Table of Contents

Contents are generated from article headings.

A beginner’s budget is a first-attempt financial plan that allocates income to spending categories, savings, and debt obligations — typically starting with 3–5 broad categories rather than the 15–20 categories that advanced budgets use. Beginner budgeting is learning a skill, not executing perfection: the first budget will be wrong, the second will be less wrong, and by month four the system begins producing reliable financial outcomes.

The most important thing a beginner must understand: the purpose of the first budget is not to control spending. It is to discover spending — to learn where money actually goes so that future budgets can be built from fact rather than assumption.

This content discusses beginner budgeting principles using financial planning fundamentals and behavioral economics. Individual financial situations, income levels, and cost of living vary. FinQuarry provides informational content only — this does not constitute personalized financial advice.

The Three Numbers That Matter Most

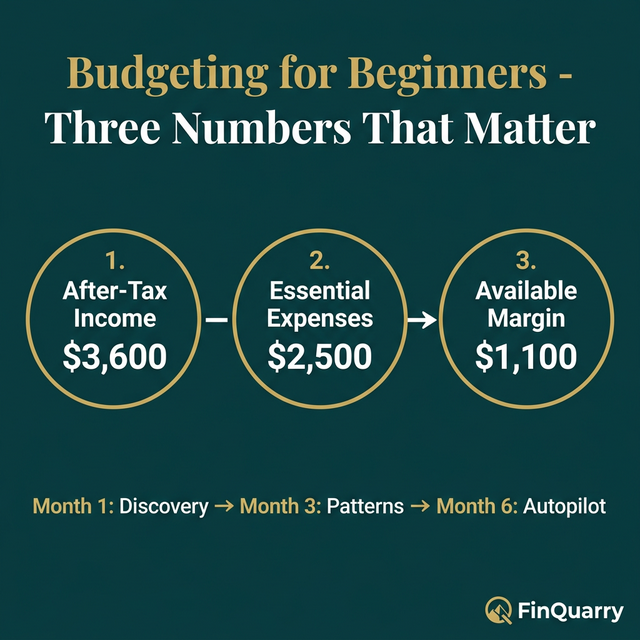

Number 1: After-Tax Monthly Income

Total money received each month after taxes. For a person earning $52,000/year, this is approximately $3,600/month after federal and state taxes (varying by jurisdiction and filing status).

If income varies month-to-month, use the average of the three lowest recent months as the baseline. This prevents building a budget on optimistic income projections.

Number 2: Total Essential Monthly Expenses

The sum of all non-negotiable costs: rent/mortgage, utilities, basic food, transportation, insurance, minimum debt payments. For a person earning $3,600/month, essential expenses typically range from $2,200–2,800 depending on location and obligations.

Number 3: The Difference

Income minus essential expenses = available margin. A person earning $3,600 with $2,500 in essentials has $1,100 of margin. This $1,100 finances savings, debt acceleration, discretionary spending, and irregular expenses. Understanding this single number is more valuable than any budgeting app.

What Month 1 Actually Looks Like

The Discovery Phase

Month 1 is an observation month — track spending without trying to change it. The goal is data collection: “Where does my money actually go?” Common discoveries include subscription costs of $50–120/month that went unnoticed, convenience spending (delivery fees, vending machines, impulse purchases) absorbing $100–300/month, and dining costs 30–50% higher than estimated.

This data forms the factual foundation for month 2’s budget.

The Surprise Budget

Month 1 reveals the gap between perceived and actual spending. This gap — typically $200–500/month across categories — explains why previous casual attempts to “spend less” did not produce savings. The person was budgeting against fiction. Month 1 establishes fact.

How to Build the Month 2 Budget

Use month 1’s actual spending as the starting point. Resist the urge to dramatically cut every category — start with 2–3 modest adjustments:

- If dining was $380, set the budget at $330 (a 13% reduction — achievable)

- If convenience spending was $180, set it at $120 (eliminating the most obviously unnecessary purchases)

- Auto-transfer $150 to savings on payday (before any spending can consume it)

Total savings from three adjustments: $200/month. Not dramatic. Sustainable.

The Week 3 Motivation Dip

Around week three of any new budget, motivation declines and the effort of tracking or restraining spending feels disproportionate to the benefit. This is normal — not a sign of failure.

The dip occurs because novelty fades (the budget is no longer interesting), willpower is depleted (accumulated resistance to spending impulses), and results are not yet visible ($150 in savings does not feel life-changing).

The fix: simplify. If tracking every transaction feels unsustainable by week 3, switch to the one-number budget — just monitor one spending account balance. The person who abandons detailed tracking but maintains savings automation is still succeeding.

The Two Beginner Mistakes That Matter Most

Mistake 1: Starting With a Complex Method

A beginner choosing zero-based budgeting with 15 categories and daily tracking is choosing the most demanding method first. Start with 3–5 categories and weekly review. Complexity can be added later. The first priority is building the habit of financial awareness.

Mistake 2: Treating the First Deviation as Failure

The first budget will have errors. Categories will overshoot. Unexpected expenses will arrive. This is calibration data — information that makes the next month’s budget more accurate. A budget that deviates 20% from plan in month 2 and 8% by month 6 is performing exactly as expected.

What Budget Method Should a Beginner Choose?

Start with the 50/30/20 rule: 50% needs, 30% wants, 20% savings/debt. Three categories. Minimal tracking. Automatic savings on payday. If this produces adequate financial progress, greater complexity is unnecessary. If specific categories repeatedly overshoot, add more granularity to those categories only.

When Will the Budget Start Working?

Months 1–2: Discovery and calibration (expect errors). Month 3: Meaningful patterns emerge as allocations match actual behavior. Months 4–6: The budget begins running with minimal daily effort. By month 6, budgeting should feel like a background system — not a daily project.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry