the card or employee level before card activation. Merchant category code (MCC) restrictions block transactions at non-approved vendor categories, preventing an employee from using a company card at a retailer outside approved spending categories. Spend limits cap transaction amounts or periodic totals per card. Specific merchant allow or deny lists restrict or permit individual vendors regardless of category. Time-based rules limit card usage to defined business hours or date ranges. Policy controls applied through MCC restrictions and spend limits prevent out-of-policy spending at the transaction point rather than detecting it during post-spend review.

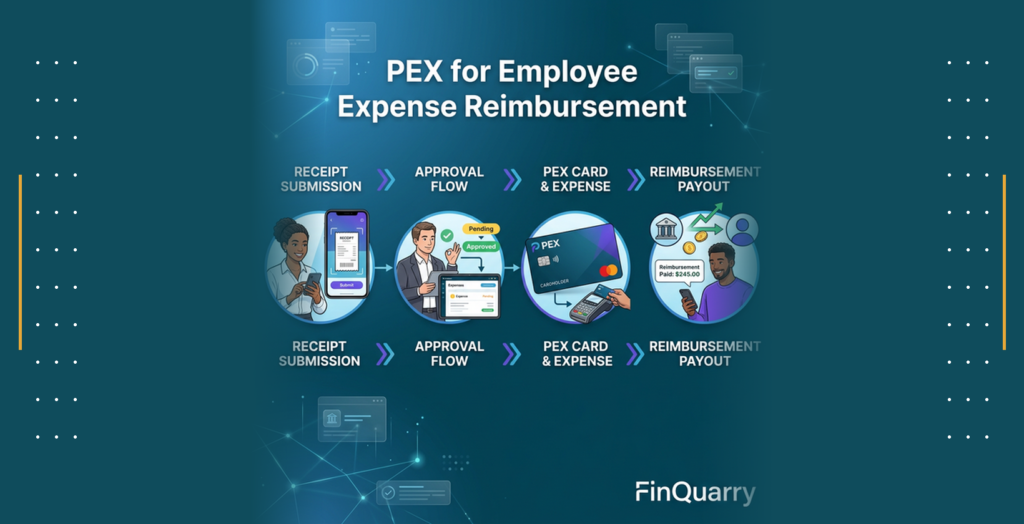

Real-Time Expense Tracking and Receipt Capture (OCR and Matching)

PEX provides a mobile application through which employees capture receipt images at the point of purchase. The platform applies optical character recognition (OCR) technology to extract merchant name, transaction date, and amount from receipt images and matches this extracted data to the corresponding card transaction record. Receipt-to-transaction matching reduces reconciliation time by replacing the manual process of pairing paper or email receipts to bank statement line items. Unmatched transactions generate automated reminders to employees, creating systematic accountability without requiring individual finance team follow-up on missing documentation.

Approval Workflows and Exception Handling

PEX routes transactions through configurable multi-step approval workflows. A standard flow proceeds from employee card user to line manager to finance reviewer, with escalation paths defined for exception cases. Transactions that exceed soft limits or fall outside defined categories route to an exception queue rather than processing automatically. The exception workflow separates routine approved spend from flagged items, allowing finance teams to concentrate review capacity on higher-risk transactions. Approval decisions and reviewer identities are recorded in the audit trail, supporting both internal compliance reporting and external audit evidence requirements.

Accounting Integrations and GL Synchronisation

PEX synchronises transaction data to accounting platforms including QuickBooks Online, NetSuite, Sage, and other supported integrations. GL coding rules map merchant categories or transaction tags to chart of accounts codes, reducing manual coding entries during the close cycle. The timing of data synchronisation, whether real-time or batch, affects when transaction data becomes visible in the general ledger and determines how quickly finance teams can act on spending information during the period. Finance teams should confirm synchronisation frequency, field mapping flexibility, and error handling procedures with PEX during the technical evaluation phase.

Evaluation Criteria That Determine If PEX Is the Right Fit

Evaluating PEX requires applying criteria that test genuine operational fit rather than generating a feature checklist. Four evaluation dimensions tend to determine whether PEX creates value for a specific organisation: use-case alignment, policy enforcement model, reporting depth, and scalability structure. Finance teams that skip these dimensions and evaluate based on interface quality or marketing claims tend to implement platforms that fail to deliver measurable process improvement.

Use-Case Fit: Card-Based Spend vs Invoice-Heavy AP Workflows

PEX addresses employee card-based discretionary spending including travel, meals, office supplies, software subscriptions, and client entertainment. PEX does not address accounts payable workflows involving vendor invoices, purchase orders, three-way matching, or supplier payment runs. Organisations where the majority of business spending flows through vendor invoices rather than employee-initiated card transactions tend to find limited ROI from PEX because the platform’s core controls apply at the card transaction level, not the invoice approval level. Finance teams should quantify the split between card-initiated spend and invoice-based spend in their current environment before proceeding with PEX evaluation.

Policy Enforcement Depth (Pre-Spend vs Post-Spend Controls)

Policy enforcement in expense management operates at two points: pre-spend blocking prevents non-compliant transactions from completing, while post-spend audit detects non-compliant transactions after they have processed. PEX enforces policy primarily at the pre-spend level through MCC restrictions, spend limits, and merchant rules. Pre-spend controls generally produce stronger compliance outcomes than post-spend audit because they prevent the policy violation rather than documenting it after the fact. Finance teams should assess which expense categories in their current environment generate the most policy violations and confirm whether PEX’s MCC controls cover those categories adequately.

Reporting and Spend Visibility (Cost Centres, Projects, Budgets)

PEX reporting provides visibility into transaction data segmented by employee, card, merchant category, department, and custom tags. Finance teams managing multi-department budgets, project-based cost allocation, or client-billable expense tracking should evaluate whether PEX’s reporting dimensions match their chart of accounts structure and reporting requirements. Reporting depth determines how useful PEX data becomes in management accounting workflows beyond expense compliance. A platform with strong controls but shallow reporting tends to create a second data reconciliation step rather than eliminating one.

Scalability and Multi-Entity Complexity

PEX operates most efficiently in single-entity or simple organisational structures. Finance teams managing multiple legal entities, subsidiaries with separate chart of accounts, or employees operating in multiple currencies should evaluate whether PEX’s multi-entity capabilities match their structural complexity. International spend coverage, multi-currency card support, and cross-entity reporting consolidation vary across PEX plan tiers and should be confirmed directly with PEX during evaluation. Organisations with high multi-entity complexity may find that PEX requires supplementary tools to support full accounting consolidation.

Security, Compliance, and Audit Readiness

Security and compliance verification for PEX evaluation covers four domains: card data security standards, internal controls certification, access and audit log architecture, and vendor-level risk assessment. Finance teams that evaluate PEX compliance by reviewing marketing materials rather than requesting formal documentation tend to underestimate the verification requirements for enterprise procurement approval. Each domain requires document requests rather than demo-screen review.

PCI DSS and Card Data Security

PCI DSS (Payment Card Industry Data Security Standard) governs the security requirements for platforms that store, process, or transmit payment card data. PEX, as a card issuance and management platform, operates within the PCI DSS framework. Finance teams should request PEX’s current PCI DSS attestation of compliance (AOC) as part of vendor due diligence. The AOC confirms the scope of the PCI DSS assessment, the version assessed (PCI DSS 4.0 as of 2024), and the qualified security assessor (QSA) who conducted the review. A current AOC provides verifiable evidence of card data security compliance rather than relying on self-reported claims.

SOC 2 Type II and Internal Controls

SOC 2 Type II certification, issued under AICPA standards, confirms that an independent auditor has examined a platform’s security, availability, processing integrity, confidentiality, and privacy controls over a defined period, typically 12 months. SOC 2 Type II differs from SOC 2 Type I in that Type II covers the operating effectiveness of controls over time rather than their design at a single point. Finance teams evaluating PEX for use in environments with internal control requirements should request PEX’s most recent SOC 2 Type II report. The report’s scope section confirms which trust service criteria were included in the assessment and whether card management workflows fall within the covered scope.

Role-Based Access and Audit Trails

Role-based access control in PEX limits platform permissions based on user role, preventing employees from viewing card configurations, approving their own transactions, or accessing reporting beyond their assigned scope. Audit trails record all platform actions including card configuration changes, transaction approvals, exception decisions, and user access modifications. Finance teams should confirm that audit logs are immutable, meaning they cannot be altered or deleted by platform users, and that log retention periods meet the organisation’s recordkeeping requirements. Immutable audit trails support both internal control testing and external audit evidence requests without requiring manual documentation assembly.

Vendor Due Diligence Checklist

Vendor due diligence for PEX extends beyond compliance certifications to cover operational continuity and service reliability. Finance teams should request the following documentation before contract execution: SOC 2 Type II report (most recent period), PCI DSS attestation of compliance, service level agreement (SLA) specifying platform uptime guarantees and incident response times, issuer bank disclosure identifying the financial institution backing the card program, and data processing agreement (DPA) if the organisation operates under GDPR or equivalent privacy regulations. The issuer bank structure determines card program continuity risk; if PEX changes issuer bank relationships, existing card programs may require reissuance or programme reconfiguration.

ROI and Total Cost of Ownership (TCO) Modeling for PEX

ROI modeling for PEX requires quantifying value across three categories: time savings from workflow automation, cost avoidance from reduced policy leakage and fraud, and efficiency gains in the finance close cycle. TCO modeling requires accounting for the full cost stack beyond subscription fees. Finance teams that evaluate ROI based on subscription cost alone tend to underestimate total platform cost and overestimate net return.

Time Savings Model (Employee and Finance Team Hours)

Time savings in PEX adoption accumulate across three groups: employees who spend less time completing expense reports, managers who spend less time reviewing and approving submissions, and finance team members who spend less time reconciling transactions and chasing missing receipts. A time savings model for a 50-employee organisation spending an average of 2 hours per month per employee on expense reporting, at a fully loaded hourly rate of $35, generates $42,000 in annual employee time value. Finance team savings from automated reconciliation and GL coding may add a further $8,000 to $15,000 annually depending on current manual process intensity. These figures are illustrative; actual savings depend on current process efficiency, transaction volume, and fully loaded compensation rates.

Fraud Reduction and Policy Leakage Savings

Policy leakage refers to spending that falls outside approved categories, exceeds approved limits, or lacks adequate documentation but passes through approval due to reviewer fatigue or insufficient controls. Organisations with manual expense reporting processes tend to experience policy leakage rates that generate measurable overspend relative to policy-compliant spending. Fraud controls in PEX, including duplicate receipt detection and MCC blocking, reduce the incidence of fictitious or inflated expense submissions. Quantifying current policy leakage requires analysing a sample of recent expense reports against policy rules to estimate the percentage of spending that would have been blocked or flagged under pre-spend controls.

Platform Costs (Subscription, Onboarding, Integration)

PEX total cost of ownership includes subscription fees per user per month, onboarding and training time for administrators and employees, integration configuration costs whether handled internally or through paid implementation services, and card program costs if applicable under the selected PEX plan tier. Validate current subscription pricing directly with PEX as pricing structures change. Onboarding time estimates typically range from 4 to 8 hours for finance administrators and 1 to 2 hours per employee for mobile application training and policy communication. Integration costs depend on whether the target accounting platform is natively supported or requires custom configuration.

Simple ROI Formula Template

ROI Formula:

ROI = (Hours Saved × Fully Loaded Hourly Rate) + (Policy Leakage Reduction) + (Fraud Reduction) minus Annual Platform Cost

Illustrative Example (Sample Numbers Only):

| Input | Sample Value |

| Employees on platform | 50 |

| Hours saved per employee per month | 2 hours |

| Fully loaded hourly rate | $35 per hour |

| Annual employee time savings | $42,000 |

| Estimated policy leakage reduction | $8,000 per year |

| Estimated fraud reduction | $3,000 per year |

| Total annual value | $53,000 |

| Annual platform cost (illustrative) | $12,000 |

| Net annual ROI | $41,000 |

| ROI percentage | 342% |

All figures in this example are illustrative. Actual results depend on organisation size, spend volume, current process efficiency, and hourly compensation rates. Finance teams should build their own model using actual figures before presenting ROI projections to stakeholders.

Implementation and Change Management Considerations

PEX implementation success depends as much on change management execution as on technical configuration. Platforms with strong spend controls and accounting integrations tend to underperform ROI projections when employee adoption rates fall below the threshold required to generate the modelled time savings. Finance teams should design implementation with adoption rate as the primary success metric rather than technical go-live date.

Pilot Testing Strategy (Department-Based Trial)

A structured pilot limits PEX deployment to a single department for 60 to 90 days before organisation-wide rollout. The pilot department should represent the organisation’s typical spending patterns rather than an outlier with unusually simple or complex spend profiles. Pilot success metrics include: employee adoption rate (percentage of eligible employees actively using PEX cards), exception rate (percentage of transactions requiring manual review or override), time-to-approve for submitted transactions, and GL coding accuracy rate. Finance teams should define minimum acceptable thresholds for each metric before the pilot begins, establishing clear criteria for proceeding with full deployment or returning for reconfiguration.

Employee Adoption and Training

Employee adoption of PEX depends on the perceived ease of the mobile receipt capture workflow relative to the existing process. Training should cover three scenarios: standard transaction completion with receipt capture, exception handling when a card transaction is declined due to MCC restrictions, and the escalation path for legitimate spending outside configured parameters. Policy communication should precede card issuance and explain both what employees can spend and what to do when the card does not work as expected. Adoption rates tend to be lower in organisations where employees are accustomed to personal card use with mileage or reward accrual benefits on their existing cards.

Change Resistance and Policy Tightening Risks

PEX implementation often coincides with tightened expense policy enforcement because the platform makes enforcement technically feasible in ways that manual processes did not. Employees accustomed to informal policy application may interpret card blocking as punitive rather than procedural. Finance teams should communicate policy changes and spending rules before cards are activated and provide a clear exception request pathway for legitimate out-of-policy spending needs. Change resistance that is not addressed during implementation tends to generate workarounds including personal card use alongside company cards, which reduces the data completeness that makes PEX reporting valuable.

Measuring Pilot Success Metrics

Pilot success measurement should occur at 30-day and 90-day intervals using pre-defined metrics. Adoption rate below 70% of eligible users at 30 days typically signals a training or communication gap requiring intervention before full deployment. Exception rate above 15% of transactions at 60 days may indicate that MCC configurations are blocking legitimate business spending and require adjustment. Time-to-approve metrics quantify whether the approval workflow is operating faster than the pre-PEX baseline. Finance teams that measure only technical metrics such as integration uptime and ignore behavioural metrics such as adoption rate tend to miss early signals of implementation failure.

PEX vs Alternatives: Comparative Evaluation Framework

Comparing PEX to alternative platforms requires evaluating platforms on the same criteria applied to the same use case rather than comparing feature lists assembled from different marketing materials. The most relevant comparisons for organisations evaluating PEX are Ramp, Brex, and reimbursement-only tools, because these represent the platforms most frequently considered in the same evaluation process.

PEX vs Ramp (Automation Depth and Card Model)

Ramp operates as a corporate charge card platform with strong automation features including automated receipt matching, duplicate charge detection, and AI-assisted expense categorisation. Ramp extends credit lines to businesses rather than using a prepaid funding model, which means spending is not pre-funded from a company balance. PEX operates primarily on a prepaid model that requires the company to load funds before cards can be used, which provides tighter cash flow control but requires active balance management. Organisations that need credit float between spend and settlement tend to find Ramp’s charge card model operationally easier than PEX’s prepaid structure. Organisations that need absolute spend control without credit exposure tend to prefer the PEX prepaid approach.

PEX vs Brex (Corporate Card Ecosystem)

Brex offers a corporate card program with integrated expense management, bill pay, and business banking features positioned primarily at technology startups and growth-stage companies. Brex’s credit underwriting model uses revenue and bank balance data rather than personal credit history, which makes it accessible to companies without established business credit. PEX does not require credit underwriting because the prepaid model does not extend credit. Organisations evaluating Brex and PEX simultaneously should assess whether the broader Brex financial ecosystem adds value beyond expense management or creates unnecessary platform complexity for their current needs.

PEX vs Reimbursement-Only Tools

Reimbursement-only tools such as Expensify (in reimbursement mode) and Concur Expense process out-of-pocket employee spending through receipt submission, approval, and ACH repayment workflows. PEX does not reimburse out-of-pocket personal spending; PEX eliminates the reimbursement step by ensuring spending occurs on company-issued cards from the outset. Finance teams cannot directly substitute PEX for a reimbursement-only tool without also changing the employee spending behaviour model. Organisations where employees regularly incur business costs on personal cards and expect prompt reimbursement may face adoption resistance when transitioning to a card-first platform regardless of the platform’s technical capabilities.

How to Build a Weighted Vendor Scorecard

A weighted vendor scorecard assigns percentage weights to evaluation criteria based on organisational priorities and scores each vendor against those criteria. A representative scorecard for PEX evaluation might weight use-case fit at 25%, policy control depth at 20%, accounting integration quality at 20%, security and compliance certification at 15%, total cost of ownership at 15%, and vendor support and SLA quality at 5%. Each criterion receives a score from 1 to 5 per vendor, multiplied by the weight, and summed to produce a total score. The weighted scorecard prevents a strong performance on a lower-priority criterion from masking a weak performance on a higher-priority one during vendor comparison.

When NOT to Choose PEX

Finance teams that evaluate PEX only for fit signals risk overlooking clear misfit signals that predict implementation failure. PEX produces the most measurable value in specific operational contexts; outside those contexts, alternative platforms or process improvements tend to generate better outcomes. Identifying misfit scenarios before procurement prevents the cost of a failed implementation.

Invoice-Heavy Procurement Environments

Organisations where the majority of business spending flows through vendor invoices, purchase orders, and accounts payable workflows rather than employee-initiated card transactions will generally find limited value in PEX. PEX controls operate at the card transaction level; they do not address invoice approval, three-way matching, vendor payment terms, or supplier management. Finance teams in manufacturing, construction, or professional services firms with high supplier payment volumes should evaluate AP automation platforms rather than card-based spend management tools as their primary expense control investment.

Strict ERP-Native Workflow Requirements

Organisations with deeply customised ERP environments, including complex multi-step approval hierarchies, project-based cost allocation rules, or industry-specific accounting requirements, may find that PEX’s integration architecture does not support the required data mapping without significant custom development. ERP-native expense modules integrated directly within SAP, Oracle, or Microsoft Dynamics environments tend to provide tighter data consistency than third-party card platforms syncing via API. Finance teams should evaluate integration depth during the technical assessment phase rather than assuming standard integration covers all required data flows.

Low Transaction Volume Organisations

Organisations with fewer than 20 to 25 employees generating expense transactions tend to find that PEX’s subscription cost does not produce a positive ROI relative to the time savings generated. At low transaction volumes, the manual overhead of expense reporting is limited enough that a simpler reimbursement tool or manual process may be more cost-effective. Finance teams should calculate the ROI model using actual transaction volume before committing to PEX evaluation; if the model does not produce a positive return at current scale, the evaluation should be deferred until transaction volume justifies the platform cost.

Global Multi-Currency Complexity Constraints

PEX’s primary card program coverage applies to US-based spending. Organisations with employees who regularly incur expenses in multiple currencies or across international markets should verify PEX’s current international coverage scope and foreign transaction fee structure directly with PEX. Platforms designed for global corporate card programs, including Brex and Ramp, tend to provide stronger multi-currency support for organisations with significant international spend. Finance teams should not assume that PEX’s domestic card capabilities extend to international operations without explicit confirmation from PEX during the evaluation process.

Final Decision Checklist for CFOs and Finance Leaders

The final decision framework for PEX adoption consolidates evaluation outputs into a structured go/no-go assessment. Finance leaders who bypass the decision framework and proceed to contract based on demo impression alone tend to encounter implementation challenges that a structured evaluation process would have identified in advance.

10-Question Executive Checklist

Before approving PEX for procurement, confirm each of the following:

- Does PEX’s card-first model match the spending behaviour of target employees or will reimbursement of personal card spend still be required?

- Do MCC restrictions in PEX cover the specific spending categories where policy leakage currently occurs?

- Does PEX integrate natively with the organisation’s accounting platform and support the required GL coding structure?

- Has PEX provided a current SOC 2 Type II report covering the relevant service scope?

- Has PEX provided a current PCI DSS attestation of compliance at PCI DSS 4.0 level?

- Does the SLA include uptime guarantees and incident response times acceptable for finance-critical operations?

- Has the issuer bank backing the PEX card program been identified and its continuity risk assessed?

- Does the ROI model using actual transaction volume and hourly rates produce a positive return within 12 months?

- Has a pilot plan been designed with defined adoption and performance thresholds before full deployment?

- Have the “when not to choose PEX” scenarios been assessed and confirmed as non-applicable to the organisation?

Documentation to Request Before Signing

Finance teams should request and review the following documents before contract execution: the most recent SOC 2 Type II report including scope and auditor opinion, PCI DSS attestation of compliance from the current assessment period, the service level agreement specifying uptime commitments and incident response obligations, the data processing agreement if the organisation’s employees are located in GDPR-covered jurisdictions, and the issuer bank disclosure identifying the financial institution behind the card program. These documents represent the minimum verification standard for a finance-critical platform procurement and should be reviewed by both finance and IT security teams.

Red Flags During Demos

Several patterns during PEX product demonstrations tend to indicate misalignment between platform capabilities and organisational requirements. Vague answers to questions about MCC restriction granularity may indicate that control depth is less flexible than marketing materials suggest. Inability to show a working integration with the organisation’s specific accounting platform version may indicate integration limitations. Reluctance to provide SOC 2 or PCI DSS documentation during the evaluation process may indicate certification gaps or delays. Pricing presented only as a total package without per-user or per-feature breakdown makes TCO modeling difficult and complicates cost comparison against alternatives.

Final Go/No-Go Framework

The go/no-go decision for PEX adoption should apply a minimum scoring threshold across five weighted dimensions. Use-case fit requires a score of at least 4 out of 5, because a fundamental model mismatch cannot be solved through configuration. Policy control depth requires a score of at least 3 out of 5 to confirm that pre-spend controls address the organisation’s primary policy leakage categories. Accounting integration quality requires a score of at least 3 out of 5 to confirm that GL synchronisation meets close cycle requirements. Security and compliance requires a score of at least 4 out of 5 given the financial data and card data security stakes. ROI model requires a positive net return within 12 months using conservative assumptions. Any dimension scoring below its minimum threshold warrants either platform reconfiguration discussion with PEX or removal of PEX from the shortlist in favour of a better-fit alternative.

How does PEX differ from a standard corporate credit card program?

PEX issues prepaid or commercial cards where spending is funded from a company-loaded balance rather than a credit line. Standard corporate credit cards extend credit that the company repays after a billing cycle. The prepaid model means PEX spending is bounded by the loaded balance, providing tighter cash flow control. Corporate credit cards provide payment float between transaction and settlement but require credit underwriting and carry credit exposure risk.

Does PEX replace expense reports entirely?

PEX replaces the out-of-pocket reimbursement cycle for spending that occurs on PEX-issued cards. Employees no longer submit expense reports for card transactions because PEX captures receipt data and routes transactions through approval workflows automatically. PEX does not replace expense reporting for spending that employees incur on personal cards outside the PEX program. Organisations that allow or require personal card use alongside PEX will still need a reimbursement tool for those transactions.

What accounting integrations does PEX support?

PEX supports integrations with QuickBooks Online, NetSuite, Sage, and other accounting platforms. Integration depth varies by platform and plan tier. Finance teams should request a technical integration guide from PEX during evaluation and confirm that the integration supports the specific version of their accounting platform, the required field mappings, and the synchronisation frequency needed for their close cycle.

How long does PEX implementation typically take?

PEX implementation timelines vary based on organisational size, integration complexity, and change management readiness. Simple deployments for small teams with straightforward accounting integrations may be operational within two to four weeks. Larger deployments with custom GL mapping requirements, multi-department rollout, and formal training programs tend to require six to twelve weeks from contract execution to full operational status. Finance teams should confirm implementation timelines and vendor support availability during the procurement process.

Is PEX suitable for international organisations?

PEX’s card program is designed primarily for US-based business spending. International coverage, foreign transaction support, and multi-currency capabilities should be confirmed directly with PEX during evaluation. Organisations with significant international employee spending requirements may find that platforms specifically designed for global corporate card programs provide better coverage than PEX’s current international offering.