Table of Contents

Contents are generated from article headings.

Invisible overspending is a pattern of unintentional, unrecognized financial outflow through small transactions, subscription accumulation, lifestyle inflation, and frictionless payment technology — typically totaling $200–500/month — that drains budgets without producing any single “big purchase” a person would identify as the problem. Invisible overspending is the most common cause of the experience “I don’t overspend, but I never have money left.”

The mechanism is mathematical: small, frequent, individually reasonable purchases that accumulate to a significant total. A $5 coffee, a $3 app purchase, a $12 lunch, a $8 delivery fee — each individually harmless, collectively consuming $300–500/month that the person cannot account for when reviewing monthly spending.

This content discusses invisible overspending patterns using behavioral economics and consumer finance research. Individual spending patterns and payment environments vary. FinQuarry provides informational content only — this does not constitute personalized financial advice.

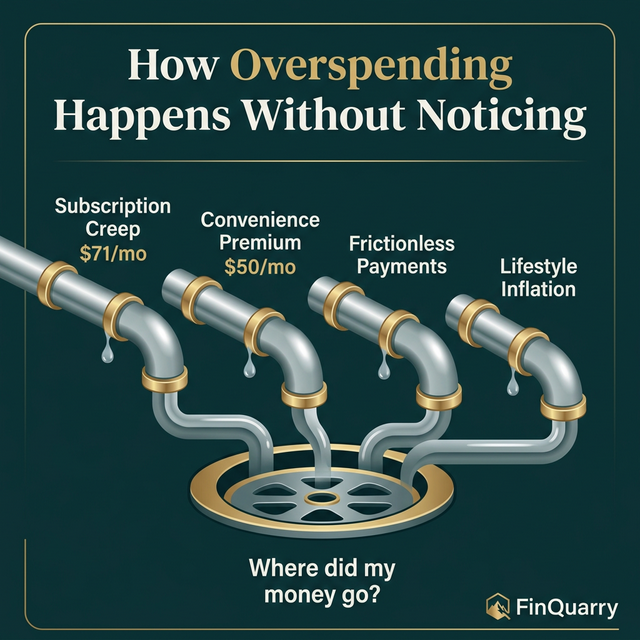

The Four Invisible Spending Mechanisms

Mechanism 1: Subscription Creep

Subscriptions accumulate gradually: one streaming service ($15), then another ($13), a news subscription ($10), a fitness app ($12), cloud storage ($3), a meal planning service ($8), a meditation app ($10). Individually, each provides value. Collectively: $71/month, $852/year — funded through automatic charges that bypass the spending decision entirely.

The average American household carries 6–8 active subscriptions. Subscription audit studies consistently reveal that 30–40% of total subscription spending goes to services used less than twice per month.

Mechanism 2: Convenience Premium

Modern commerce includes embedded convenience costs: delivery fees ($3–8 per order), service charges ($2–5), “small cart” fees ($3–5), and tip-included pricing. A person ordering food delivery twice weekly pays $6–16/week in fees alone — $312–832/year in convenience costs that do not appear as a budget category.

Convenience premium is invisible because each charge is small and bundled with the purchase. The person sees a $25 dinner delivery — not a $18 meal plus $7 in fees.

Mechanism 3: Frictionless Payment Technology

Contactless payments, stored card information, and one-click purchasing reduce the cognitive friction that historically acted as a spending brake. The 2-second delay of physically counting cash provides a “pause moment” that digital payments eliminate.

Research indicates that contactless payments increase transaction frequency by 15–25% compared to cash, not because people want to spend more but because the spending action carries less psychological weight when physical money is not involved.

Mechanism 4: Lifestyle Inflation

Spending increases that match income increases — without conscious decision. A person receiving a $400/month raise who gradually drifts into slightly nicer restaurants, slightly more frequent takeout, and slightly higher grocery quality has absorbed the entire raise into imperceptible lifestyle expansion. The raise produced zero additional savings because spending expanded to meet it.

How to Find the Leaks

The Subscription Audit

Pull credit card and bank statements for 3 months. Highlight every recurring charge. Total them. The number is typically 20–40% higher than the person would have estimated. Cancel or downgrade every subscription used less than twice monthly.

The 30-Day Cash Experiment

For one month, pay for all variable purchases with cash. Withdraw the weekly spending allocation ($75, $100, $150 — whatever the budget allows) and use only physical money. When the cash is gone, spending stops.

Cash experiment participants consistently report spending 15–20% less than their digital payment average — not from deprivation but from the friction of physically counting money creating awareness that digital payments suppress.

The Small Transaction Review

Filter bank statements for transactions under $10. Total them. This number — typically $100–250/month — represents the “I don’t know where the money goes” category. Not every small transaction is wasteful, but the total reveals whether micro-spending is a significant financial drain.

Structural Fixes

The Spending Account Separation

Move variable spending to a dedicated account with a defined monthly allocation. No credit card for daily purchases. The account balance provides a real-time spending gauge without transaction-level tracking.

The 24-Hour Rule for Non-Essential Purchases Over $30

Any non-essential purchase over $30 waits 24 hours. Studies on impulse purchasing indicate that 40–60% of impulse purchases are not completed when a mandatory waiting period is introduced — the emotional urgency dissipates and the purchase loses its appeal.

The Fee Audit

Calculate total delivery fees, service charges, and convenience costs from 3 months of statements. Many people discover $50–150/month in pure friction costs that can be eliminated by batch shopping, cooking at home for 2 additional meals per week, or picking up orders instead of delivery.

Is Invisible Overspending a Discipline Problem?

No. Invisible overspending is a visibility problem amplified by payment technology designed to minimize spending friction. The person is not weak — the system is engineered to make spending easy and invisible. Structural solutions (cash use, account separation, autopay audits) address the system rather than demanding superhuman awareness from the person.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry