Table of Contents

Contents are generated from article headings.

Money habits are recurring financial behaviors that operate with minimal conscious deliberation. Money habits form through repetition — a financial action performed frequently in a consistent context eventually becomes automatic, requiring less cognitive effort and conscious decision-making with each occurrence. Money habits include daily spending patterns, saving routines, bill-paying behaviors, and impulse responses to financial triggers. These automatic behaviors collectively determine long-term financial outcomes more reliably than isolated financial decisions, because habits execute consistently while deliberate decisions depend on cognitive resources that fluctuate with stress, fatigue, and emotional state.

Money habits differ from financial knowledge in a critical way: knowing what to do financially and habitually doing it are governed by different cognitive systems. Financial knowledge operates through the prefrontal cortex (deliberate, analytical processing), while habits operate through the basal ganglia (automatic, pattern-based processing). This distinction explains why financial education alone often fails to change financial behavior — the knowledge exists in one cognitive system while the behavior is governed by another.

Scope and Context: This content discusses money habits and behavioral patterns using behavioral psychology research, established financial planning frameworks, and consumer survey data. Financial products, regulations, and economic conditions vary by jurisdiction and institution. Readers should evaluate habit-change strategies in the context of their own financial circumstances and current economic environment.

How Money Habits Form: The Habit Loop in Financial Behavior

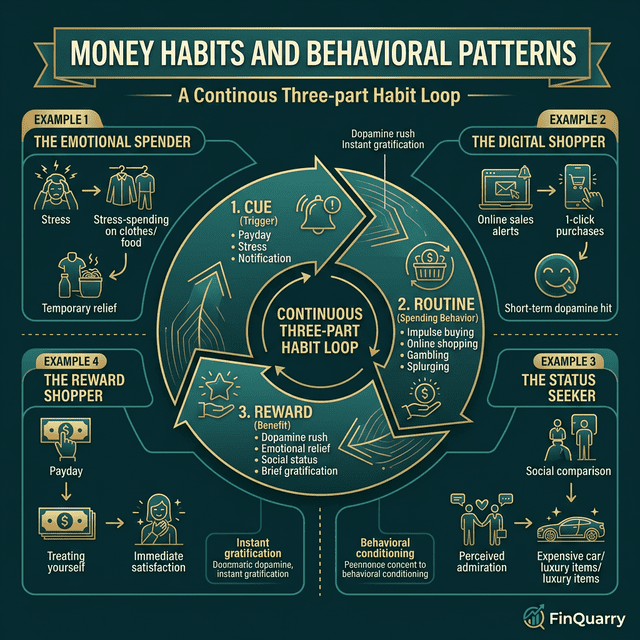

Money habits form through the same neurological mechanism that governs all habit formation: the habit loop. The habit loop consists of three components — a cue (trigger), a routine (behavior), and a reward (reinforcement) — that, when repeated, encode the behavior into the basal ganglia as an automatic pattern.

The Three Components of a Financial Habit Loop

A financial cue is any stimulus that triggers an automatic financial behavior. Financial cues include environmental triggers (walking past a coffee shop), temporal triggers (payday), emotional triggers (stress, boredom), social triggers (seeing a friend’s purchase on social media), and digital triggers (push notifications from shopping apps). The cue does not cause the behavior directly — it activates a stored routine that the brain associates with a specific reward.

The routine is the financial behavior itself — the action that follows the cue automatically. Financial routines range from constructive (transferring a fixed amount to savings on payday) to destructive (opening a shopping app when feeling stressed). The defining characteristic of a routine is its automaticity: the person performs it without deliberating over whether to do it.

The reward is the neurological reinforcement that completes the loop and strengthens the habit for future repetition. Financial rewards are often emotional rather than financial — the dopamine release from a purchase, the anxiety reduction from checking an account balance, or the satisfaction of seeing a savings balance increase. The reward does not need to be objectively beneficial; it needs only to produce a neurological signal that the brain registers as positive reinforcement.

Why Financial Habits Resist Change

Financial habits resist change because the basal ganglia, where habits are encoded, does not “delete” old habit loops — it can only be overwritten by new, stronger loops. This means that a person who has habitually spent impulsively when stressed cannot simply stop the behavior through willpower; they must replace the routine with a different behavior that responds to the same cue and provides a comparable reward. The Wells Fargo 2025 Money Study found that 48% of individuals who feel financially constrained attribute their situation to money habits they find difficult to break — a finding consistent with the neurological persistence of encoded habit loops.

Common Money Habits That Compound Over Time

Individual financial habits appear small in isolation. The compounding effect of habits — repeated across days, weeks, and years — determines whether these behaviors build financial resilience or erode it.

Constructive Habits That Build Financial Stability

Automatic saving is the most reliably constructive money habit because it operates independently of motivation, mood, or cognitive load. A person who has automated a fixed savings transfer on payday will save consistently regardless of whether they feel motivated to save on any given day. This structural feature makes automated saving more effective than intention-based saving, where the decision to save must be re-made each period.

Delayed purchasing is a habit pattern where a person introduces a mandatory waiting period between the impulse to buy and the act of buying. Common implementations include a 24-hour rule for non-essential purchases over a set amount, or a “wish list” system where desired items must remain on the list for a defined period before purchase. Delayed purchasing works because it interrupts the cue-routine-reward loop at the routine stage — the cue still fires, but the automatic routine (immediate purchase) is replaced with a deliberate pause.

Routine financial monitoring — checking account balances, reviewing spending categories, tracking progress toward savings goals — operates as a habit that maintains awareness of financial position and enables early detection of problems. Financial monitoring differs from anxiety-driven account checking: monitoring is scheduled and purposeful, while anxiety-driven checking is reactive and often increases rather than decreases financial anxiety.

Destructive Habits That Erode Financial Position

Convenience spending is a habit pattern where a person consistently chooses the most immediately accessible option rather than the most cost-effective one. Examples include daily coffee purchases when coffee could be prepared at home, frequent food delivery orders when cooking is feasible, and subscription services that continue without active use. Each individual convenience expenditure is financially insignificant, but the compound effect across multiple convenience habits can consume a substantial portion of discretionary income.

Lifestyle inflation is a behavioral pattern where spending automatically increases in proportion to income increases, preventing the income growth from improving financial position. Lifestyle inflation operates as a habit because it does not require a conscious decision to spend more — the spending increase occurs automatically as higher-income options become accessible and social reference groups shift.

Minimum payment habits on revolving credit represent one of the most financially destructive behavioral patterns because they exploit the gap between habit and analysis. Making the minimum payment feels like responsible behavior (the bill is “paid”), but the mathematical reality is that minimum payments on high-interest debt can extend repayment over decades and multiply the total cost several times beyond the original balance.

The Role of Environment in Financial Habits

Financial habits do not form in isolation — they are shaped by the physical, digital, and social environments in which financial decisions occur. Modifying the environment is often more effective than attempting to modify behavior directly, because environmental changes alter the cues that trigger habitual responses.

How Digital Environments Shape Spending Habits

Digital payment systems reduce the psychological friction associated with spending by removing the physical experience of parting with money. When payment requires handing over cash, the anterior insula — a brain region associated with negative affect — activates in proportion to the amount spent. Digital payments attenuate this response, making each transaction feel less consequential and enabling higher spending frequency.

Mobile shopping applications are specifically designed to create and reinforce spending habits through behavioral design elements: push notifications serve as cues, one-click purchasing reduces friction in the routine, and immediate order confirmation provides reward. The cumulative effect of these design elements is that spending through mobile applications tends to become more habitual and less deliberate over time.

How Social Environment Influences Money Habits

Social reference groups exert a powerful influence on money habits through a mechanism called social norming — the tendency to adjust personal behavior to match the perceived behavior of a relevant peer group. A person whose social circle normalizes frequent dining out, luxury purchases, or status-signaling spending will tend to develop spending habits that match those norms, even when those habits are misaligned with their financial position. This is the same herd mentality mechanism that operates in investment markets.

Social media amplifies social norming effects by presenting curated, highlight-reel versions of other people’s consumption patterns. The visibility of others’ spending creates cues that trigger comparison-based spending habits — a dynamic that disproportionately affects younger adults who are still establishing their financial behavioral patterns.

How to Change Money Habits: Evidence-Based Approaches

Changing money habits requires strategies that work with the neurological structure of habits rather than against it. Willpower-based approaches fail because willpower is a depletable cognitive resource — it functions at its lowest when the person is stressed, tired, or emotionally depleted, which are precisely the conditions under which destructive financial habits are most likely to activate.

Habit Stacking for Financial Behavior

Habit stacking is a technique where a new desired financial behavior is attached to an existing established habit, using the existing habit as the cue for the new one. The formula is: “After I [existing habit], I will [new financial habit].” For example: “After I receive my direct deposit notification, I will transfer $200 to my savings account.” Habit stacking works because it leverages an existing cue-routine pathway rather than requiring the creation of a new cue, which reduces the cognitive effort needed to initiate the new behavior.

Environment Design for Financial Defaults

Designing the financial environment to make constructive behaviors the default and destructive behaviors require effort is more effective than relying on repeated decisions. Practical environment design strategies include removing saved payment information from shopping apps (increasing friction for impulse purchases), setting up automatic transfers to savings accounts (making saving the default), unsubscribing from marketing emails (removing purchase cues), and using separate accounts for spending categories to make budgeting visible and concrete.

The 21-Day Myth and Realistic Habit Timelines

Popular financial advice often claims that habits form in 21 days. Research published by Phillippa Lally and colleagues at University College London found that the actual time to habit formation averages approximately 66 days, with a range from 18 to 254 days depending on the complexity of the behavior and the individual. Financial habits — which involve emotional triggers, social pressures, and environmental cues — tend to fall toward the longer end of this range. Setting realistic expectations for habit change timelines reduces the likelihood of abandoning the effort when results are not immediate.

How Do Money Habits Differ from Financial Decisions?

Money habits and financial decisions are distinct cognitive processes. A financial decision involves deliberate evaluation of options, costs, and outcomes using the prefrontal cortex — the brain’s analytical processing center. A money habit is an automatic behavioral response encoded in the basal ganglia that executes without deliberate evaluation. The practical difference is that decisions require cognitive effort and can be derailed by stress or fatigue, while habits execute consistently regardless of cognitive state. Most daily financial behaviors are habits rather than decisions, which is why habit change is more impactful than information-based financial education for long-term behavior modification.

Can Financial Habits Be Changed at Any Age?

Financial habits can be changed at any age because the neurological mechanism of habit formation — the creation of new cue-routine-reward loops — remains functional throughout the lifespan. However, the difficulty of changing established habits tends to increase with age because longer-established neural pathways are more deeply encoded. Older adults may require more repetitions and more deliberate environmental design to overwrite established financial habits, but the capacity for habit change is not age-limited.

What Is the Most Effective Single Change for Improving Money Habits?

Automating savings is consistently identified as the single most effective habit intervention for improving financial outcomes. Automation works because it removes the recurring decision point where competing impulses, stress, and cognitive depletion can override intention. Research on automatic enrollment in retirement plans has demonstrated that making saving the default — rather than requiring active opt-in — increases investment discipline and participation rates from approximately 60% to over 90%, regardless of the individual’s existing money habits.

How Does Stress Affect Money Habits?

Stress increases reliance on habitual behaviors and decreases the influence of deliberate decision-making. Under stress, the prefrontal cortex — responsible for analytical financial thinking — is suppressed by cortisol, while the basal ganglia — which executes habits — continues to function normally. This means that stress does not change a person’s financial knowledge; it changes which cognitive system controls their behavior. A person with constructive financial habits will tend to maintain those habits under stress, while a person with destructive habits will tend to revert to them, as described in how psychology affects financial decisions.