Table of Contents

Contents are generated from article headings.

Psychology affects financial decisions by introducing cognitive biases, emotional responses, and mental shortcuts that systematically override rational analysis. Behavioral finance research demonstrates that emotions such as fear, greed, and regret influence spending, saving, and investing choices more powerfully than mathematical logic or financial knowledge alone. Cognitive biases like loss aversion cause individuals to feel losses twice as intensely as equivalent gains, leading to risk-averse behavior that limits wealth-building potential. Heuristics—mental shortcuts the brain uses to simplify complex choices—create predictable errors in financial judgment, from anchoring to initial reference points to following crowd behavior during market volatility.

Financial psychology examines how these psychological factors shape money decisions across all income levels and educational backgrounds. The field emerged from recognition that traditional economic models assuming perfect rationality fail to explain real-world financial behavior. Research by Daniel Kahneman and Amos Tversky established that humans consistently deviate from rational choice theory through predictable patterns rooted in evolutionary psychology, emotional processing, and cognitive limitations. These patterns affect everyday financial decisions—impulse purchases, inadequate retirement savings, panic selling during market downturns—as well as long-term wealth accumulation trajectories.

Behavioral finance provides the academic framework for understanding why intelligent, educated individuals often make poor financial choices despite access to accurate information and professional guidance. The discipline combines insights from psychology, neuroscience, and economics to explain phenomena that traditional finance cannot address: market bubbles driven by herd behavior, persistent undersaving despite awareness of retirement needs, emotional spending that conflicts with stated goals. Understanding these psychological mechanisms enables individuals to recognize their own behavioral patterns and implement decision frameworks that work with human psychology rather than assuming unrealistic levels of constant rational analysis.

The practical implications of psychology’s influence on financial decisions extend beyond individual outcomes to affect market-level phenomena, household financial stress, and relationship dynamics around money. Emotional and cognitive patterns explain why budgets fail despite mathematical soundness, why investment strategies get abandoned during volatility, and why couples with identical incomes achieve vastly different financial outcomes. Readers will learn the specific mechanisms through which psychology shapes financial behavior, the risks and failure scenarios these patterns create, practical interventions proven to reduce bias-driven mistakes, and decision frameworks that acknowledge psychological reality while supporting better long-term financial outcomes.

This article covers the causes of psychological influence on money decisions, the mechanisms through which biases and emotions operate, the real-world financial risks these patterns create, evidence-based behavioral interventions, and guidance for making better financial choices despite inherent psychological limitations. The content draws from peer-reviewed behavioral finance research, neuroscience findings on decision-making, and practical applications tested across diverse financial contexts. Understanding how psychology affects financial decisions represents essential knowledge for anyone seeking to improve financial outcomes, reduce money-related stress, or align daily financial behaviors with long-term goals and values.

Understanding the Psychology of Financial Decision Making

The psychology of financial decision making examines how mental processes, emotional states, and cognitive limitations shape choices about money across saving, spending, investing, and risk-taking behaviors. This field recognizes that financial decisions occur within psychological constraints rather than through purely logical analysis. Human brains evolved to handle immediate survival threats and social dynamics, not complex financial calculations involving distant future outcomes and abstract probabilities. This evolutionary mismatch creates systematic patterns in how individuals process financial information and make money-related choices.

Financial decision-making psychology operates through three primary channels: cognitive processes that determine how information gets interpreted, emotional responses that assign value and urgency to choices, and social influences that shape perceived norms and acceptable behaviors. These channels interact continuously, with emotional states affecting which information receives attention, cognitive biases filtering how that information gets processed, and social context influencing which options feel appropriate or desirable. Understanding these mechanisms helps explain why financial knowledge alone rarely translates to optimal financial behavior.

The study of financial decision-making psychology emerged from observed gaps between how traditional economic theory predicted people would behave and how they actually behaved with money. Classical economics assumed rational actors who consistently maximize utility based on complete information and logical analysis. Real-world observation revealed systematic deviations from this model—individuals regularly made choices that reduced their financial well-being when measured against their own stated preferences and long-term goals. This recognition led to development of behavioral finance as a field that incorporates psychological realism into financial analysis.

What Is Financial Psychology?

Financial psychology refers to the study of how psychological factors—including emotions, cognitive biases, personality traits, heuristics, and mental models—influence financial choices and money-related behaviors. This field examines the mental processes underlying decisions about spending, saving, investing, borrowing, and risk-taking across individual, household, and organizational contexts. Financial psychology recognizes that money decisions involve psychological dimensions that operate independently of financial knowledge or mathematical ability.

The scope of financial psychology includes both conscious deliberation and automatic mental processes that occur below awareness. Conscious financial psychology involves explicit reasoning about money choices, weighing options, and intentional decision-making. Automatic financial psychology operates through habitual responses, emotional reactions, and cognitive shortcuts that produce financial behaviors without deliberate thought. Research demonstrates that automatic psychological processes often dominate financial decision-making, particularly for routine choices and during emotional arousal or cognitive overload.

Financial psychology differs from financial education in focus and methodology. Financial education teaches knowledge of concepts, products, and strategies—what individuals should know about money management. Financial psychology examines what individuals actually do with money and why behavior often diverges from knowledge. A person might understand compound interest intellectually yet fail to save consistently due to present bias. Someone might know diversification principles yet concentrate investments based on familiarity bias. Financial psychology addresses this gap between knowledge and behavior through understanding psychological mechanisms.

Money psychology influences financial decisions by shaping how individuals perceive value, assess risk, experience delayed gratification, and respond to gains versus losses. Psychological research demonstrates that humans exhibit loss aversion—feeling losses approximately twice as intensely as equivalent gains. This asymmetry affects risk tolerance, investment holding periods, and willingness to realize losses. Similarly, present bias causes individuals to overweight immediate rewards relative to delayed benefits, explaining persistent undersaving despite intellectual understanding of retirement needs.

The relationship between financial psychology and outcomes operates through accumulated small decisions that compound over time. Daily spending choices influenced by emotional states, investment timing affected by market sentiment, savings consistency determined by willpower depletion—these micro-decisions collectively determine long-term financial trajectories. Financial psychology helps explain why individuals with similar incomes and knowledge achieve different financial outcomes based on behavioral patterns rooted in psychological factors rather than capability or information differences.

Behavioral Finance and Its Role

Behavioral finance represents the academic discipline that systematically studies how psychological phenomena influence financial markets and individual financial decisions. This field emerged in the late 20th century as researchers documented persistent violations of rational choice theory across investment behavior, market pricing, and personal finance decisions. Behavioral finance integrates insights from cognitive psychology, social psychology, and neuroscience into financial analysis, creating frameworks that explain real-world financial behavior more accurately than traditional models assuming perfect rationality.

The role of behavioral finance extends beyond explaining individual mistakes to modeling market-level phenomena that rational frameworks cannot address. Market bubbles, crashes, momentum effects, and volatility clustering all reflect psychological factors operating at scale. When individual investors exhibit herd behavior—following crowd decisions due to social proof and fear of missing out—these individual biases aggregate into market-wide mispricing. Behavioral finance provides tools for understanding these collective patterns through psychological mechanisms rather than treating them as anomalies requiring separate explanation.

Behavioral finance challenges traditional rational-agent models by demonstrating that observed violations of rational choice occur systematically rather than randomly. If deviations from rationality were random, they would cancel out across large populations, leaving aggregate behavior consistent with rational models. Instead, research documents predictable directional biases—loss aversion causing consistent risk aversion in gains and risk-seeking in losses, overconfidence producing excessive trading, confirmation bias creating persistent mispricing. These systematic patterns require psychological explanation rather than statistical noise interpretation.

Daniel Kahneman and Amos Tversky’s Prospect Theory represents foundational behavioral finance research explaining how people actually make decisions under uncertainty versus how rational choice theory predicts they should decide. Prospect Theory demonstrates that individuals evaluate outcomes relative to reference points rather than absolute wealth levels, exhibit loss aversion, and weight probabilities non-linearly. These findings explain phenomena like the disposition effect—investors’ tendency to sell winning investments too quickly while holding losing investments too long—through psychological mechanisms rather than rational strategy.

Behavioral finance explains deviations from rational choice through documented cognitive limitations and emotional influences rather than assuming irrationality or lack of intelligence. The field recognizes that psychological biases often served adaptive functions in evolutionary environments even when they produce suboptimal outcomes in modern financial contexts. For example, loss aversion protected ancestors from risks that could threaten survival, though it now causes excessive risk aversion in investment contexts where diversified long-term exposure would serve better. Understanding these evolutionary roots helps frame biases as natural human tendencies requiring management rather than personal failures requiring correction through willpower alone.

Neuroscience and Decision-Making

Neuroscience research reveals the brain mechanisms underlying financial decision-making, demonstrating how neural processes shape risk perception, reward evaluation, and emotional influences on money choices. Brain imaging studies show that financial decisions activate both rational analysis regions in the prefrontal cortex and emotional processing areas in the limbic system, with the interaction between these systems determining actual choices. This neurological architecture means purely rational financial decision-making rarely occurs—emotion and cognition interact continuously in normal brain function.

Risk perception in financial decisions involves the amygdala—a brain region processing threat detection and emotional responses—which activates more strongly during potential losses than equivalent gains. This neural asymmetry provides biological basis for loss aversion documented in behavioral finance research. The amygdala’s threat response to financial losses can override prefrontal cortex analysis, explaining why individuals make defensive choices during market volatility despite logical arguments for maintaining long-term investment strategies. Understanding this neural mechanism helps explain why emotional regulation techniques prove essential for consistent financial decision-making.

Reward processing in financial contexts activates the brain’s dopamine system, particularly the nucleus accumbens and ventral striatum regions associated with anticipation and experience of pleasure. Research shows these reward centers respond more intensely to potential gains than actual gains, explaining why anticipation drives speculative behavior and why realized gains often feel less satisfying than expected. This neural pattern contributes to excessive risk-taking in pursuit of reward anticipation and disappointment with achieved outcomes that fail to match anticipated pleasure.

The Somatic Marker Hypothesis, developed by neuroscientist Antonio Damasio, proposes that bodily emotional signals guide decision-making through learned associations between choices and emotional outcomes. According to this framework, the body generates physiological responses—increased heart rate, muscle tension, gut feelings—when considering options previously associated with positive or negative outcomes. These somatic markers influence decisions by creating emotional biases toward or against specific choices before conscious analysis completes. In financial contexts, somatic markers explain gut reactions to investment opportunities, anxiety around spending decisions, and emotional discomfort with certain financial strategies.

Somatic markers bias risk evaluation by associating bodily sensations with financial choices based on past experiences. An investor who experienced significant losses during a market crash might develop negative somatic markers—anxiety, tension, avoidance—activated when considering equity investments, even when current analysis suggests appropriate risk levels. Similarly, someone who profited from speculative investments might develop positive somatic markers that override rational caution about concentration risk. These learned emotional responses operate faster than conscious analysis and often determine initial reactions to financial decisions that subsequent reasoning struggles to override.

Mechanisms of Psychological Influence on Money Decisions

Psychological mechanisms influence money decisions through systematic patterns in how the brain processes financial information, evaluates options, and generates behavioral responses. These mechanisms operate through cognitive biases that distort perception and judgment, emotional responses that alter risk tolerance and time preferences, and heuristics that simplify complex choices through mental shortcuts. Understanding these mechanisms enables recognition of when psychological factors likely override rational analysis and implementation of decision frameworks that account for these influences.

The influence of psychological mechanisms on financial decisions varies based on decision complexity, emotional state, time pressure, and individual differences in cognitive capacity and self-regulation. Simple, familiar financial choices might engage minimal conscious processing, relying primarily on habits and heuristics developed through past experiences. Complex, novel financial decisions—major purchases, investment strategy changes, debt management approaches—require more deliberate analysis but remain vulnerable to cognitive biases and emotional influences that shape which information receives attention and how alternatives get evaluated.

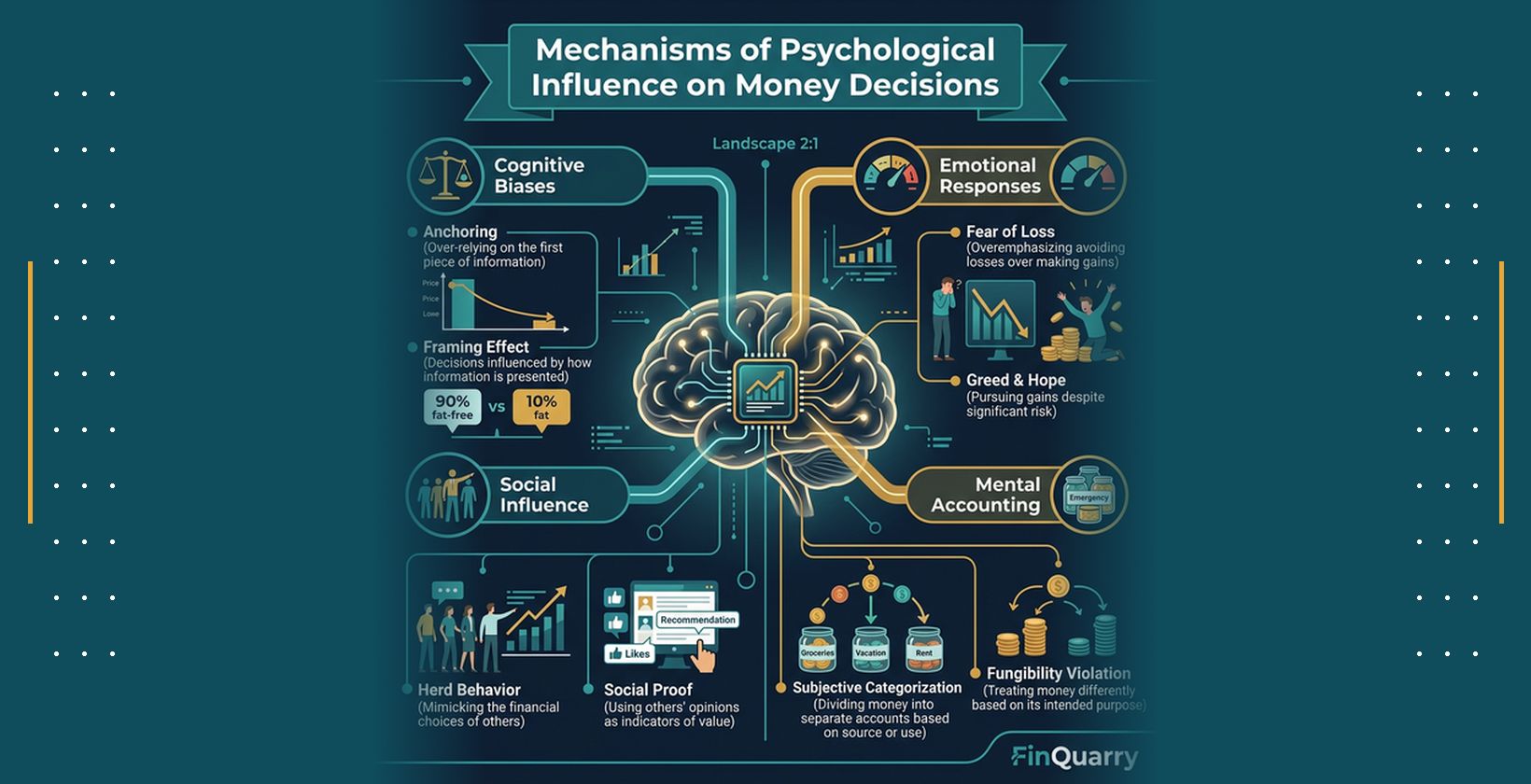

Cognitive biases represent systematic patterns in judgment and decision-making that deviate from normative standards of logic and probability. These biases result from the brain’s reliance on simplified mental models and limited information processing capacity. Rather than analyzing every financial decision comprehensively, the brain applies rules of thumb, makes assumptions based on limited data, and satisfices—choosing options that meet minimum criteria rather than optimizing across all possibilities. While these cognitive shortcuts enable efficient decision-making, they create predictable errors when applied to financial contexts requiring careful probability assessment and long-term outcome consideration.

Emotional influences on money decisions operate through multiple pathways: affecting which information receives attention, altering risk perception and tolerance, changing time preferences between immediate and delayed outcomes, and triggering behavioral responses that bypass analytical reasoning. Fear constricts attention toward threats and triggers defensive behaviors like avoiding risk or selling investments during downturns. Greed expands risk tolerance and increases focus on potential gains while diminishing attention to downside possibilities. These emotional influences often operate unconsciously, shaping decisions through feelings rather than explicit emotional awareness.

Heuristics and mental shortcuts enable rapid decision-making by applying simple rules to complex situations without complete information processing. While heuristics serve valuable functions in many contexts, they create systematic financial decision errors when the simplified rules fail to match actual financial relationships. Mental accounting—treating money differently based on arbitrary categories—helps manage budgets through psychological separation but can lead to inefficient allocation when high-interest debt coexists with low-return savings. Understanding how heuristics influence financial decisions allows designing choice architectures that work with these mental shortcuts rather than requiring their elimination.

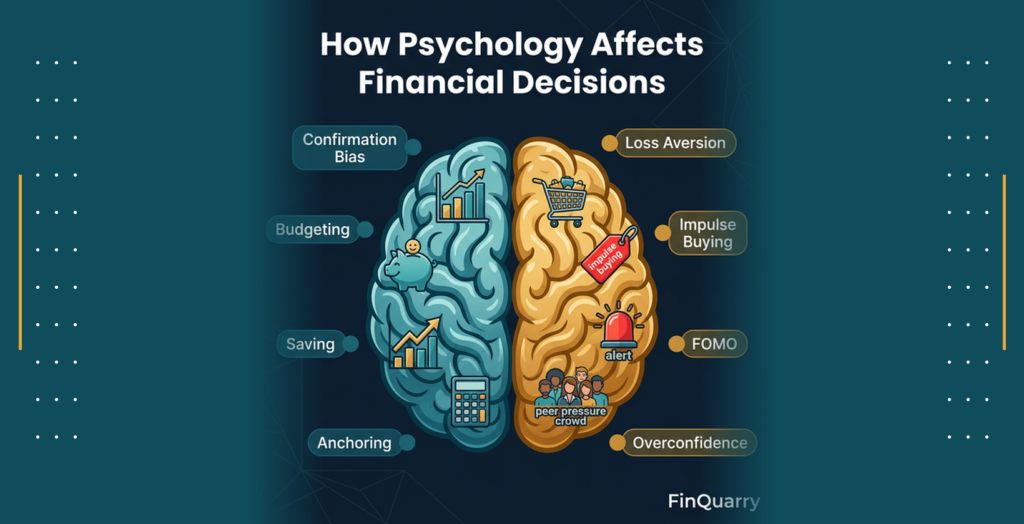

Cognitive Biases in Financial Behavior

Cognitive biases in financial behavior represent systematic patterns of judgment and decision-making that consistently deviate from optimal financial choices. These biases result from the brain’s reliance on mental shortcuts, limited processing capacity, and evolutionary adaptations that prioritized survival over wealth optimization. Behavioral finance research documents dozens of cognitive biases affecting financial decisions, with several showing particularly strong influence on investment behavior, spending patterns, and long-term financial outcomes. Understanding specific biases enables recognition of when they likely influence decisions and implementation of mitigation strategies.

Loss Aversion

Loss aversion describes the tendency to experience losses approximately twice as intensely as equivalent gains, creating asymmetric responses to positive and negative financial outcomes. This bias causes individuals to take excessive risk to avoid losses while exhibiting excessive caution to protect gains. Research demonstrates that most people reject bets offering equal probability of winning or losing money even when the potential win exceeds the potential loss, requiring win-to-loss ratios of approximately 2:1 before accepting such gambles.

Loss aversion affects financial decisions by causing investors to hold losing investments too long while selling winning investments too quickly, a pattern called the disposition effect. When facing paper losses, loss aversion creates strong motivation to avoid realizing the loss, leading to extended holding periods hoping for recovery. Conversely, paper gains trigger desire to lock in the win before it disappears, causing premature selling. This pattern reduces investment returns by extending exposure to underperforming assets while limiting gains from successful investments.

In personal finance contexts, loss aversion manifests as excessive risk aversion that prevents appropriate equity allocation despite long time horizons. Individuals experiencing loss aversion might maintain excessive cash holdings earning minimal returns to avoid potential investment losses, sacrificing long-term wealth accumulation to prevent psychological pain of temporary market declines. This bias explains why many people avoid equity investments entirely after experiencing market downturns, missing subsequent recoveries that restore and exceed prior values.

Loss aversion prioritizes avoiding loss over equivalent gains through neural mechanisms that process losses more intensely than gains. Brain imaging research shows stronger activation in emotion-processing regions during losses compared to equivalent gains, providing biological basis for the asymmetric psychological impact. This neural asymmetry means loss aversion represents a fundamental aspect of human decision-making rather than a correctable error, requiring decision frameworks that acknowledge this bias rather than assuming it can be eliminated through education alone.

Anchoring

Anchoring bias causes individuals to rely heavily on initial information—the anchor—when making subsequent judgments, even when the anchor lacks relevance to the decision. In financial contexts, anchoring affects price perceptions, investment valuations, spending decisions, and negotiation outcomes. Original prices serve as anchors making discounted prices appear more attractive regardless of actual value. Purchase prices anchor investment decisions, causing investors to evaluate positions relative to cost basis rather than current value and future prospects.

Anchoring influences financial behavior by distorting value assessments based on arbitrary reference points. Retailers exploit anchoring by displaying high original prices before showing discounts, making the sale price appear more attractive even if it represents standard market value. Investors anchor to purchase prices when evaluating whether to hold or sell positions, treating recovery to break-even as psychologically important despite economic irrelevance—the decision should depend on future prospects relative to alternative investments, not historical cost.

The mechanism underlying anchoring involves insufficient adjustment from initial reference points. When presented with an anchor, individuals make adjustments but typically stop before reaching values they would have generated without the anchor’s influence. This insufficient adjustment occurs because the brain uses the anchor as a starting point for evaluation, then adjusts until reaching a value that feels plausible, often stopping before reaching optimal estimates. Anchoring persists even when individuals recognize the anchor as irrelevant, demonstrating the bias’s resistance to conscious override.

Anchoring distorts decision accuracy by introducing irrelevant information into valuation processes. In investment contexts, anchoring to historical prices—whether purchase price, 52-week highs, or recent peaks—prevents objective evaluation of current value relative to alternatives. An investor anchored to a stock’s prior high might wait for return to that level before selling, ignoring evidence that fundamental value has permanently declined. This anchoring-driven behavior increases exposure to declining assets while opportunity cost accumulates through delayed reallocation to better prospects.

Present Bias

Present bias describes the tendency to overweight immediate outcomes relative to delayed outcomes beyond what would occur through rational time discounting. This bias causes individuals to prefer smaller immediate rewards over larger delayed rewards at rates inconsistent with their own stated time preferences. Present bias explains persistent undersaving despite awareness of retirement needs, excessive current consumption despite future financial goals, and difficulty maintaining beneficial behaviors requiring immediate effort for delayed benefits.

Present bias affects financial decisions by making future consequences feel less important than immediate gratification, leading to choices that provide short-term satisfaction while undermining long-term financial security. Individuals exhibiting present bias might choose to spend money immediately rather than save for retirement despite intellectually valuing future security, skip bill payments to maintain current spending, or choose high-interest convenient credit over lower-cost alternatives requiring upfront effort. These choices reflect genuinely different preferences across time rather than simple miscalculation.

The mechanism underlying present bias involves hyperbolic discounting—applying higher discount rates to near-term tradeoffs than distant tradeoffs. An individual might prefer $100 today over $110 tomorrow (implying extremely high discount rate) while simultaneously preferring $110 in 31 days over $100 in 30 days (implying much lower discount rate). This time inconsistency reveals that present bias stems from special status assigned to immediate outcomes rather than consistent time preferences, making the bias particularly difficult to overcome through rational analysis alone.

Present bias reduces long-term financial planning effectiveness by causing repeated preference reversals that undermine sustained beneficial behaviors. An individual might sincerely commit to starting a savings plan next month while continuing to spend available funds currently. When next month arrives, the same present bias makes current spending feel more important than saving, perpetuating procrastination. This pattern explains why many people delay starting beneficial financial behaviors indefinitely despite never intending to permanently forgo them—each present moment receives privileged status over future moments.

Overconfidence

Overconfidence bias causes individuals to overestimate their knowledge, abilities, and the precision of their beliefs about financial matters. This bias manifests as excessive certainty in market predictions, underestimation of investment risks, overestimation of stock-picking abilities, and insufficient recognition of uncertainty in financial outcomes. Overconfidence particularly affects active investors who believe their analysis provides edge over market consensus despite evidence that most active trading reduces returns after accounting for transaction costs.

Overconfidence influences financial behavior by increasing trading frequency, reducing diversification, and creating excessive risk exposure. Overconfident investors trade more frequently based on beliefs that their analysis identifies mispriced securities, generating transaction costs that typically exceed any skill-based returns. They concentrate portfolios in positions where they feel highest conviction, reducing diversification below optimal levels. They underestimate downside risks while overestimating upside potential, leading to risk exposure exceeding appropriate levels for their actual risk tolerance and financial situation.

The mechanism underlying overconfidence involves multiple cognitive patterns: better-than-average effect (believing one’s abilities exceed typical levels), illusion of control (overestimating ability to influence outcomes), and miscalibration (assigning excessive confidence to judgments). Individuals displaying overconfidence might believe their investment analysis exceeds average quality despite statistical impossibility that most investors achieve above-average results. They might feel their actions influence investment outcomes more than warranted by actual control, leading to excessive trading and attention.

Overconfidence increases trading costs and reduces portfolio returns through excessive turnover driven by unjustified certainty in market timing or security selection abilities. Research demonstrates that investors who trade most frequently typically achieve the lowest returns after accounting for transaction costs, consistent with overconfidence-driven excessive trading. The bias also increases vulnerability to concentrated positions that create unnecessary volatility and downside risk when high-conviction positions fail to perform as expected, demonstrating how psychological certainty can generate financial vulnerability.

Confirmation Bias

Confirmation bias describes the tendency to seek, interpret, and remember information that confirms existing beliefs while dismissing or minimizing contradictory evidence. In financial contexts, this bias causes investors to selectively attend to information supporting their investment theses while ignoring warning signs. Individuals exhibiting confirmation bias construct echo chambers of self-reinforcing information that strengthen confidence in potentially flawed financial decisions, increasing vulnerability to significant losses when contradictory evidence accumulates beyond ignorable levels.

Confirmation bias affects financial decisions by preventing objective evaluation of information and maintaining commitment to failing strategies longer than warranted. An investor bullish on a stock might focus on positive news and analyst reports while dismissing negative developments as temporary or irrelevant. This selective attention delays recognition of fundamental deterioration until losses accumulate substantially. In personal finance, confirmation bias causes individuals to seek information validating desired purchases while avoiding analysis that might reveal unaffordability or poor value.

The mechanism underlying confirmation bias involves directional information processing where existing beliefs shape attention, interpretation, and memory. Attention naturally focuses on information consistent with expectations, as the brain efficiently processes confirming information while requiring more effort to integrate contradictory data. Ambiguous information gets interpreted in ways supporting existing beliefs through motivated reasoning. Memory more readily encodes and retrieves confirming information while contradictory information decays faster, creating biased information samples when making subsequent decisions.

Confirmation bias reinforces poor financial decisions by creating self-confirming information environments that prevent course correction until damage becomes severe. The bias increases holding periods for deteriorating investments as investors attend only to information suggesting eventual recovery while dismissing evidence of permanent impairment. It perpetuates ineffective personal finance behaviors by supporting rationalizations for continuing problematic patterns while minimizing information suggesting need for change. Breaking confirmation bias requires deliberate seeking of contradictory evidence and objective evaluation mechanisms that override natural selective attention.

Herd Mentality

Herd mentality describes the tendency to follow crowd behavior and make decisions based on what others are doing rather than independent analysis. In financial contexts, herd behavior manifests as buying investments because prices are rising and others are buying (FOMO—fear of missing out) or selling because prices are falling and others are selling (panic). This social influence creates market phenomena like bubbles, crashes, and momentum effects where price movements become self-reinforcing through behavioral feedback loops rather than reflecting fundamental value changes.

Herd mentality affects financial decisions through multiple psychological mechanisms: social proof (inferring correctness from others’ actions), conformity pressure (desire to match group behavior), and information cascades (assuming others possess relevant information). When investors observe others profiting from specific investments, social proof suggests those investments must be sound even without personal analysis. Conformity pressure makes contrarian positions psychologically uncomfortable, increasing tendency to match crowd behavior. Information cascades occur when individuals assume others have valid reasons for their choices and follow suit without independent verification.

Herd behavior causes irrational market behavior by creating price movements disconnected from fundamental value changes. During bubbles, herd buying drives prices beyond levels justified by earnings, growth prospects, or asset values. Each price increase attracts additional buyers through social proof and fear of missing gains, creating self-reinforcing upward spirals. When sentiment shifts, herd selling produces equally irrational price collapses as each decline triggers additional selling through fear of further losses. These patterns demonstrate how individual biases aggregate into market-level inefficiency through behavioral synchronization.

Herd mentality contributes to market bubbles through positive feedback loops where price increases attract buyers whose purchases drive further increases, repeating until some trigger breaks confidence. Historical bubbles—Dutch tulip mania, dot-com boom, housing bubble—all exhibited herd behavior where social proof and fear of missing out drove participation beyond levels supported by fundamental analysis. The psychological mechanism involves conformity overwhelm where social pressure to participate exceeds individual judgment capacity, causing mass participation in obviously overvalued markets that subsequently crash when herd reverses.

Emotional Influences on Decisions

Emotional influences on financial decisions operate through direct effects on choice behavior and indirect effects on information processing and risk perception. Emotions activate physiological responses, shift attention toward emotion-congruent information, alter risk tolerance, and can trigger immediate behavioral responses that bypass analytical reasoning. While traditional finance assumed emotions represent noise interfering with rational decisions, research demonstrates that emotions serve important decision-making functions while also creating systematic biases requiring management for optimal financial outcomes.

Fear represents one of the most powerful emotional influences on financial decisions, typically increasing risk aversion and triggering defensive behaviors. During market volatility or personal financial stress, fear narrows attention toward threats while reducing consideration of opportunities. This threat focus causes excessive portfolio conservatism, panic selling during downturns, and paralysis around necessary financial decisions perceived as risky. Fear-driven financial behavior prioritizes immediate threat reduction over long-term optimization, explaining why investors sell positions during market crashes despite logical arguments for maintaining exposure through recovery cycles.

Fear drives risk-averse choices through neural mechanisms that prioritize immediate threat response over analytical decision-making. The amygdala—brain region processing fear and threat detection—can override prefrontal cortex functions responsible for logical analysis when threat perception becomes intense. In financial contexts, market losses or job insecurity activate fear responses that make conservative options feel compelling regardless of long-term implications. This neural override explains why fear-driven decisions often conflict with individuals’ stated risk tolerance measured during calm periods—the emotional state fundamentally changes decision-making processes.

Greed and excessive optimism create opposite distortions, increasing risk tolerance beyond appropriate levels and focusing attention on potential gains while minimizing downside risks. During bull markets or when hearing about others’ investment success, greed can trigger speculative behavior, concentrated positions, and use of leverage to amplify returns. The emotional reward anticipated from large gains overwhelms consideration of loss probabilities or portfolio risk, explaining why individuals sometimes take risks they later recognize as excessive when emotional state normalizes.

Greed leads to over-risking and speculative behavior through reward system activation that creates urgency around potential gains. The brain’s dopamine pathways respond strongly to anticipated rewards, creating powerful motivation to pursue actions expected to generate pleasure or profit. In financial contexts, greed-driven reward anticipation can overwhelm analytical evaluation of risk-return tradeoffs. Investors experiencing greed might concentrate portfolios in high-risk positions, use leverage to amplify exposure, or chase performance by buying recent winners at elevated valuations, all while minimizing attention to downside scenarios.

Regret—both anticipated regret about potential outcomes and experienced regret about past decisions—substantially influences financial behavior. Anticipated regret about missing gains drives FOMO behavior and trend-following, as the psychological pain of watching others profit while sitting on sidelines feels worse than potential losses from joining late. Experienced regret about past losses or missed opportunities can cause either excessive caution (avoiding actions that previously led to regret) or reactive overcorrection (taking opposite actions without adequate analysis).

Regret creates hesitation in investing and spending through fear of negative outcomes that will feel worse due to personal responsibility. Individuals avoiding investment decisions might be postponing to prevent potential regret about losses more than rationally assessing probabilities. Regret also manifests as action inaction bias—tendency to regret harmful actions more than equally harmful inactions. This bias causes people to maintain status quo positions (inaction) even when analysis suggests change would improve outcomes, because losses from action feel more regrettable than equal losses from inaction.

Anxiety about financial matters creates avoidance behaviors where individuals postpone or completely avoid necessary financial decisions due to stress and uncertainty. Anxiety narrows cognitive resources, making complex financial decisions feel overwhelming. This overwhelm triggers avoidance as coping mechanism, explaining why people delay reviewing finances, postpone retirement planning, or avoid addressing debt despite knowing these behaviors worsen outcomes. Anxiety-driven avoidance operates through immediate stress relief (avoiding uncomfortable tasks) despite creating long-term financial vulnerability.

Anxiety drives avoidance of complex financial decisions through cognitive resource depletion and threat perception. Complex decisions requiring analysis of multiple factors, probability assessment, and long-term consequence consideration demand substantial cognitive effort. When anxiety depletes available cognitive resources, these complex decisions feel impossibly difficult, triggering avoidance or oversimplified heuristic-based choices. The brain prioritizes immediate anxiety reduction over long-term optimization, making avoidance feel like stress management even while knowing it perpetuates problems.

Heuristics and Mental Shortcuts

Heuristics represent mental shortcuts or rules of thumb that enable rapid decision-making without comprehensive information processing. These cognitive strategies evolved to handle routine decisions efficiently by applying simple rules to complex situations, conserving cognitive resources for novel or critical problems. While heuristics serve valuable functions in many contexts, they create systematic errors when applied to financial decisions requiring careful probability assessment, long-term thinking, or numerical precision. Understanding common heuristics helps identify when they likely influence financial choices and enables implementation of decision frameworks that override problematic mental shortcuts.

Mental accounting describes the cognitive tendency to treat money differently based on arbitrary categories rather than recognizing fungibility—the principle that money has equivalent value regardless of source or intended use. Individuals exhibiting mental accounting might maintain separate mental or actual accounts for different purposes (vacation fund, emergency savings, investing) while applying different rules to each category. This compartmentalization helps with budgeting and self-control but can lead to inefficient overall resource allocation when high-interest debt coexists with low-return savings or when arbitrary category constraints prevent optimal choices.

Mental accounting affects financial behavior by creating psychological separation that enables contradictory simultaneous behaviors. An individual might aggressively save in a retirement account earning 8% annually while carrying credit card debt costing 20% interest—mental accounting makes these feel like separate decisions rather than a combined strategy destroying wealth through negative arbitrage. Similarly, people treat “found money” like bonuses or tax refunds differently than regular income, spending it more freely despite economic equivalence. This differential treatment violates rational money management but serves psychological functions around self-control and goal achievement.

Mental accounting leads to inefficient allocation when category-based rules prevent optimal resource deployment. The bias might cause someone to refuse withdrawing from emergency savings to pay off high-interest debt because the mental account labels prevent recognizing this as wealth-destroying behavior. Conversely, mental accounting might enable beneficial behaviors that would fail without psychological separation—an individual struggling with spending might successfully save through automatic deductions into retirement accounts that feel off-limits despite being legally accessible.

The availability heuristic causes individuals to judge probability and frequency based on how easily examples come to mind rather than actual statistical likelihood. Vivid, recent, or emotionally charged events dominate memory and feel more probable than they actually are, while common but mundane events feel less likely. In financial contexts, availability heuristic explains excessive fear of rare but salient risks like fraud or market crashes while underestimating common risks like inflation eroding purchasing power or insufficient retirement savings.

Availability heuristic distorts risk perception by overweighting memorable events in probability judgments. After hearing about someone’s investment fraud loss, individuals overestimate fraud risk and might avoid investments entirely despite statistical rarity. Following market crashes, availability makes downside risks feel overwhelming, causing excessive conservatism that misses recoveries. Conversely, during bull markets, recent gains dominate memory making further gains feel inevitable and downside risk feel distant, contributing to overconfidence and excess risk-taking at market peaks.

Availability heuristic operates through memory accessibility determining perceived frequency—events that come to mind easily feel more common than events requiring effort to recall. Media coverage, personal experience, and emotional intensity all increase availability, making these factors influence risk perception more than actual statistical frequency. A dramatic news story about financial disaster creates strong memory traces that surface easily when considering related decisions, making similar outcomes feel probable despite actual rarity. This memory-based judgment process enables quick assessment but systematically distorts probability evaluation.

The Impact and Importance of Psychology in Financial Decisions

Psychology’s impact on financial decisions extends from individual money choices to household financial outcomes, market-level phenomena, and broader economic patterns. Understanding psychological influences matters because these factors determine whether financial knowledge translates to beneficial behavior, whether sound financial strategies get maintained through implementation, and whether long-term financial goals get achieved through consistent daily choices. The importance of psychology in finance increases with decision complexity, emotional stakes, and time horizons—precisely the conditions characterizing major financial choices most affecting life outcomes.

Research demonstrates that psychological factors often influence financial outcomes more powerfully than financial knowledge or mathematical ability. Studies comparing individuals with varying financial literacy levels show that behavioral consistency—maintaining savings habits, avoiding emotional investment decisions, resisting lifestyle inflation—predicts wealth accumulation more strongly than test scores measuring financial knowledge. This finding suggests that psychological self-awareness and behavioral management represent critical skills for financial success independent of technical financial expertise.

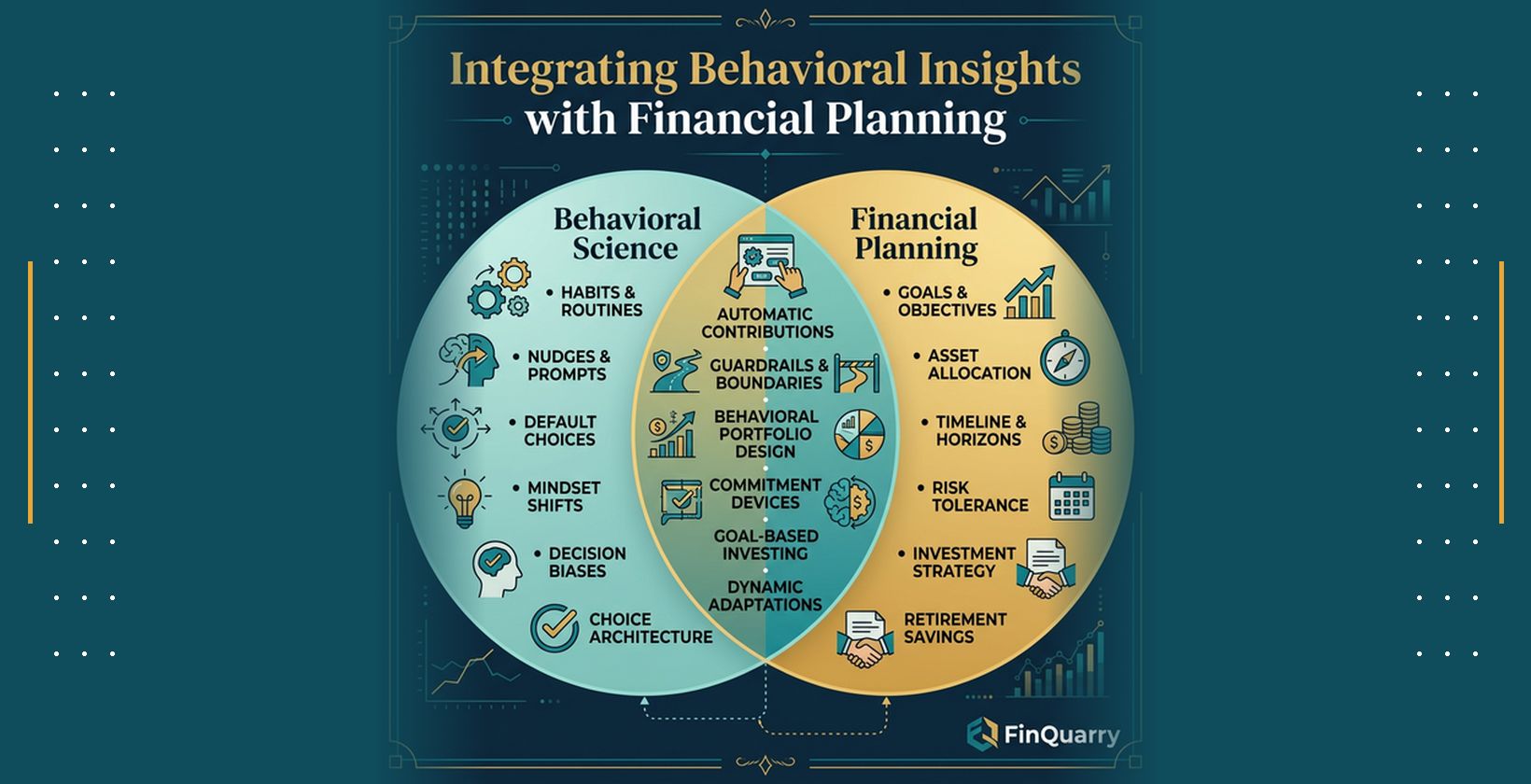

The importance of understanding psychology in financial decisions reflects the gap between optimal theoretical strategies and realistic implementation given human limitations. Financial advice often assumes unlimited willpower, constant rational analysis, and emotional neutrality—assumptions violated by psychological reality. Effective financial decision-making requires strategies acknowledging psychological constraints: automating beneficial behaviors to reduce reliance on willpower, implementing commitment devices that prevent future selves from reversing current intentions, and designing choice architectures that work with rather than against natural human tendencies toward present bias, loss aversion, and social influence.

Real-World Financial Outcomes

Psychology explains real-world financial outcomes including undersaving, panic selling, and overspending through mechanisms that cause behavioral patterns inconsistent with stated financial goals and values. These behavioral patterns result from psychological influences overriding intellectual understanding of beneficial financial practices. An individual might intellectually recognize retirement savings importance while exhibiting present bias that makes current spending feel more compelling than distant retirement security, resulting in undersaving despite awareness. This disconnect between knowledge and behavior characterizes many financial struggles rooted in psychological rather than informational deficits.

Undersaving for retirement represents a widespread financial outcome explained primarily by psychological factors rather than income constraints or knowledge gaps. Present bias makes immediate consumption more psychologically compelling than saving for retirement decades away, even when individuals intellectually value future security. Procrastination—itself rooted in present bias and decision avoidance—leads to delayed savings start dates that dramatically reduce final retirement assets through lost compound growth. Optimism bias causes underestimation of required savings by assuming future income increases will enable later catch-up, often failing to materialize as competing priorities absorb income growth.

Panic selling during market volatility demonstrates how emotional responses override rational investment strategy, destroying wealth through poorly-timed exits that lock in losses and miss recoveries. When market values decline significantly, fear activates threat responses that make selling feel necessary despite intellectual understanding that long-term investment strategies require maintaining exposure through market cycles. Loss aversion intensifies this fear by making losses feel more painful than equivalent gains feel pleasurable, creating overwhelming motivation to stop the pain through selling. Investors who panic sell typically re-enter markets after prices recover, buying high and selling low in patterns destroying long-term returns.

Overspending relative to income reflects multiple psychological influences including present bias, lifestyle inflation, social comparison, and emotional regulation through consumption. Present bias makes immediate gratification from purchases feel more important than long-term financial security, explaining persistent overspending despite awareness of consequences. Lifestyle inflation—automatically increasing spending to match income growth—reflects adaptation to reference points where previous luxuries become perceived necessities. Social comparison drives spending to signal status or maintain perceived standing relative to peer groups, often creating consumption patterns unsustainable relative to actual financial capacity.

Cognitive and emotional patterns impact wealth-building capacity through accumulated effects of thousands of small decisions over time. An individual exhibiting strong present bias might make marginally different consumption choices each day—slightly higher spending on convenience, entertainment, or status goods—that individually feel insignificant but compound to thousands annually. Over decades, these accumulated differences combined with investment return differentials create substantial wealth gaps between individuals with similar incomes but different psychological patterns around delayed gratification, lifestyle inflation, and emotional spending.

Investor Behavior and Market Phenomena

Investor behavior driven by emotional and psychological biases creates market-level phenomena including bubbles, crashes, and persistent trends that traditional efficient market theory cannot explain. When individual psychological biases synchronize across many investors—herd behavior causing simultaneous buying or selling, overconfidence creating excessive trading, loss aversion triggering coordinated exit during downturns—these individual patterns aggregate into observable market inefficiencies. Understanding how psychology shapes investor behavior helps explain why markets exhibit volatility exceeding what fundamental value changes would justify.

Market bubbles demonstrate psychological influences operating at scale through positive feedback loops where price increases attract attention, generate social proof of investment validity, trigger fear of missing out, and drive additional buying that pushes prices higher still. During bubbles, fundamental valuation analysis gets dismissed through confirmation bias and rationalization while psychological factors dominate decision-making. The dot-com bubble of the late 1990s exhibited classic psychological bubble patterns: extrapolation of recent trends (availability heuristic), belief that traditional valuation metrics no longer applied (overconfidence and confirmation bias), and herd behavior as social proof of stock gains drove increasingly aggressive participation.

Market crashes reflect synchronized fear responses where declining prices trigger panic selling that drives prices lower in self-reinforcing downward spirals. Loss aversion makes losses feel particularly painful, creating strong motivation to exit positions before losses grow. As prices fall, availability of negative news increases, making further declines feel inevitable. Herd behavior synchronizes selling as social proof suggests others possess information justifying exit. These psychological factors create market crashes where selling overwhelms buying, driving prices temporarily below levels supported by fundamental analysis until fear subsides and rational buying resumes.

Herd behavior contributes to market bubbles through social proof mechanisms where individuals infer decision quality from others’ actions, creating information cascades where everyone follows the crowd regardless of private information or analysis. During market rallies, observing others profit from investments creates powerful social proof that these investments must be sound. Fear of missing out adds emotional urgency to participation before prices rise further. Each person joining the trend provides additional social proof to others, creating self-reinforcing cycles where crowd behavior becomes self-validating until some event breaks confidence and reverses the herd.

Emotional and bias-driven market behavior creates systematic deviations from efficient market predictions including momentum effects where recent price trends continue longer than fundamental justification, overreaction where prices move more than new information warrants, and volatility clustering where high volatility periods persist. These patterns reflect psychological influences—trend-following based on availability and herd behavior creates momentum, overconfidence and availability cause overreaction to news, and fear synchronization creates volatility clustering. While these inefficiencies create opportunities for disciplined contrarian investors, most individuals reinforce rather than exploit them through bias-driven participation.

Five Common Emotional Biases Affecting Financial Decisions

Five emotional biases consistently emerge as particularly influential across personal finance and investment contexts, each creating distinct patterns of suboptimal financial behavior. These biases—loss aversion, overconfidence, herd mentality, regret-driven emotional spending, and present bias—operate through different psychological mechanisms but share common features: they override rational analysis during emotionally charged decisions, they persist despite awareness and education, and they require behavioral interventions rather than just information to mitigate effectively.

Loss Aversion in Personal Finance

Loss aversion affects personal finance decisions by making risk feel more significant than equivalent opportunity, causing excessive financial conservatism that prevents appropriate wealth-building strategies. Individuals experiencing strong loss aversion might maintain excessive emergency savings earning minimal returns while avoiding equity investments despite long time horizons where equity exposure would likely enhance outcomes. This bias also manifests as extreme debt aversion where individuals prioritize any debt elimination over investment even when debt carries low interest rates and investment returns would exceed borrowing costs, violating wealth optimization through excessive focus on avoiding negative account balances.

Loss aversion creates reluctance to change financial strategies even when current approaches clearly fail, because changing feels like admitting failure and accepting associated psychological loss. Someone maintaining ineffective budgeting system might continue despite poor results because abandoning the approach feels like accepting defeat. This status quo bias reinforced by loss aversion causes financial inertia where suboptimal situations persist because change requires accepting psychological losses even when leading to better future outcomes.

Overconfidence in Investment Decisions

Overconfidence particularly damages investment outcomes through excessive trading based on unjustified conviction in market timing or security selection abilities. Research demonstrates that investors who trade most frequently typically achieve the lowest returns after accounting for transaction costs, consistent with overconfidence-driven excessive activity. The bias also causes insufficient diversification as overconfident investors concentrate holdings in positions where they feel highest conviction, increasing portfolio volatility and downside risk when concentrated positions underperform.

Overconfidence manifests in personal finance through underestimation of expenses, overestimation of future income growth, and excessive optimism about ability to change spending habits. Individuals exhibiting overconfidence might commit to mortgages or other obligations based on optimistic income projections that fail to materialize, creating financial stress when reality falls short of confident predictions. The bias prevents adequate emergency savings through underestimation of job loss probability or medical emergency likelihood, leaving individuals vulnerable when adverse events occur at rates matching statistical norms rather than optimistic personal estimates.

Herd Mentality in Consumer Behavior

Herd mentality extends beyond investment contexts to affect consumer spending decisions through social proof and conformity pressure. Observing peer group spending patterns creates perceived norms that feel compelling to match, explaining lifestyle inflation and consumption beyond financial means to maintain social standing. The bias drives spending on visible consumption that signals status—vehicles, homes, clothing, experiences—while potentially neglecting less visible but financially beneficial behaviors like adequate retirement savings or debt reduction.

Social media intensifies herd mentality’s influence on spending by increasing exposure to others’ consumption patterns and creating pressure to participate in experiences, purchases, or lifestyle choices that might exceed personal financial capacity. The curated nature of social media content—showing highlights while hiding financial stress—makes peer spending appear easily affordable, normalizing consumption levels that actually strain many participants’ finances. This social comparison–driven spending explains significant financial stress among individuals with adequate or even high incomes who overspend relative to peer reference groups.

Regret and Emotional Spending

Regret influences financial behavior both prospectively (anticipated regret about future outcomes) and retrospectively (experienced regret about past choices). Anticipated regret drives FOMO spending on experiences or investments to avoid future regret about missing out, often leading to participation in overpriced opportunities or consumption beyond true preferences. Retrospective regret about past financial mistakes can cause either excessive caution that prevents beneficial risk-taking or reactive overcorrection taking opposite actions without adequate analysis.

Emotional spending represents purchasing behavior driven primarily by emotional regulation needs rather than genuine consumption needs or values. Individuals might shop when stressed, bored, sad, or celebratory as coping mechanism, using purchases to generate temporary positive emotion or distract from negative states. This emotional spending creates recurring patterns where specific emotional states trigger purchasing behaviors that provide short-term relief but undermine long-term financial goals, explaining persistent overspending despite awareness that behavior conflicts with stated priorities.

Present Bias in Savings Behavior

Present bias most dramatically affects savings behavior by making future benefits feel insufficiently compelling to motivate current sacrifice. The bias explains persistent undersaving despite awareness of retirement needs—the psychological impact of reducing current consumption feels more significant than distant benefits of enhanced retirement security. Present bias also drives credit card debt accumulation as immediate consumption desire overwhelms consideration of future interest costs and reduced financial flexibility.

Present bias creates time-inconsistent preferences where individuals sincerely intend to start beneficial financial behaviors “later” but when later arrives, present bias makes current consumption feel more important than saving, perpetuating procrastination indefinitely. This explains why many people delay starting retirement savings, emergency fund building, or debt reduction despite never intending to permanently forgo these goals—each present moment receives psychological privilege over future moments, preventing transition from intention to action.

Risks, Pitfalls, and Failure Scenarios

Psychological influences on financial decisions create predictable risks and failure scenarios where behavioral patterns systematically undermine financial outcomes despite adequate knowledge or resources. These failure scenarios typically involve emotional responses overwhelming rational analysis during critical decision points—market volatility, major purchases, debt management, career transitions—when stakes are highest. Understanding common failure patterns enables proactive implementation of safeguards before emotional or cognitive biases damage financial outcomes irreversibly.

Financial failure scenarios driven by psychological factors share common features: they involve decisions made under emotional arousal or cognitive stress, they reflect systematic biases rather than random errors, they create losses that compound through time or opportunity cost, and they often involve social dynamics that reinforce rather than correct problematic patterns. Recognizing these common elements helps identify personal vulnerability to specific failure scenarios and motivate implementation of behavioral interventions before crisis situations test psychological resilience.

Panic Selling and Emotional Reactions

Panic selling represents a common failure scenario where fear-driven emotional reactions during market volatility trigger premature exit from investment positions, locking in losses and missing subsequent recoveries. This pattern destroys long-term investment returns through poorly-timed selling that realizes paper losses while abandoning positions before market cycles complete. Research demonstrates that investors who maintain positions through market downturns typically achieve superior returns compared to those who sell during declines and re-enter after prices recover, yet panic selling remains widespread during every significant market correction.

Fear triggers reactive selling through neural mechanisms that prioritize immediate threat response over long-term strategic analysis. During market downturns, watching portfolio values decline activates amygdala responses similar to physical threats, creating overwhelming motivation to stop the pain through selling. This emotional intensity makes rational arguments about long-term market cycles feel irrelevant compared to immediate imperative to exit positions. Loss aversion intensifies fear by making losses feel particularly painful, adding psychological urgency to selling before losses grow despite this representing exactly wrong response for long-term investors.

Panic selling leads to locked-in losses by converting temporary market declines into permanent wealth reduction. While maintaining positions through downturns preserves opportunity to benefit from eventual recovery, selling converts paper losses to realized losses with no recovery potential. The common pattern involves selling near market bottoms when fear peaks, sitting in cash through early recovery phases due to continued anxiety, then re-entering markets after significant recovery already occurred. This buy-high-sell-low sequence destroys wealth through behavioral timing that inverts optimal strategy.

The financial damage from panic selling extends beyond direct losses to include opportunity costs from missing recoveries and potential abandonment of beneficial long-term investment strategies. Investors who panic sell often conclude they lack psychological capacity for equity investment, moving permanently to overly conservative allocations that fail to achieve growth needed for long-term goals. This overreaction to emotional experience prevents learning better emotional regulation strategies while preserving appropriate risk exposure, instead solving emotional discomfort through reducing potential returns.

Overconfidence and Excessive Trading

Overconfidence creates financial failure through excessive trading that generates transaction costs exceeding any skill-based returns while increasing tax liabilities and reducing diversification through concentrated positions. Research consistently demonstrates inverse relationship between trading frequency and returns—investors who trade most frequently achieve lowest returns after accounting for costs. This pattern reflects overconfidence leading individuals to believe their analysis provides edge justifying active trading despite statistical evidence that such edge rarely exists outside professional contexts with substantial resource advantages.

Excessive trading driven by overconfidence generates multiple drags on portfolio performance beyond direct transaction costs. Frequent trading triggers short-term capital gains taxed at ordinary income rates rather than preferential long-term rates, reducing after-tax returns. Active trading tends to reduce diversification as overconfident investors concentrate in highest-conviction positions, increasing portfolio volatility and downside risk. High turnover prevents compound growth from fully operating as positions get churned before long-term appreciation potential realizes.

Overconfidence leads to excessive risk-taking through underestimation of downside possibilities and overestimation of ability to predict outcomes or control results. Investors exhibiting overconfidence might use leverage to amplify returns based on conviction that analysis identifies mispricing, generating magnified losses when predictions fail. They might concentrate positions based on confidence that reduces appropriate diversification, creating vulnerability to individual security underperformance. These risk-taking patterns reflect genuine belief in superior ability rather than reckless gambling, making overconfidence particularly dangerous because it feels justified.

Higher transaction costs from frequent trading compound over time to create substantial performance drag that typically overwhelms any benefit from attempted market timing or security selection. A portfolio experiencing 50% annual turnover generating 1% total transaction costs underperforms by that 1% annually compared to buy-and-hold approach before considering tax disadvantages or diversification reduction. Over decades, this seemingly modest annual drag accumulates to dramatically different wealth outcomes through compound effects, demonstrating how behavioral patterns creating small annual differences generate enormous long-term impacts.

Herd Mentality and Market Bubbles

Herd mentality creates individual financial failure through participation in market bubbles where social proof and fear of missing out override fundamental valuation analysis, leading to purchases at inflated prices followed by losses when bubbles burst. The psychological pattern involves increasing conviction that “this time is different” as social proof builds, rationalization of stretched valuations through new paradigm thinking, and reluctance to exit despite warning signs due to continued strong performance and social pressure to maintain participation.

Following crowd behavior leads to suboptimal decisions by encouraging entry at precisely wrong times—when social proof is strongest (during late bubble stages when prices are highest) and when fear is most intense (during crashes when prices are lowest). The herd dynamic creates inverse optimal timing where individuals feel most compelled to buy after major price appreciation and most compelled to sell after significant declines, though optimal strategy involves opposite timing. This behavioral pattern explains how bubbles attract widest participation near peaks just before burst, concentrating losses on late entrants.

Herd behavior manifests in personal finance beyond investing through social comparison driving consumption matching peer groups regardless of personal financial capacity. This social spending pattern explains lifestyle inflation, status-driven purchases, and consumption beyond means to maintain perceived social standing. The psychological mechanism involves using peer spending as reference point for “normal” consumption, creating pressure to match group norms even when doing so strains personal finances. Social media intensifies this dynamic by increasing exposure to peer consumption while hiding financial stress.

The financial failure from herd-driven behavior stems from making decisions based on social proof rather than personal analysis, financial capacity, or fundamental value assessment. An individual buying overpriced assets due to bubble herd behavior suffers losses when prices correct toward fundamental value. Someone overspending to match peer consumption patterns accumulates debt or sacrifices savings while others in the group might have resources making their spending sustainable. These failures share root cause of allowing social dynamics to override personal financial analysis and capacity assessment.

Mental Accounting and Present Bias

Mental accounting creates financial inefficiency when rigid category-based rules prevent optimal resource allocation across artificial boundaries. The most common costly example involves maintaining low-return savings while carrying high-interest debt—mental accounting makes these feel like separate decisions governed by different rules (emergency savings must be preserved, debt must be paid down gradually) despite combined impact creating wealth destruction through negative arbitrage. This pattern persists even when individuals intellectually recognize the inefficiency because psychological separation feels necessary for maintaining savings discipline.

Mental accounting can lead to misallocation of funds when category labels prevent fungibility recognition and optimal deployment across financial goals. An individual might maintain separate accounts for different purposes—emergency fund, vacation savings, retirement investing—while applying different investment strategies or tolerance for depletion to each account despite money having equivalent economic value regardless of label. This compartmentalization helps some people maintain discipline but can prevent beneficial reallocation when one goal becomes more important or one category significantly underperforms others.

Present bias causes retirement underfunding through systematic prioritization of current consumption over future security despite intellectual awareness of retirement needs. The bias makes reducing current consumption feel psychologically painful while distant retirement benefits feel insufficiently compelling to motivate current sacrifice. This creates time-consistent preference for starting retirement savings “next year” while maintaining current spending, perpetuating procrastination indefinitely through repeated present bias at each future decision point. The financial cost compounds dramatically as delayed start dates sacrifice decades of potential compound growth.

Mental accounting and present bias often interact to reinforce financially detrimental patterns. Present bias makes current spending more appealing than saving, while mental accounting creates rigid categories that prevent reallocation even when clearly beneficial. For example, present bias might cause someone to spend “bonus money” immediately while present bias combined with mental accounting prevents considering that money for retirement savings that would generate long-term wealth growth. These biases operating together create behavioral patterns particularly resistant to change through education alone, requiring structural interventions that work with rather than against psychological realities.

How to Make Better Financial Decisions Despite Psychological Biases

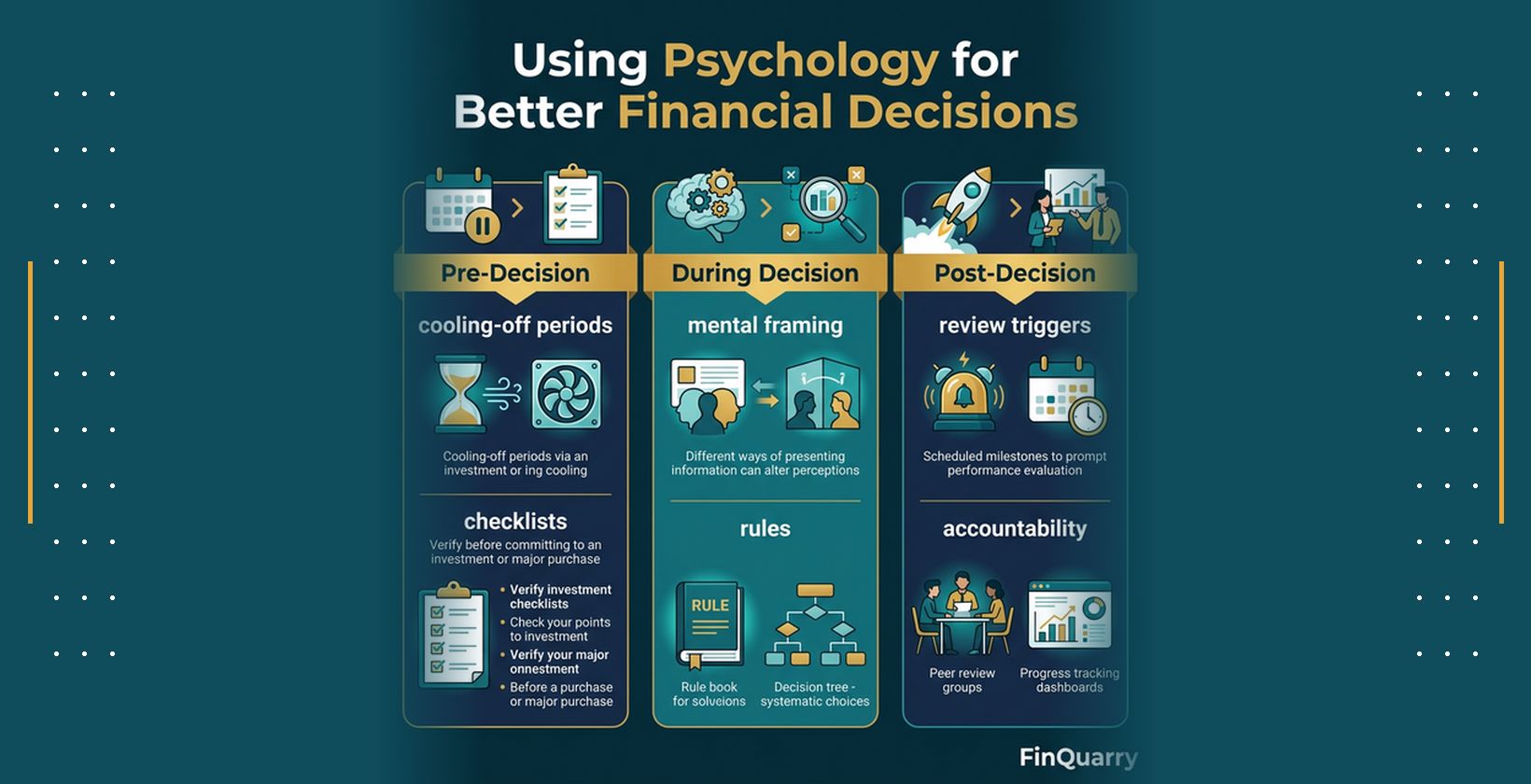

Making better financial decisions despite psychological biases requires implementing decision frameworks and behavioral interventions that acknowledge cognitive limitations and emotional influences rather than assuming these can be eliminated through awareness alone. Effective strategies work with human psychology by automating beneficial behaviors, creating commitment devices that prevent future reversal of current intentions, and designing choice architectures that make desired behaviors easier while creating friction for problematic patterns. These approaches recognize that knowing about biases rarely suffices to prevent their influence during emotionally charged decision moments.

Improvement strategies focus on changing decision environments and processes rather than attempting to change fundamental psychology. Eliminating biases proves impossible—these represent how human brains naturally function given evolutionary heritage and cognitive architecture. Sustainable improvement comes from designing around biases through automated systems, pre-commitment devices, decision rules applied before emotional involvement peaks, and external accountability mechanisms that operate when psychological self-control fails. This systems-based approach proves more effective than willpower-dependent strategies that require constant active bias resistance.

Awareness-Based Controls

Awareness-based controls involve recognizing personal bias patterns, understanding situations where they likely operate, and implementing monitoring systems that highlight when emotional or cognitive influences may be distorting decisions. While awareness alone rarely prevents biases, it enables recognition of high-risk situations where additional safeguards become necessary. Effective awareness-based approaches combine self-monitoring with external checks rather than relying solely on internal recognition during decision moments when biases operate most powerfully.

Identifying personal bias patterns requires systematic reflection on past financial decisions, recognizing situations that consistently preceded suboptimal choices, and understanding emotional or cognitive tendencies that created vulnerability. Keeping a decision journal noting the reasoning and emotional state behind major financial choices helps identify patterns over time. For investment decisions, tracking rationale for purchases and sales alongside subsequent outcomes reveals systematic biases—holding losers too long suggests disposition effect, frequent trading indicates overconfidence, buying recent strong performers suggests trend-chasing and herd behavior.

Separating emotion from action timing represents critical awareness-based control that improves decision quality despite continued emotional responses to financial events. This approach acknowledges that eliminating emotional reactions proves impossible but creates distance between emotional activation and behavioral response. When experiencing strong emotions around financial decisions—fear during market volatility, excitement about investment opportunity, anxiety about spending—implement mandatory waiting periods before acting. A simple rule like “no investment decisions within 24 hours of major market moves” prevents fear or greed–driven reactive choices while allowing time for emotional intensity to subside.

Personal bias awareness develops through examining recurring patterns in financial behavior that produce regret or suboptimal outcomes. Someone who regularly overspends during stress might recognize emotional spending as personal vulnerability requiring management. An investor who panic sold during past market downturns might identify fear-driven selling as bias needing preventive measures. Recognizing these patterns enables proactive safeguards—the emotional spender might remove saved payment information from shopping apps, the panic seller might establish rules preventing position reduction during high-volatility periods without advisor consultation.

Structural Decision Tools

Structural decision tools create frameworks and systems that reduce reliance on moment-to-moment willpower or rational analysis by establishing rules, defaults, and automated processes that operate regardless of psychological state. These tools prove particularly effective because they function during exactly the conditions where biases most powerfully influence behavior—emotional arousal, cognitive overload, time pressure. By pre-committing to beneficial behaviors during calm rational periods, structural tools enable maintaining those behaviors during future emotional periods when maintaining them through willpower alone would likely fail.

Rules-based decisions involve establishing clear criteria for specific financial choices in advance, then applying those rules mechanically regardless of emotional state or market conditions when decision moments arrive. Investment rebalancing rules might specify selling portions of asset classes exceeding target allocation by specific percentages, removing emotional decision-making from the process. Spending rules might establish maximum amounts for discretionary categories or mandatory waiting periods before purchases exceeding thresholds, preventing impulse buying while preserving deliberate purchasing freedom.

Pre-commitment strategies leverage current rational intentions to constrain future behavior that might deviate due to psychological influences. These strategies recognize that individuals often intend beneficial behaviors during calm periods but fail to maintain intentions during emotional or challenging moments when biases activate. Automatic investment contributions represent effective pre-commitment—during rational periods, individuals authorize automatic deductions, then these continue during future periods when present bias or market fear might otherwise prevent saving or investing.