Table of Contents

Contents are generated from article headings.

Irrational money decisions are financial choices that contradict a person’s own best interests, logic, or stated goals. Behavioral finance — the field that combines psychology with economics — reveals that irrational financial decisions are not random errors but predictable patterns driven by cognitive biases, emotional responses, and mental shortcuts that evolved long before modern financial systems existed.

People do not make irrational money decisions because they lack intelligence. Irrational financial behavior occurs because the human brain processes financial information through two competing systems: a fast, intuitive, emotion-driven system and a slower, deliberate, analytical system. When the fast system dominates — as it frequently does under stress, time pressure, or emotional activation — financial decisions tend to reflect psychological patterns rather than rational calculation. Understanding these patterns is the first step toward recognizing when cognitive biases are influencing financial choices.

Scope and Context: This content discusses behavioral finance concepts and cognitive bias research drawn from peer-reviewed academic literature and regulatory publications. Specific financial regulations, consumer protection standards, and available interventions vary by jurisdiction and institution. Research findings cited reflect conditions as of their publication dates; behavioral patterns are well-established across decades of study, but readers should evaluate strategies in the context of their own financial situation, local regulations, and current economic conditions.

What Behavioral Finance Reveals About Irrational Decisions

Behavioral finance provides the theoretical framework for understanding why people consistently deviate from rational financial behavior. This field challenges the traditional economic assumption that individuals always act to maximize their financial self-interest.

The Gap Between Rational and Actual Financial Behavior

Behavioral finance identifies a systematic gap between how people should make financial decisions and how they actually make them. Traditional economics assumes that individuals evaluate all available information, weigh costs and benefits accurately, and choose the option that maximizes their utility. Behavioral finance demonstrates that real financial decisions are filtered through cognitive shortcuts, emotional states, and social influences that can distort rational evaluation.

Daniel Kahneman and Amos Tversky’s prospect theory — one of the foundational concepts in behavioral finance — demonstrated that people evaluate potential losses and gains asymmetrically. In their original 1979 paper “Prospect Theory: An Analysis of Decision under Risk” published in Econometrica, Kahneman and Tversky established that losses feel approximately twice as painful as equivalent gains feel pleasurable, a phenomenon that explains why investors often make irrational decisions to avoid losses rather than to capture gains. This asymmetry affects decisions ranging from investment portfolio management to everyday purchasing behavior.

Dual-Process Theory and Financial Decision-Making

Dual-process theory explains irrational money decisions through the interaction of two cognitive systems. System 1 operates automatically, quickly, and with little conscious effort — it generates intuitive judgments and emotional reactions. System 2 operates deliberately, slowly, and requires conscious mental effort — it handles logical analysis and complex calculation.

Financial decisions ideally require System 2 processing because they involve evaluating trade-offs, calculating opportunity costs, and projecting future outcomes. However, System 1 frequently hijacks financial decisions, particularly when a person is tired, stressed, or facing information overload. A consumer comparing mortgage rates benefits from System 2 analysis, but that same consumer may default to System 1 when making an impulse purchase after a stressful workday. The default to intuitive processing under cognitive load is one reason money psychology identifies stress as a primary driver of suboptimal financial behavior.

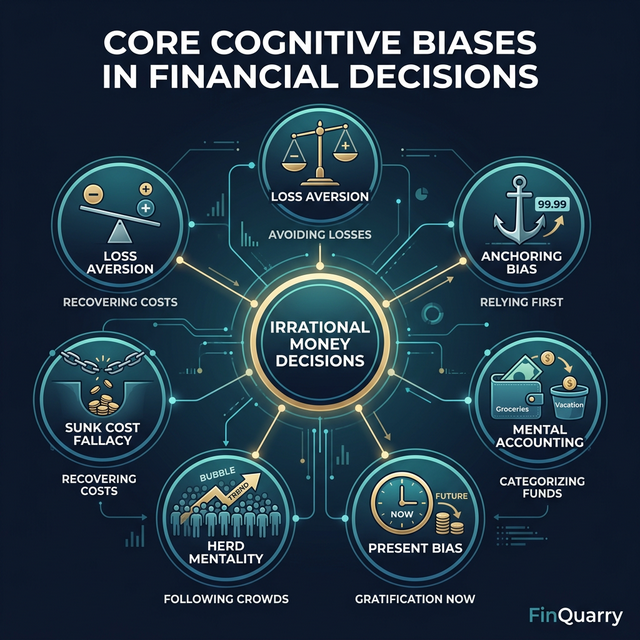

Core Cognitive Biases That Distort Financial Decisions

Cognitive biases are systematic errors in thinking that occur when the brain uses mental shortcuts to process information. These biases are not character flaws — they are structural features of human cognition that served survival functions in ancestral environments but can produce poor outcomes in modern financial contexts.

Loss Aversion and Risk-Distorted Choices

Loss aversion causes people to weigh potential losses more heavily than potential gains of equal magnitude. Research in behavioral economics — including Kahneman and Tversky’s foundational work and subsequent replications documented in Kahneman’s Thinking, Fast and Slow (2011) — suggests that the pain of losing $100 feels approximately twice as intense as the pleasure of gaining $100, though the exact ratio varies by context and individual.

Loss aversion distorts financial decisions in multiple directions. An investor experiencing loss aversion may hold a declining stock position far longer than rational analysis would justify, hoping to avoid realizing the loss — a behavior known as the disposition effect. Conversely, loss aversion can make a person excessively conservative, keeping funds in low-yield savings accounts rather than investing in diversified portfolios with higher expected returns, because the possibility of any loss feels intolerable. For a person already experiencing financial anxiety, loss aversion can compound into financial paralysis where no investment decision feels safe enough to execute.

Anchoring Bias and Distorted Value Assessment

Anchoring bias occurs when a person relies disproportionately on the first piece of information encountered — the "anchor" — when making subsequent judgments. Anchoring bias operates largely outside conscious awareness, affecting financial decisions even when the anchor is arbitrary or irrelevant.

Anchoring bias influences financial decisions in situations ranging from salary negotiation to real estate purchasing. A homebuyer who sees a property listed at $500,000 will unconsciously anchor to that price, even if comparable properties in the area sell for $420,000. When the seller "reduces" the price to $460,000, the buyer perceives a bargain relative to the anchor, not relative to the actual market value. This same mechanism operates in retail environments where an original price of $200 makes a "sale price" of $120 feel like a deal, regardless of whether the item’s functional value justifies $120. Anchoring bias persists even when people are informed about it, which is why structural countermeasures — like conducting independent valuations before viewing asking prices — tend to be more effective than willpower alone.

Mental Accounting and Non-Fungible Money Treatment

Mental accounting describes the cognitive tendency to treat money differently based on its source, intended use, or the mental category assigned to it, rather than treating all money as interchangeable. Nobel laureate Richard Thaler first formalized mental accounting in his 1985 paper “Mental Accounting and Consumer Choice” published in Marketing Science, identifying it as a fundamental violation of the economic principle of fungibility — the idea that a dollar is a dollar regardless of where it came from.

Mental accounting leads to irrational financial behaviors such as maintaining a savings account earning 1% interest while simultaneously carrying credit card debt at 22% APR. A rational actor would use the savings to eliminate the high-interest debt, producing a net financial benefit of 21 percentage points. However, mental accounting creates separate psychological "accounts" — the savings feel different from the debt — preventing the rational calculation from overriding the categorical distinction. Similarly, people tend to spend windfall income (tax refunds, bonuses, gambling winnings) more freely than earned income, even though the money has identical purchasing power. This is one mechanism observed in how psychology affects financial decisions across income levels and financial sophistication.

Present Bias and the Discounting of Future Consequences

Present bias is the tendency to overvalue immediate rewards while undervaluing future outcomes, even when the future outcome is objectively larger or more important. Present bias explains why people struggle with saving, retirement planning, and long-term financial goal-setting despite intellectually understanding their importance.

Present bias operates through a process called hyperbolic discounting, where the perceived value of a future reward decreases disproportionately as the delay increases. A person offered $100 today versus $110 in one week tends to choose the immediate $100, but that same person offered $100 in 52 weeks versus $110 in 53 weeks tends to choose the $110 — even though the delay is identical in both scenarios. This inconsistency reveals that the bias is not about rational time-value-of-money calculations but about the psychological pull of immediacy. Present bias directly undermines retirement savings, where the benefits are decades away and the sacrifice is immediate, which contributes to why compounding takes time to demonstrate its full impact and many people abandon long-term investment strategies prematurely.

How Emotions Override Financial Logic

Emotional states do not simply influence financial decisions — they can completely override rational analysis. Understanding the emotional mechanisms behind irrational financial behavior explains why knowledge alone is often insufficient to prevent poor financial choices.

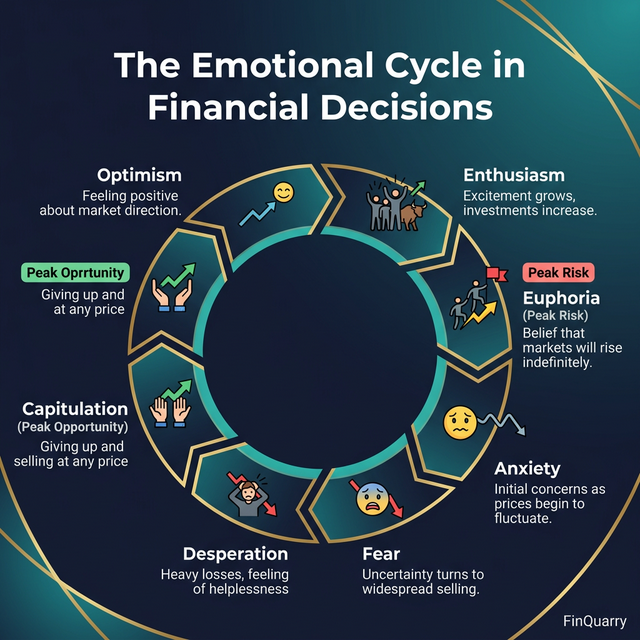

Fear, Greed, and the Emotional Cycle in Markets

Fear and greed function as opposing emotional forces that drive cyclical patterns in both individual financial behavior and collective market movements. Fear triggers risk-averse behavior — selling investments during market downturns, hoarding cash, avoiding necessary financial commitments. Greed triggers risk-seeking behavior — chasing speculative investments, over-leveraging, ignoring diversification principles.

The emotional cycle in financial markets follows a predictable pattern: optimism leads to enthusiasm, which escalates to euphoria at market peaks. Anxiety follows as prices decline, progressing to fear, then desperation, and finally capitulation — the point where investors sell at the worst possible moment. This cycle repeats because each phase is driven by emotional contagion rather than fundamental analysis. Individual investors who sell at market bottoms and buy at market peaks are not making calculation errors — they are responding to emotional intensity that overrides their analytical knowledge. Data from the DALBAR Quantitative Analysis of Investor Behavior (QAIB) consistently shows that average investor returns significantly underperform the market indices they invest in, largely due to emotionally timed buying and selling decisions. DALBAR’s 2024 report found that the average equity fund investor earned 16.54% compared to the S&P 500’s 25.02%, an 8.48 percentage-point gap — marking the fourth-largest underperformance since the study began in 1985 and extending a 15-consecutive-year streak of investor underperformance.

The Sunk Cost Fallacy and Emotional Commitment

The sunk cost fallacy occurs when people continue investing time, money, or effort into something because of what they have already spent, rather than evaluating the decision based on future costs and benefits. The sunk cost fallacy is driven by emotional attachment to past investments and the psychological discomfort of admitting a mistake.

The sunk cost fallacy leads to financial decisions such as continuing to pay for an unused gym membership because "I’ve already spent so much on it," or holding shares in a declining company because selling would mean accepting that the original buy decision was wrong. A rational evaluation considers only future outcomes: will the gym membership generate value going forward? Will the stock recover based on its current fundamentals? The sunk cost — money already spent and unrecoverable — should be irrelevant to these forward-looking decisions. However, the emotional weight of past investment creates a sense of waste that most people find psychologically difficult to accept, which keeps them committed to losing positions.

Emotional Spending as a Mood Regulation Mechanism

Emotional spending operates through the brain’s dopamine reward system, where the anticipation and act of purchasing generate temporary mood elevation. Emotional spending becomes irrational when the purchase serves a psychological function — stress relief, boredom alleviation, identity reinforcement — rather than fulfilling a genuine need or a planned financial allocation.

Emotional spending produces irrational outcomes because the emotional benefit is temporary while the financial cost is permanent. A person who spends $200 on an unplanned purchase to relieve work stress experiences dopamine-mediated satisfaction that typically fades within hours, leaving a $200 reduction in their financial position and often a subsequent feeling of guilt that can itself trigger further emotional spending. This cycle — emotional trigger, spending response, temporary relief, guilt, repeated trigger — is one of the most common patterns of irrational financial behavior. According to a LendingTree survey on emotional spending, approximately 50% of emotional spenders identify stress as their primary spending trigger, and nearly three-quarters report that emotional purchasing leads them to overspend beyond their planned budgets.

Social and Environmental Drivers of Irrational Financial Behavior

Irrational money decisions are not exclusively internal cognitive events. External social pressures, environmental design, and cultural norms systematically influence financial behavior in ways that people often fail to recognize.

Herd Mentality and Social Proof in Financial Decisions

Herd mentality describes the tendency to follow the financial behavior of a group rather than conducting independent analysis. Herd mentality operates through a cognitive shortcut: if many people are doing something, it must be correct. This shortcut can be useful in some contexts but produces irrational outcomes in financial markets where crowd behavior often amplifies rather than corrects pricing errors.

Herd mentality contributed to documented financial events including the dot-com bubble of the late 1990s, the U.S. housing bubble of the mid-2000s, and various cryptocurrency speculation cycles. In each case, the pattern followed a similar structure: early adopters generated returns, media coverage attracted broader participation, social proof accelerated buying, prices exceeded fundamental values, and eventual correction produced losses concentrated among late entrants. The Financial Crisis Inquiry Commission’s 2011 report identified herd behavior among both institutional and retail investors as a contributing factor to the 2008 financial crisis. Research from the Consumer Financial Protection Bureau further documents that social comparison and peer influence are significant factors in household financial decision-making, particularly for major purchases and investment allocation decisions.

Choice Architecture and Decision Fatigue

Choice architecture — the way options are structured and presented — significantly influences financial decisions. People do not evaluate financial options in a vacuum; the framing, default settings, and comparison structure of choices systematically shape outcomes. Research by Brigitte Madrian and Dennis Shea, published in the Quarterly Journal of Economics (2001), demonstrated that changing the default option in retirement plan enrollment from opt-in to opt-out increases participation rates from approximately 60% to over 90%, without changing the economic incentives at all. The U.S. Department of Labor has since recognized automatic enrollment as a best practice for improving retirement savings outcomes.

Decision fatigue further undermines rational financial behavior. The brain’s capacity for deliberate, analytical thinking is a finite resource that depletes with use throughout the day. Financial decisions made after extended periods of cognitive exertion tend to rely more heavily on System 1 processing — defaulting to the easiest option, the most familiar choice, or the status quo. This explains why financial professionals recommend making important financial decisions in the morning, when cognitive resources are freshest, and why budgeting frameworks that automate routine financial decisions can reduce the impact of decision fatigue on household money management.

How to Recognize and Reduce Irrational Financial Patterns

Recognizing irrational financial patterns is a necessary first step, but awareness alone does not eliminate cognitive biases. Effective mitigation requires structural changes to the decision-making environment, not simply greater willpower or financial knowledge.

Building Awareness of Personal Financial Biases

Personal financial bias identification involves systematic observation of one’s own decision patterns over time. A financial decision journal — recording not only what financial decisions were made but the emotional context, time of day, and reasoning behind each decision — can reveal recurring patterns that are invisible without deliberate tracking.

Common patterns that financial decision journaling reveals include: spending that increases after specific emotional triggers, investment decisions that correlate with recent market news rather than long-term strategy, and savings behavior that varies based on how income was received rather than its amount. The goal of bias awareness is not to eliminate biases — which is generally not possible — but to create a recognition window between the biased impulse and the financial action, allowing System 2 processing to engage before the decision is finalized.

Structural Interventions That Counteract Bias

Structural interventions modify the decision environment to reduce the impact of cognitive biases on financial outcomes. These interventions are generally more effective than knowledge-based approaches because they do not require continuous conscious effort to maintain.

Effective structural interventions for common financial biases include:

- automating savings contributions before money enters the spending account, which counteracts present bias by removing the decision point entirely

- establishing predetermined investment rebalancing schedules, which reduces the influence of loss aversion and recency bias on portfolio management

- implementing mandatory waiting periods (24–72 hours) before executing large unplanned purchases, which allows emotional activation to subside before System 2 evaluates the decision

- using commitment devices such as goal-linked savings accounts that impose penalties for early withdrawal, which aligns present incentives with future objectives

These structural approaches work because they redesign the choice architecture to make the rational choice the default, rather than requiring active resistance against cognitive biases. As research in behavioral economics consistently demonstrates, changing the environment is more reliable than changing the person when it comes to sustained financial behavior modification.

When Irrational Financial Behavior May Require Professional Support

Irrational financial behavior that produces recurring negative consequences — persistent debt accumulation, inability to save despite adequate income, repeated investment losses from emotional trading — may indicate patterns that benefit from professional intervention. Financial therapy, which integrates psychological techniques with financial planning, addresses the emotional and behavioral roots of financial decision-making rather than treating money management as a purely mathematical exercise.

The Financial Therapy Association maintains a directory of practitioners trained in both psychological and financial disciplines. Professional support may be particularly valuable when irrational financial behavior co-occurs with anxiety, depression, or relationship conflict, as the emotional drivers of financial decisions often intersect with broader psychological patterns.

What Is the Difference Between Irrational and Rational Financial Decisions?

Rational financial decisions are choices where a person evaluates available options, weighs costs against benefits using accurate information, and selects the option that best serves their stated financial goals. Irrational financial decisions occur when cognitive biases, emotional states, or social pressures cause a person to choose options that conflict with their own financial interests or goals. The distinction is not about intelligence — even financially sophisticated individuals exhibit irrational patterns because cognitive biases are structural features of human cognition, not knowledge deficits.

Can Financial Education Eliminate Irrational Money Decisions?

Financial education improves knowledge of financial concepts and products, but research consistently shows that education alone does not eliminate irrational financial behavior. Cognitive biases operate largely outside conscious awareness and activate automatically, meaning that a person can understand a bias intellectually while still being influenced by it. Effective financial behavior change typically requires combining education with structural interventions — automated savings, default enrollment, commitment devices — that reduce reliance on conscious decision-making in moments of bias activation.

What Are the Most Common Cognitive Biases in Financial Decisions?

The most commonly documented cognitive biases affecting financial decisions include loss aversion (overweighting potential losses relative to potential gains), anchoring bias (relying disproportionately on initial information), mental accounting (treating money differently based on source or category), present bias (overvaluing immediate rewards over future outcomes), confirmation bias (seeking information that supports existing beliefs), and herd mentality (following group behavior rather than independent analysis). These biases interact with each other and with emotional states, creating compound effects that can amplify irrational financial behavior.

Does Stress Make Financial Decisions More Irrational?

Stress significantly increases the likelihood of irrational financial decisions by shifting cognitive processing from System 2 (deliberate, analytical) to System 1 (fast, intuitive, emotion-driven). Under stress, the prefrontal cortex — responsible for planning, impulse control, and rational evaluation — operates with reduced efficiency, while the amygdala — which processes threat and emotional responses — becomes more active. This neurological shift means that financial decisions made under acute stress tend to be more reactive, more loss-averse, and more influenced by immediate emotional states than decisions made in calm conditions.

Can Irrational Financial Behavior Be Completely Eliminated?

Irrational financial behavior cannot be completely eliminated because cognitive biases are inherent features of human cognition that evolved over hundreds of thousands of years. However, the impact of cognitive biases on financial outcomes can be substantially reduced through awareness, structural interventions, and environmental design. The most effective approaches do not attempt to override biases through willpower but instead restructure the decision environment so that biased impulses encounter friction while rational choices become the path of least resistance.