Table of Contents

Contents are generated from article headings.

Envelope budgeting is a cash-based spending control method where physical cash is divided into labeled envelopes — one per spending category — and spending from each category stops when the envelope is empty. The envelope system creates a hard spending boundary that digital payment methods structurally cannot replicate because card and app spending lacks the tangible feedback of watching money physically leave a container.

Envelope budgeting predates every budgeting app and spreadsheet method by decades. Despite its simplicity, it remains one of the most effective behavioral budgeting tools available because it converts abstract account balances into visible, touchable spending limits — which directly reduces the unconscious overspending that occurs when purchases exist only as numbers on a screen.

This content discusses envelope budgeting using financial planning principles and behavioral economics research. Spending habits, income structures, and financial product availability vary by jurisdiction. FinQuarry provides informational content only — this does not constitute personalized financial advice.

How the Envelope System Works

Envelope budgeting operates on a simple mechanism: withdraw the month’s variable spending budget in cash, distribute it into category-labeled envelopes, and pay for each category exclusively from its envelope.

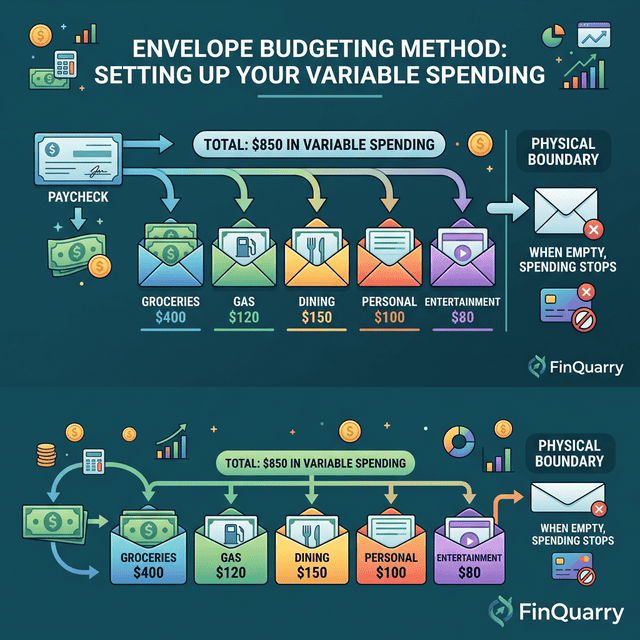

The Setup Process

On payday, after fixed obligations (rent, utilities, insurance, debt minimums) are paid from the bank account, the remaining variable spending budget is withdrawn in cash and divided into envelopes.

A person with $1,600 in monthly variable spending might create six envelopes: Groceries ($500), Gas ($120), Dining Out ($150), Entertainment ($100), Personal ($80), and Household ($50). When the Groceries envelope reaches $0, grocery spending stops until the next pay period — or funds are transferred from another envelope, making the trade-off visible and intentional.

Why Physical Cash Changes Spending Behavior

Research on payment method and spending behavior demonstrates that cash payments activate loss aversion more strongly than card payments. Physically handing over $47 for groceries produces a stronger “spending pain” signal than tapping a card for the same amount because cash spending involves a tangible, visible reduction in resources.

Studies cited by the Consumer Financial Protection Bureau indicate that consumers tend to spend 12–18% less when using cash compared to credit cards, even for identical purchase categories. This spending reduction occurs not through discipline but through the psychological mechanism of enhanced transaction awareness.

When Envelope Budgeting Works Best

For Chronic Overspenders

People who consistently overspend in specific categories — dining out, entertainment, impulse purchases — benefit from envelope budgeting because the empty envelope creates an absolute stopping point that willpower alone cannot provide. A person who budgets $150 for dining but regularly spends $280 on a card will spend closer to $150 when limited to cash, because the physical absence of money overrides the impulse.

For People Who Dislike Tracking

Envelope budgeting requires zero transaction tracking. The envelope balance is the tracking system — glancing inside the envelope shows remaining capacity. This makes it particularly effective for people who find apps and spreadsheets more stressful than helpful, or who have abandoned detailed tracking methods due to effort fatigue.

For Couples With Spending Disagreements

When two people share finances but disagree on spending priorities, dedicated envelopes create individual spending autonomy within shared constraints. Each person receives a personal spending envelope — $150 each, for example — that they control independently. No justification required. No receipts reviewed. The envelope contains the boundary.

Where Envelope Budgeting Breaks Down

Online and Digital Purchases

Envelope budgeting depends on cash transactions, which excludes online shopping, subscription payments, and any card-required purchase. In 2024, e-commerce represented approximately 20% of total retail in the United States, making a purely cash-based system incomplete. The common adaptation is managing online-purchase categories separately through a dedicated debit card with a fixed monthly transfer.

Large or Irregular Expenses

A $600 car repair cannot be paid from a $120 Gas envelope. Large, irregular expenses require a separate financial defense (sinking funds, emergency fund) outside the envelope system — which means budgeting for unpredictable costs still requires complementary planning.

Safety and Convenience Concerns

Carrying $500–1,600 in cash monthly creates theft risk and ATM withdrawal logistics. Some envelope budgeters mitigate this by using the “virtual envelope” approach — keeping money in the bank but tracking spending against virtual category limits using a simple notebook or app.

How to Start Envelope Budgeting

Step 1: Calculate Your Variable Spending Pool

Total take-home income minus all fixed obligations equals the cash available for envelopes. Use your actual spending data from three months of bank statements — not aspirational targets.

Step 2: Identify 5–7 Categories

Limit envelopes to the categories where overspending actually occurs. Most people overspend in 3–4 categories — groceries, dining, entertainment, and personal purchases. Non-problem categories can remain on cards.

Step 3: Fund Envelopes on Payday

Withdraw the total variable budget, distribute into labeled envelopes, and commit to the rule: when the envelope is empty, category spending stops until the next funding cycle.

Step 4: Track Only the Envelopes

At the end of each pay period, note which envelopes ran out early and which had surplus. Adjust allocations the following period based on this data.

Can I Combine Envelope Budgeting With Other Methods?

Envelope budgeting combines effectively with nearly any other method. The most common hybrid: use 50/30/20 or zero-based budgeting for overall income allocation, then implement envelopes for the specific variable categories where overspending occurs.

This hybrid captures the strategic planning of a comprehensive method with the behavioral control of physical cash — producing stronger outcomes than either approach alone.

Is Envelope Budgeting Outdated?

Envelope budgeting is not outdated — it addresses a behavioral spending mechanism that has not changed. The tendency to overspend when payment is abstract (card, app, tap) versus tangible (cash) is consistent across decades of consumer research. The method’s reliance on physical cash limits its scope in a digital-first economy, but the underlying principle — making spending visible and bounded — remains as effective as it was before digital payments existed.

Written by Marcus Tremblay, Senior Financial Analyst | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry