Table of Contents

Contents are generated from article headings.

Past experiences shape money behavior through deeply encoded psychological patterns that operate below conscious awareness. Past experiences — particularly those from childhood and formative financial events — create internal frameworks called money scripts that automatically guide financial decisions throughout adulthood. These scripts form when a person’s brain associates specific emotional responses with financial situations, encoding those associations into long-term memory patterns that activate whenever similar financial situations arise later in life.

Money behavior psychology reveals that most financial behaviors are not the result of rational cost-benefit analysis. Financial behaviors are driven by emotional conditioning, learned associations, and cognitive patterns that formed years or decades before the person makes a given financial decision. Understanding how past experiences create these patterns is the first step toward identifying which current financial behaviors are serving present goals and which are replaying outdated responses to circumstances that no longer exist.

Scope and Context: This content discusses how past experiences influence financial behavior using financial psychology research, behavioral economics frameworks, and clinical findings from financial therapy. Financial products, regulations, and economic conditions vary by jurisdiction and institution. Readers should evaluate behavioral patterns in the context of their own financial circumstances and personal history.

What Are Money Scripts and How Do They Form?

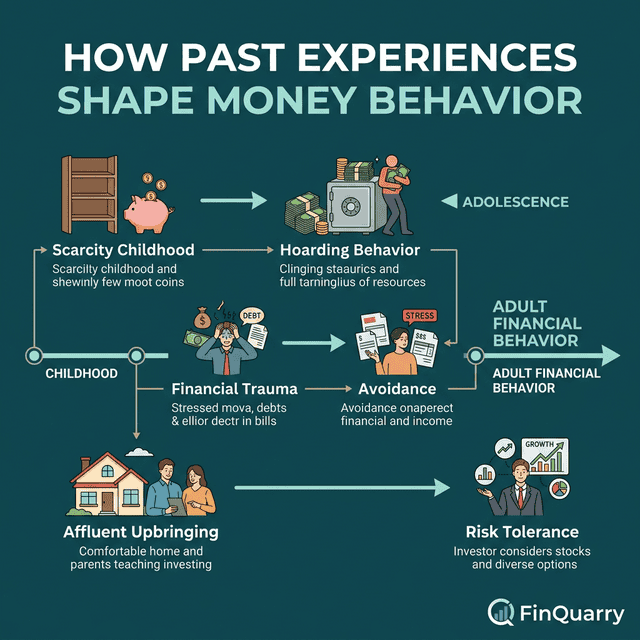

Money scripts are unconscious beliefs about money that are typically formed in childhood and continue to guide financial decisions throughout adulthood. Financial psychologists Brad Klontz and Ted Klontz identified money scripts as the core mechanism through which past experiences translate into current financial behavior. Money scripts form during “financial flashpoint” experiences — emotionally charged events involving money that encode specific beliefs about what money means, what it can do, and what role it should play in a person’s life.

The Four Money Script Patterns

Money avoidance scripts develop when a person’s formative experiences associate money with negative outcomes — conflict, guilt, corruption, or moral compromise. A person who grew up in a household where money was a source of constant conflict between parents may develop the unconscious belief that money is inherently destructive. Money avoidance scripts can produce behaviors like chronic under-earning, giving away money compulsively, financial denial, or sabotaging financial opportunities that could increase wealth.

Money worship scripts form when early experiences associate more money with the resolution of problems, the achievement of happiness, or the elimination of negative emotional states. A person who experienced childhood poverty may develop the belief that acquiring enough money would have prevented the suffering they experienced. Money worship scripts can drive compulsive earning, overwork, excessive spending to “enjoy” money, or chronic dissatisfaction with any level of financial achievement — because the belief that “more money equals more happiness” has no internal limit.

Money status scripts develop when past experiences connect financial position with personal identity, social worth, or self-esteem. A person who experienced social exclusion based on their family’s financial position may develop a script equating net worth with personal value. Money status scripts produce behaviors like overspending to project an image of wealth, taking on debt to maintain appearances, and experiencing shame about financial reality when it does not match the projected image. This pattern directly connects to emotional spending behavior.

Money vigilance scripts form when formative experiences emphasize the importance of financial caution, secrecy, and preparedness for worst-case scenarios. Money vigilance produces excessive saving, anxiety about spending, refusal to discuss financial matters, and difficulty enjoying financial security even when it exists. While vigilance can produce positive financial outcomes (higher savings rates), excessive vigilance creates its own form of financial dysfunction — the person accumulates resources but cannot deploy them toward goals that would improve quality of life.

How Childhood Financial Experiences Create Adult Patterns

Childhood financial experiences create adult behavioral patterns through a process called financial socialization — the transmission of financial values, attitudes, and behaviors from the family environment to the developing child. Financial socialization occurs through three channels: direct instruction (explicit teachings about money), modeling (observing how caregivers handle money), and experiential learning (the child’s own early financial experiences within the family system).

Parental Financial Behaviors as Templates

Children encode their parents’ financial behaviors as templates for “how money works” long before they have the cognitive capacity to evaluate those behaviors critically. A child who observes a parent hiding purchases from a partner learns that spending requires secrecy. A child who watches a parent check bank balances repeatedly and express anxiety learns that financial monitoring is a source of stress rather than a tool for awareness. A child whose family celebrates financial windfalls with immediate spending learns that unexpected money exists to be spent, not saved.

These observational templates operate through the same modeling mechanism that governs language acquisition and social behavior — the child’s mirror neuron system encodes observed patterns as behavioral templates regardless of whether the observed behavior is effective, rational, or healthy. The patterns persist into adulthood because they were encoded before the person developed the ability to critically evaluate them.

Financial Trauma and Its Long-Term Effects

Financial trauma is the lasting psychological impact of severely negative financial experiences — events like bankruptcy, foreclosure, sudden job loss, or being raised in persistent poverty. Financial trauma operates through the same neurological mechanisms as other forms of trauma: the amygdala encodes the threatening experience as a survival-relevant memory, and subsequently triggers alarm responses when any similar financial situation arises.

A person who experienced foreclosure during childhood may develop a persistent fear response around housing costs that causes them to either avoid homeownership entirely (avoidance response) or obsessively overpay for housing security (overcompensation response). Neither response is objectively rational — both are automatic reactions to an encoded trauma pattern. An Experian survey found that a significant percentage of U.S. adults report experiencing financial trauma, with younger generations reporting higher rates of money-related stress and anxiety — suggesting that financial trauma is widespread and multigenerational.

Financial trauma is distinct from financial stress. Financial stress is the cognitive and emotional response to current financial difficulty. Financial trauma is the persistent activation of stress responses in financial situations that are no longer objectively threatening — the threat exists in the encoded memory, not in the present circumstance. This distinction matters because trauma-driven financial behaviors require different interventions than stress-driven behaviors, as discussed in the context of financial anxiety.

How Past Experiences Distort Financial Risk Assessment

Past experiences systematically distort how people assess financial risk by creating availability biases — the tendency to judge the probability of an event based on how easily examples come to mind rather than on actual statistical frequency.

The Recency and Availability Effect

A person who experienced a significant investment loss assigns a higher probability to future investment losses than statistical data would support — not because they have analyzed the data differently, but because their personal experience makes investment loss cognitively “available” as an outcome. Conversely, a person whose early investment experiences were profitable may underestimate investment risk because loss is not readily available in their experiential memory.

This experience-driven risk perception distortion explains generational differences in financial behavior. People who lived through the 2008 financial crisis exhibit measurably different savings and investment behaviors than people who entered adulthood during bull markets — the crisis experience created an availability bias that persistently skews risk assessment toward caution, even years after market recovery.

Scarcity Mindset from Past Deprivation

Past experiences of financial scarcity create a cognitive pattern that behavioral economists Sendhil Mullainathan and Eldar Shafir describe as a “scarcity mindset” — a persistent, automatic focus on immediate resource management that narrows attention and reduces the cognitive bandwidth available for long-term financial planning.

A person who grew up in poverty may continue to operate with a scarcity mindset even after achieving financial stability. The scarcity mindset produces specific behavioral patterns: difficulty planning beyond the current pay period, reluctance to invest in long-term financial instruments, tendency to deplete resources quickly rather than accumulate them (“resource capture” behavior), and difficulty distinguishing between genuine scarcity and perceived scarcity. The mindset was adaptive in the original context — when resources are genuinely scarce, immediate resource management is optimal — but maladaptive when the person’s circumstances have changed.

How Cultural and Generational Experiences Shape Money Behavior

Money behavior is not shaped only by individual experiences — collective experiences at the cultural and generational level create shared financial behavioral patterns that persist across populations.

Generational Financial Imprinting

Each generation’s formative financial experiences create shared behavioral tendencies. People who experienced the Great Depression developed extreme frugality patterns and distrust of financial institutions that persisted for decades after economic recovery. Baby Boomers whose formative financial experiences occurred during prolonged economic growth tend to exhibit higher confidence in market-based wealth accumulation. Millennials who entered the workforce during the 2008 recession show measurably higher risk aversion and delayed financial milestones compared to previous generations at the same age.

Generational financial imprinting interacts with individual money scripts: a person’s unique family experiences operate within the broader context of their generation’s shared financial environment. A Millennial raised by Depression-era-influenced grandparents may carry both generational risk aversion and inherited scarcity scripts, producing layered behavioral patterns that are difficult to untangle without understanding both influences.

Cultural Attitudes Toward Money

Cultural frameworks create baseline assumptions about money that individuals absorb as default beliefs. Cultures that emphasize collectivism tend to produce financial behaviors oriented toward family obligation, shared resources, and community investment. Cultures that emphasize individualism tend to produce behaviors oriented toward personal accumulation, independent financial planning, and self-reliance.

Neither cultural orientation is inherently superior — each produces both constructive and destructive financial patterns. The important mechanism is that cultural money attitudes are absorbed as defaults — the person treats their culture’s financial assumptions as obvious truths rather than as one framework among many, which limits the range of financial strategies they consider available.

How to Identify and Modify Experience-Driven Money Patterns

Identifying experience-driven money patterns requires examining current financial behaviors for signs that they are responding to past circumstances rather than present realities. The primary indicator is a mismatch between behavior and context — doing something that would have been appropriate in a past situation but is unnecessary or counterproductive in the current one.

Self-Assessment Questions for Pattern Recognition

Effective self-assessment involves asking specific questions about financial behaviors. Does any current financial behavior produce anxiety disproportionate to the actual financial stakes involved? Does spending or saving behavior change dramatically in response to emotional triggers rather than financial triggers? Are there financial actions consistently avoided despite evidence that they would be beneficial? Do financial decisions feel “inevitable” rather than chosen — as though there is no alternative? A “yes” to any of these questions may indicate experience-driven patterns operating below conscious awareness.

Financial Therapy and Professional Approaches

Financial therapy is a specialized field that integrates psychological counseling with financial planning to address experience-driven money patterns. The Financial Therapy Association defines the practice as integrating cognitive, emotional, behavioral, relational, and financial aspects of financial health. Financial therapy approaches include identifying the origin events of current money scripts, examining the beliefs that formed during those events, testing those beliefs against current reality, and deliberately constructing new behavioral patterns aligned with present goals rather than past experiences, using techniques similar to those applied in changing money habits.

Can People Change Money Behaviors That Were Formed in Childhood?

Money behaviors formed in childhood can be modified, though the process requires more than awareness alone. Because childhood money scripts are encoded in implicit memory systems that operate below conscious deliberation, changing them requires both cognitive recognition of the pattern and sustained behavioral practice of alternative responses. The script itself does not disappear — instead, a new, more adaptive behavioral pattern is strengthened until it becomes the automatic response in the situations where the old script previously activated. This process typically takes months of consistent practice, not days.

How Do People Know If Their Money Behavior Is Driven by Past Trauma?

A money behavior is likely driven by past trauma when the emotional intensity of the response is disproportionate to the financial significance of the situation. If checking a bank balance produces panic, if spending any money produces guilt regardless of affordability, or if financial decision-making triggers fight-or-flight responses (racing heart, difficulty breathing, cognitive shutdown), these somatic indicators suggest trauma-driven activation rather than rational financial assessment. Financial trauma responses are involuntary — the person cannot simply decide to stop having them — which distinguishes them from financial stress, where the emotional response is proportionate to an actual financial difficulty.

Do Different Socioeconomic Backgrounds Create Different Money Scripts?

Different socioeconomic backgrounds systematically produce different money script distributions. Research on money scripts shows that households experiencing financial instability produce higher rates of money avoidance and money worship scripts, while households experiencing financial stability produce higher rates of money vigilance scripts. However, exceptions are common — the specific dynamics within the household (how money was discussed, how conflict was handled, what emotional associations were attached to financial events) matter as much as the objective financial position.

How Do Past Experiences Affect a Couple’s Financial Dynamic?

Past experiences affect a couple’s financial dynamic when each partner brings different money scripts into the relationship. A partner with money vigilance scripts may conflict with a partner with money worship scripts — one prioritizes cautious accumulation while the other prioritizes spending for quality of life. These conflicts feel like disagreements about money, but they are actually conflicts between two different sets of encoded beliefs formed by two different sets of formative experiences. Effective resolution requires identifying the money scripts each partner carries, understanding the experiences that produced them, and constructing shared financial frameworks that accommodate both partners’ legitimate needs without being controlled by either partner’s unexamined scripts, similar to how irrational money decisions are best addressed through awareness and structural countermeasures.