Table of Contents

Contents are generated from article headings.

Risk perception in personal finance is the subjective process through which individuals evaluate the likelihood and severity of financial threats and opportunities. Financial risk perception differs fundamentally from objective risk measurement because it is filtered through cognitive biases, emotional states, past experiences, and social influences that systematically distort how people interpret financial uncertainty. Two people facing identical financial options — the same investment, the same insurance decision, the same debt structure — will perceive the risks differently based on their psychological risk profile, not the mathematical probabilities involved.

Financial risk perception determines behavior more reliably than financial risk analysis. A person who objectively understands that long-term equity investment has historically produced positive returns may still avoid investing if their subjective risk perception codes equities as “dangerous.” Conversely, a person who understands that concentrated positions carry high risk may still hold them if their subjective perception codes concentration as “conviction.” The gap between perceived risk and actual risk is the source of most systematic financial errors in personal finance.

Scope and Context: This content discusses financial risk perception using behavioral economics research, cognitive psychology frameworks, and established financial planning principles. Financial products, regulations, and market conditions vary by jurisdiction and institution. Risk tolerance assessments and investment strategies should be evaluated with appropriate professional guidance.

How the Brain Processes Financial Risk

The brain processes financial risk through two competing systems that evaluate uncertainty differently. Daniel Kahneman’s dual-process framework — System 1 (fast, automatic, emotional) and System 2 (slow, deliberate, analytical) — explains why financial risk perception often contradicts financial risk analysis.

System 1 Risk Processing: The Emotional Response

System 1 evaluates financial risk through affect — the immediate emotional feeling (positive or negative) that a financial situation produces. When System 1 encounters a financial option, it generates a gut-level risk assessment based on associative memory: does this situation feel similar to something that produced a good or bad outcome in the past? If it triggers a negative affective association, System 1 codes it as “risky” regardless of the objective probability involved.

System 1 risk processing is fast, automatic, and useful for simple threats — but systematically unreliable for financial decisions that involve compound probabilities, delayed outcomes, or statistical base rates. The feeling that an investment is “dangerous” or “safe” provides no information about its actual risk-return profile, yet System 1 presents that feeling with the certainty of a factual judgment.

System 2 Risk Processing: The Analytical Response

System 2 processes financial risk through deliberate calculation — evaluating probabilities, comparing historical returns, assessing correlation structures, and modeling potential outcomes. System 2 risk processing produces more accurate risk assessments but requires cognitive effort, time, and access to relevant data. Because System 2 is cognitively expensive, the brain defaults to System 1 risk judgments for most financial decisions, particularly those that feel familiar, routine, or urgent.

The interaction between the two systems creates a specific vulnerability: System 1 generates an immediate risk judgment, and System 2 is often recruited not to independently evaluate the risk but to rationalize the judgment System 1 has already produced. This “motivated reasoning” pattern means that a person who feels that an investment is too risky will use System 2 to find analytical reasons supporting that feeling, rather than using System 2 to independently assess whether the feeling is accurate.

Prospect Theory and Asymmetric Risk Perception

Prospect theory, developed by Daniel Kahneman and Amos Tversky, provides the most empirically validated framework for understanding how people perceive financial risk asymmetrically. Prospect theory identifies three systematic distortions in risk perception that affect virtually all personal finance decisions.

Loss Aversion in Risk Assessment

Loss aversion — the tendency to experience potential losses as approximately twice as psychologically impactful as equivalent potential gains — fundamentally distorts financial risk perception. A financial option with a 50% chance of gaining $1,000 and a 50% chance of losing $1,000 has an expected value of zero, yet most people perceive this option as net-negative because the psychological weight of the potential loss exceeds the psychological weight of the potential gain.

Loss aversion produces specific risk perception distortions in personal finance. People overinsure against low-probability losses (purchasing extended warranties where the expected payout is far below the premium cost). People underinvest in risk-appropriate assets because the possibility of loss dominates their perception even when the probability-weighted expected return is strongly positive. People hold losing positions indefinitely because realizing the loss would convert a perceived “temporary” situation into a definitive one — which loss aversion makes disproportionately painful. These patterns connect directly to the cognitive biases that undermine financial decision-making.

Reference Point Dependence

Prospect theory demonstrates that people evaluate financial risk relative to a reference point — typically their current financial position — rather than in absolute terms. The same financial outcome is perceived as a gain or a loss depending on the reference point from which it is evaluated.

A person earning $80,000 who receives a job offer at $90,000 perceives a gain. The same person, if they had been earning $100,000, would perceive the $90,000 offer as a loss — even though the absolute financial position is identical. Reference point dependence means that risk perception is not driven by where a financial outcome would place a person objectively, but by whether the outcome represents an improvement or deterioration relative to where they currently are (or where they expect to be).

Probability Weighting Distortion

People systematically overweight small probabilities and underweight moderate-to-high probabilities when assessing financial risk. This probability weighting distortion explains why people simultaneously buy lottery tickets (overweighting the tiny probability of a large gain) and buy excessive insurance (overweighting the small probability of a large loss). Both behaviors are risk-perception errors driven by the same underlying mechanism: small probabilities receive more psychological weight than their mathematical size justifies.

Probability weighting also distorts investment risk perception. Investors overweight the probability of catastrophic market events (crashes, collapses) relative to their actual historical frequency, which causes them to maintain excessively conservative allocations. Simultaneously, investors overweight the probability of exceptional returns from concentrated positions, which causes periodic episodes of speculative overallocation — the same fear and greed dynamic that drives market cycles.

Factors That Shape Individual Risk Perception

Financial risk perception varies systematically across individuals based on factors that have little to do with objective financial analysis.

Past Experience and the Availability Heuristic

Personal financial history is the strongest determinant of individual risk perception. The availability heuristic causes people to judge the probability of financial events based on how easily relevant examples come to mind — and personal experiences are the most cognitively available examples. A person who lost money in a real estate investment perceives real estate as riskier than a person who gained money in real estate, even when both are evaluating the same current market conditions.

This experience-driven distortion explains why past experiences shape money behavior far more powerfully than statistical education. A person who has intellectually learned that the long-term average stock market return is approximately 10% annually may still perceive stocks as “too risky” if their personal experience includes a significant loss — because the availability heuristic prioritizes experiential data over statistical data.

Time Horizon and Temporal Discounting

Risk perception changes systematically based on the time horizon of the financial decision. Near-term financial outcomes receive disproportionate psychological weight compared to distant-term outcomes — a phenomenon called temporal discounting. A potential loss that could occur next month feels more risky than the same potential loss in 20 years, even though the objective risk may be identical or even lower in the short term.

Temporal discounting distorts risk perception particularly in retirement planning. The risk of outliving savings is objectively one of the most significant financial risks a person faces, but because the threat is decades away, it receives less psychological weight than near-term risks like market volatility or unemployment. The result is a systematic underestimation of longevity risk and overestimation of market risk in retirement planning decisions.

Emotional State and Affect-Driven Risk Perception

A person’s current emotional state directly influences their financial risk perception independent of any change in objective circumstances. Anxiety increases risk perception across all financial domains — a person who is anxious about their job perceives investment risk, spending risk, and borrowing risk as higher than the same person in a calm state evaluating the same options.

Conversely, positive emotional states decrease risk perception. A person who has recently experienced a financial success (bonus, investment gain, raise) perceives financial risks as lower — not because the risks have changed, but because the positive affect creates a generalized “things will work out” cognitive bias. This affect-driven risk cycling — overperceiving risk when anxious, underperceiving risk when optimistic — produces the systematic behavioral pattern of buying high (when optimism reduces risk perception) and selling low (when fear amplifies it).

Common Risk Perception Errors in Personal Finance

Several specific risk perception errors recur across personal finance domains because they arise from fundamental features of human cognitive architecture rather than from individual knowledge deficits.

Familiarity Bias in Risk Assessment

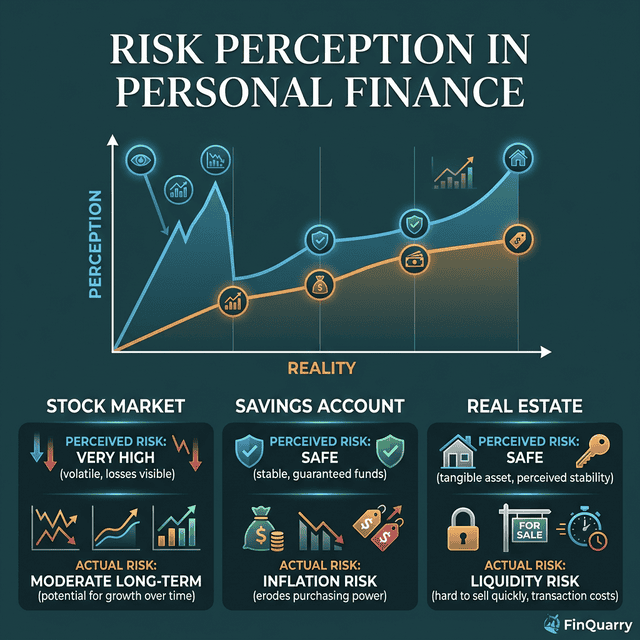

People perceive familiar financial products and structures as less risky than unfamiliar ones, independent of actual risk profiles. A person may perceive a savings account as “safe” and a diversified equity fund as “risky” — when in reality, the savings account carries inflation erosion risk (purchasing power declines over time) while the diversified equity fund, held long-term, has historically preserved and grown purchasing power.

Familiarity bias produces home-country bias in investing (overweighting domestic equities because they feel familiar), employer-stock concentration (employees feel their company’s stock is less risky because they know the company), and product-type bias (favoring financial products that resemble things they have used before, like savings accounts, over products that are unfamiliar, like index funds).

Denominator Neglect

Denominator neglect is the tendency to focus on event magnitude (numerator) while ignoring event frequency (denominator). A headline reporting “$2 billion lost in crypto hack” increases crypto risk perception even if the denominator — total crypto market capitalization or number of users who were not affected — renders the event statistically marginal. Denominator neglect explains why dramatic, low-probability financial events (bank failures, flash crashes, Ponzi scheme collapses) disproportionately influence risk perception compared to undramatic, high-probability risks (inflation erosion, fee drag, inadequate savings rates).

Risk Compensation Behavior

Risk compensation is the behavioral tendency to increase risk-taking when a safety measure is introduced, partially or fully offsetting the safety measure’s benefit. In personal finance, risk compensation occurs when a person who has purchased insurance or built an emergency fund perceives their overall financial position as safer and consequently takes larger risks in other areas.

How to Calibrate Risk Perception in Financial Decisions

Risk perception cannot be made perfectly accurate — it is a subjective process embedded in human cognitive architecture — but it can be calibrated through structural approaches that introduce objective data into the assessment process.

Pre-Commitment to Risk Rules

Establishing predetermined rules for financial risk decisions — such as maximum position sizes, minimum diversification requirements, or mandatory waiting periods for high-risk decisions — removes the decision point where distorted risk perception would otherwise operate. The rule was created during a neutral cognitive state and executes regardless of the person’s emotional risk perception at the moment of decision.

Base Rate Consultation

Before making a risk-influenced financial decision, consulting statistical base rates — historical return distributions, insurance claim frequencies, default rates — provides System 2 with objective data that can counterbalance System 1’s experiential risk judgment. Base rate consultation does not eliminate affective risk perception, but it creates a cognitive friction point where the person must reconcile their feeling about the risk with the data about the risk.

Scenario Modeling with Probability Weights

Explicitly assigning probability weights to potential outcomes and calculating expected values forces System 2 engagement and counteracts the probability weighting distortion. Rather than asking “How do I feel about this risk?”, the person asks “What is the probability of each outcome, and what is the probability-weighted expected value?” This reframing shifts the evaluation from affect-based to analysis-based, reducing — though not eliminating — the influence of subjective risk perception. This approach is particularly effective when combined with understanding how mental accounting compartmentalizes financial thinking.

What Is the Difference Between Risk Tolerance and Risk Perception?

Risk tolerance is the amount of financial risk a person can objectively afford to take given their financial position, time horizon, liquidity needs, and income stability. Risk perception is the subjective experience of how risky a financial option feels. The two often diverge: a young person with a 40-year investment horizon and stable income has high objective risk tolerance but may have low risk perception tolerance if their formative experiences included financial loss. Effective financial planning requires assessing both dimensions — the person’s objective capacity to absorb risk and their subjective willingness to experience the emotional discomfort that risk creates.

Can Risk Perception Be Trained Over Time?

Risk perception can be recalibrated through repeated exposure to outcomes that contradict the current perception — a process called “experiential updating.” A person who perceives stock market investing as extremely risky may gradually recalibrate their perception through the experience of maintaining a diversified portfolio across market cycles and observing that temporary losses recovered over time. However, this recalibration is fragile: a single severe negative experience can reset risk perception to its baseline fear-state faster than years of positive experience built it up, because negative experiences are encoded more strongly than positive ones due to the brain’s negativity bias.

How Does Media Coverage Affect Financial Risk Perception?

Media coverage systematically distorts financial risk perception through availability bias amplification. Financial media disproportionately covers dramatic, negative financial events (crashes, fraud, failures) relative to normal, positive financial outcomes (steady growth, dividend payments, debt repayment). This coverage asymmetry creates a distorted information environment where dramatic risks are cognitively overavailable, causing consumers to overperceive the probability and severity of dramatic financial events while underperceiving gradual, undramatic risks that may actually have larger cumulative impact on their financial outcomes.

Does Higher Financial Knowledge Reduce Risk Perception Errors?

Higher financial knowledge reduces some risk perception errors — particularly those caused by misunderstanding financial products or probability concepts — but does not eliminate the affective and experiential components of risk perception. A person with extensive financial knowledge will still experience loss aversion, will still be influenced by reference point dependence, and will still overweight dramatic low-probability events. Knowledge provides tools for recognizing when risk perception may be distorted, but it does not prevent the distortion from occurring at the automatic processing level.