Table of Contents

Contents are generated from article headings.

Cognitive biases are systematic patterns of deviation from rational judgment that affect how people process financial information, evaluate options, and make money decisions. Cognitive biases are not random errors — they are predictable mental shortcuts (heuristics) that the brain uses to reduce the cognitive effort required for complex decisions. In personal finance, these shortcuts consistently produce suboptimal outcomes because financial decisions involve probabilities, delayed consequences, and trade-offs that heuristic processing handles poorly.

Cognitive biases operate below conscious awareness. A person subject to a cognitive bias does not experience the bias as an error — the biased conclusion feels correct, logical, and well-reasoned precisely because the bias operates within the reasoning process itself rather than outside it. This is why knowing about cognitive biases does not automatically prevent them from influencing financial decisions; awareness is necessary but structurally insufficient without systems that counteract biased processing at the decision point.

Scope and Context: This content discusses cognitive biases and their impact on personal finance using established behavioral economics research, peer-reviewed psychological frameworks, and financial planning principles. Financial products, regulations, and market conditions vary by jurisdiction and institution. Readers should evaluate strategies in the context of their own financial circumstances.

How Cognitive Biases Operate in Financial Decision-Making

Cognitive biases affect financial decisions through a mechanism described by Daniel Kahneman’s dual-process theory. The brain uses two distinct processing systems — System 1 (fast, automatic, intuitive) and System 2 (slow, deliberate, analytical) — and cognitive biases emerge primarily when System 1 handles decisions that require System 2’s analytical capacity.

System 1 and System 2 in Financial Contexts

System 1 processing handles financial decisions that feel routine, familiar, or urgent. When a person decides whether to make an everyday purchase, reacts to a market headline, or evaluates a “limited time” offer, System 1 generates an intuitive response based on pattern recognition, emotional association, and past experience. This response is fast and effortless but inherently imprecise for decisions involving compound interest, probability assessment, or long-term trade-offs.

System 2 processing handles financial decisions that are recognized as complex, novel, or high-stakes. Calculating the true cost of a mortgage, comparing insurance policies, or evaluating investment allocations engages System 2’s analytical capacity. However, System 2 processing is cognitively expensive — it requires attention, working memory, and mental energy — and the brain defaults to System 1 whenever possible to conserve resources. Financial anxiety further reduces System 2 availability by consuming cognitive bandwidth, which increases susceptibility to bias-driven financial decisions.

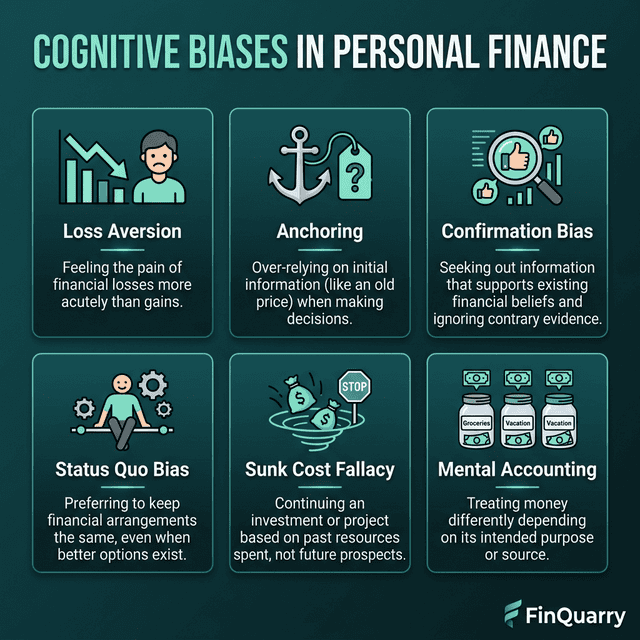

Anchoring Bias in Personal Finance

Anchoring bias is the tendency to rely disproportionately on the first piece of information encountered when making a financial evaluation. The initial number — whether relevant or arbitrary — serves as a cognitive “anchor” that influences all subsequent judgments about value, price, or worth.

How Anchoring Distorts Price Evaluation

Anchoring bias affects purchasing decisions by establishing a reference point that shapes the perception of subsequent prices. When a retailer displays an item’s “original price” of $200 crossed out with a “sale price” of $120, the $200 figure anchors the customer’s value perception even though the original price may have been artificially inflated. The $120 price feels like a bargain relative to the anchor, regardless of the item’s actual market value.

In real estate, listing prices function as anchors that influence what buyers perceive as reasonable offer amounts. A house listed at $450,000 anchors negotiations around that figure; buyers and appraisers adjust from the listing price rather than independently calculating value from comparable sales, property condition, and market fundamentals. This happens even when the listing price is inaccurate.

Anchoring in Investment Decisions

Anchoring bias produces a specific investment error: evaluating a stock’s current price relative to a previous price rather than relative to the company’s current fundamental value. An investor who bought a stock at $50 and watches it decline to $30 may anchor on their purchase price, waiting for the stock to “return” to $50 before selling — even when fundamental analysis suggests the stock is overvalued at $30. The purchase price is financially irrelevant to the stock’s future trajectory, but anchoring makes it feel like the natural reference point.

Confirmation Bias and Financial Belief Systems

Confirmation bias is the tendency to seek, interpret, and remember information that confirms existing financial beliefs while discounting or ignoring information that contradicts them. Confirmation bias is particularly insidious in personal finance because it operates on the information gathering process itself — the person believes they are conducting objective research when they are actually curating evidence that supports a conclusion they have already reached.

How Confirmation Bias Affects Investment Decisions

An investor who believes a particular sector will outperform the market will selectively attend to news, analysis, and expert opinions that support that belief while unconsciously filtering out contrary evidence. This selective information processing creates a self-reinforcing cycle: the investor sees only confirming evidence, which strengthens their conviction, which further narrows their information search, which produces even more confirming evidence.

Confirmation bias contributes directly to portfolio concentration risk. An investor who is certain about a specific stock or sector may overweight that position because their biased information processing has made them overly confident in their analysis. When the position underperforms, the same confirmation bias may delay recognition of the problem, as the investor seeks explanations for why the downturn is temporary rather than evaluating the evidence objectively.

Confirmation Bias in Financial Planning

Confirmation bias affects financial planning by causing people to seek validation for financial strategies they have already chosen rather than genuinely evaluating alternatives. A person who has decided to pay down their mortgage early may seek only information supporting that strategy while ignoring analysis showing that investing the same funds in a diversified portfolio would likely produce a better risk-adjusted return over the same period. The decision feels informed because the person has “researched” it — but the research was confirmation-seeking rather than truth-seeking.

Loss Aversion and the Disposition Effect

Loss aversion — the tendency to experience losses as approximately twice as psychologically painful as equivalent gains are pleasurable — is one of the most empirically documented cognitive biases in behavioral economics, established in Kahneman and Tversky’s prospect theory. Loss aversion produces specific, measurable distortions in how people manage investments, evaluate financial risks, and respond to market conditions.

How Loss Aversion Distorts Portfolio Management

Loss aversion produces the disposition effect: the tendency to sell investments that have increased in value (locking in gains) while holding investments that have decreased in value (avoiding the pain of realizing losses). This behavior is the opposite of what rational analysis would recommend — tax-efficient portfolio management suggests holding winners longer and selling losers to realize tax losses.

The disposition effect reduces long-term portfolio returns because it systematically cuts profitable positions short while allowing unprofitable positions to consume capital and opportunity cost. The investor experiences each sale of a profitable position as a reward (confirming their decision to buy) and avoids selling unprofitable positions because doing so would require acknowledging a mistake — which loss aversion makes disproportionately painful. This same fear mechanism drives many of the behaviors described in how fear and greed influence money choices.

Loss Aversion in Everyday Financial Decisions

Loss aversion extends beyond investment decisions to everyday financial behavior. People pay for insurance on low-cost items (extended warranties on electronics) because the potential loss feels more threatening than the cost of the insurance, even when the expected value of the insurance is negative. People maintain subscriptions they rarely use because canceling feels like “losing” access, even when they are paying more than the service is worth. People overpay for flat-rate plans (unlimited data, all-you-can-eat memberships) because the flat rate eliminates the possibility of an unexpected high bill — a loss — even when pay-per-use pricing would cost less on average.

Status Quo Bias and Financial Inertia

Status quo bias is the preference for the current state of affairs even when change would produce objectively better outcomes. In personal finance, status quo bias manifests as financial inertia — the tendency to maintain existing financial arrangements not because they have been evaluated and found optimal, but because changing them requires cognitive effort, decision-making, and acceptance of short-term uncertainty.

How Status Quo Bias Affects Financial Products

Status quo bias causes people to keep financial products (bank accounts, insurance policies, investment allocations) long after those products have ceased to be optimal for their circumstances. A person may maintain a savings account earning 0.5% interest when multiple alternatives offer 4%+ simply because switching requires effort and the current arrangement is familiar. The annual cost of this inertia can be substantial — on a $50,000 balance, the difference between 0.5% and 4.5% is $2,000 per year in foregone interest.

Status quo bias is particularly powerful in retirement plan management. A person who set an asset allocation when they first enrolled in a workplace retirement plan may maintain that same allocation for years without review, even as their age, risk tolerance, and financial circumstances change. This is why automatic rebalancing and target-date fund structures — which build adjustment into the default system — can partially counteract status quo bias in long-term investing.

Sunk Cost Fallacy in Financial Decisions

The sunk cost fallacy is the tendency to continue investing resources (money, time, effort) in a losing course of action because of the resources already invested, rather than evaluating the decision based solely on future costs and benefits. The resources already spent are “sunk” — they cannot be recovered regardless of the future decision — but the bias causes people to treat them as relevant to the choice.

How Sunk Costs Distort Financial Behavior

The sunk cost fallacy operates in personal finance whenever a person’s reason for continuing a financial behavior is “I’ve already spent so much on this.” Examples include continuing to pay for home renovations that have exceeded budget and will not proportionally increase the home’s value, maintaining an underperforming investment because selling would confirm the loss of previously invested capital, continuing to pay gym membership fees because of the enrollment cost, even when the gym is not being used, and driving across town to use a coupon that saves less than the cost of fuel and time required.

The sunk cost fallacy is psychologically connected to loss aversion: recognizing that sunk costs are irrecoverable means accepting a loss, which loss aversion makes disproportionately painful. The person continues investing to avoid the emotional resolution of acknowledging the loss, even when continuing produces worse financial outcomes than stopping.

Overconfidence Bias in Financial Self-Assessment

Overconfidence bias is the tendency to overestimate one’s financial knowledge, analytical ability, or capacity to predict financial outcomes. Overconfidence manifests in three forms: overestimation (believing one’s performance is better than it actually is), overplacement (believing one is better than others), and overprecision (excessive certainty that one’s estimates are correct).

The Cost of Overconfidence in Investing

Overconfidence causes investors to trade more frequently, maintain less diversified portfolios, and take larger positions than their information would justify. Research published in the Journal of Finance by Brad Barber and Terrance Odean demonstrated that the most active individual traders earned significantly lower net returns than the least active traders — a pattern the researchers attributed to overconfidence driving unnecessary trading that incurred transaction costs without producing information-based returns.

Overconfidence is particularly dangerous in combination with confirmation bias: the overconfident investor conducts biased research, receives biased results, and interprets the biased results as confirming evidence of their superior analysis — producing escalating confidence in a flawed conclusion.

How to Counteract Cognitive Biases in Personal Finance

Cognitive biases cannot be eliminated through awareness alone because they operate within the reasoning process itself. Effective countermeasures are structural — they change the decision environment or introduce systematic checks that interrupt biased processing before it produces action.

Rules-Based Decision Systems

Establishing predefined rules for financial decisions removes the decision point where cognitive biases would otherwise operate. Examples include a predetermined asset allocation with scheduled rebalancing (counteracts anchoring and status quo bias), a fixed savings rate that adjusts automatically with income changes (counteracts lifestyle inflation), and a mandatory waiting period before any purchase above a set threshold (counteracts impulse-driven System 1 processing).

Seeking Disconfirming Evidence

Actively seeking information that contradicts a financial conclusion is one of the few approaches that directly counteracts confirmation bias. Before making a significant financial decision, deliberately searching for reasons why the decision might be wrong — “What would have to be true for this to be a bad choice?” — engages System 2 processing and broadens the information base beyond the confirming evidence that System 1 naturally selects.

Reframing Decisions to Counteract Loss Aversion

Reframing financial decisions in terms of total portfolio value rather than individual position gains or losses can reduce the influence of loss aversion on portfolio management. Instead of asking “Has this stock gone up or down?”, reframing to “Is my total portfolio on track for my goals?” shifts attention from individual loss/gain evaluation to aggregate performance, reducing the disposition effect. Understanding money psychology provides a broader framework for recognizing when emotional processing is overriding analytical assessment.

What Is the Most Harmful Cognitive Bias in Personal Finance?

Loss aversion is often identified as the most financially harmful cognitive bias because of its pervasive influence across multiple financial domains — investment management, insurance purchasing, subscription behavior, and debt repayment decisions. Loss aversion produces measurable underperformance: the DALBAR Quantitative Analysis of Investor Behavior consistently documents a significant gap between market returns and individual investor returns, attributable primarily to emotionally timed buying and selling driven by loss aversion and related biases.

Can Financial Education Eliminate Cognitive Biases?

Financial education can increase awareness of cognitive biases but cannot eliminate their influence on financial decisions. Cognitive biases are features of human cognitive architecture — they are hardwired processing shortcuts, not knowledge deficits. A person who can accurately describe anchoring bias will still be influenced by anchoring when evaluating a purchase price, because the bias operates automatically before conscious analysis begins. Effective bias management requires structural interventions (rules, defaults, automation) rather than information-based interventions alone.

How Many Cognitive Biases Affect Financial Decisions?

Behavioral economics has identified more than 180 distinct cognitive biases, of which approximately 15 to 20 have been empirically demonstrated to have measurable effects on personal finance decisions. The most extensively documented include loss aversion, anchoring, confirmation bias, status quo bias, sunk cost fallacy, overconfidence bias, availability bias, present bias, herd mentality, and mental accounting. The number of biases affecting any individual financial decision is typically three to five, operating simultaneously and often reinforcing each other.

Do Cognitive Biases Affect Wealthy People Differently?

Cognitive biases affect individuals across all income and wealth levels because they are features of human cognition, not symptoms of financial inexperience. However, the financial consequences of biased decisions scale with the amounts involved — an anchoring-biased overpayment on a $500,000 home produces a larger absolute loss than the same bias applied to a $50 purchase. Wealthy individuals may face additional bias exposure through overconfidence (attributing past financial success to skill rather than circumstances) and status quo bias (the comfort of maintaining large existing positions rather than optimizing allocation).