Table of Contents

Contents are generated from article headings.

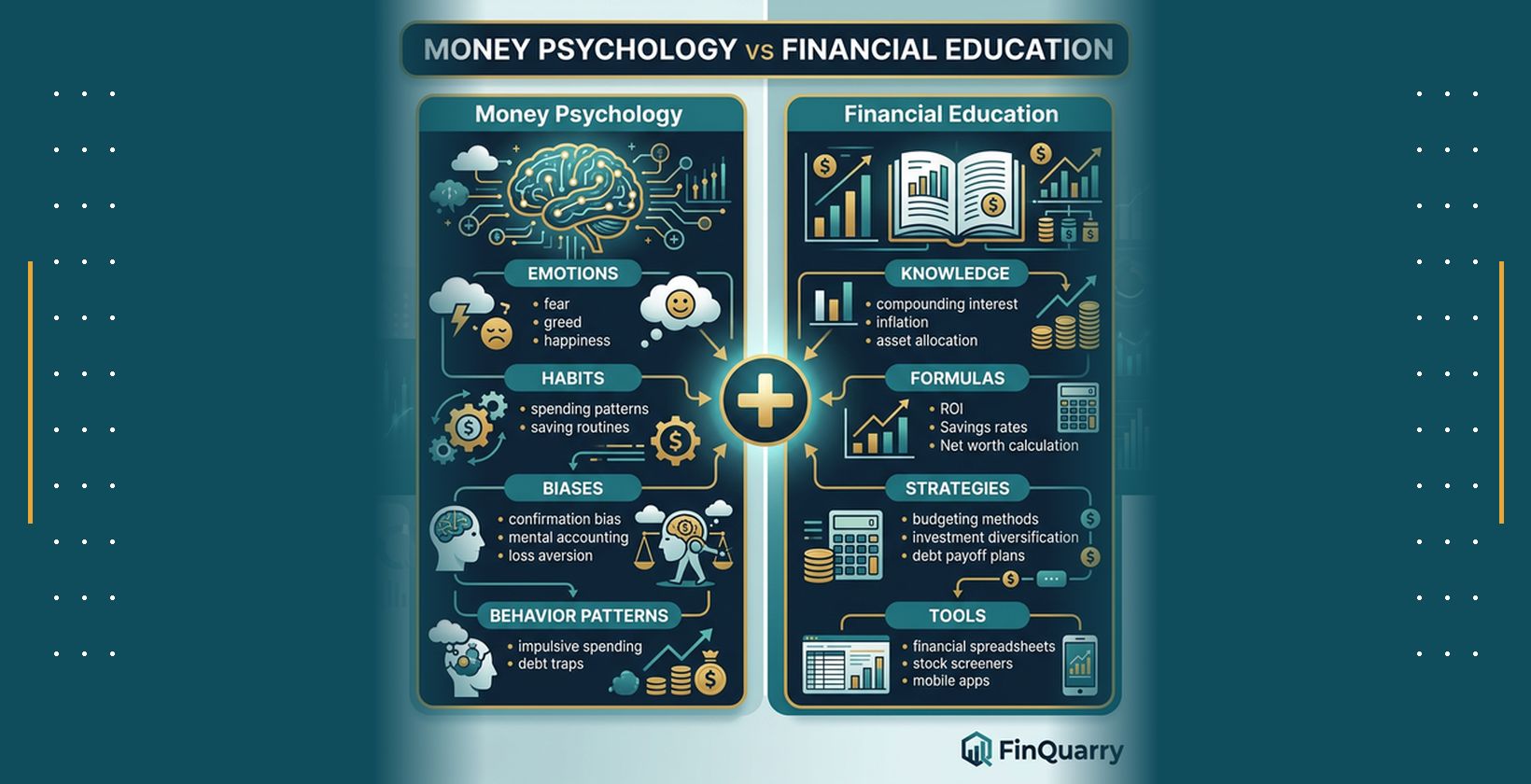

Money psychology refers to the study of how psychological factors—including emotions, cognitive biases, personality traits, and mental models—influence financial decisions and behaviors. Unlike financial literacy, which focuses on knowledge of financial concepts, money psychology examines why people make specific money choices even when they understand the logical alternatives. This field operates at the intersection of behavioral finance and psychology, explaining patterns in spending, saving, investing, and risk tolerance that traditional financial education alone cannot address.

Money psychology differs from money mindset in scope and application. Money mindset typically refers to personal beliefs and attitudes about wealth and abundance, often framed around positive thinking or self-improvement. Money psychology, in contrast, is grounded in behavioral finance research and examines measurable psychological mechanisms such as loss aversion, anchoring bias, and emotional regulation. While financial literacy teaches what to do with money, money psychology explains why people often fail to follow through on what they know.

The focus of money psychology is on behavior rather than income level. Research in behavioral finance demonstrates that psychological patterns affect financial outcomes across all income brackets. High earners can struggle with impulsive spending or poor investment timing just as lower earners might, because the underlying psychological drivers—fear, status-seeking, emotional avoidance—operate independently of wealth. Understanding money psychology helps individuals recognize their own behavioral patterns and make more intentional financial choices aligned with long-term goals.

Money psychology examines how thoughts, emotions, and habits influence financial decisions in measurable ways. Emotional states such as anxiety, excitement, or regret can trigger specific spending or saving behaviors. Cognitive biases like confirmation bias or recency bias distort how individuals evaluate financial risks and opportunities. Habitual patterns formed over years—often rooted in childhood experiences—create automatic responses to money situations that bypass rational analysis. These psychological factors collectively determine financial outcomes more powerfully than mathematical knowledge alone.

Readers will gain practical insights into emotional spending triggers, saving psychology, investing behavior, and long-term financial health. This article explains how money psychology shapes daily financial choices, why financial strategies often fail without behavioral alignment, and how self-awareness of psychological patterns can improve financial outcomes. The content covers cognitive biases that affect money decisions, childhood influences on adult financial behavior, personality-based money patterns, and actionable techniques for improving money psychology over time.

How Money Psychology Explains Financial Behavior Patterns

Money psychology explains why people with similar incomes behave differently with money by examining the psychological variables that shape financial decisions. Two individuals earning identical salaries can have vastly different financial outcomes based on their emotional responses to money, cognitive biases, risk tolerance, and learned behaviors. One person might prioritize long-term savings and delayed gratification, while another focuses on immediate consumption and present enjoyment. These differences stem from psychological factors rather than financial knowledge or income capacity.

Emotions play a central role in financial behavior patterns, often overriding logical analysis. Fear can drive excessive saving or avoidance of necessary financial decisions. Greed can lead to high-risk investments or speculative behavior beyond reasonable risk tolerance. Regret about past financial mistakes can cause decision paralysis or reactive overcorrection. Overconfidence can result in insufficient diversification or neglect of expert guidance. These emotional drivers create consistent behavioral patterns that determine long-term financial trajectories.

Cognitive biases and mental shortcuts systematically influence how individuals process financial information and make money choices. The human brain relies on heuristics—quick decision rules—to manage the overwhelming complexity of daily financial choices. While these mental shortcuts increase decision speed, they often introduce predictable errors. Understanding these biases helps explain why smart, educated individuals sometimes make poor financial choices despite having access to accurate information and resources.

Money psychology connects directly to spending, saving, investing, and risk-taking behaviors through observable cause-and-effect mechanisms. Spending behavior reflects emotional regulation patterns and reward-seeking tendencies. Saving behavior correlates with anxiety levels, future orientation, and perceived financial security. Investing behavior reveals risk tolerance, overconfidence levels, and susceptibility to social proof. Risk-taking patterns demonstrate how loss aversion and regret avoidance shape portfolio construction and asset allocation decisions.

Behavioral finance provides the academic framework for understanding money psychology without requiring technical expertise. This field emerged from the recognition that traditional economic models assuming perfect rationality fail to explain real-world financial behavior. Behavioral finance incorporates psychological research on decision-making, emotion, and bias into financial analysis. Key concepts include loss aversion (the tendency to feel losses more intensely than equivalent gains), mental accounting (treating money differently based on its source or intended use), and herd behavior (following crowd decisions during market volatility).

Why Rational Financial Decisions Rarely Happen in Real Life

Rational financial decisions rarely happen in real life because humans process money choices through emotional and psychological filters rather than pure logic. The brain’s emotional centers activate before analytical reasoning when evaluating financial decisions, particularly those involving uncertainty or potential loss. This neurological sequence means emotional responses often determine initial reactions to money situations, with rational justification constructed afterward to support emotionally-driven choices.

Emotional drivers such as fear, greed, regret, and overconfidence consistently influence financial behavior in predictable patterns. Fear triggers risk-averse responses that can lead to missed investment opportunities or excessive cash holdings that fail to keep pace with inflation. This emotion intensifies during market downturns, often causing panic selling at exactly the wrong time. Greed drives speculative behavior and concentration in high-performing assets, increasing portfolio risk beyond appropriate levels for individual circumstances.

Regret about past financial mistakes creates decision paralysis or reactive overcorrection that compounds problems. Individuals who experienced losses in previous investments might avoid equity markets entirely, missing long-term growth opportunities. Alternatively, they might chase past winners in an attempt to recover losses, leading to poorly-timed entries at market peaks. Overconfidence causes individuals to overestimate their financial knowledge, ignore expert guidance, or take excessive risks based on limited information or recent success.

Impulse spending demonstrates how emotional states override long-term planning in everyday financial behavior. Stress, boredom, sadness, or excitement can trigger unplanned purchases that provide immediate emotional relief but conflict with stated financial goals. Retailers and marketers design purchasing environments to exploit these emotional vulnerabilities through limited-time offers, scarcity messaging, and social proof. The gap between what individuals plan to spend and actual spending behavior reflects the power of emotional triggers over rational budgeting.

Long-term financial planning requires sustained discipline and delayed gratification, both of which conflict with the brain’s preference for immediate rewards. Behavioral research demonstrates that humans systematically discount future benefits in favor of present consumption, a pattern called hyperbolic discounting. This bias explains why individuals struggle to save for retirement decades away while readily spending on immediate pleasures. The emotional satisfaction of current consumption feels more compelling than abstract future security, even when individuals intellectually understand the importance of long-term planning.

How Cognitive Biases Shape Everyday Money Choices

Cognitive biases shape everyday money choices by creating systematic errors in how individuals evaluate financial information and make decisions. These mental shortcuts operate automatically and unconsciously, influencing behavior even when people are aware of the biases intellectually. Recognizing specific biases helps explain patterns in spending, investing, debt management, and financial planning that seem irrational from a purely mathematical perspective.

Anchoring bias causes individuals to rely heavily on the first piece of information encountered when making financial decisions, even when that information is irrelevant or misleading. In retail settings, original prices serve as anchors that make discounted prices appear more attractive, regardless of actual value. During salary negotiations, the first number mentioned often anchors the entire discussion, affecting final outcomes. In investing, purchase prices create psychological anchors that influence hold-or-sell decisions, even when current fundamentals suggest different actions.

Loss aversion—the tendency to feel losses approximately twice as intensely as equivalent gains—profoundly affects investment behavior and risk tolerance. This bias causes individuals to hold losing investments too long in hopes of breaking even, while selling winning investments too quickly to “lock in” gains. Loss aversion explains why market downturns trigger panic selling despite logical arguments for staying invested. The psychological pain of realized losses overrides rational analysis of long-term investment strategy and market cycles.

Confirmation bias leads individuals to seek, interpret, and remember information that confirms existing beliefs while dismissing contradictory evidence. Investors exhibiting confirmation bias selectively focus on news supporting their investment thesis while ignoring warning signs or alternative viewpoints. This bias reinforces poor financial decisions by creating echo chambers of self-confirming information. In spending behavior, confirmation bias helps rationalize unnecessary purchases by emphasizing reasons to buy while minimizing financial constraints or alternative uses of funds.

Mental shortcuts, or heuristics, simplify complex financial decisions but introduce predictable errors in judgment. The availability heuristic causes people to overweight recent or vivid information when assessing risks and opportunities. After hearing about a friend’s investment success, individuals might overestimate their own chances of similar outcomes. The representativeness heuristic leads to assuming that recent market patterns will continue, contributing to trend-chasing behavior and poorly-timed market entries or exits.

Real-life scenarios demonstrate how cognitive biases affect spending and investing across common situations. During sales events, anchoring bias makes discounts appear larger than actual savings, driving purchases of items not originally needed. Stock market hype around specific sectors or companies triggers herd behavior and confirmation bias, creating bubbles when investors pile into overvalued assets. Debt management suffers from present bias, where immediate gratification from purchases outweighs the delayed pain of interest payments and reduced financial flexibility.

Emotional Triggers That Drive Spending and Saving Habits

Emotional triggers drive spending and saving habits through psychological associations between money behaviors and emotional states. Stress spending occurs when individuals use purchases as coping mechanisms for anxiety, frustration, or overwhelm. The temporary relief from acquiring new items or experiences creates a reinforcement loop, even when spending conflicts with financial goals or creates additional stress through debt accumulation or budget depletion.

Comfort buying represents spending behavior motivated by emotional needs for security, belonging, or self-worth rather than practical necessity. Individuals might purchase specific brands or products associated with positive childhood memories, social status, or identity reinforcement. This emotional association with consumption makes spending feel like self-care or identity expression, blurring the line between genuine needs and emotionally-driven wants.

Fear-based saving demonstrates how anxiety about future uncertainty can drive excessive saving behavior that reduces current quality of life. While prudent emergency savings improve financial security, fear-driven hoarding can prevent individuals from enjoying present experiences or investing in opportunities with acceptable risk-return profiles. This pattern often originates from childhood experiences of financial instability or messages equating spending with irresponsibility.

Emotional associations with money fall into three primary categories: reward, safety, and status. Money as reward creates spending patterns tied to achievement, celebration, or self-gifting after accomplishments or difficult periods. This association can lead to lifestyle inflation where income increases automatically translate to increased spending rather than saving or investing. Money as safety drives conservative financial behavior focused on accumulation, risk avoidance, and security-seeking, sometimes to the detriment of growth opportunities or present enjoyment.

Money as status fuels spending on visible consumption that signals social position or success to others. This emotional driver explains purchases of luxury goods, premium brands, or experiences primarily valued for their signaling function rather than intrinsic utility. Status-driven spending often operates unconsciously, influenced by social comparison and perceived expectations from peer groups. The emotional reward from status signaling can override logical analysis of financial sustainability or alignment with deeper values.

Why Money Psychology Matters for Financial Success

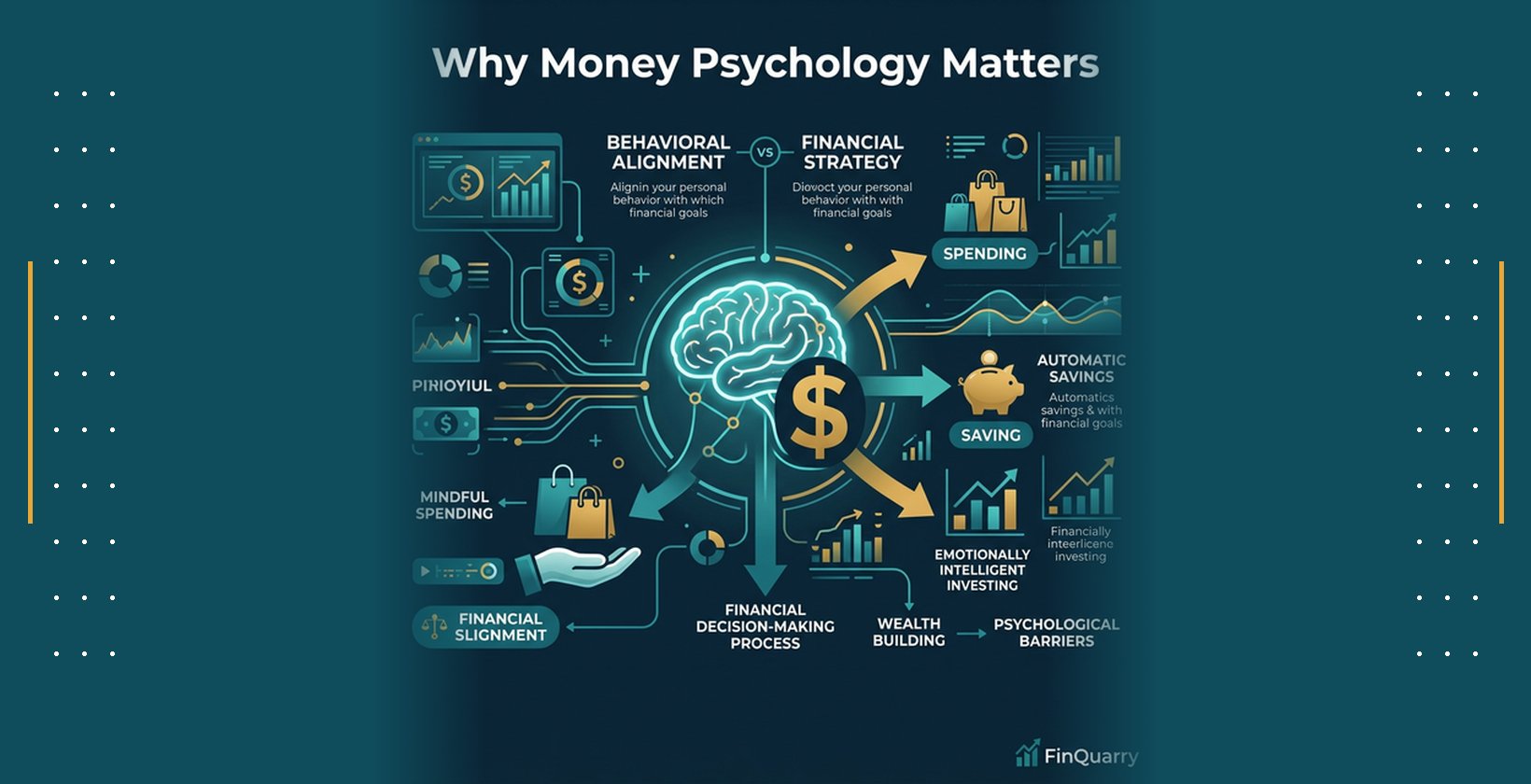

Money psychology matters for financial success because financial strategies fail without behavioral alignment, regardless of how mathematically sound the plans appear. Traditional financial planning focuses on optimization—ideal savings rates, asset allocation models, tax efficiency strategies—but consistently underestimates the role of psychology in execution. Individuals who understand optimal financial strategies but cannot maintain behavioral consistency see worse outcomes than those with simpler strategies executed reliably over time.

Long-term wealth depends on consistency and emotional understanding more than superior financial knowledge or market timing ability. Behavioral finance research demonstrates that maintaining a moderately effective investment strategy through complete market cycles outperforms sophisticated strategies abandoned during market volatility. The ability to continue systematic savings during income fluctuations, resist panic selling during downturns, and avoid speculative bubbles requires psychological stability and self-awareness that transcends technical financial knowledge.

Psychology impacts financial goal achievement through its influence on daily micro-decisions that compound over time. Grand financial goals—retirement security, home ownership, financial independence—require thousands of small decisions aligned with those objectives. Each spending choice, savings contribution, and investment decision either moves individuals toward or away from stated goals. Money psychology determines the consistency of these daily decisions by shaping how individuals respond to emotional triggers, cognitive biases, and situational pressures that test commitment to long-term plans.

Financial success requires sustainable behavior patterns rather than perfect decisions or optimal strategies. Individuals with realistic self-knowledge about their psychological tendencies can design financial systems that work with their psychology rather than against it. Someone aware of their impulsive spending tendencies might automate savings before funds reach checking accounts. Someone prone to analysis paralysis might simplify investment choices to low-cost index funds rather than attempting to construct optimal portfolios they never implement.

The gap between financial knowledge and financial behavior—knowing what to do versus actually doing it—explains why educated professionals often struggle financially while individuals with less formal education sometimes achieve greater financial security. Knowledge creates necessary awareness, but psychology determines action. Understanding money psychology helps close this gap by addressing the emotional, habitual, and cognitive factors that govern actual financial behavior in real-world conditions with competing priorities and limited willpower.

How Money Psychology Impacts Budgeting and Saving Consistency

Money psychology impacts budgeting and saving consistency by revealing why budgets fail emotionally rather than mathematically. Most budget failures occur not because individuals lack arithmetic skills or understanding of income versus expenses, but because budgets conflict with psychological needs, identity, or behavioral patterns. A mathematically perfect budget that requires constant willpower and deprivation typically fails within weeks, while a psychologically sustainable budget with modest targets often succeeds long-term.

Discipline-based budgeting relies on willpower to override emotional spending impulses and maintain spending limits through conscious effort. This approach works temporarily but depletes limited self-control resources, leading to eventual breakdown when willpower weakens under stress, fatigue, or competing demands. Identity-based budgeting, in contrast, aligns spending with self-image and values, reducing the need for constant vigilance. When individuals see themselves as “someone who values financial security” or “a person who invests in experiences over things,” spending decisions align with identity rather than requiring constant discipline.

Habit loops in saving and spending operate through cue-routine-reward patterns that function automatically without conscious deliberation. Saving becomes easier when structured as habitual responses to specific cues—automatic transfers on payday, rounding up purchases to savings accounts, or allocating windfalls to predetermined categories. Spending habits similarly follow cue-routine-reward patterns, where specific emotional states or environmental triggers activate purchasing behaviors that provide temporary emotional relief or satisfaction.

Budgeting serves as a psychological tool for emotional clarity, control, and predictability as much as a financial planning mechanism. The act of categorizing expenses and setting limits reduces financial anxiety by creating a clear picture of money flow and remaining resources. This psychological benefit explains why some individuals feel less stressed after creating budgets even before changing spending behavior—the clarity itself reduces uncertainty and provides a sense of control over financial circumstances.

Saving consistency depends more on automated systems and behavioral architecture than conscious commitment. Individuals who automate savings through payroll deduction or automatic transfers maintain higher savings rates with less effort than those relying on manual transfers requiring repeated decisions. The psychological principle underlying this pattern is decision fatigue—each financial choice depletes limited mental resources, making automation superior to willpower for long-term consistency.

How Money Psychology Influences Investing Decisions and Risk Tolerance

Money psychology influences investing decisions through emotional responses to market volatility that override rational analysis of long-term fundamentals. Panic selling during market downturns represents fear-driven behavior where the psychological pain of watching portfolio values decline triggers selling at exactly the wrong time—after prices have fallen. This pattern repeats across market cycles because the emotional intensity of losses activates flight responses in the brain’s threat-detection systems, overriding logical understanding that market fluctuations are normal.

FOMO (fear of missing out) investing demonstrates how social proof and regret aversion drive speculative behavior during market rallies. When individuals hear repeated stories of others profiting from specific investments, the psychological pain of missing potential gains overwhelms analysis of fundamental value or risk. This emotional driver explains buying behavior near market peaks when valuations are stretched but social proof is strongest, followed by losses when momentum reverses.

Risk perception versus actual risk often diverge significantly based on psychological factors rather than objective assessment. Recent experiences disproportionately influence risk perception through availability bias—investors who lived through significant market downturns often perceive equity risk as higher than historical data suggests, while those who experienced only rising markets underestimate downside risk. Personal risk tolerance also reflects anxiety levels, need for control, and financial security feelings more than statistical risk capacity based on time horizon and financial resources.

Emotional cycles during bull and bear markets create predictable behavioral patterns that reduce investment returns. During bull markets, rising portfolio values trigger overconfidence and increased risk-taking, often leading to concentrated positions, reduced diversification, or leverage use. As markets peak, euphoria and social proof drive maximum risk exposure. During bear markets, fear and regret trigger the opposite response—selling equities, fleeing to cash, and remaining on the sidelines during recovery phases when the best long-term buying opportunities appear.

Investment psychology explains why the typical investor underperforms the market indices they could easily access through low-cost index funds. This “behavior gap” results from emotional buying and selling at suboptimal times, chasing recent performance, and abandoning investment strategies during periods of underperformance. Market timing attempts driven by fear and greed consistently reduce returns compared to staying invested through complete market cycles, despite the psychological difficulty of maintaining positions during downturns.

Money Psychology and Financial Stress, Anxiety, and Guilt

Money psychology directly impacts mental well-being through the bidirectional relationship between financial stress and psychological health. Financial anxiety can trigger avoidance behaviors where individuals stop checking account balances, ignore bills, or delay important financial decisions, creating a negative feedback loop that worsens financial circumstances. This avoidance provides temporary emotional relief from anxiety but compounds financial problems, increasing long-term stress and reducing financial outcomes.

Money-related guilt often stems from misalignment between spending behavior and stated values or goals. Individuals who spend impulsively might experience persistent guilt that erodes self-esteem and financial confidence without translating into behavior change. This guilt can become paralyzing, creating shame cycles that prevent constructive problem-solving or seeking help. Understanding the psychological roots of guilt—often tied to childhood money messages or social comparison—helps individuals address underlying issues rather than suppressing uncomfortable emotions.

Shame around money differs from guilt in focusing on self-worth rather than specific behaviors. While guilt says “I made a bad financial decision,” shame says “I am bad with money.” This distinction matters because shame damages identity and self-efficacy, making positive change feel impossible. Financial shame often leads to secrecy, isolation, and resistance to seeking expert guidance, prolonging financial difficulties and preventing learning from mistakes.

Financial anxiety manifests in both excessive worry and avoidance, depending on individual psychology. Some individuals obsessively check accounts, constantly analyze spending, and struggle to enjoy present experiences due to future financial fears. Others avoid all financial information, allowing problems to accumulate unchecked. Both patterns reflect underlying anxiety about financial security and control, though they express through opposite behaviors. Effective approaches address the anxiety itself rather than only the surface behaviors.

The psychological impact of financial stress extends beyond direct money concerns to affect overall life satisfaction, relationship quality, and physical health. Chronic financial stress correlates with sleep problems, anxiety disorders, depression, and relationship conflict. Money conflicts rank among the top predictors of relationship dissolution, not because of actual resource scarcity but due to psychological differences in money values, communication patterns, and unresolved financial fears or traumas.

How Childhood Experiences Shape Your Money Psychology

Childhood experiences shape money psychology through a process called financial imprinting, where early observations and experiences create default patterns that operate automatically in adulthood. These learned behaviors function largely unconsciously, influencing financial decisions without deliberate thought. Individuals often replicate parental money patterns or react against them through opposite extremes, rarely developing independent money relationships without conscious examination of early influences.

Financial imprinting operates through observational learning rather than explicit instruction. Children absorb parental attitudes toward spending, saving, risk, and money discussions by observing emotional responses, overhearing conversations, and experiencing family financial dynamics. A child who witnesses parental stress about bills learns to associate money with anxiety. A child who observes generous giving learns money can create positive impact. These associations become neural patterns that activate automatically when encountering similar situations in adulthood.

The distinction between learned behaviors and conscious choices becomes clear when examining money decisions that conflict with stated values or goals. An individual might intellectually value saving but find themselves unable to maintain consistent savings behavior because early learning associated spending with love, reward, or temporary stress relief. Without awareness of these learned patterns, change efforts focus on willpower rather than addressing underlying psychological associations that drive behavior.

Self-awareness of early experiences is essential for developing healthier money psychology because unconscious patterns cannot be changed. By examining childhood money memories, family financial dynamics, and emotional associations with money formed early, individuals can identify which current behaviors represent genuine preferences versus unexamined learned patterns. This awareness creates choice—the ability to maintain helpful inherited patterns while consciously changing those that no longer serve adult financial goals and values.

Childhood money experiences vary widely even within similar economic circumstances, demonstrating that subjective interpretation matters more than objective financial situation. Two children growing up in identical households might develop opposite money psychology based on their unique interpretations of family dynamics, their position in birth order, parental attention patterns, or specific memorable events. This variability explains why siblings often exhibit dramatically different adult money behaviors despite shared upbringing.

How Parents’ Money Habits Influence Adult Financial Behavior

Parents’ money habits influence adult financial behavior through observational learning that operates more powerfully than explicit financial instruction. Children develop money patterns by watching how parents handle financial decisions, emotional responses to money, spending versus saving priorities, and financial stress management. These observations create behavioral templates that feel normal and correct, even when objectively dysfunctional, because early learning establishes baseline expectations for how money “should” work.

Saver versus spender households create distinct behavioral imprints that often persist into adulthood. Children raised in saver households might develop strong saving habits and frugality that serve them well financially but potentially limit present enjoyment or create anxiety around any spending. Those from spender households might struggle with delayed gratification and savings consistency but feel more comfortable enjoying money and present experiences. Neither pattern is inherently superior; awareness allows individuals to balance inherited tendencies.

Family conflict around money teaches children that money discussions are dangerous, shameful, or avoided. In households where parents fought about finances, children often develop anxiety around money conversations and avoid financial planning or communication with partners. Conversely, families that discussed money openly and collaboratively teach children that financial issues can be addressed constructively, leading to better financial communication and problem-solving skills in adult relationships.

Transparency versus secrecy in family finances shapes adult comfort with seeking help, discussing money, and managing financial complexity. When parents treat money as taboo or shameful, children internalize that money problems must be hidden and handled alone. This pattern contributes to financial isolation, delayed problem-solving, and resistance to seeking expert guidance when needed. Families that normalized money discussions as practical life skills create adults more comfortable with financial planning and collaborative money management.

Parental money trauma—experiences of significant financial loss, poverty, or instability—can transmit across generations through heightened emotional responses to money situations. A parent who experienced Depression-era scarcity might overemphasize saving and undervalue present enjoyment, passing excessive financial anxiety to children despite current financial security. Understanding these intergenerational patterns helps adults recognize which fears reflect current reality versus inherited trauma from parental experiences.

How Scarcity and Abundance Mindsets Are Formed Early

Scarcity and abundance mindsets form early through childhood experiences of resource availability and parental messaging about sufficiency. Growing up with “not enough” creates neural associations between money and survival threat, activating stress responses around financial decisions that persist into adulthood even when objective circumstances improve. This scarcity mindset tends to manifest as excessive risk aversion, hoarding behavior, difficulty spending on present needs, and persistent financial anxiety regardless of actual resource levels.

Scarcity mindset affects decision-making quality by narrowing focus to immediate financial threats while reducing capacity for long-term planning. When the brain perceives scarcity, it enters a state of heightened alertness to immediate risks that can improve short-term problem-solving but reduces bandwidth for considering future implications or creative solutions. This psychological state helps explain why financial stress often perpetuates itself—the anxiety created by financial pressure reduces the mental capacity needed for effective financial planning and decision-making.

Abundance mindset, formed through consistent experiences of “always enough,” creates different behavioral patterns around risk-taking, spending, and security needs. Individuals raised with abundance generally feel more comfortable with calculated risks, trust that resources will be available when needed, and approach money from a growth orientation rather than protection focus. However, extreme abundance during childhood can create entitlement, poor spending discipline, or difficulty understanding consequences of financial decisions without built-in accountability.

The effects of scarcity versus abundance mindsets on long-term financial behavior extend beyond obvious patterns. Scarcity mindset might drive high achievement and wealth accumulation but prevent enjoyment of accumulated resources or create perpetual feelings of inadequacy despite objective success. Abundance mindset can support entrepreneurial risk-taking and creative problem-solving but potentially underestimate financial risks or fail to develop necessary discipline for sustainable wealth building.

Security-seeking versus opportunity-seeking financial behavior often traces to early scarcity or abundance experiences. Those with scarcity backgrounds tend to prioritize financial security, stable employment, and risk minimization, which can limit income growth potential or investment returns. Those with abundance backgrounds might prioritize growth opportunities, career satisfaction, and risk-taking, which can accelerate wealth building but increase vulnerability to financial setbacks without adequate safety margins.

Can You Change Money Beliefs Formed in Childhood?

Money beliefs formed in childhood can change through neuroplasticity—the brain’s ability to form new neural pathways and modify existing ones throughout life. While early financial imprinting creates strong default patterns, these are not permanent. Change requires awareness of existing patterns, intentional practice of new behaviors, and patience as new neural pathways strengthen through repetition. Research in neuroscience demonstrates that behavioral patterns can be modified at any age, though change requires more conscious effort than maintaining established patterns.

The change process follows a three-stage pattern: awareness, reframing, and new behaviors. Awareness involves identifying current money patterns, their childhood origins, and how they affect present financial decisions. Without this recognition, change attempts focus on surface behaviors without addressing underlying psychological drivers. Reframing challenges inherited beliefs by examining whether they serve current circumstances and values, questioning automatic assumptions, and developing alternative interpretations of money and financial security.

New behaviors require consistent practice to override established neural pathways and create new automatic responses. Initially, changed behaviors feel uncomfortable or “wrong” because they conflict with deeply ingrained patterns that feel normal. This discomfort leads many people to abandon change attempts, interpreting discomfort as evidence they’re doing something inappropriate rather than recognizing it as natural during the transition from old to new patterns. Sustained practice through this discomfort phase is necessary for new behaviors to feel natural.

Practical mindset shift exercises include money autobiography writing to identify formative experiences, values clarification to distinguish inherited versus chosen beliefs, and behavioral experiments to test alternative approaches. Keeping a spending journal that tracks emotional states and triggers helps build awareness of psychological patterns. Gradually increasing spending in feared areas or implementing systematic savings helps those addressing opposite extremes. Working with financial therapists or counselors trained in money psychology can accelerate change by providing expert guidance and accountability.

Changing money beliefs does not require rejecting all childhood influences—many inherited patterns serve individuals well. The goal is conscious choice about which patterns to maintain and which to modify. An individual might keep inherited frugality in some spending categories while relaxing it in areas aligned with current values. Someone might maintain inherited risk tolerance while adding more systematic planning. Selective modification based on self-awareness creates money psychology aligned with adult circumstances and goals.

Money Personality Types Explained Through Psychology

Money personality types provide frameworks for understanding individual differences in financial behavior, though no type is inherently superior or inferior. These categorizations help build self-awareness by identifying characteristic patterns in spending, saving, risk tolerance, and financial decision-making. Understanding personality-based tendencies allows individuals to design financial systems that work with their natural inclinations rather than requiring constant resistance to ingrained patterns.

Categorization helps self-awareness by naming and normalizing the diversity in money approaches. Recognizing that different personalities experience money differently reduces shame around financial tendencies that conflict with perceived norms. A natural spender is not morally inferior to a natural saver—they simply weight present enjoyment versus future security differently based on personality, values, and learned patterns. This recognition allows for self-acceptance while still pursuing beneficial changes.

Avoiding extremes and balancing behaviors represents the practical application of personality awareness. Pure money personality types rarely exist—most individuals exhibit blended patterns or context-dependent behaviors. The goal is not to change fundamental personality but to recognize where natural tendencies become problematic and develop counterbalancing strategies. A spender might maintain enjoyment focus while implementing systems that ensure adequate savings. A saver might keep security priority while building capacity for present enjoyment that enhances life quality.

Money personality frameworks serve as starting points for self-examination rather than rigid categories. Individuals might recognize aspects of multiple personality types or notice their dominant type shifts across life stages as circumstances and priorities change. The value lies in the self-reflection these frameworks prompt rather than perfectly fitting into predefined boxes. By examining emotional responses to different financial situations, individuals gain insight into their psychological drivers and can make more intentional financial choices.

Different money personality frameworks emphasize different dimensions—risk tolerance, spending versus saving orientation, control versus freedom preferences, emotional versus analytical decision-making. Exploring multiple frameworks often provides richer self-understanding than relying on a single categorization. The common thread across frameworks is recognizing that psychological differences in money approach are normal, predictable, and manageable through appropriate strategies tailored to individual psychology.

Spender vs Saver Psychology: Strengths, Risks, and Balance

Spender psychology reflects personality and value patterns that prioritize present experiences, immediate gratification, and enjoyment over future accumulation. Spenders find satisfaction in using money for current needs and desires, value experiences and possessions that enhance present quality of life, and often exhibit generosity toward others. The emotional reward from spending provides immediate positive feedback that reinforces the behavior pattern, making spending feel natural and restraint uncomfortable.

Saver psychology emphasizes security, future preparation, and accumulation over present consumption. Savers derive satisfaction from watching balances grow, feel anxiety when depleting reserves, and value financial cushions that provide security against uncertainty. The emotional reward from saving comes from reduced anxiety and increased sense of control, though this can become problematic when excessive saving prevents enjoying accumulated resources or present experiences that enhance life quality.

The strengths of spender psychology include ability to enjoy life’s moments, flexibility in allocating resources to changing priorities, and often stronger social connections through generosity and shared experiences. Spenders typically exhibit less financial anxiety about present enjoyment and more comfort with calculated financial risks that could improve quality of life. These strengths serve individuals well in creating fulfilling lives, though without balance they can undermine long-term financial security.

The risks of spender psychology include insufficient emergency savings, inadequate retirement preparation, and potential for debt accumulation that reduces future financial freedom. Spenders might struggle during income disruptions, face financial stress in later life stages, or experience relationship conflict with partners who have saver psychology. The challenge for spenders involves maintaining their enjoyment orientation while implementing systems that ensure adequate future security.

The strengths of saver psychology include financial security, low debt levels, retirement preparedness, and resilience during income fluctuations or economic downturns. Savers typically maintain emergency reserves, avoid lifestyle inflation, and achieve financial independence earlier than spenders with similar incomes. These strengths create objective financial stability and reduced money-related stress about future security, though they can reduce present life quality if taken to extremes.

The risks of saver psychology include missed life experiences, strained relationships due to perceived deprivation, and perpetual feelings of inadequacy despite objective abundance. Excessive saving might reflect anxiety rather than prudent planning, potentially indicating need for addressing underlying security fears. The challenge for savers involves maintaining security priority while developing capacity for present enjoyment and strategic spending aligned with values and life goals.

Balance between spending and enjoyment requires acknowledging that both present experiences and future security contribute to life satisfaction. Individuals can implement automated savings that run in the background while spending remaining funds with less guilt. Creating specific categories for guilt-free spending and non-negotiable savings helps both personalities honor competing needs. The goal is conscious allocation that serves both present and future rather than unconscious dominance of either extreme.

Budget Nerd vs Free Spirit: How Personality Affects Money Management

Budget nerd psychology emphasizes control, structure, detailed tracking, and optimization in financial management. Individuals with this orientation find satisfaction in understanding exactly where money goes, creating detailed budget categories, optimizing tax strategies, and maximizing efficiency in financial systems. The emotional reward comes from the sense of control and predictability that detailed financial planning provides, reducing anxiety through clear understanding of financial status and projections.

Free spirit psychology values flexibility, spontaneity, and freedom from financial constraints or detailed tracking. Free spirits experience detailed budgeting as restrictive and anxiety-producing rather than comforting. They prefer simplified financial approaches, general awareness over detailed tracking, and flexibility to adjust spending based on changing circumstances and opportunities. The emotional reward comes from feeling unconstrained and able to respond spontaneously to life without constant reference to predetermined categories and limits.

Control-oriented behavior in budget nerds manifests as preference for detailed planning, regular financial reviews, optimization strategies, and discomfort with ambiguity or unplanned spending. This orientation serves individuals well in achieving financial goals that require sustained discipline and long-term planning. The challenge arises when excessive control creates anxiety, reduces spontaneity, or causes relationship friction with partners who experience detailed tracking as controlling or distrustful.

Freedom-oriented behavior in free spirits manifests as resistance to detailed tracking, preference for general awareness, and flexibility in resource allocation. This orientation supports adaptability, reduces financial anxiety for those who find detailed planning stressful, and allows spontaneous opportunities. The challenge arises when lack of structure prevents achieving long-term goals that require consistent behavior, or when spending unconsciously exceeds income without awareness until problems emerge.

Conflict in couples often reflects budget nerd versus free spirit differences rather than disagreement about financial goals. The budget nerd experiences the free spirit’s approach as irresponsible and anxiety-producing, threatening financial security through lack of structure. The free spirit experiences the budget nerd’s approach as controlling and restrictive, reducing quality of life through excessive limitation. Without recognizing these as personality differences rather than value conflicts, couples can spiral into repeated unproductive arguments.

Designing financial systems for both personality types requires honoring legitimate needs while establishing minimum necessary structure. Automated savings and bill payments provide security that budget nerds need while reducing detailed involvement that free spirits resist. Simplified budget categories replace detailed tracking—perhaps three to five major categories instead of twenty detailed ones. Establishing “no questions asked” spending amounts for each partner prevents feeling controlled while maintaining overall financial discipline. Regular but not excessive financial check-ins provide accountability without constant monitoring.

Safety-Driven vs Status-Driven Financial Motivation

Safety-driven financial motivation prioritizes security, stability, and protection against future uncertainty over consumption, status, or visible wealth display. Individuals with safety-driven psychology allocate resources toward emergency funds, insurance, debt reduction, and conservative investments that preserve capital. The emotional driver is anxiety reduction through building financial buffers against job loss, health emergencies, market downturns, or other threats to financial stability.

Status-driven financial motivation prioritizes visible consumption, lifestyle signaling, and maintaining or advancing social position through spending patterns. Status-driven individuals allocate disproportionate resources toward items visible to others—vehicles, homes, clothing, experiences—that communicate success or belonging to desired social groups. The emotional driver is social acceptance, admiration, or competitive positioning relative to peer groups and reference populations.

Security-seeking behavior manifests in high savings rates, risk-averse investment approaches, preference for stable employment over higher-risk career moves, and discomfort with debt even at low interest rates. Safety-driven individuals often continue conservative financial behavior long after achieving objective financial security, driven by deep-seated need for protection against perceived threats. This pattern serves well for building wealth and weathering economic downturns but can limit growth opportunities or prevent enjoying accumulated resources.

Status-driven behavior manifests in lifestyle inflation that matches or exceeds income growth, preference for premium brands and visible consumption, and financial stress despite high income due to high spending. Status-driven individuals often carry debt to maintain desired lifestyle, prioritize consumption over savings, and experience anxiety around social comparison. This pattern can provide legitimate emotional benefits from social connection and identity expression but frequently undermines long-term financial security.

The difference between “looking rich” versus “being wealthy” reflects status versus security orientation. Looking rich requires high visible consumption that depletes resources on depreciating assets and experiences. Being wealthy requires accumulation of productive assets that compound over time, often while maintaining modest lifestyle that appears less impressive to observers. Research on millionaires demonstrates that most accumulated wealth through high savings rates and modest living rather than high income and impressive consumption.

Status-driven spending often operates unconsciously through social comparison and conformity pressure. Individuals might not recognize they’re making financial decisions based on peer spending patterns or perceived social expectations rather than personal values. Increasing awareness of this driver allows more intentional choice about which status signals align with genuine values versus social pressure. Some status spending serves legitimate identity and connection needs; the goal is conscious allocation rather than unconscious social conformity that undermines financial security.

How Money Psychology Affects Daily Financial Decisions

Money psychology affects daily financial decisions more powerfully than occasional major choices because small behaviors compound over time to determine financial outcomes. Daily spending on coffee, meals, subscriptions, convenience purchases, and impulse items accumulates to thousands or tens of thousands annually. These micro-decisions operate largely automatically, driven by habits, emotional states, and environmental cues rather than conscious deliberation. Understanding the psychological drivers of daily choices allows individuals to design better decision environments and default behaviors.

Daily decisions are psychology-driven because they occur too frequently for conscious analysis. The brain conserves cognitive resources by automating recurring choices through habit formation. These habits develop based on emotional associations—if purchasing coffee provides morning comfort, the behavior becomes automatic without weighing costs versus alternatives. If stress triggers food delivery ordering, the pattern repeats whenever similar emotional states arise. Changing daily financial outcomes requires addressing these psychological patterns rather than attempting constant willpower.

Small behaviors compound over time through consistency of direction rather than magnitude of individual choices. The difference between spending four versus five dollars daily appears trivial in individual instances but represents $365 annually. Across decades, this pattern either creates or destroys thousands in accumulated wealth through different spending, saving, and investing trajectories. Compound interest magnifies these differences—money not spent can grow through investment returns over years and decades.

Awareness of money psychology leads to better outcomes and long-term wealth building by enabling intentional design of financial systems and environments. Individuals who recognize their specific triggers—emotional states, environmental cues, time of day patterns—can implement targeted interventions. Someone who stress-spends in evenings might establish evening routines that don’t involve shopping. Someone who overspends on convenience during busy periods might batch meal preparation during free time. Awareness converts unconscious reactions into conscious choices.

Long-term wealth building depends more on consistent behavior across thousands of small decisions than optimal investment strategy or sophisticated financial tactics. An individual with modest investment returns but consistent savings behavior typically achieves better outcomes than someone with superior investment knowledge but inconsistent implementation. Money psychology determines this consistency by shaping whether individuals maintain beneficial behaviors through market volatility, life changes, and competing priorities that test commitment to long-term financial goals.

How Money Acts as a Behavioral Amplifier

Money acts as a behavioral amplifier by magnifying existing personality traits and tendencies rather than fundamentally changing character. Individuals who exhibit generosity with limited resources tend to become more generous with wealth, while those inclined toward selfishness often become more so. Disciplined individuals typically maintain or increase discipline with higher income, while impulsive personalities often experience greater impulsivity. This amplification effect explains why increased income alone rarely solves financial problems rooted in behavioral patterns.

Income increases often reveal character through how individuals allocate additional resources. Some direct windfalls or raises toward long-term goals, debt reduction, or charitable giving. Others immediately increase lifestyle consumption to match new income levels, a pattern called lifestyle inflation that prevents wealth accumulation despite income growth. These different responses reflect underlying values, priorities, and self-regulation capacity that money amplifies rather than creates.

The psychological principle underlying behavioral amplification is that money removes constraints that previously limited expression of natural tendencies. Limited income forces everyone to exercise some spending restraint regardless of personality. As income increases, this external constraint weakens, allowing internal psychological patterns to determine behavior. Individuals with strong intrinsic values and self-regulation maintain chosen behaviors independent of resource availability. Those who relied primarily on external constraints face difficulty when constraints relax.

Greed, discipline, impulsiveness, and generosity all magnify with increased financial resources. Greedy individuals with limited means might obsess over small amounts but avoid extreme behaviors due to resource constraints. With wealth, this tendency can escalate to unethical or illegal behavior in pursuit of still more resources. Impulsive individuals make larger consequential mistakes when resources allow. Generous individuals increase positive impact through larger contributions, while disciplined individuals build greater wealth through consistent behavior amplified by larger resource base.

Income alone does not change character because personality traits, values, and psychological patterns form through childhood experiences, neurological predispositions, and years of habitual behavior. Money provides a tool that reflects and amplifies these existing patterns. Lasting positive change requires addressing underlying psychology—values clarification, habit modification, emotional regulation improvement—rather than assuming that financial success or income growth will automatically improve financial behavior or life satisfaction.

Why Budgeting Is a Psychological Tool, Not Just a Financial One

Budgeting functions as a psychological tool by providing emotional clarity, sense of control, and reduced anxiety about financial uncertainty beyond its purely mathematical function of tracking income and expenses. The process of creating a budget forces explicit acknowledgment of resource limits, priority trade-offs, and alignment between spending and stated values. This awareness itself reduces anxiety even before behavior changes, because uncertainty about financial status often creates more stress than the actual situation once clearly understood.

Budget as emotional clarity tool means the primary value comes from understanding money flow, identifying spending patterns, and recognizing gaps between intended and actual resource allocation. Many individuals feel surprised when first tracking spending systematically, discovering that small frequent purchases add up differently than estimated or that certain categories consume disproportionate resources. This clarity enables informed choice about whether current patterns align with priorities or require adjustment.

Control and predictability represent core psychological benefits of budgeting that explain why some individuals find detailed tracking comforting while others find it stressful. For those with high need for control or significant financial anxiety, budgets provide reassuring structure and ability to project future financial status. This reduces amorphous worry into concrete plans and challenges. For those who value spontaneity or find constraint stressful, simplified budgeting approaches that provide accountability without excessive detail better serve psychological needs.

Reduced anxiety from budgeting occurs through multiple mechanisms. Budgets clarify that resources either do or do not exist for specific purposes, eliminating ambiguity. They provide permission to spend in planned categories without guilt, knowing savings and obligations are handled. They reveal problems early when corrective action is easier rather than allowing escalation until crisis forces recognition. They demonstrate that individuals can manage money responsibly, building self-efficacy and confidence.

Identity-based budgeting links financial actions to self-image and personal values rather than relying solely on willpower or external tracking. When individuals develop identity as “someone who lives below their means” or “a person who prioritizes experiences over possessions,” spending decisions align with this identity naturally. Creating budgets based on values—allocating most resources to highest priorities—builds this identity connection. Categories labeled by purpose (adventure fund, family experiences, financial freedom) engage values more effectively than generic categories (entertainment, miscellaneous).

How Awareness of Money Psychology Improves Long-Term Wealth Building

Awareness of money psychology improves long-term wealth building by shifting focus from tactics to sustainable behavior patterns that compound over decades. Many individuals chase optimal investment strategies, tax minimization techniques, or sophisticated financial products while neglecting the behavioral consistency that determines actual outcomes. Understanding psychological patterns enables designing systems that work reliably across varying market conditions, life circumstances, and emotional states rather than requiring constant willpower.

Consistency beats optimization in long-term wealth building because maintaining a moderately effective strategy through complete market cycles outperforms sophisticated approaches abandoned during volatility. An individual who continues systematic investing through bear markets, even in simple index funds, typically achieves better results than someone pursuing optimal timing and security selection but stopping contributions or panic selling during downturns. Behavioral consistency creates the time in market that drives compound growth.

Behavior-focused strategies prioritize reliable execution over theoretical superiority. Automated savings and investment contributions continue regardless of motivation or market conditions. Simplified investment approaches reduce decision paralysis and abandonment risk. Moderate targets that feel sustainable maintain consistency better than aggressive goals that create deprivation and eventual rebellion. These behavior-focused strategies acknowledge psychological reality rather than assuming perfect rational execution of mathematically optimal plans.

Long-term habit alignment techniques focus on creating sustainable patterns that become automatic rather than requiring ongoing conscious effort. Starting with small achievable behaviors builds self-efficacy and momentum. Linking new financial habits to existing routines leverages established neural pathways. Creating environmental supports—removing saved payment information, implementing waiting periods for purchases, using separate accounts for different purposes—reduces reliance on willpower. Tracking progress builds awareness and reinforcement without creating excessive constraint.

Wealth building psychology recognizes that financial success requires sustained behavior across decades, through job changes, relationship changes, market cycles, and evolving life priorities. Systems that worked during career building might need adjustment in retirement. Behaviors appropriate for high income might require modification during income disruption. Psychological awareness enables recognizing when circumstances warrant strategy adjustment versus when emotional discomfort reflects normal volatility that requires maintaining established approaches despite temporary psychological difficulty.

How to Improve Your Money Psychology (Action-Oriented)

Improving money psychology requires transitioning from awareness to action through systematic behavior change rather than pursuing perfection or radical transformation. Understanding psychological patterns provides necessary foundation, but change occurs through implementing specific practices that gradually reshape automatic responses to money situations. Focusing on progress rather than perfection prevents the all-or-nothing thinking that causes many people to abandon improvement efforts after inevitable setbacks.

The transition from awareness to action begins with identifying specific behaviors to modify rather than attempting comprehensive psychological overhaul. Choose one or two high-impact patterns to address first—perhaps emotional spending triggered by stress, or avoidance of necessary financial planning. Success with focused change builds confidence and momentum for addressing additional patterns. Attempting to change too many behaviors simultaneously often results in changing none, as limited self-regulation resources become overwhelmed.

Behavior change rather than perfection represents the realistic goal for improving money psychology. Individuals will continue experiencing emotional responses to money, facing cognitive biases, and sometimes making impulsive choices. The goal is reducing frequency and magnitude of problematic patterns while increasing beneficial behaviors, not achieving perfect rational financial decision-making. This realistic framing prevents discouragement when setbacks occur and maintains focus on overall trajectory rather than individual decisions.

Sustainable improvement requires matching strategies to individual personality, circumstances, and specific psychological patterns rather than following generic advice. Spending trackers help some individuals but trigger anxiety in others. Detailed budgets serve analytical personalities while overwhelming those preferring simplicity. High savings rates suit those with security focus but create resentment in present-oriented individuals. Effective improvement involves experimenting to discover which specific techniques work for individual psychology.

Action-oriented improvement acknowledges that insight alone rarely changes behavior—implementation systems determine outcomes. Reading about money psychology provides understanding, but improvement requires applying specific techniques consistently over time. This means scheduling regular financial reviews, implementing automated systems, establishing accountability mechanisms, and tracking progress. The gap between knowing and doing closes through structured action rather than additional information or understanding.

Identifying Your Money Triggers and Emotional Patterns

Identifying money triggers and emotional patterns requires systematic tracking of spending decisions alongside emotional states, situations, and thought patterns that preceded purchases. Effective tracking captures not just amounts and categories but contextual factors—time of day, emotional state, social situation, preceding events—that reveal psychological patterns invisible in standard budget spreadsheets. This detailed awareness enables recognizing specific triggers that drive unplanned spending or financial avoidance.

Track emotional spending by maintaining a simple journal for several weeks noting purchases and emotional states. Record what you felt immediately before spending—stressed, bored, excited, sad, celebratory. Note whether purchases were planned or impulsive. Identify patterns across multiple instances—perhaps stress consistently triggers food delivery orders, or boredom leads to online browsing and purchases. These patterns reveal which emotions drive spending behavior and which situations create vulnerability to impulsive choices.

Recognize fear and stress signals that trigger specific money behaviors beyond spending. Fear might manifest as checking accounts obsessively or avoiding reviewing financial status entirely. Stress might cause delay of important financial decisions or rushed poorly-considered choices. Anxiety might drive excessive saving despite adequate reserves or paralysis around investing decisions. Identifying these stress responses enables developing alternative coping mechanisms that don’t undermine financial goals.

Self-audit exercises help systematize the identification process. Review three months of spending and categorize each purchase as planned versus impulsive, need versus want, aligned with values versus social pressure or emotional trigger. Calculate what percentage of spending falls into each category. Identify your five largest spending categories and evaluate whether they reflect stated priorities. List emotional states or situations when you’re most likely to overspend or avoid necessary financial tasks. This comprehensive assessment reveals patterns requiring attention.

Common triggers to investigate include specific emotional states (stress, boredom, sadness, excitement), social situations (peer spending, social comparison, keeping up appearances), time patterns (evening, weekend, end of month), environmental cues (sales notifications, targeted advertising, passing certain stores), and relationship dynamics (conflict, celebration, gift-giving pressure). Understanding personal trigger inventory enables designing targeted interventions that address specific vulnerabilities rather than relying on general willpower.

Reframing Limiting Beliefs About Money

Reframing limiting beliefs about money begins with identifying common patterns that constrain financial behavior and outcomes. Limiting beliefs include “I’m bad with money,” “rich people are greedy,” “I don’t deserve financial success,” “money isn’t important,” or “I’ll never get ahead financially.” These beliefs operate as self-fulfilling prophecies by justifying behavior that confirms the belief, creating cycles that perpetuate financial struggles despite opportunities for improvement.

Identify limiting beliefs through self-reflection about money attitudes, reactions to others’ financial success, automatic thoughts during financial decisions, and childhood money messages that still influence behavior. Writing money autobiography—narrative about earliest money memories, family financial dynamics, formative experiences—often surfaces beliefs operating unconsciously. Notice defensive reactions or strong emotions around money topics, as these often signal underlying beliefs worth examining.

Challenge limiting beliefs by examining evidence and considering alternative interpretations. The belief “I’m bad with money” might actually mean “I haven’t learned effective money management skills yet” or “my current approach doesn’t match my personality.” “Rich people are greedy” might reflect specific negative examples while ignoring generous wealthy individuals. “I don’t deserve financial success” likely stems from childhood messages or experiences rather than objective reality about worthiness.

Replace limiting beliefs with positive, empowering narratives grounded in reality and possibility rather than toxic positivity. “I’m developing better money management skills through learning and practice” acknowledges current challenges while affirming capacity for growth. “Money is a tool I can use for values I care about” reframes money as neutral instrument rather than inherently positive or negative. “I deserve financial security as much as anyone” affirms basic worthiness without requiring superiority claims.

Identity and language shifts support belief changes by influencing how individuals view themselves and their financial capabilities. Shift from “I can’t afford it” to “that’s not a priority right now” changes the frame from scarcity to choice. Replace “I’m a spender” with “I’m learning to balance enjoyment and security” acknowledges tendency while asserting ability to change. Use “I choose to” instead of “I have to” around financial obligations to emphasize agency and reduce resentment.

Building Healthy Money Habits That Match Your Personality

Building healthy money habits requires using systems and environmental design rather than relying on willpower, which depletes under stress and competing demands. Sustainable habits work with personality tendencies and natural preferences instead of requiring constant resistance to inclinations. The goal is creating default behaviors that support financial goals automatically, reducing decisions that drain limited self-control resources.

Systems over willpower means structuring finances so beneficial behaviors happen automatically without requiring repeated conscious choices. Automated savings transfers eliminate the decision to save each month, converting it to default behavior requiring deliberate action to prevent. Automatic bill payments prevent late fees without requiring deadline tracking. Automated investment contributions continue through market volatility without requiring conviction during downturns. These systems recognize that willpower is finite and unreliable across varying circumstances.

Automation serves as the cornerstone of behavior-focused financial systems. Automate savings by setting up transfers scheduled immediately after paycheck deposits, treating savings as first expense rather than residual. Automate debt payments above minimums to accelerate progress without monthly willpower requirements. Automate investment contributions to retirement and taxable accounts at sustainable levels that continue through market cycles. The initial setup effort pays ongoing dividends through reliable execution.

Rules and guardrails provide structure for individuals who need some flexibility but benefit from clear boundaries. Establish waiting periods for purchases above specific thresholds—perhaps 24 hours for purchases over $100, one week for purchases over $500. Create spending rules tied to specific triggers—windfalls get split 50/50 between savings and discretionary spending. Set category budgets with alerts but not hard stops for those who resist rigid constraints. These rules provide accountability while maintaining some freedom.

Sustainable behavior design acknowledges that overly restrictive approaches often backfire through eventual rebellion or abandonment. Build “release valves” into financial systems—budget categories for guilt-free spending, planned splurges that prevent feeling deprived, periodic review points to adjust systems as needed. Match savings rates and investment approaches to personality—aggressive targets for those energized by challenge, modest targets for those who need wins to maintain motivation. Sustainability matters more than short-term optimization.

Personality-matched strategies recognize that identical financial advice fails different personalities. Spenders benefit from automating savings then freely spending remainder without guilt. Savers benefit from creating permission for enjoyment spending and releasing excessive hoarding. Detail-oriented individuals excel with comprehensive tracking and optimization. Big-picture thinkers prefer simplified categories and automated systems. Match the system to the individual rather than forcing everyone into identical approaches that work well for some personalities but create stress and failure for others.

Money Psychology in Relationships and Family Finances

Money psychology in relationships and family finances reveals that most money conflict is psychological rather than numerical. Couples with ample income might fight constantly about spending while lower-income couples living within means maintain financial harmony. The source of conflict lies in different money scripts—learned beliefs and emotional associations about money—and personality differences in spending, saving, control needs, and risk tolerance rather than resource scarcity.

Different money scripts reflect divergent childhood experiences, family messages, and emotional associations that create incompatible assumptions about “normal” or “right” money behavior. One partner might view spending on experiences as wasteful while the other sees it as essential to quality of life. One might feel security requires significant cash reserves while the other considers uninvested cash a wasted opportunity. Neither perspective is objectively correct; conflict arises from treating personal preferences as universal truths.

Family dynamics affect financial outcomes through accumulated small decisions and emotional patterns that compound over years. Couples who avoid financial discussions due to conflict never develop shared goals or collaborative approaches. Families where one partner controls all decisions build resentment and disengagement. Households where children observe constant money stress learn anxiety around finances regardless of actual resource levels. Understanding these psychological dynamics enables addressing root causes rather than surface symptoms.

Financial conflict without psychological understanding tends to recur in cycles—the same arguments repeat without resolution because partners address specific instances rather than underlying psychological differences. Understanding money psychology enables recognizing that the argument about a specific purchase actually reflects deeper differences in values, security needs, control preferences, or childhood experiences. This awareness shifts conversations from blame and defensiveness to problem-solving that addresses actual incompatibilities.

Successful financial management in relationships requires honoring legitimate psychological differences while establishing systems that serve shared goals. This means neither partner gets to unilaterally impose their money psychology on the other. Instead, collaborative systems respect both personalities while maintaining necessary accountability for joint financial health. The goal is solutions where both partners feel heard, respected, and able to express their money personality within reasonable constraints.

How Different Money Psychologies Cause Financial Conflict

Different money psychologies cause financial conflict when partners interpret identical situations through incompatible psychological frameworks without recognizing that both perspectives can be valid. A spender views the saver’s resistance to present enjoyment as miserliness or life avoidance. A saver views the spender’s consumption as irresponsibility or future risk. Both feel their position is obviously correct and the other’s clearly wrong, creating cycles of judgment and defensiveness.

Saver versus spender tension represents the most common money psychology conflict in relationships. Savers feel anxiety when reserves decline or present consumption increases. Spenders feel restricted and deprived when prevented from enjoying current resources. Neither position is objectively superior—both present and future matter, requiring balance. Conflict escalates when each partner tries to convert the other rather than finding middle ground honoring both perspectives.

Control versus freedom tension reflects different psychological needs around structure, predictability, and autonomy. Control-oriented partners need detailed tracking, clear systems, and predictability to feel secure. Freedom-oriented partners experience detailed tracking as controlling and restrictive, needing flexibility and autonomy to feel comfortable. Arguments about budgeting often reflect this deeper psychological difference rather than disagreement about the importance of financial responsibility.

Misaligned values in households or couples create conflict when partners prioritize different categories or goals. One might value experiences and travel while the other prioritizes home ownership or career investment. One might prioritize charitable giving while the other focuses on family security. These value differences are legitimate, but without explicit discussion and compromise, each partner’s spending in their priority area feels wasteful to the other.

Risk tolerance differences create particularly intense conflict because they involve fear—one partner genuinely feels threatened by what the other views as reasonable choices. Conservative investors experience higher-risk portfolios as dangerous threats to security. Aggressive investors view conservative approaches as opportunity waste and failure to optimize. Both experience their position emotionally, not just intellectually, making compromise psychologically difficult without understanding the emotional drivers involved.

How Couples Can Align Money Goals Despite Different Personalities

Couples can align money goals despite different personalities by establishing communication frameworks that separate goal-setting from implementation tactics. Partners might share goals—retirement security, travel experiences, debt freedom—while differing in psychological approach to achieving them. This distinction allows collaborative goal development while honoring personality differences in execution preferences. The key is distinguishing shared destinations from individual paths.