Table of Contents

Contents are generated from article headings.

Saving money feels hard psychologically because the human brain is structured to prioritize immediate rewards over delayed ones. Saving money psychology reveals a fundamental mismatch between evolutionary cognitive design and modern financial requirements: the brain evolved to value certainty, immediacy, and tangible resources — qualities that spending provides — over abstraction, delay, and intangibility — qualities that define the experience of saving. This mismatch means that the difficulty of saving is not primarily a willpower problem or an income problem; it is a cognitive architecture problem.

Saving requires a person to voluntarily reduce their present resources in exchange for a future benefit they cannot see, touch, or experience. The cost of saving is immediate and concrete (less money available now), while the reward is delayed and abstract (more money available later). Every other financial action — spending, paying bills, investing — produces an immediate, tangible outcome that the brain registers as reinforcement. Saving produces no immediate outcome; it produces the absence of action. The brain does not reward inaction, which is why saving feels effortful in a way that spending does not.

Scope and Context: This content discusses the psychology of saving using behavioral economics research, cognitive science frameworks, and financial planning principles. Financial products, interest rates, and economic conditions vary by jurisdiction and change over time. Readers should evaluate saving strategies in the context of their own financial circumstances and current economic environment.

Present Bias: Why the Brain Devalues Future Money

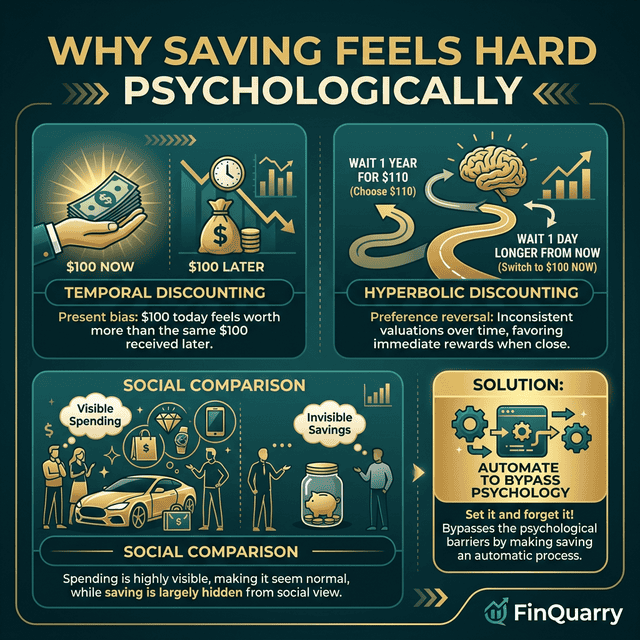

Present bias is the systematic tendency to assign greater value to rewards available now compared to equivalent or larger rewards available in the future. Present bias is one of the most extensively documented findings in behavioral economics, and it is the primary cognitive mechanism that makes saving feel difficult.

How Present Bias Operates in Financial Decisions

Present bias causes a person to prefer $100 today over $110 tomorrow — even though waiting one day produces a 10% return, which vastly exceeds any available market return. The same person, when offered a choice between $100 in 30 days versus $110 in 31 days, will often choose to wait the extra day for the larger amount. The objective trade-off is identical in both cases (one additional day for $10 more), but the first scenario involves receiving money now, which activates the brain’s immediate-reward circuits and overrides the analytical calculation.

Present bias produces specific saving difficulties. When a person receives income, the choice between spending it now and saving it for later is not evaluated objectively — the immediate spending option receives a psychological “bonus” from the brain’s reward system that the saving option does not. This bonus is not a conscious choice; it is an automatic neurological response that makes spending feel more rewarding than saving regardless of whether the person intellectually understands that saving is more beneficial for their long-term financial position.

Hyperbolic Discounting and the Savings Gap

The specific mathematical pattern through which present bias devalues future rewards is called hyperbolic discounting. Unlike rational (exponential) discounting — where the discount rate is constant across time periods — hyperbolic discounting applies a steep discount rate to near-term delays and a shallow discount rate to distant-term delays.

The practical effect for saving is that the psychological “cost” of saving feels highest for money that is available right now, and decreases for money that is not yet available. This is why Richard Thaler and Shlomo Benartzi’s “Save More Tomorrow” program — which asks people to commit to saving a percentage of future raises rather than current income — dramatically increases savings rates. The program works because future money is already hyperbolic-discounted: people discount the value of money they don’t yet have, so committing to save it feels less costly than saving money they currently possess.

The Scarcity Perception Problem

Saving feels harder when a person perceives their resources as scarce — and perception of scarcity is governed by cognitive factors that do not necessarily correspond to actual income levels.

Why Higher Income Does Not Automatically Make Saving Easier

If saving difficulty were purely an income problem, higher-income individuals would find saving proportionally easier. In practice, savings rates do not increase proportionally with income because lifestyle inflation — the automatic expansion of spending to match available income — absorbs income increases before they can be directed to savings. Lifestyle inflation operates as a money habit: it is automatic, unconscious, and driven by social comparison rather than by deliberate evaluation of whether each additional expenditure improves well-being.

The Federal Reserve’s Survey of Household Economics and Decisionmaking (SHED) has consistently documented that a significant percentage of adults across income levels report difficulty covering an unexpected $400 expense — indicating that the subjective experience of financial scarcity extends well into middle and upper-middle income ranges where objective scarcity does not exist.

Cognitive Bandwidth and Saving Capacity

Behavioral economists Sendhil Mullainathan and Eldar Shafir demonstrated that the perception of scarcity — whether financial, temporal, or material — reduces cognitive bandwidth: the mental processing capacity available for complex decisions. When a person perceives their financial resources as scarce, their brain allocates disproportionate cognitive resources to managing immediate needs, leaving less bandwidth for the analytical processing required to plan, prioritize, and execute saving behavior.

This bandwidth reduction creates a paradox: the people who would benefit most from saving (those with fewer financial reserves) experience the greatest cognitive barriers to saving, because their perception of scarcity consumes the mental resources that saving requires. This is not a character failure — it is a documented cognitive consequence of perceived resource constraint.

The Visibility and Feedback Problem

Saving produces no visible, immediate feedback — and the absence of feedback is psychologically experienced as the absence of progress.

Spending Feedback vs. Saving Feedback

Every spending action produces immediate, multimodal feedback: a new possession, a service received, social recognition, a dopamine release from the novelty of acquisition. The brain registers spending as an event — something happened, something was gained, the action produced a result.

Saving produces no equivalent feedback signal. The person’s bank balance increases by a number, but the number itself does not trigger the brain’s reward system in the same way that a tangible acquisition does. There is no novelty, no social visibility, no sensory experience associated with the act of saving. The brain treats saving as non-action — nothing happened — and non-action does not receive reinforcement from the dopamine system that governs motivation and habit formation.

This feedback asymmetry explains why people often “know” they should save more but consistently fail to do so: the knowledge is analytical (System 2), while the motivation system operates on experiential feedback (System 1), and saving provides no experiential feedback for System 1 to process. The resulting emotional dissonance between knowing and doing is a central feature of saving difficulty.

The Intangibility of Future Self

Saving is fundamentally an act of transferring resources from the present self to the future self — but the brain processes the future self as a partially separate entity. Neuroimaging research has shown that when people think about their future selves, the brain regions that activate are more similar to the regions activated when thinking about a stranger than when thinking about the current self.

This neural “stranger” effect means that saving for retirement, for example, feels psychologically similar to giving money to someone else — a generous act, perhaps, but not a personally rewarding one. The future self who will benefit from today’s savings does not feel like “me” in the way that the present self who wants to spend the money does. This temporal self-discontinuity is a deep source of saving difficulty that operates independently of income, education, or financial knowledge.

Social Comparison and Saving Undermining

Social comparison — the automatic tendency to evaluate one’s financial position relative to peers — systematically undermines saving by creating pressure to spend at peer-group levels regardless of personal financial goals.

Lifestyle Reference Groups and Spending Pressure

Each person’s lifestyle is benchmarked against a reference group — the social peer set whose consumption patterns establish “normal” spending levels. When a person’s reference group spends at a level that consumes most of their income, maintaining social parity requires spending at the same level, leaving little room for saving. The pressure is not experienced as peer pressure in the explicit sense — it is experienced as a sense of normalcy. Not going to restaurants, not taking vacations, not buying new devices feels like deprivation relative to the reference group’s baseline, even when those activities are optional.

Social media amplifies reference group pressure by making consumption patterns visible across much larger and more aspirational peer networks. A person’s effective reference group expands from the people they interact with daily to hundreds or thousands of social connections whose curated spending is on constant display. This expanded reference creates upward pressure on “normal” spending levels, which directly compresses the margin available for saving.

The Keeping-Up Paradox

The keeping-up paradox is the observation that consuming at peer-group levels often requires consuming at a rate that prevents wealth accumulation — meaning that the behavior designed to signal financial success (spending at peer level) actually prevents financial success (wealth building through saving). Many high-income, high-spending households maintain the appearance of wealth while accumulating little actual net worth — a pattern documented extensively in research on irrational money decisions and underscored by the distinction between income and wealth.

The Pain-of-Not-Spending Problem

Saving requires saying “no” to spending opportunities — and each “no” triggers a psychological response called reactance. Reactance is the automatic negative emotional reaction to perceived restriction of freedom. When a person decides not to buy something they want in order to save the money instead, the brain registers the decision not as a positive action (saving) but as a negative restriction (loss of the option to buy).

Opportunity Cost Neglect

People are systematically poor at recognizing opportunity costs — the things they could have done with money they spent. When a person spends $200 on a dinner, they do not automatically register that the $200 could instead have been added to savings. The dinner produces an experience; the alternative (saving) produces nothing visible. This opacity of opportunity costs means that each spending decision is evaluated in isolation rather than as a trade-off against saving, making saving feel like it gets “none” of the money while spending gets “all” of it.

Effective saving frameworks counteract opportunity cost neglect by making the trade-off visible. Automated savings transfers — which remove money from the spending-available pool before the person experiences it as available — eliminate the trade-off experience entirely. The person never perceives the money as available to spend, so saving it does not trigger the reactance or opportunity cost neglect that manual saving produces. This approach leverages the same default-setting principles used in mental accounting to reshape behavior without requiring sustained willpower.

Evidence-Based Approaches to Making Saving Psychologically Easier

The cognitive barriers to saving are structural — they arise from the architecture of the brain rather than from individual character — so effective interventions must be structural rather than motivational.

Automate to Bypass Present Bias

Automatic savings transfers executed before income reaches the spending-available pool bypass present bias by removing the decision point where present bias operates. When saving is automatic, the person does not experience the choice between spending now and saving for later — the saving happens without requiring the brain to overcome its preference for immediate rewards. The “Save More Tomorrow” framework extends this principle by automating future increases in saving rates, leveraging hyperbolic discounting (future money feels less costly to commit) to build savings rates over time.

Make Saving Visible Through Feedback Systems

Creating visual feedback for saving progress counteracts the invisibility problem by giving the brain something to register as a reward signal. Progress bars showing movement toward a savings goal, milestone notifications when savings thresholds are reached, and visual projection tools showing the future value of current savings all create experiential feedback that the brain’s reward system can process.

Reduce the Psychological Distance to Future Self

Strategies that reduce the neural “stranger” effect of the future self can increase the motivation to save. Research suggests that visualizing the future self in concrete, specific terms — not “retirement someday” but “living independently at 75 with specific activities and specific living arrangements” — reduces the temporal self-discontinuity and increases the psychological reward of saving. Financial planning tools that project specific lifestyle outcomes based on current saving rates make the future self’s needs feel more real and personally relevant, and connect to the broader principles of understanding money psychology.

Use Loss Framing Instead of Gain Framing

Because loss aversion makes people approximately twice as responsive to potential losses as to potential gains, framing saving in terms of what will be lost by not saving (loss frame) is more motivating than framing it in terms of what will be gained by saving (gain frame). “If you don’t save $500/month, you will lose approximately $X in retirement purchasing power” produces stronger behavioral response than “If you save $500/month, you will gain approximately $X.” The content is identical; the psychological impact differs because loss aversion creates stronger motivation to avoid a loss than to pursue a gain.

Why Does Saving Feel Like Deprivation Even When Income Is Sufficient?

Saving feels like deprivation because the brain evaluates financial decisions relative to a reference point — the spending level that feels “normal.” If a person’s reference spending level equals their income, any saving requires spending below what feels normal, which the brain registers as a loss relative to the reference point. This reference-dependent evaluation means that saving will feel like deprivation at any income level unless the person’s reference spending level is recalibrated to a point below their income, creating psychological room for saving without the feeling of loss.

Is Willpower a Reliable Strategy for Saving?

Willpower is not a reliable long-term saving strategy because willpower is a depletable cognitive resource that functions at its lowest when the person is stressed, fatigued, or emotionally depleted — precisely the conditions that most frequently trigger impulse spending. Research in self-regulation demonstrates that people who rely on willpower for financial discipline experience progressive degradation in saving behavior over time as their self-control reserves are consumed by other life demands. Structural approaches — automation, defaults, environment design — are more effective because they do not require willpower to execute.

At What Income Level Does Saving Become Psychologically Easy?

No income level eliminates the psychological difficulty of saving, because the barriers are cognitive rather than financial. Lifestyle inflation ensures that spending reference points expand with income, maintaining the subjective experience of financial constraint regardless of objective income level. Surveys consistently document that individuals at all income levels report difficulty saving, though the specific barriers differ: lower-income individuals face genuine resource constraints, while higher-income individuals face reference-point inflation and expanded lifestyle expectations. The psychological difficulty of saving is a constant; only the specific mechanism producing that difficulty changes with income.

How Long Does It Take to Build a Saving Habit?

Building a saving habit follows the same neurological timeline as other habit formation: research indicates an average of approximately 66 days, with a range from 18 to 254 days depending on behavioral complexity and individual factors. The critical period for saving habit formation is the first 30 days — the period when the behavior is most fragile and most likely to be abandoned. Automating the saving behavior during this critical period removes the fragility by ensuring the behavior continues regardless of the person’s motivational state. After the saving has been automated long enough to become an accepted part of the financial landscape, it transitions from a deliberate action to a perceived default, at which point it no longer requires conscious effort to maintain.