Table of Contents

Contents are generated from article headings.

Emotional spending is the pattern of making unplanned purchases driven by emotional states rather than by need, logic, or budget planning. Emotional spending occurs when feelings such as stress, sadness, boredom, excitement, or anxiety override a person’s rational decision-making process, leading to purchases that provide temporary emotional relief but often create long-term financial consequences.

Emotional spending differs from planned discretionary spending because it bypasses conscious evaluation. A person engaged in emotional spending typically does not assess whether the purchase fits their budget or financial goals. Instead, the spending decision originates from a psychological need for mood regulation, comfort, or a sense of control. Research from behavioral economics indicates that individuals experiencing heightened emotional states tend to weigh immediate emotional rewards more heavily than future financial outcomes.

FinQuarry provides informational content only. This article does not constitute personalized financial, legal, tax, or investment advice.

How Emotional Spending Works as a Psychological Mechanism

Emotional spending operates through a neurochemical feedback loop involving the brain’s dopamine reward system. Understanding this mechanism reveals why emotional spending feels rewarding in the moment but rarely leads to lasting satisfaction.

The Dopamine Reward Loop in Purchasing Behavior

Dopamine, a neurotransmitter associated with motivation and pleasure, plays a central role in emotional spending behavior. Dopamine release occurs not only during the act of purchasing but also during the anticipation of a purchase — browsing online stores, adding items to a cart, or walking through a shopping center. This anticipatory dopamine surge creates a temporary sense of excitement that the brain associates with reward.

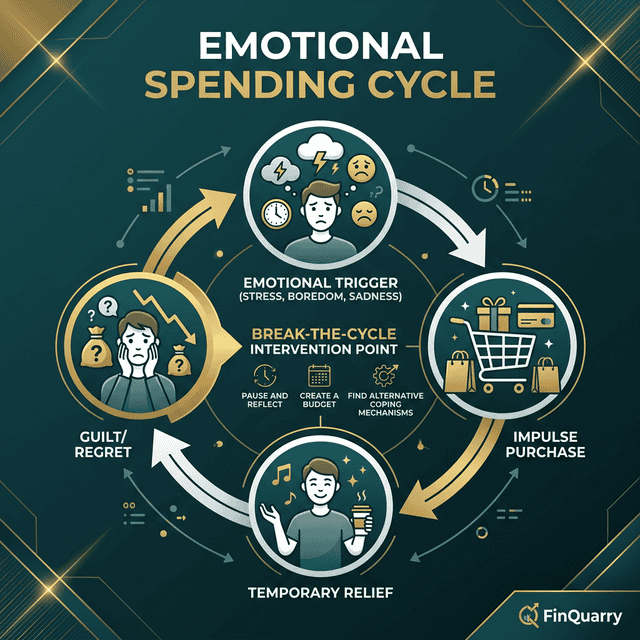

The dopamine reward loop in emotional spending follows a predictable cycle: an emotional trigger activates a desire for relief, browsing or shopping generates dopamine-driven anticipation, the purchase provides a brief spike in satisfaction, and the effect fades within hours or days. This cycle reinforces itself because the brain records the emotional relief as a successful outcome, increasing the likelihood of repeating the behavior during future emotional episodes. The temporary nature of this dopamine response is what distinguishes emotional spending from purchases that produce sustained utility or satisfaction.

Why Emotional Triggers Override Financial Reasoning

Emotional spending bypasses rational financial evaluation because emotional processing and logical reasoning operate through separate neural pathways. When a person experiences acute stress, sadness, or even euphoria, the brain’s limbic system — responsible for emotional responses — activates before the prefrontal cortex, which handles long-term planning and impulse control.

This sequencing means that emotional impulses reach decision-making centers before rational analysis can intervene. A person under financial anxiety may purchase an item they cannot afford because the immediate emotional relief outweighs, in the moment, the abstract consequence of budget disruption. Research in consumer psychology suggests that people experiencing sadness tend to pay up to 30% more for products than those in a neutral emotional state, demonstrating how emotions directly inflate perceived value and willingness to spend. This dynamic is one reason why people make irrational money decisions even when they intellectually understand the financial consequences.

Common Triggers That Lead to Emotional Spending

Emotional spending triggers fall into two categories: negative emotional triggers that drive spending as a coping mechanism, and positive emotional triggers that encourage spending as celebration or reward. Both categories activate the same dopamine-mediated spending cycle, though the underlying motivations differ.

Negative Emotional Triggers

Stress is the most frequently reported trigger for emotional spending. According to survey data from LendingTree, approximately 50% of emotional spenders identify stress as their primary spending trigger. Financial anxiety, workplace pressure, relationship conflict, and health concerns all generate stress responses that can lead to compensatory spending behavior. Understanding these triggers is a foundational element of money psychology — the study of how emotional and cognitive factors shape financial behavior.

Sadness and loneliness represent the second major category of negative triggers. Emotional spending driven by sadness often takes the form of what consumer psychologists call “retail therapy” — the act of purchasing items specifically to elevate mood. The mechanism behind retail therapy involves the sense of autonomy and control that shopping provides. A person experiencing sadness or helplessness in one area of life may use purchasing decisions as a domain where they can exercise choice and agency, thereby restoring a temporary sense of personal control.

Boredom functions as an underrecognized emotional spending trigger. Unlike stress or sadness, boredom does not produce acute emotional distress. Instead, boredom creates a motivational deficit — a lack of stimulation that the brain attempts to resolve through novelty-seeking behavior. Online shopping platforms, with their infinite scroll interfaces and personalized recommendation algorithms, exploit this novelty-seeking response by continuously presenting new products that provide micro-doses of dopamine through visual engagement. Over time, these boredom-driven purchases can crystallize into money habits that persist even after the original emotional trigger fades.

Positive Emotional Triggers

Excitement and celebration trigger emotional spending through a different mechanism than negative emotions. When a person receives positive news — a promotion, a milestone birthday, a personal achievement — the existing elevated mood lowers spending inhibitions. The cognitive framing shifts from “Can I afford this?” to “I deserve this,” which creates psychological permission to spend outside normal budget parameters.

Fear of missing out, commonly referred to as FOMO, represents a hybrid trigger that combines social anxiety with anticipatory excitement. Limited-time offers, flash sales, and social media posts showing others’ purchases create urgency signals that override deliberate decision-making. FOMO-driven spending tends to produce higher regret rates than other forms of emotional spending because the purchase decision is driven by perceived scarcity rather than genuine desire or need. The interplay between fear and greed in financial choices explains why FOMO operates as a spending accelerator across both retail and investment contexts.

Financial Consequences of Unchecked Emotional Spending

Emotional spending, when it becomes a recurring behavioral pattern rather than an occasional indulgence, can produce measurable financial damage that compounds over time.

Budget Disruption and Savings Erosion

Emotional spending disrupts household budgets by introducing unpredictable, unplanned expenses that reduce the funds available for fixed obligations and savings goals. Survey data indicates that 74% of self-identified emotional spenders report that emotional purchasing leads them to overspend beyond their planned budgets. The average American consumer spends approximately $282 per month on impulse purchases, totaling roughly $3,400 per year — funds that, if redirected, could contribute to emergency savings or debt reduction.

The savings erosion effect of emotional spending is particularly significant because it compounds. Each month of emotional overspending reduces the capital base available for investment or interest-bearing savings, meaning the true cost of emotional spending includes not only the purchase price but also the forgone compounding returns on that money over time. A person who redirects even $150 per month from emotional spending into savings may accumulate significantly more capital over a decade, depending on the return environment. This is one dimension of why saving feels hard psychologically — present-focused emotional spending competes directly with future-oriented savings behavior.

Debt Accumulation and Credit Impact

Emotional spending frequently accelerates debt accumulation, particularly when purchases are financed through credit cards or Buy Now, Pay Later (BNPL) services. According to the Consumer Financial Protection Bureau, BNPL usage has grown substantially, with 21% of consumers financing at least one purchase through BNPL services. The CFPB’s research indicates that BNPL availability can increase the likelihood of emotionally driven purchases because it removes the immediate financial friction that might otherwise pause a spending impulse.

Credit card debt generated through emotional spending carries particularly high cost because revolving balances accrue interest at annual percentage rates that frequently exceed 20%. A person who carries a $3,000 balance from emotional purchases at 22% APR would pay approximately $660 in annual interest alone — effectively increasing the true cost of those purchases by more than 20%. Over time, this debt servicing cost can strain cash flow and delay progress toward financial goals such as building an emergency fund, eliminating existing debt, or saving for retirement.

Emotional Spending Versus Compulsive Buying: A Critical Distinction

Emotional spending and compulsive buying disorder share surface-level similarities but differ in severity, frequency, and clinical classification. Recognizing this distinction matters because the intervention strategies for each are fundamentally different.

Defining the Boundary

Emotional spending is a behavioral pattern in which a person occasionally uses purchasing to regulate emotions. Emotional spending tends to be situational — it occurs in response to specific emotional triggers and often resolves when the triggering condition subsides. A person who engages in emotional spending retains the ability to recognize and evaluate the behavior, even if they do not always control it in the moment. Past experiences that shape money behavior often influence whether a person’s emotional spending remains occasional or escalates into a chronic pattern.

Compulsive buying disorder, by contrast, is recognized as a behavioral condition characterized by persistent and uncontrollable urges to purchase items regardless of need, financial capacity, or consequences. Compulsive buying disorder tends to escalate rather than self-correct. Individuals with compulsive buying patterns often experience significant impairment in daily functioning, strained relationships, and severe financial distress. The key clinical differentiator is whether the person can stop or moderate the behavior when they become aware of it — emotional spenders generally can, while compulsive buyers generally struggle to do so without professional support.

When Emotional Spending May Require Professional Intervention

Emotional spending may cross into territory requiring professional intervention when the behavior produces any of the following patterns:

- recurring debt accumulation that the person cannot explain through planned expenses

- persistent feelings of guilt, shame, or secrecy surrounding purchases

- inability to reduce spending despite conscious attempts and awareness of financial consequences

- spending that interferes with meeting essential financial obligations such as rent, utilities, or debt payments

The Financial Therapy Association maintains a directory of licensed financial therapists — practitioners trained in both psychological and financial counseling — who specialize in helping individuals address the emotional roots of problematic spending patterns. Financial therapy differs from traditional financial advising because it integrates behavioral and emotional analysis with financial planning, rather than addressing numbers alone.

How to Identify and Manage Emotional Spending Patterns

Managing emotional spending requires both self-awareness of triggers and the implementation of structural changes that create barriers between emotional impulses and spending actions.

Recognizing Personal Spending Triggers

Spending trigger identification involves tracking the emotional context of unplanned purchases over a period of at least 30 days. Individuals who keep a spending journal — recording not only what they purchased and the amount, but why they felt compelled to buy at that moment — typically identify recurring patterns. Common patterns include spending after specific types of stressful events, spending during particular times of day, or spending on specific product categories associated with comfort or self-reward.

The value of trigger identification lies in creating a window of awareness between the emotional impulse and the spending action. Once a person recognizes that their spending spikes after workplace conflicts, for example, they can prepare alternative responses in advance. This precommitment strategy reduces the cognitive load of resisting impulse spending in real time because the decision has already been made before the trigger occurs.

Structural Barriers That Reduce Emotional Spending

Structural barriers modify the spending environment to make impulsive purchases more difficult, reducing reliance on willpower alone. Research in behavioral economics consistently demonstrates that small increases in friction — the effort required to complete an action — significantly reduce the frequency of impulsive behaviors.

Effective structural barriers for emotional spending include:

- removing saved credit card information from online shopping platforms, requiring manual entry for each purchase

- implementing a mandatory 24-hour waiting period before completing any unplanned purchase exceeding a personal threshold

- unsubscribing from promotional emails and disabling push notifications from retail applications

- designating a specific, limited “discretionary spending” allocation within the monthly budget that permits occasional emotional purchases without destabilizing the overall financial plan — a concept closely related to mental accounting where people compartmentalize money into distinct psychological categories

These interventions work by inserting a pause between impulse and action. The 24-hour waiting period, in particular, allows the prefrontal cortex to re-engage with rational cost-benefit analysis after the initial emotional activation subsides. Many people who implement this waiting period find that the urgency of the purchase diminishes substantially within hours, indicating that the desire was emotionally driven rather than needs-based.

Redirecting the Emotional Need Without Spending

Emotional spending serves a legitimate psychological function — it provides temporary mood regulation. Eliminating emotional spending entirely without addressing the underlying emotional need often fails because the person still requires a mechanism for managing difficult emotions. Sustainable management of emotional spending involves identifying alternative mood regulation strategies that fulfill the same emotional function without the financial cost.

Activities that provide dopamine-mediated mood elevation without purchasing include physical exercise, social connection, creative engagement, and mindfulness practices. Each of these alternatives activates the brain’s reward circuits through different pathways. Physical exercise, for example, stimulates endorphin and serotonin release alongside dopamine, producing mood elevation that typically persists longer than the brief satisfaction of a purchase. The goal is not to eliminate emotional responses but to develop a broader repertoire of responses that does not default to spending.

What Emotional Spending Does Not Solve

Emotional spending provides temporary emotional relief, but it does not address the underlying conditions that generate the emotional triggers. Financial anxiety, for example, originates from structural financial problems — insufficient income, excessive debt, lack of emergency savings — that spending can only worsen. A person who responds to financial anxiety by spending creates a self-reinforcing cycle in which the behavior designed to relieve distress actually intensifies the conditions that produce distress. For individuals who have already experienced a budget disruption from emotional spending, understanding how to reset a budget after overspending provides a structured recovery framework.

Emotional spending also does not produce lasting mood improvement. Research on hedonic adaptation demonstrates that the satisfaction derived from material purchases diminishes rapidly as the novelty fades — an effect psychologists call the “hedonic treadmill.” Material purchases generally produce shorter-duration happiness than experiential purchases or investments in relationships and personal development. Understanding this asymmetry can help individuals redirect spending toward experiences that produce more sustained psychological benefit, when spending does occur.

What Is the Difference Between Emotional Spending and Normal Spending?

Normal spending involves purchases that are planned, budgeted, or evaluated against financial goals before completion. Emotional spending occurs when the motivation to purchase originates from an emotional state — stress, sadness, excitement, boredom — rather than from a assessed need or a planned allocation. The distinguishing factor is whether the spending decision passes through rational evaluation or bypasses it due to emotional activation.

Can Emotional Spending Lead to Debt?

Emotional spending can contribute to debt accumulation, particularly when financed through credit cards or BNPL services. Survey data indicates that approximately 43% of self-identified emotional spenders report having incurred debt specifically from emotional purchases. The risk of debt increases when emotional spending occurs frequently, involves high-value items, or is financed through revolving credit that accrues interest on carried balances.

Is Retail Therapy Always Harmful?

Retail therapy — making purchases specifically to improve mood — is not inherently harmful when it occurs within a person’s discretionary budget and does not disrupt financial obligations. Occasional planned indulgences can serve a legitimate function in mood regulation. Retail therapy becomes financially harmful when it occurs impulsively, exceeds budgeted amounts, creates debt, or becomes the primary mechanism for managing emotional distress rather than one option among several coping strategies. Maintaining a structured budgeting framework helps distinguish between affordable discretionary spending and spending that undermines financial stability.

What Are the Most Common Emotional Spending Triggers?

The most frequently reported triggers for emotional spending include stress (reported by approximately 50% of emotional spenders), excitement and happiness (44%), boredom, sadness, and anxiety. Positive and negative emotions can both trigger spending, though the psychological mechanism differs. Negative emotions drive spending as a coping and escape mechanism, while positive emotions drive spending through lowered inhibitions and self-reward framing.

How Can I Tell if I Am an Emotional Spender?

Indicators of emotional spending patterns include: frequent unplanned purchases that were not budgeted, feelings of regret or guilt after buying, difficulty explaining to yourself why you made certain purchases, spending that increases during periods of emotional stress, and accumulation of items that are rarely or never used after purchase. Tracking purchases alongside emotional states for 30 days often reveals patterns that are not visible without deliberate observation.

When Should I Seek Professional Help for Emotional Spending?

Professional help may be warranted when emotional spending produces recurring debt, when a person cannot reduce spending despite conscious effort, when spending interferes with essential financial obligations, or when spending is accompanied by significant shame, secrecy, or relationship conflict. Financial therapists, who integrate psychological techniques with financial planning, specialize in addressing the behavioral and emotional roots of problematic spending patterns. The Financial Therapy Association provides a directory of qualified practitioners.