Table of Contents

Contents are generated from article headings.

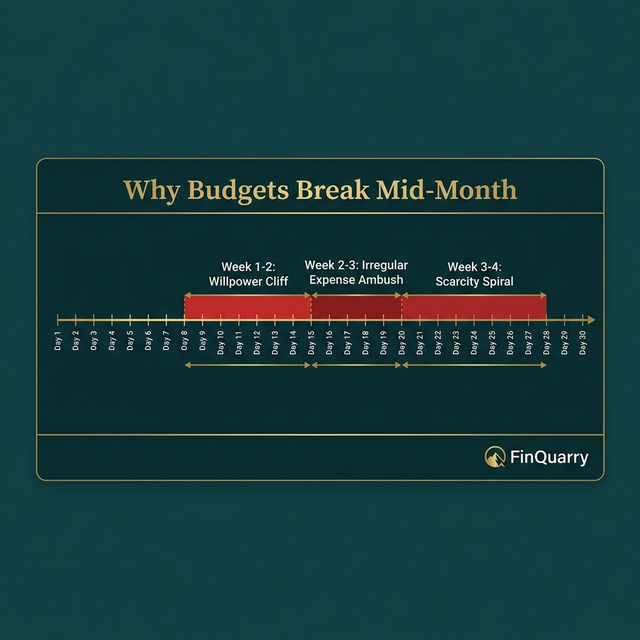

A mid-month budget failure is a predictable collapse pattern where a financial plan functions during the first 10–14 days and then deteriorates — categories overshoot, spending accelerates, and the person either abandons tracking or resorts to credit. Mid-month failure is caused by three structural forces: willpower depletion, irregular expense ambushes, and scarcity-driven behavior shifts — not a lack of commitment.

Understanding these three failure windows transforms mid-month collapse from a personal failing into a diagnosable engineering problem with specific structural fixes.

This content discusses mid-month budget failure using behavioral economics and financial planning principles. Individual spending patterns and psychological responses vary. FinQuarry provides informational content only — this does not constitute personalized financial advice.

Failure Window 1: The Willpower Cliff (Days 10–14)

The Depletion Pattern

Behavioral researchers identify a consistent willpower depletion curve: the person starts the month with renewed commitment (high willpower), maintains restriction through week one (willpower declining), and hits a depletion threshold around day 10–14 where accumulated resistance exhausts cognitive control capacity.

A person whose budget requires 8–12 daily “no” decisions (no coffee out, no convenience meal, no impulse purchase, no app subscription) has made approximately 80–120 resistance decisions by day 10. The cognitive fatigue from this accumulated resistance produces what appears to be “giving up” but is actually resource exhaustion — the same mechanism that makes physical exercise impossible beyond a certain point.

The Structural Fix

Reduce the number of daily decisions the budget requires. Auto-pay all fixed bills (zero decisions). Auto-transfer savings on payday (zero decisions). Set a weekly spending allocation that the person can use freely (zero per-transaction decisions). A budget requiring 2–3 weekly decisions instead of 8–12 daily decisions extends sustainable operation well beyond the day-14 cliff.

Failure Window 2: The Irregular Expense Ambush (Days 15–22)

The Mid-Month Surprise

Non-monthly expenses arrive mid-month with no advance warning in the monthly budget: a $200 medical co-pay, a $150 auto repair deposit, a $90 annual subscription renewal. These costs are predictable annually but invisible in the monthly plan.

When an unfunded $200 expense arrives on day 17, it consumes funds allocated to groceries, gas, or discretionary spending — creating cascading shortfalls across remaining categories. The budget did not fail on day 17. It failed on day 1, when irregular expenses were not pre-funded.

The Structural Fix

Create a sinking fund from last year’s non-monthly expenses totaled and divided by 12. If annual irregular expenses total $3,600, the monthly sinking fund is $300 — set aside on payday, before spending allocations are calculated. The sinking fund absorbs mid-month surprises without disrupting the operating budget.

Failure Window 3: The Scarcity Spiral (Days 22–30)

The “Already Blown It” Response

By day 22, if the budget shows multiple overspent categories, the person enters either resignation mode (“it’s already ruined, so why try”) or panic mode (“I have $120 left for 8 days”). Both responses produce irrational spending behavior: resignation spending ignores limits entirely, while panic hoarding creates anxiety that makes the final week miserable.

A person with $150 remaining on day 22 for a month with 8 days left has $18.75/day — mathematically tight but manageable under normal psychology. Under scarcity psychology, $150 triggers threat responses that make rational allocation harder, not easier.

The Structural Fix

The weekly budget approach divides total monthly spending money into 4–5 weekly envelopes. Each week receives its allocation. Overspending in week one does not visually contaminate weeks three and four. The person evaluates one week at a time rather than facing the demoralizing “remaining for the month” number that triggers scarcity responses.

The Mid-Month Check-In Protocol

A single 10-minute review on day 15 prevents mid-month collapse:

Step 1: Check spending account balance. Is it roughly half of the start-of-month amount?

Step 2: If below half — identify which category overshoot is causing early depletion. Reduce that category for the remaining two weeks.

Step 3: If irregular expenses hit — assess whether the sinking fund covered them. If not, adjust the sinking fund amount for next month.

This single mid-month data point prevents the silent drift that produces week-four crisis.

How to Budget Weekly Instead of Monthly

Weekly budgeting is the most effective prevention for all three failure windows:

Total monthly spending money (after fixed bills and savings) ÷ 4.3 = weekly allocation. A person with $1,200 in monthly spending money gets approximately $280/week. Each week resets — last week’s overage does not contaminate this week’s allocation.

Weekly budgeting reduces the planning horizon from 30 days (cognitively demanding) to 7 days (manageable), provides more frequent reset points, and prevents the “month is already ruined” psychology that drives late-month budget abandonment.

Is It Normal for Budgets to Break Mid-Month?

Mid-month failure is one of the most common budgeting experiences — it reflects structural design issues present in most first-attempt budgets rather than personal failing. The person experiencing mid-month collapse is not undisciplined. The budget is under-engineered for the predictable forces acting on it.

Written by Sarah Mitchell, Financial Content Strategist | Reviewed by Riley Thompson, Editor & Compliance Reviewer, FinQuarry