Table of Contents

Contents are generated from article headings.

Withdrawing funds from a bank account before divorce is legally permissible in most jurisdictions, but the legality and consequences depend on account ownership, timing, intent, and state or provincial law. Personal accounts funded with separate property generally allow withdrawal without immediate legal restriction, while joint accounts or accounts containing marital property may trigger court scrutiny, dissipation claims, or financial sanctions if withdrawals lack legitimate purpose or mutual consent.

Courts evaluate pre-divorce withdrawals by examining whether funds qualify as marital property, whether the withdrawal served a legitimate expense, and whether the action was disclosed transparently. Impulsive or secretive withdrawals—especially from joint accounts—often result in equitable distribution adjustments, court-ordered reimbursement, or sanctions that negatively impact the withdrawing spouse’s final settlement.

The core question is not whether you can physically access funds, but whether doing so exposes you to legal consequences that outweigh any short-term financial gain. Jurisdictional rules vary significantly: community property states like Texas treat most marital earnings as jointly owned, while equitable distribution states like Illinois or Washington evaluate contributions and need. Understanding account classification, documenting all transactions, and consulting legal counsel before major withdrawals are essential steps to protect both legal standing and financial interests during divorce proceedings.

Understanding Different Account Types and Ownership

Account ownership determines legal access and vulnerability to dissipation claims during divorce. Courts classify accounts based on title, funding source, and timing of deposits, which directly affects whether withdrawals trigger legal consequences.

Personal vs Joint Accounts

A personal account is an individual account held in one spouse’s name and typically funded by that spouse’s earnings or separate property. A joint account lists both spouses as account holders with equal legal access to all deposited funds.

Personal accounts funded entirely with separate property—such as inheritance, gifts, or pre-marital savings—generally remain outside marital property classification in most jurisdictions. Withdrawals from these accounts before divorce carry lower legal risk because the funds were never subject to equitable distribution. However, if marital income was deposited into a personal account during marriage, those commingled funds may be reclassified as marital property, exposing withdrawals to court review.

Joint accounts, by contrast, are typically classified as marital property regardless of which spouse deposited the funds. Both spouses possess equal legal authority to withdraw funds, but unilateral withdrawal without consent or legitimate justification often constitutes dissipation of marital assets. Courts may adjust equitable distribution to compensate the non-withdrawing spouse or impose sanctions if the withdrawal appears intended to deprive the other party of rightful access.

The critical distinction is not account title alone, but the source and nature of deposited funds. A personal account containing marital earnings loses its separate classification, while a joint account funded solely by one spouse’s inheritance may retain partial separate property protection depending on jurisdiction and documentation.

Community Property vs Separate Property (US Context)

In community property states—including Texas, California, Arizona, and others—most assets and income acquired during marriage are classified as community property, owned equally by both spouses. Separate property includes assets owned before marriage, inheritances, and gifts received individually, provided these assets remain unmixed with marital funds.

Community property classification means that income earned by either spouse during marriage belongs equally to both, regardless of whose name appears on the account. Withdrawing community property funds before divorce does not legally deprive the other spouse of ownership, but it may trigger court intervention if the withdrawal reduced the marital estate’s value without mutual consent or legitimate need.

Equitable distribution states, such as Illinois, Washington, and North Carolina, do not assume equal ownership. Instead, courts divide marital property based on factors like contribution, need, duration of marriage, and each spouse’s financial circumstances. Marital property in these states includes income and assets acquired during marriage, while separate property remains individually owned if properly documented and not commingled.

The classification determines legal risk. In community property states, withdrawing funds from a joint account may require reimbursement of the other spouse’s 50% share. In equitable distribution states, courts evaluate whether the withdrawal was reasonable, transparent, and aligned with legitimate expenses, adjusting the final settlement accordingly.

Trust, Retirement, and Investment Accounts

Trust accounts, retirement accounts, and investment portfolios follow distinct legal rules that limit unilateral access before divorce. Trust accounts established for beneficiaries other than the account holder—such as children or third parties—are generally not considered marital property and cannot be freely accessed by either spouse for personal use.

Retirement accounts, including 401(k)s, IRAs, and pension plans, are typically classified as marital property to the extent contributions were made during marriage. However, early withdrawal from retirement accounts before divorce triggers tax penalties, potential early distribution fees, and court scrutiny. Courts may view such withdrawals as dissipation if the funds were not used for legitimate marital expenses or if the withdrawal reduced the marital estate’s long-term value.

Investment accounts held jointly or funded with marital income are subject to the same dissipation analysis as bank accounts. Liquidating investments or transferring assets to third parties before divorce often raises judicial concern, particularly if the action appears designed to hide wealth or reduce the other spouse’s equitable share.

Account custodians and financial institutions may impose additional restrictions on withdrawals during divorce proceedings, especially after temporary restraining orders are issued. Courts often freeze accounts or require mutual consent for large transactions to preserve the marital estate pending final distribution.

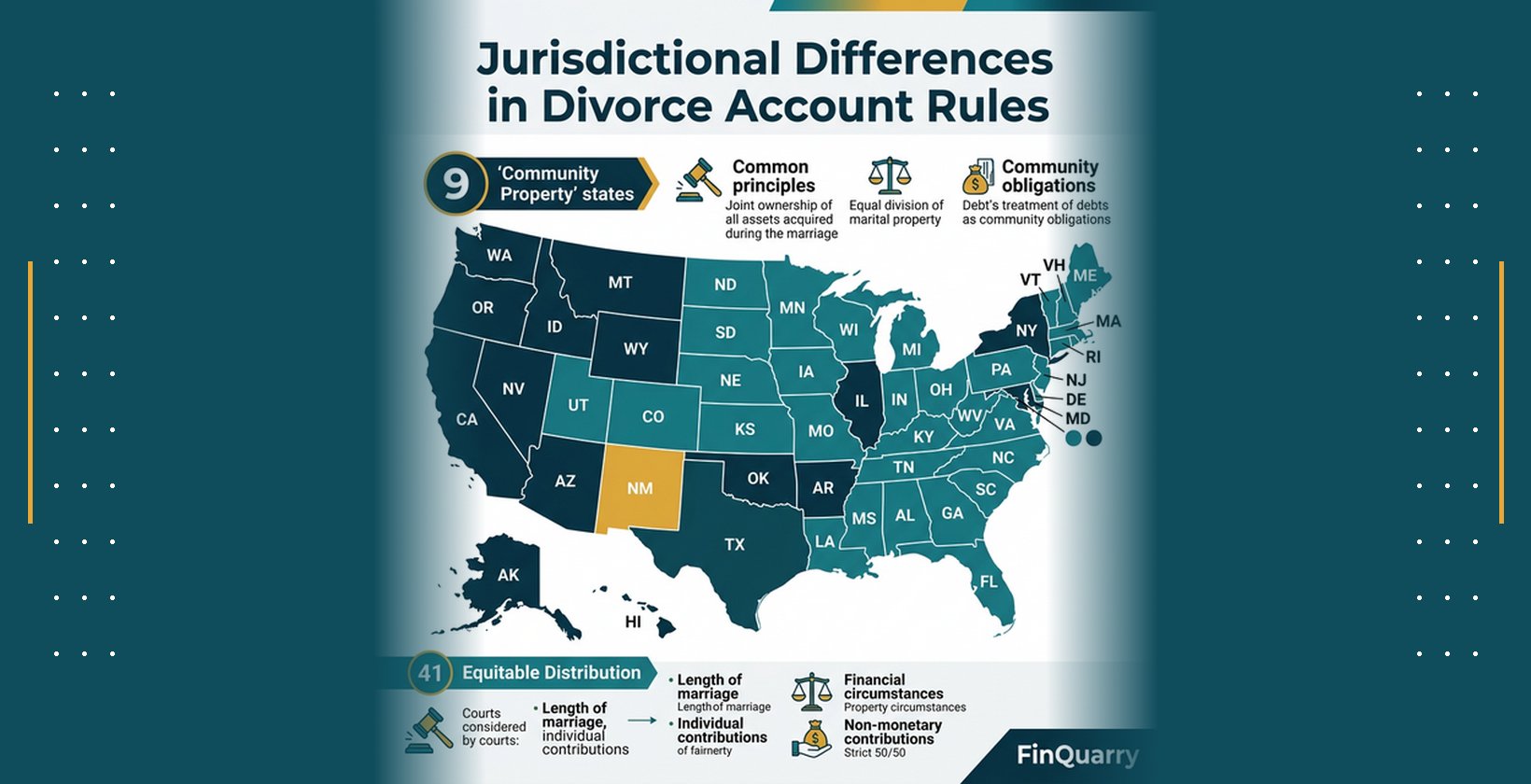

Jurisdictional Differences in Divorce and Account Rules

Jurisdictional variation significantly impacts how courts classify property, evaluate withdrawals, and impose consequences. State, provincial, and international legal frameworks apply different standards for marital property, burden of proof, and dissipation claims.

United States – State Variations (TX, WA, IL)

Texas operates under community property law, where most income and assets acquired during marriage are owned equally by both spouses. Texas Family Code §3.002 defines community property as all property acquired during marriage except for inheritances, gifts, and property owned before marriage. Withdrawing community property funds without legitimate justification may result in court-ordered reimbursement or adjustment in the final property division.

Washington applies equitable distribution principles but also recognizes community property classification. Courts evaluate whether withdrawals were made for legitimate purposes such as household expenses, legal fees, or child-related costs. Washington law allows courts to award a disproportionate share of remaining assets to the non-withdrawing spouse if dissipation is proven.

Illinois follows pure equitable distribution, where courts divide marital property based on fairness rather than equal splits. Illinois law requires full financial disclosure, and courts scrutinize pre-divorce withdrawals for evidence of intent to deprive the other spouse. Concealed withdrawals or transfers to third parties often trigger sanctions, including attorney fee awards and reduced settlement allocations.

These variations require understanding local legal standards before taking financial action. What constitutes permissible withdrawal in one state may result in penalties in another, depending on classification rules, burden of proof, and judicial discretion.

Canada – Federal vs Provincial Rules

Canadian family law operates under provincial jurisdiction, with each province applying its own framework for property division. Federal law governs divorce proceedings, but property classification and division follow provincial statutes.

In British Columbia, the Family Law Act treats family property as equally divisible unless excluded as separate property. Withdrawals from joint accounts before separation may be evaluated as dissipation if they reduced the family property pool without legitimate purpose. Courts may order equitable adjustments or reimbursement to the non-withdrawing spouse.

Ontario’s Family Law Act similarly divides net family property equally, but allows exclusions for inheritances, gifts, and pre-marital assets. Withdrawals from excluded property remain legally protected, while withdrawals from marital accounts may trigger equalization claims if they reduced the other spouse’s entitlement.

Provincial courts emphasize transparency and good faith financial conduct during separation. Concealed withdrawals, transfers to relatives, or undisclosed account closures often result in judicial penalties, including increased financial disclosure obligations and reduced credibility in settlement negotiations.

International Considerations (General Overview)

International divorce cases involve jurisdictional conflicts, treaty obligations, and cross-border asset protection laws. The jurisdiction where divorce is filed typically governs property division rules, but enforcement of judgments across borders requires compliance with international treaties such as the Hague Convention.

Account ownership and withdrawal legality depend on the legal system governing the account’s location. Funds held in offshore accounts or foreign banks may be subject to both the jurisdiction of the account’s location and the divorce court’s jurisdiction. Concealing foreign accounts or failing to disclose international assets often leads to severe legal consequences, including contempt findings, criminal penalties, and forfeiture of equitable claims.

Cross-border financial institutions may refuse to honor withdrawal requests during active divorce proceedings if temporary orders or asset freezes are issued by competent courts. Understanding both local and international legal obligations is essential before accessing funds held outside the primary divorce jurisdiction.

How Courts Handle Pre-Divorce Withdrawals?

Courts evaluate pre-divorce withdrawals by examining timing, intent, documentation, and impact on the marital estate. Judges possess broad discretion to adjust equitable distribution, impose sanctions, or order reimbursement when withdrawals appear improper or unjustified.

Equitable Distribution Principles

Equitable distribution divides marital property based on fairness, considering factors such as length of marriage, each spouse’s financial contribution, earning capacity, and future needs. Courts do not automatically split assets equally but instead allocate property in a manner deemed just under the circumstances.

When one spouse withdraws funds before divorce, courts may adjust the remaining asset distribution to compensate the non-withdrawing spouse. If a spouse withdrew $20,000 from a joint account for personal expenses unrelated to marital needs, the court may allocate an additional $20,000 in remaining assets to the other spouse, effectively reversing the withdrawal’s financial impact.

Equitable distribution analysis also considers whether the withdrawal served legitimate purposes such as paying household bills, covering children’s expenses, or funding necessary legal representation. Withdrawals for extramarital affairs, luxury purchases, or transfers to third parties are more likely to trigger negative adjustments.

Sanctions for Dissipation of Assets

Dissipation of marital assets occurs when one spouse intentionally wastes, conceals, or transfers marital property to reduce the other spouse’s equitable share. Courts impose sanctions to deter dissipation and restore financial fairness.

Common sanctions include court-ordered reimbursement, where the dissipating spouse must return withdrawn funds or compensate the other party through reduced asset allocation. Courts may also award attorney fees to the non-dissipating spouse, require forensic accounting at the dissipator’s expense, or hold the offending spouse in contempt.

In severe cases, judges may impose punitive adjustments that exceed the amount dissipated, particularly if the conduct was deliberate, concealed, or involved fraudulent transfers. Repeated dissipation or refusal to comply with court orders may result in criminal contempt findings, fines, or jail time.

Impact on Custody, Support, and Settlement

Pre-divorce financial misconduct influences judicial credibility assessments, which can extend beyond property division to affect custody, spousal support, and child support determinations. Judges evaluate trustworthiness, transparency, and good faith conduct when making discretionary rulings.

A spouse who concealed withdrawals or lied about financial transactions may face reduced credibility in custody disputes, particularly if financial instability or dishonesty raises concerns about parenting judgment. Courts may also increase spousal or child support obligations if dissipation reduced the marital estate’s ability to meet ongoing family needs.

Settlement negotiations are similarly affected. Opposing counsel may use evidence of improper withdrawals to leverage more favorable settlement terms, knowing that trial outcomes could result in harsher judicial penalties than negotiated agreements.

Evidence & Documentation Required

Courts rely on documentary evidence to determine whether withdrawals were legitimate, transparent, and consistent with marital obligations. Proper documentation protects against dissipation claims and strengthens legal defensibility.

Bank Statements, Transaction Logs

Bank statements and transaction logs provide chronological records of deposits, withdrawals, and account balances. Courts review these documents to identify unusual patterns, large withdrawals, or transfers that coincide with divorce filing or separation.

Complete transaction records should be preserved for all accounts, including checking, savings, investment, and credit accounts. Missing statements or gaps in documentation raise judicial suspicion and may shift the burden of proof to the spouse claiming withdrawals were legitimate.

Digital banking records, screenshots, and PDF downloads serve as admissible evidence, provided they are authenticated and unaltered. Maintaining organized financial records from at least two years before separation strengthens evidentiary credibility.

Emails, Texts, or Written Consent

Written communications between spouses regarding withdrawals demonstrate consent, transparency, or lack thereof. Emails, text messages, and formal agreements serve as critical evidence when disputes arise over whether withdrawals were authorized or disclosed.

A text message stating “I’m withdrawing $5,000 for the mortgage payment” establishes notice and intent, reducing the risk of dissipation claims. Conversely, deleted messages or absence of communication may suggest concealment.

Courts also review communications with third parties, such as financial advisors, accountants, or family members, to assess whether withdrawals were planned, impulsive, or designed to hide assets.

Expert Testimony (Forensic Accountants)

Forensic accountants trace fund movements, identify hidden assets, and evaluate financial discrepancies during divorce litigation. Courts may appoint neutral experts or allow parties to retain their own forensic professionals to analyze complex financial transactions.

Forensic accounting services include examining deposit sources, tracking transferred funds, reconstructing account histories, and identifying unexplained expenditures. Expert testimony carries significant weight in dissipation disputes, particularly when financial records are incomplete or contested.

Courts may order the spouse suspected of dissipation to pay for forensic accounting costs, especially if the analysis reveals concealed assets or fraudulent transfers.

Steps to Protect Yourself Legally and Financially

Protective measures reduce exposure to dissipation claims, preserve marital assets, and maintain legal compliance during divorce proceedings. Proactive financial planning before filing enhances both legal positioning and settlement outcomes.

Opening Separate Accounts

Opening a separate personal account before divorce allows for independent financial management without triggering joint account disputes. Separate accounts should be funded only with personal earnings or separate property to avoid commingling issues.

When opening a separate account, notify your spouse if transparency is required by local law or existing agreements. Concealing account existence may backfire during financial disclosure, while documented notice reduces accusations of financial misconduct.

Direct deposit changes should redirect only the account holder’s individual income, not joint funds or the other spouse’s earnings. Courts view transparent account separation more favorably than secret transfers.

Adjusting Direct Deposits or Payroll

Changing direct deposit destinations ensures personal income flows into separate accounts rather than joint accounts accessible by both spouses. This step prevents unauthorized withdrawals by the other spouse and establishes financial independence before formal separation.

Employers typically process direct deposit changes within one to two pay cycles, so timing is important. Documentation of the change—such as payroll confirmation emails—provides evidence that only personal earnings were redirected, not marital funds.

Courts generally permit adjustment of direct deposits for personal income, but redirecting the other spouse’s income or joint benefits may constitute dissipation or conversion.

Using Temporary Restraining Orders or Freezes

Temporary restraining orders (TROs) or automatic temporary injunctions prevent either spouse from depleting marital assets during divorce proceedings. Many jurisdictions automatically impose these restrictions upon divorce filing, while others require formal motions.

TROs typically prohibit large withdrawals, asset transfers, account closures, or incurring new debt without court approval or mutual consent. Violating a TRO may result in contempt findings, sanctions, or criminal penalties.

Account freezes initiated by financial institutions or courts preserve asset values pending final distribution. Requesting a freeze protects against dissipation by the other spouse but also limits the requesting party’s access, so careful planning is necessary.

Best Practices to Avoid Legal Consequences

Transparent, well-documented financial conduct reduces litigation risk and enhances settlement credibility. Following best practices demonstrates good faith and protects against dissipation claims.

Legitimate Expenses vs Hidden Withdrawals

Legitimate expenses include mortgage or rent payments, utilities, groceries, children’s educational costs, medical bills, insurance premiums, and reasonable legal fees. Withdrawals for these purposes are generally defensible if properly documented and proportionate to actual needs.

Hidden withdrawals—such as transfers to undisclosed accounts, cash withdrawals without receipts, payments to third parties without explanation, or luxury purchases—raise judicial concern and often trigger dissipation findings.

Maintaining receipts, invoices, and written explanations for all significant withdrawals strengthens legal defensibility. Courts evaluate reasonableness based on historical spending patterns, family size, and documented needs.

Maintaining Transparency with Your Spouse and Court

Transparency requires full financial disclosure, timely communication about withdrawals, and cooperation with discovery requests. Courts penalize spouses who conceal assets, provide incomplete financial statements, or obstruct the other party’s access to information.

Voluntary disclosure of withdrawals—even those that may appear questionable—often results in more favorable judicial treatment than concealment discovered through forensic analysis. Judges reward honesty and penalize deception, particularly in YMYL-sensitive family law matters.

Transparency also includes responding promptly to interrogatories, producing requested documents, and correcting errors in financial disclosures. Credibility established through transparent conduct improves settlement leverage and trial outcomes.

Consulting an Attorney Before Major Withdrawals

Legal consultation before withdrawing significant funds reduces the risk of unintended dissipation, sanctions, or strategic mistakes. Attorneys evaluate jurisdiction-specific rules, document withdrawal justifications, and advise on timing and amounts.

Major withdrawals—typically defined as amounts exceeding routine monthly expenses or exceeding 10-20% of total account value—warrant legal review before execution. Attorneys can structure withdrawals to align with legitimate needs, obtain necessary court approvals, or negotiate consent with the other spouse.

Consultation also protects against criminal liability in jurisdictions where fraudulent asset concealment constitutes criminal conduct. Early legal advice prevents costly mistakes and strengthens the withdrawing spouse’s legal position.

Common Behavioral Pitfalls Pre-Divorce

Emotional stress during divorce often triggers impulsive financial decisions that harm long-term legal and financial outcomes. Recognizing common behavioral patterns reduces risk of costly mistakes.

Panic Withdrawals and Emotional Spending

Panic withdrawals occur when spouses fear losing access to funds and withdraw large amounts without clear justification or planning. Emotional spending—such as luxury purchases, revenge expenditures, or impulsive investments—often follows, reducing the marital estate and triggering dissipation claims.

Courts recognize panic-driven behavior but do not excuse it. Judges evaluate intent and reasonableness, and impulsive withdrawals lacking legitimate purpose generally result in adverse financial adjustments.

Behavioral awareness helps individuals pause before acting, consult advisors, and document legitimate needs before withdrawing funds. Cooling-off periods and neutral third-party advice reduce panic-driven mistakes.

Misjudging the Court’s View of Intent

Spouses often misjudge how courts interpret withdrawal timing, amounts, and purposes. What seems justified from one spouse’s perspective may appear deceptive or wasteful to a judge reviewing documentary evidence.

Courts evaluate intent based on objective factors: timing relative to separation or filing, withdrawal size compared to historical patterns, lack of documentation, and consistency with stated financial needs. Subjective justifications without supporting evidence carry little weight.

Understanding judicial skepticism toward large, undocumented, or secretive withdrawals helps spouses align their conduct with legal expectations. Intent is inferred from actions, not post-hoc explanations.

Psychological Triggers that Lead to Asset Dissipation

Psychological triggers—including anger, betrayal, fear of financial loss, or desire for control—drive dissipation behavior. Spouses may rationalize withdrawals as “protecting themselves” or “getting what they deserve,” but courts evaluate conduct objectively.

Loss aversion, a well-documented cognitive bias, causes individuals to feel financial losses more intensely than equivalent gains. This bias may lead spouses to withdraw funds preemptively, even when doing so harms their legal position.

Revenge spending or transferring assets to relatives to “punish” the other spouse typically backfires, as courts impose sanctions that exceed the original dissipation amount. Recognizing these emotional drivers allows individuals to seek professional guidance before acting impulsively.

How Behavioral Awareness Protects Your Case

Self-awareness and structured decision-making reduce the likelihood of financially and legally harmful conduct. Behavioral strategies improve outcomes by aligning actions with long-term interests.

Planning Before Action

Financial planning before taking withdrawals involves assessing legitimate needs, documenting expenses, consulting legal counsel, and obtaining necessary approvals. Planning reduces impulsivity and creates defensible evidence trails.

Written financial plans—such as budgets, expense projections, or temporary support calculations—demonstrate intentionality and reasonableness. Courts view planned conduct more favorably than reactive, undocumented withdrawals.

Using Neutral Advisors or Mediators

Neutral advisors, including financial planners, accountants, or mediators, provide objective guidance free from emotional bias. Mediation facilitates negotiated agreements on account management, temporary fund access, and expense allocation.

Mediators help spouses reach consent-based solutions that avoid court intervention, reduce litigation costs, and preserve credibility. Documented mediation agreements protect both parties by establishing mutual understanding and transparent financial conduct.

How to Legally Manage Funds Before Divorce (Step-by-Step Guidance )

Systematic financial management before divorce reduces legal risk and protects both parties’ interests. Following structured steps ensures compliance and defensibility.

Step 1 – Assess Account Ownership

Review all bank accounts, investment accounts, retirement accounts, and credit accounts to determine legal title and funding source. Identify which accounts are individual, joint, or commingled with marital and separate property.

Account statements from the past 24 months provide baseline data for classification. Separate property accounts should show no deposits of marital income, while joint accounts typically contain mixed funds.

Step 2 – Document Existing Assets

Create comprehensive records of current balances, recent transactions, and account histories. Photograph or download statements, organize records chronologically, and store copies securely.

Documentation serves as evidence if disputes arise later, establishing baseline asset values and transaction patterns. Courts rely heavily on contemporaneous records rather than reconstructed memories.

Determine Legitimate Expenses

Calculate necessary monthly expenses, including housing, utilities, food, transportation, children’s costs, insurance, and reasonable legal fees. Compare planned withdrawals to historical spending patterns and documented needs.

Legitimate expense determinations should be conservative, documented, and proportionate to actual obligations. Overestimating needs or withdrawing excessive amounts invites judicial scrutiny.

Step 4 – Consult Legal Counsel

Schedule consultations with family law attorneys to review jurisdiction-specific rules, evaluate withdrawal risks, and obtain strategic advice. Attorneys assess whether planned actions comply with local law and protect client interests.

Legal counsel also drafts necessary disclosures, negotiates temporary agreements, and prepares documentation to support withdrawal justifications if litigation occurs.

Step 5 – Take Protective Actions (Freeze, Separate Accounts)

Implement account separations, direct deposit changes, or formal freeze requests based on legal advice. Execute protective measures transparently, documenting all actions and notifying the other spouse or court as required.

Protective actions reduce vulnerability to unauthorized withdrawals by the other spouse while maintaining compliance with legal obligations.

Case Scenarios and Lessons Learned

Real-world examples illustrate how different withdrawal strategies produce varying legal and financial outcomes. These scenarios demonstrate practical application of legal principles.

Example: Emptying a Joint Account vs Personal Account

Scenario A: Spouse withdraws $30,000 from a joint account funded entirely with marital income to “secure funds” before filing divorce. No documentation, no notice to other spouse.

Outcome: Court classified withdrawal as dissipation. Spouse ordered to reimburse $15,000 (other spouse’s share) plus attorney fees. Final settlement reduced by additional $10,000 as sanction.

Scenario B: Spouse withdraws $30,000 from personal account funded solely with inheritance received before marriage. Provides documentation proving separate property status.

Outcome: Withdrawal upheld as legitimate separate property access. No court intervention or sanctions.

Lesson: Account funding source and documentation determine legal risk, not withdrawal amount alone.

Example: Hidden Withdrawals Leading to Court Sanctions

Scenario: Spouse makes multiple cash withdrawals totaling $50,000 over six months, providing vague explanations like “household expenses” without receipts. Other spouse discovers withdrawals during discovery.

Outcome: Court found dissipation due to lack of documentation and secretive conduct. Spouse ordered to reimburse full $50,000, pay forensic accounting costs ($8,000), and pay opposing counsel fees ($15,000). Judge cited credibility damage in final ruling, reducing overall settlement by 10%.

Lesson: Hidden withdrawals with inadequate documentation trigger severe consequences exceeding the initial withdrawal amount.

Example: Properly Documented Withdrawals Avoiding Dispute

Scenario: Spouse withdraws $25,000 from joint account for mortgage payments, children’s tuition, and legal fees. Provides receipts, emails notifying other spouse, and detailed expense breakdown.

Outcome: Other spouse challenged withdrawal initially but dropped claim after reviewing documentation. No court intervention needed. Withdrawal treated as legitimate marital expense in final settlement.

Lesson: Transparency, documentation, and notice prevent disputes even when significant funds are withdrawn.

What counts as dissipation of marital assets?

Dissipation of marital assets occurs when one spouse intentionally wastes, conceals, or transfers marital property to reduce the other spouse’s equitable share. Examples include extramarital affair expenses, gambling losses, undisclosed transfers to relatives, luxury purchases unrelated to family needs, or business investments without legitimate justification.

Courts evaluate dissipation by examining timing, intent, documentation, and whether the expenditure benefited the marital estate. Not all wasteful spending qualifies—dissipation requires intentional conduct designed to deprive the other spouse of rightful property.

Can a spouse access retirement or trust accounts?

Retirement accounts can be accessed before divorce, but early withdrawals trigger tax penalties, distribution fees, and court scrutiny. Courts may classify early retirement withdrawals as dissipation if funds were used for non-marital purposes or if the withdrawal reduced the marital estate’s long-term value.

Trust accounts established for beneficiaries other than the account holder generally cannot be accessed by either spouse for personal use. Courts protect trust assets for intended beneficiaries unless the trust was created fraudulently to hide marital property.

How fast can funds be legally withdrawn?

Legal withdrawal speed depends on account type and financial institution policies. Electronic transfers typically process within one to three business days, while wire transfers may complete same-day. However, legal permissibility does not depend on transaction speed but on account ownership, fund classification, and compliance with court orders.

Rapid, large withdrawals immediately before filing divorce raise judicial suspicion and may support dissipation claims even if technically accessible.

Are online and digital transactions treated differently?

Online and digital transactions are treated identically to traditional transactions for legal purposes. Digital records, including screenshots, online banking statements, and electronic confirmations, serve as admissible evidence in divorce proceedings.

Digital banking platforms may provide more detailed transaction records, timestamps, and IP logs that strengthen or undermine dissipation claims. Courts increasingly rely on digital evidence to trace fund movements and verify disclosures.

How to handle cross-state or cross-country account rules?

Cross-state or cross-country accounts require understanding both the jurisdiction where divorce is filed and the jurisdiction governing the account’s location. Legal counsel familiar with multi-jurisdictional issues should review complex account structures before withdrawals occur.

International accounts may be subject to treaty obligations, foreign asset disclosure requirements, and enforcement challenges. Failing to disclose foreign accounts often results in severe penalties, including contempt findings and forfeiture of equitable claims.

H2: Summary of Legal, Practical, and Behavioral Guidance

Always Document Transactions

Comprehensive documentation of all financial transactions protects against dissipation claims and strengthens legal credibility. Maintain receipts, bank statements, emails, and written explanations for every significant withdrawal or transfer.

Seek Legal Counsel

Consult a family law attorney before withdrawing significant funds from any account. Legal guidance ensures compliance with jurisdiction-specific rules, reduces litigation risk, and protects long-term financial interests.

Avoid Joint Account Emptying Without Consent

Withdrawing substantial amounts from joint accounts without mutual consent or legitimate justification typically constitutes dissipation. Obtain written consent, document legitimate needs, or seek court approval before large withdrawals.

Plan Financial Actions Strategically to Protect Assets

Strategic financial planning involves assessing account ownership, documenting expenses, separating personal income, and implementing protective measures transparently. Proactive planning reduces emotional decision-making and aligns financial conduct with legal expectations, improving both settlement outcomes and judicial credibility.

Final Note: This content explains general financial and legal principles. Specific rules, thresholds, and outcomes vary by jurisdiction and individual circumstances. Always consult a licensed family law attorney before making financial decisions during divorce proceedings.