Table of Contents

Contents are generated from article headings.

A budgeting method is a systematic framework for dividing income into spending categories, savings targets, and debt obligations — with each method making a distinct trade-off between simplicity and control, automation and awareness, structure and flexibility. No single budgeting method is universally optimal; the right method is the one whose behavioral demands match what the person can sustain.

The most common budgeting failure is choosing the most impressive method rather than the most sustainable one. A loose, imperfect budget maintained for six months consistently produces better financial outcomes than a detailed, precise budget abandoned in January. Method selection is primarily a question of behavioral fit, not theoretical superiority.

This content compares budgeting methods using financial planning frameworks and behavioral research. Individual effectiveness varies based on income type, financial goals, tracking tolerance, and personal preferences. FinQuarry provides informational content only — this does not constitute personalized financial advice.

The Five Major Budgeting Methods

Method 1: The 50/30/20 Rule

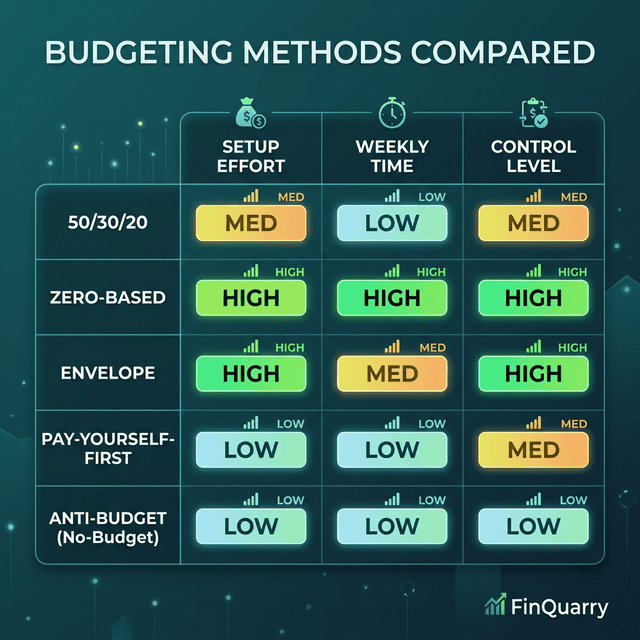

The 50/30/20 rule divides after-tax income by percentage: 50% needs, 30% wants, 20% savings and debt repayment. It requires only three-category monitoring — no transaction-level tracking.

Tracking effort: Low — 5 minutes weekly.

Strongest scenario: A person earning $4,500/month after taxes with $2,100 in fixed costs. The 50/30/20 framework naturally fits: $2,250 needs ceiling, $1,350 wants ceiling, $900 savings minimum. Setup takes 30 minutes; maintenance is minimal.

Breaks when: Housing costs exceed 35% of income (pushing needs above 50%), or the person needs category-level visibility to address specific spending problems.

Method 2: Zero-Based Budgeting

Zero-based budgeting assigns every dollar to a specific category until income minus all allocations equals zero. This produces maximum visibility over where money goes.

Tracking effort: High — 20–30 minutes weekly.

Strongest scenario: A person carrying $8,000 in credit card debt who needs to identify every redirectable dollar. Zero-based visibility reveals that $280/month in dining, subscriptions, and impulse spending can be redirected to debt — cutting payoff time from 11 years (minimums only) to 24 months.

Breaks when: Tracking fatigue sets in (typically 60–90 days), income varies monthly, or the person treats category overages as personal failures rather than adjustment signals.

Method 3: Envelope Budgeting

Envelope budgeting distributes cash into labeled envelopes for each spending category. When an envelope is empty, category spending stops.

Tracking effort: Very low during the month — zero digital tracking. Requires cash handling at each pay period.

Strongest scenario: A person who consistently overspends $200/month on dining using cards. Switching dining to a $150 cash envelope produces an immediate, physical spending ceiling. Consumer research indicates cash spending tends to be 12–18% lower than card spending for identical categories.

Breaks when: Online purchases are frequent, large irregular expenses arise, or carrying significant cash creates safety concerns.

Method 4: Pay-Yourself-First

Pay-yourself-first automates savings and debt payments on payday, then budgets the remainder for spending. The savings amount is the primary decision; spending management is secondary.

Tracking effort: Very low — requires setting up automatic transfers, then spending what remains without category tracking.

Strongest scenario: A person earning $5,000/month who has never successfully saved. Auto-transferring $500 to savings on payday and spending the remaining $4,500 produces $6,000/year in savings with zero daily tracking effort.

Breaks when: The automated savings amount leaves insufficient spending money (causing credit card reliance), or the person needs spending visibility to make informed financial changes.

Method 5: Values-Based Budgeting

Values-based budgeting allocates money according to personal priorities (family, health, career development, experiences) rather than traditional categories. Spending is evaluated by alignment with stated values rather than compliance with percentage targets.

Tracking effort: Moderate — requires both category tracking and ongoing self-assessment.

Strongest scenario: A person frustrated by the needs-vs-wants distinction because personally essential spending (gym membership for mental health, childcare enabling career advancement) is technically a “want.” Values-based framing eliminates this friction.

Breaks when: Values are not clearly defined (making allocation arbitrary), essential costs consume most income, or all spending gets rationalized as “values-aligned,” removing the constraint entirely.

Comparison Matrix

| Factor | 50/30/20 | Zero-Based | Envelope | Pay-First | Values |

|——–|———-|————|———-|———–|——–|

| Setup time | 30 min | 2–4 hrs | 1–2 hrs | 30 min | 1–2 hrs |

| Weekly effort | 5 min | 20–30 min | 5–10 min | 0 min | 15 min |

| Control level | Low | Maximum | Moderate | Low | Moderate |

| Best for debt | Moderate | Excellent | Good | Excellent | Moderate |

| Irregular income | Poor | Moderate | Good | Poor | Moderate |

| Sustainability | High | Moderate | High | Very high | Moderate |

How to Choose: Match Method to Problem

Start with the specific financial problem, not the method’s reputation.

“I never save anything” → Pay-Yourself-First. Automates the savings decision.

“I don’t know where my money goes” → Zero-Based Budgeting. Creates complete dollar-level visibility.

“I overspend on my card without realizing it” → Envelope Budgeting. Removes the abstraction that enables unconscious spending.

“I need a system I’ll actually follow” → 50/30/20 Rule. Minimizes tracking effort, maximizing sustained use.

“Budgeting makes me feel bad about spending on things I care about” → Values-Based Budgeting. Reframes spending as alignment with priorities rather than restriction compliance.

Tracking Tolerance Is the Decision Filter

Predict how much effort you will sustain in week eight — not week one. If past experience shows that detailed tracking leads to budget abandonment, selecting a simpler method produces better financial results through sustained engagement.

Can I Combine Methods?

Method combination is how most sustained budgeters operate in practice. Common effective hybrids:

Pay-yourself-first + 50/30/20: Automate savings on payday, then allocate remaining income using percentage targets. Captures saving discipline with spending structure.

Zero-based + envelope: Use zero-based planning for overall allocation, implement envelopes for problem variable categories only. Captures planning precision with behavioral spending control.

Values-based + any tracking method: Define priorities first, then execute through whichever tracking method fits personal tolerance. Values-based budgeting functions as a decision layer on top of any execution method.

What If Multiple Methods Have Failed?

When multiple methods fail, the problem is typically one of three underlying issues rather than method selection. First, the budget may be mathematically impossible — expenses genuinely exceed income, requiring structural change (income increase or obligation reduction), not a different method. Second, tracking tolerance may be lower than any method requires — in which case, automating everything and checking monthly is the only sustainable approach. Third, the relationship with money may involve financial anxiety that makes any spending-awareness system feel threatening — addressing the anxiety is the prerequisite, not switching methods.

Written by Marcus Tremblay, Senior Financial Analyst | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry